Credit Intermediation Market Size 2024-2028

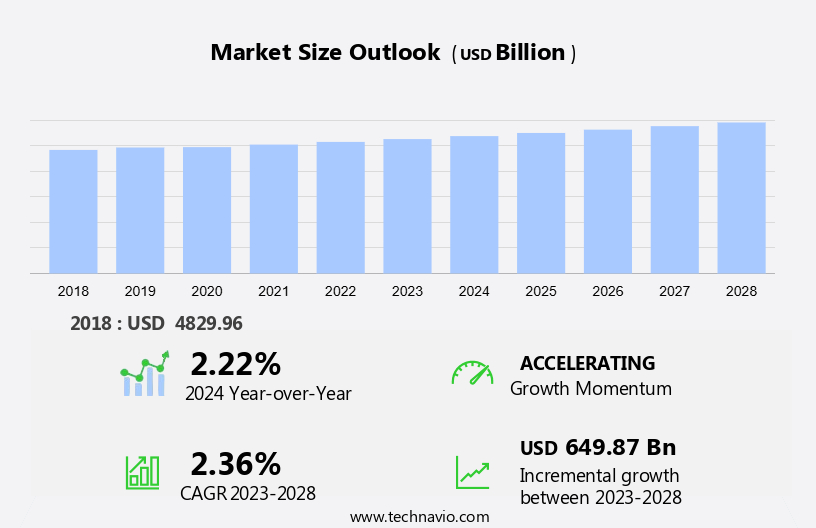

The credit intermediation market size is forecast to increase by USD 649.87 billion at a CAGR of 2.36% between 2023 and 2028. The market is experiencing significant developments and challenges, driven by various factors. One key trend is the increasing preference for discounted monthly installment plans, which allow consumers to access credit more affordable. However, this trend is not without risks, particularly during economic recessions when global economies face instability and credit availability becomes scarce. Banks, as primary credit intermediaries, are facing growing vulnerabilities and deficiencies, necessitating the development of an active secondary credit market to ensure smooth intermediation. This market growth is essential for maintaining financial stability and facilitating economic growth. Effective financialization and a strong secondary credit market can help mitigate risks and ensure credit availability to consumers and businesses, even during challenging economic conditions.

What will be the Size of the Market During the Forecast Period?

Credit intermediation is a vital process in the financial market that facilitates the connection between borrowers and lenders. This process involves credit intermediaries, such as commercial banks and credit unions, acting as middlemen in the lending process. These institutions offer various credit products to individuals and entities, enabling them to access funds for personal or business purposes. The market plays a crucial role in the economy by making credit available to consumers and businesses. Credit agreements are legally binding contracts between the borrower and the lender, outlining the terms and conditions of the loan, including monthly installments, discounts, and refunds.

Moreover, the infrastructure required to support credit intermediation includes a strong workforce, advanced technology, and adherence to stringent money security regulations. Operating costs for credit intermediaries can be substantial due to the need for maintaining infrastructure, safeguarding investors, and managing market risk. One of the primary responsibilities of credit intermediaries is to assess the financial status of potential borrowers and ensure the mishandling of credit agreements is minimized. This process involves evaluating the borrower's ability to repay the loan and assessing the risk associated with the loan. Fraud prevention is also a significant concern, with credit intermediaries implementing measures to protect against fraudulent activities by both borrowers and enterprises.

Furthermore, the financial services industry is undergoing significant financial services innovation driven by the rise of digital banking and the growing adoption of financial technology (fintech). Digital financial services are transforming the landscape, with mobile banking, mobile payments, and digital lending playing a key role in promoting financial inclusion. As financial inclusion programs expand, innovative solutions like microfinance, peer-to-peer lending, and data-driven lending are empowering underserved communities. Financial inclusion strategies are further enhanced by financial literacy initiatives and financial education efforts, while sustainable finance and responsible lending practices ensure long-term stability. With an increasing focus on financial crime prevention, cybersecurity in finance, and compliance and risk, financial services regulation continues to adapt to new challenges. Financial technology trends and financial services transformation will drive future growth, ensuring greater financial well-being and financial security for consumers worldwide.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Individual

- Enterprise

- Type

- Tied credit intermediation

- Ancillary credit intermediation

- Non-tied credit intermediation

- Geography

- North America

- US

- APAC

- China

- India

- Japan

- Europe

- Germany

- Middle East and Africa

- South America

- North America

By Application Insights

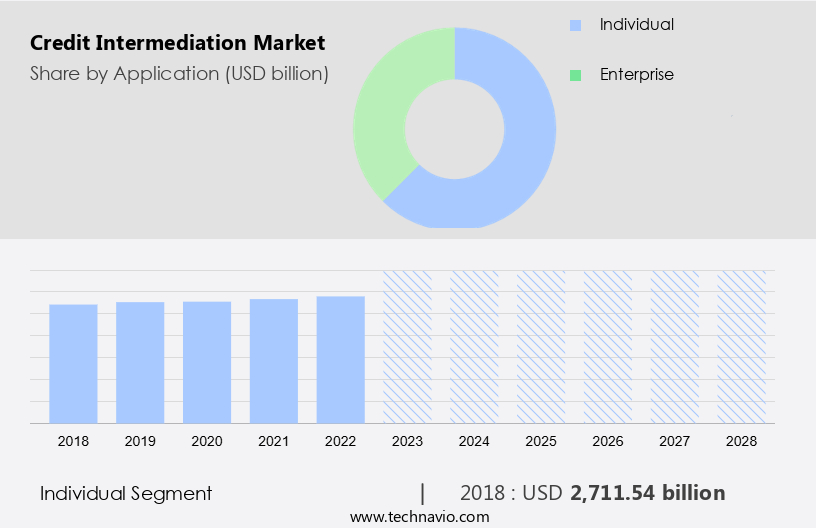

The individual segment is estimated to witness significant growth during the forecast period. The individual sector holds a significant market share in the market and is anticipated to lead the market growth during the forecast period. This segment's expansion can be attributed to the rising preference for personalized credit agreements and the growing role of intermediaries as credit advisors. The demand for credit counseling services has grown due to economic challenges, including increasing interest rates and inflation, which make it difficult for individuals to manage their debts. According to the US Bureau of Labor Statistics, employment in the credit counseling sector is projected to grow by 9% between 2021 and 2031. Middlemen play a crucial role in the lending process by connecting individuals with potential lenders and facilitating credit agreements. These entities provide valuable services, including credit education, debt management, and financial planning, making them indispensable in today's complex financial landscape.

Get a glance at the market share of various segments Request Free Sample

The individual segment was valued at USD 2,711.54 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

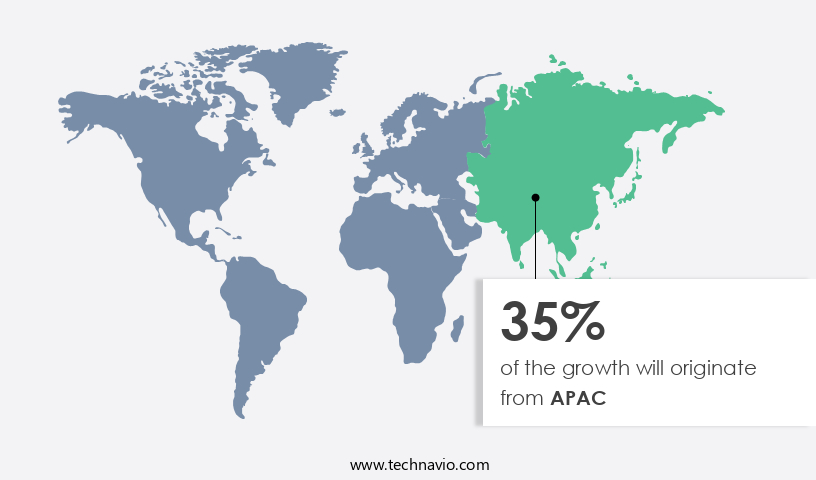

APAC is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American market is experiencing significant growth due to the increasing number of small and medium enterprises (SMEs) in the region. With over 30 million SMEs in the US alone, as reported by the US Chamber of Commerce, there is a growing demand for credit intermediation services. These businesses often require credit lending to finance their operations and expand, making the market a vital component of the financial landscape. Credit intermediation plays a crucial role in safeguarding investors by connecting borrowers with potential lenders. The market's growth is driven by the presence of numerous established companies in North America.

Moreover, the financial status of businesses and individuals seeking credit is a primary concern for these companies, ensuring that only credible borrowers gain access to funds. Fraudulent enterprises pose a significant risk to the security of investors' money. Stringent money security regulations are in place to mitigate this risk, providing an added layer of protection for both borrowers and lenders. The market in North America is committed to adhering to these regulations, ensuring a secure and reliable environment for all market participants. In conclusion, the North American market is thriving due to the increasing number of SMEs, the need for credit lending, and the presence of reputable companies. The market's role in connecting borrowers with lenders while maintaining strict regulatory compliance makes it an essential part of the financial sector.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growing focus on effective financialization is the key driver of the market. The market in the United States is experiencing significant expansion due to the increasing emphasis on efficient financialization. Financial institutions are expanding their reach and offering banking services through various channels, enabling them to provide last-mile connectivity.

Furthermore, the emergence of non-bank credit intermediaries and their commitment to broadening financial access and loosening credit restrictions have significantly contributed to market growth. Innovations such as door-step banking and banking correspondents have also fueled the demand for credit intermediation. Effective financialization remains a priority, and this focus is expected to propel the growth of the US market throughout the forecast period.

Market Trends

The development of an active secondary credit sector ensuring smooth credit intermediation is the upcoming trend in the market. In the financial sector, the importance of facilitating seamless credit flow and its intermediation is increasingly recognized. For instance, the Reserve Bank of India established a Secondary Loan Market Association in 2020 to bring together financial institutions and non-banking financial companies. The primary objective of this platform is to promote a vibrant secondary credit market, thereby ensuring efficient credit intermediation. Through a market-based auction mechanism, the platform enables fair pricing for credit transfers between members.

Moreover, this approach contrasts with traditional bilateral arrangements, providing greater transparency and fairness in credit and credit risk among participants. By fostering a deep and active secondary credit market, the platform plays a crucial role in enhancing the overall credit ecosystem's efficiency and effectiveness. The Secondary Loan Market Association, launched by the Reserve Bank of India in 2020, plays a pivotal role in addressing the challenges of ensuring smooth credit flow and its intermediation. This platform brings together financial institutions and non-banking financial companies, fostering a deep and active secondary credit market. By employing a market-based auction mechanism, the platform guarantees fair pricing for credit transfers, ensuring transparency and fairness in credit and credit risk among participants. Such factors wll increase the market trends and analysis during the forecast period.

Market Challenge

Growing vulnerabilities and deficiencies in banks related to credit intermediaries are key challenges affecting the market growth. The non-bank financial intermediary (NBFI) sector plays a significant role in credit intermediation services, creating intricate connections between banks and NBFIs through various channels. However, the expansion of NBFI exposures comes with inherent risks, as the sector's opaque nature and swift evolution of risks can pose challenges to banks' risk management practices. Recent events, such as the collapse of Archegos Capital Management and stresses in government bond markets, have underscored the need for improved risk management in the NBFI sector.

Furthermore, the types and sizes of NBFI exposures vary across jurisdictions, potentially leading to financial instability concerns. As the global economy navigates economic downturns, such as recessions, the importance of effective credit risk management becomes increasingly crucial for maintaining financial stability. In this context, banks must remain vigilant and adapt to the evolving risks in the NBFI sector to ensure the security of their investments and the broader financial system.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Bank of America Corp. - The company offers credit intermediation services such as personal loans, and mortgage lending.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Barclays PLC

- Citigroup Inc.

- Credit Suisse Group AG

- Deutsche Bank AG

- HSBC Holdings Plc

- JPMorgan Chase and Co.

- Morgan Stanley

- The Goldman Sachs Group Inc.

- Wells Fargo and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Credit intermediation is a vital process in the financial market where legal individuals and enterprises act as middlemen between lenders and borrowers. This involves the lending process, where credit agreements are formed between the parties, and consumers or entities receive the required credit. Commercial banks and credit unions are significant institutions in the market, offering various types of credit, including personalized agreements and advisory services. Operating costs, market risk, fraud, and infrastructure are crucial factors that influence the market. Lenders need to safeguard investors from fraudulent enterprises and ensure the mishandling of agreements does not occur. Money security regulations are essential to maintain cash liquidity and prevent a cash crisis.

In summary, borrowers face monthly installments, discounts, and refunds, which impact their financial status during a recession or global economies' downturn. Lenders assess the financial status of the borrower before approving credit, considering their ability to repay and the risk involved. Credit availability is a significant factor, as consumers and businesses rely on credit to manage their cash flow during challenging economic conditions. The market faces challenges such as fraud, infrastructure, workforce management, and regulatory compliance. However, it plays a vital role in facilitating economic growth by connecting lenders and borrowers, enabling businesses and individuals to access credit when needed.

Moreover, the fintech revolution is reshaping the financial services landscape, with technological advancements like AI and big data driving improvements in credit decisions, credit assessment, and credit underwriting processes. Online lending platforms and bank intermediation are increasingly providing personalized credit options to meet the consumption needs of underserved populations, offering more accessible financing needs and reducing loan default rates. However, predatory lending practices, frauds, and non-performing loans present significant business challenges for lending institutions. The rise of buy now, pay later (BNPL) services and pay later models highlights changing consumer behavior but also raises concerns over the regulatory landscape and loan terms. The shift towards personal investments and savers has increased credit demand, while economic uncertainty and housing affordability continue to impact mortgages and loan defaults. In response, credit services and financing options are evolving to ensure complete positive compliance, minimize operational costs, and adapt to the agreement process and maintenance of loans.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.36% |

|

Market growth 2024-2028 |

USD 649.87 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

2.22 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 35% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Bank of America Corp., Barclays PLC, Citigroup Inc., Credit Suisse Group AG, Deutsche Bank AG, HSBC Holdings Plc, JPMorgan Chase and Co., Morgan Stanley, The Goldman Sachs Group Inc., and Wells Fargo and Co. |

|

Market dynamics |

Parent market analysis and report , market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -