Crude Oil Desalter Market Size 2025-2029

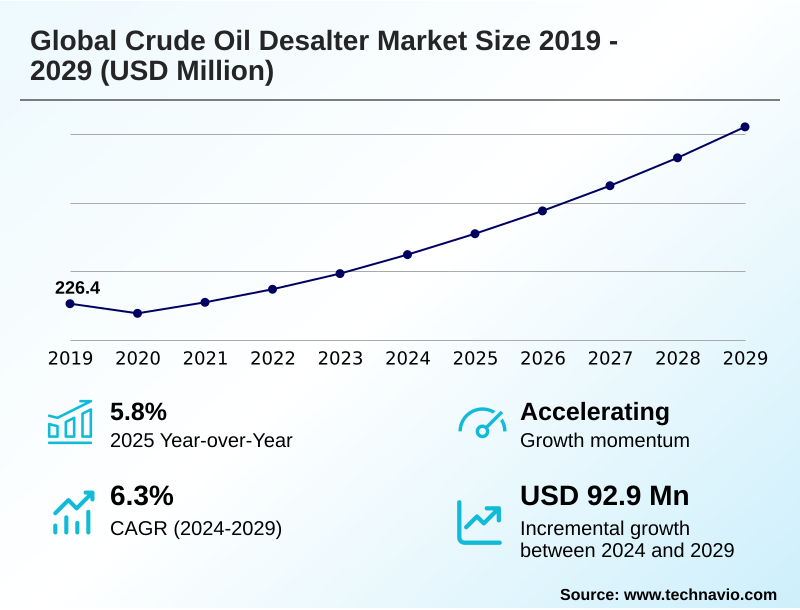

The crude oil desalter market size is valued to increase by USD 92.9 million, at a CAGR of 6.3% from 2024 to 2029. Processing heavier crude slates will drive the crude oil desalter market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 34% growth during the forecast period.

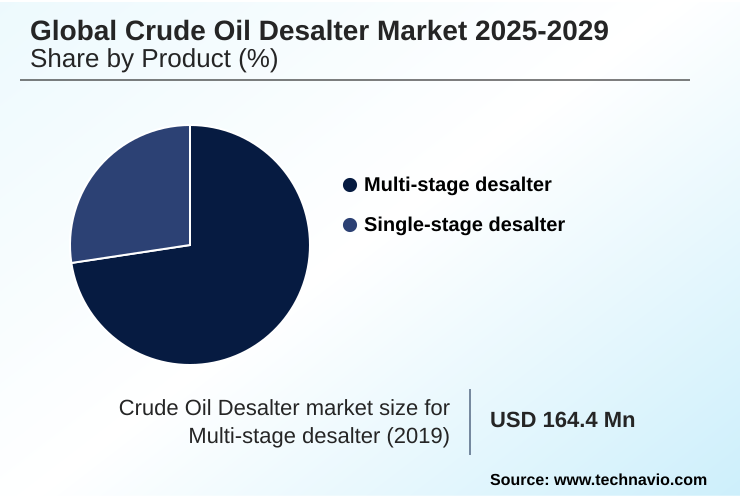

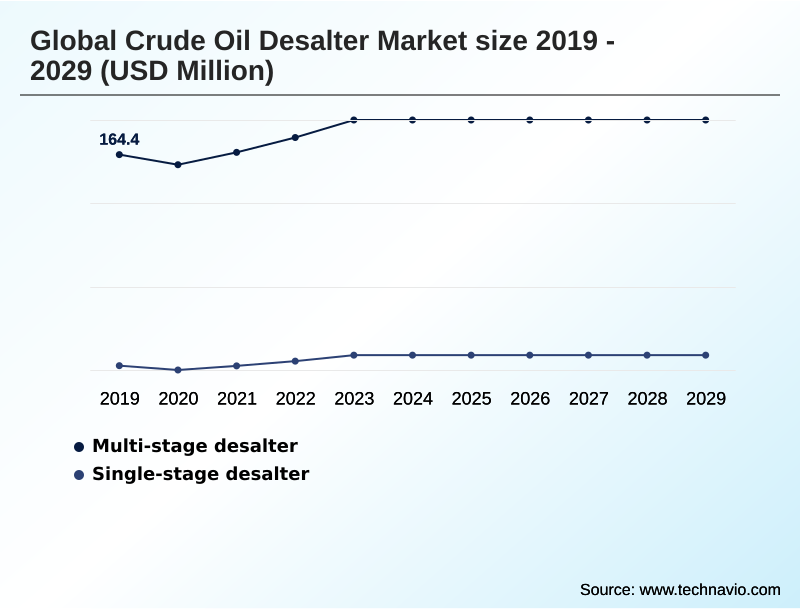

- By Product - Multi-stage desalter segment was valued at USD 181.2 million in 2023

- By Type - Electrostatic dehydrator segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 128.6 million

- Market Future Opportunities: USD 92.9 million

- CAGR from 2024 to 2029 : 6.3%

Market Summary

- The crude oil desalter market is shaped by the critical need for efficient crude oil pre-treatment to protect downstream refinery assets. The industry's shift toward heavy crude processing necessitates advanced solutions like multi-stage desalting and sophisticated electrostatic coalescence to manage challenging water-in-oil emulsions and prevent catalyst poisoning prevention.

- A key business scenario involves a refinery retrofitting its single-stage unit to a two-stage system to handle opportunity crudes; this investment in refinery modernization is justified by preventing costly downstream corrosion mitigation and heat exchanger fouling, thereby improving margins. Concurrently, trends like the adoption of compact desalter systems for offshore processing facilities are gaining traction.

- Innovations in process control systems and demulsifier chemical programs are pivotal for optimizing performance. However, the market faces challenges related to the high capital cost of turnkey modular packages and the technical complexities of asphaltene stabilization.

- Ultimately, the market evolves to balance economic incentives with operational reliability and environmental compliance, focusing on technologies that ensure efficient sediment and water removal and enable processing of diverse feedstocks, including those from crude-to-chemicals (COTC) operations.

What will be the Size of the Crude Oil Desalter Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Crude Oil Desalter Market Segmented?

The crude oil desalter industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Multi-stage desalter

- Single-stage desalter

- Type

- Electrostatic dehydrator

- Desalting process

- Application

- Refineries

- Oil and gas production

- Petrochemical plants

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- UK

- France

- Italy

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Product Insights

The multi-stage desalter segment is estimated to witness significant growth during the forecast period.

The multi-stage desalter segment is expanding, driven by the economic imperative for heavy crude processing. These systems employ sequential vessels for superior salt removal efficiency, which is critical for downstream corrosion mitigation.

Unlike single-stage units, multi-stage systems use a counter-current flow of crude and wash water, enabling a higher degree of purification and achieving up to 99% removal of corrosive salts.

This protects high-value downstream assets from accelerated heat exchanger fouling and catalyst poisoning prevention. The adoption of this technology is a direct response to the operational risks posed by opportunity crude processing, making it essential for refinery modernization.

This approach supports comprehensive asset integrity management and is vital for processing high salinity crude feedstocks.

The Multi-stage desalter segment was valued at USD 181.2 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

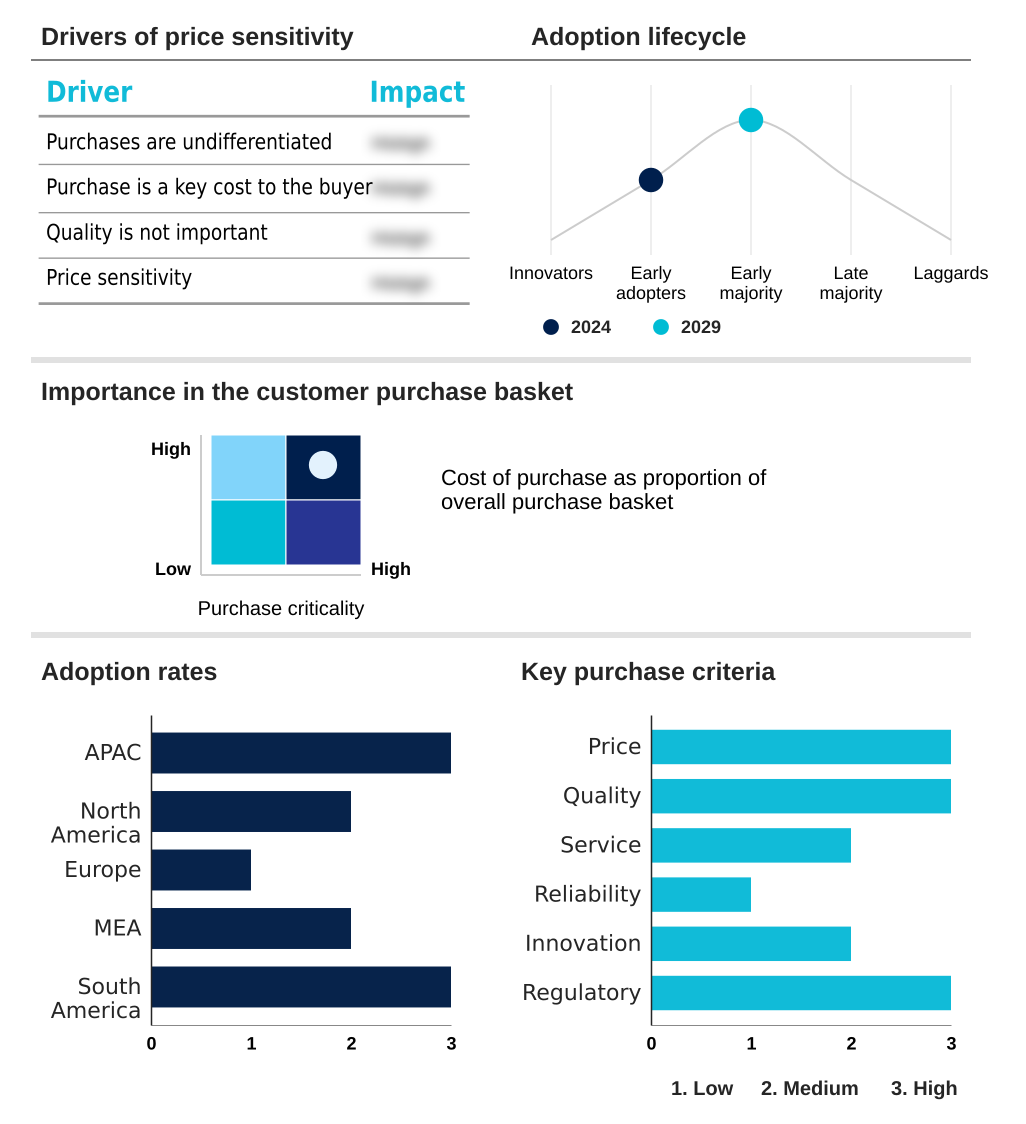

APAC is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Crude Oil Desalter Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is characterized by distinct regional dynamics. APAC is the primary growth engine, contributing over 34% of the incremental growth, fueled by new refinery construction in China and India focused on heavy crude processing.

These projects demand advanced multi-stage desalting and electrostatic dehydrator units. In contrast, North America and Europe are mature markets where the focus is on refinery modernization and brownfield retrofit projects.

Here, investments are driven by regulatory compliance tools and the need for operational expenditure reduction, with facilities achieving up to 15% lower energy use after upgrading to modern process control systems.

The Middle East is expanding its crude-to-chemicals (COTC) capacity, requiring high-performance crude oil pre-treatment and produced water treatment technologies to protect sensitive catalysts.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the crude oil desalter market hinges on a deep understanding of long-tail operational factors. The desalter performance for heavy crude is a primary concern, as is optimizing chemical usage in desalters to manage costs without compromising emulsion breaking.

- The total cost of desalter fouling, which can reduce heat transfer efficiency by over 25% compared to clean systems, is a critical metric driving investment in electrostatic grid design improvements and advanced desalting for opportunity crudes. For upstream operations, managing high water cut emulsions and preventing desalter electrical upsets are key to maintaining production.

- In refineries, the focus is on upgrading single-stage to multi-stage systems to improve reliability and achieve effective corrosion control in crude units. Key performance indicators include desalter wash water optimization and reducing desalter energy consumption. The salt content impact on catalysts remains a paramount concern, pushing innovation in desalter control system automation.

- For new projects, footprint reduction in modular desalters is vital for offshore platforms, while the ROI of desalter modernization must be clearly justified. The environmental impact of desalter effluent is driving demand for integrated desalter and water treatment solutions.

- Furthermore, specialized desalting technology for shale oil and predictive analytics for desalter maintenance are becoming standard requirements, with desalter design for offshore platforms demanding unique engineering solutions.

What are the key market drivers leading to the rise in the adoption of Crude Oil Desalter Industry?

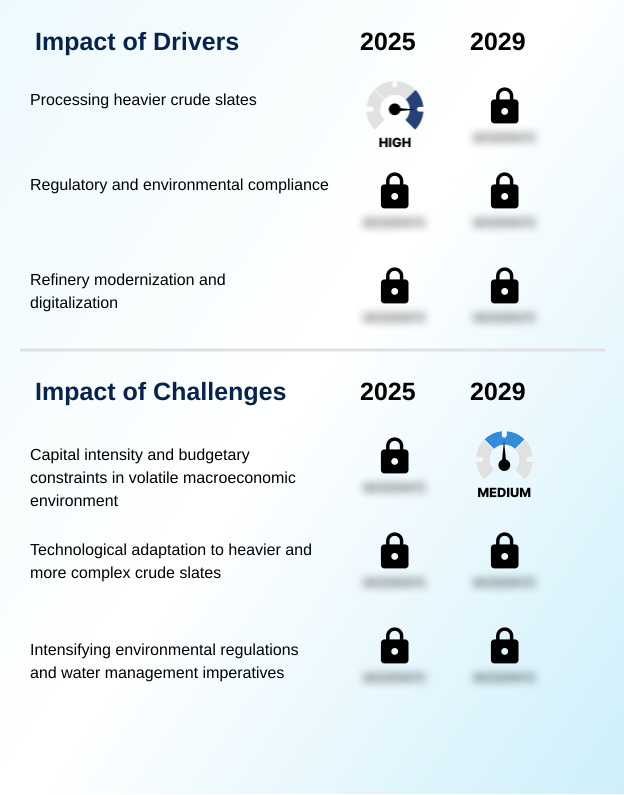

- The increasing necessity to process heavier and more contaminated crude slates stands as a primary driver for the market.

- Market growth is primarily propelled by the structural shift toward processing heavier, more challenging feedstocks. This necessity for heavy crude processing drives demand for advanced multi-stage desalting technologies capable of handling high salinity crude.

- Refineries processing such opportunity crudes can improve margins by over 5%, but only with robust crude oil pre-treatment to avoid catastrophic equipment failure.

- A second major driver is stringent regulatory pressure, compelling investment in high-performance regulatory compliance tools for effective downstream corrosion mitigation. Thirdly, the push for refinery modernization and operational expenditure reduction is accelerating the adoption of new technologies.

- Upgrading to advanced electrostatic coalescence systems can increase processing throughput by 10% without expanding footprint.

What are the market trends shaping the Crude Oil Desalter Industry?

- The integration of digitalization and advanced process control systems is emerging as a transformative market trend. This shift moves operations from traditional mechanical processes toward intelligent, data-driven optimization for enhanced efficiency.

- Key trends are reshaping the market, moving beyond basic separation to integrated, intelligent systems. The digitalization of operations, incorporating the industrial internet of things (IIoT) and advanced process control (APC), is a major focus, with some operators reporting a 15% reduction in unplanned downtime through predictive maintenance models.

- Another significant trend is the push toward sustainability, driving demand for advanced produced water treatment and zero-liquid discharge (ZLD) solutions to meet stricter wastewater effluent quality regulations. This focus on energy efficiency in refining has led to designs that improve heat integration.

- Additionally, the move toward modular engineering packages and compact desalter systems allows for faster deployment in brownfield retrofit projects and offshore processing facilities, reducing installation time by up to 30%.

What challenges does the Crude Oil Desalter Industry face during its growth?

- High capital intensity and budgetary constraints within a volatile macroeconomic environment present a significant challenge to industry growth.

- The market faces significant hurdles, led by the high capital cost of new systems, which often delays brownfield retrofit projects in volatile economic climates. A primary technical challenge is the continuous adaptation required for effective dehydration and desalting of increasingly complex feedstocks, such as those from bitumen desalting and heavy oil upgrading.

- Failure to manage difficult emulsions can lead to a 25% increase in maintenance costs for downstream units. Another major challenge is intensifying environmental regulation, which demands significant investment in hydrocarbon recovery systems and technologies to improve wastewater effluent quality.

- Meeting these standards adds to the total cost of ownership, making asset integrity management more complex while navigating the need for operational excellence.

Exclusive Technavio Analysis on Customer Landscape

The crude oil desalter market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the crude oil desalter market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Crude Oil Desalter Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, crude oil desalter market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agar Corp. - Key solutions focus on high-performance separation systems, engineered for optimized dehydration and effective salt removal to enhance crude oil quality and protect downstream assets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agar Corp.

- Alfa Laval AB

- AMR Process Inc.

- Axens Group

- Baker Hughes Co.

- Canadian Petroleum Processing Equipment Inc.

- Croda International Plc

- Desalters LLC

- EN-FAB Inc

- Forum Energy Technologies Inc.

- Frames Energy Systems BV

- GEA Group AG

- Komax Systems

- Mackenzie Hydrocarbons Australia Pty Ltd.

- McDermott International Ltd.

- Petro Techna International

- Schlumberger Ltd.

- TechnipFMC plc

- Veolia Environment SA

- VME Process Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Crude oil desalter market

- In August, 2024, PetroProcess Innovators announced a strategic partnership with Axiom Digital Solutions to develop a comprehensive digital twin for desalters, aiming to optimize chemical dosage and predict maintenance needs in real-time for heavy crude processing.

- In November, 2024, Separation Specialists Inc. acquired Emulsion-Break Technologies, a niche provider of advanced demulsifier chemical programs, to enhance its integrated solutions for upstream and refinery applications.

- In February, 2025, Modular Systems Co. launched its new compact desalter system, the 'Offshore Pro,' specifically designed for FPSO topside modules to reduce footprint and weight while maximizing water removal efficiency.

- In April, 2025, Eco-Refine Technologies received regulatory approval for its integrated zero-liquid discharge (ZLD) system, which combines multi-stage desalting with advanced produced water treatment to meet stringent new environmental standards for refinery wastewater effluent.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Crude Oil Desalter Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2025-2029 | USD 92.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.8% |

| Key countries | China, Japan, India, Australia, South Korea, Indonesia, US, Canada, Mexico, Russia, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The crude oil desalter market is fundamentally driven by the need to protect refinery assets through effective crude oil pre-treatment. The shift to heavy crude processing requires advanced technologies like multi-stage desalting and dual-frequency treaters for robust emulsion breaking and sediment and water removal.

- For boardroom decisions, the key consideration is balancing capital expenditure on turnkey modular packages against the long-term operational savings from downstream corrosion mitigation and catalyst poisoning prevention. A major trend is refinery modernization, where integrating advanced process control systems with electrostatic dehydrator units has demonstrated a reduction in chemical overuse by 20%.

- Technologies such as high-voltage electrostatic fields and sophisticated interface level control are standard. Compact desalter systems are becoming critical for offshore processing facilities and crude-to-chemicals (COTC) plants, which have zero tolerance for contaminants. The market's evolution is also shaped by the performance of demulsifier chemical programs in handling water-in-oil emulsions and mitigating issues like asphaltene stabilization and heat exchanger fouling.

- Efficient produced water treatment is now a key part of any desalter solution.

What are the Key Data Covered in this Crude Oil Desalter Market Research and Growth Report?

-

What is the expected growth of the Crude Oil Desalter Market between 2025 and 2029?

-

USD 92.9 million, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Multi-stage desalter, Single-stage desalter), Type (Electrostatic dehydrator, Desalting process), Application (Refineries, Oil and gas production, Petrochemical plants) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Processing heavier crude slates, Capital intensity and budgetary constraints in volatile macroeconomic environment

-

-

Who are the major players in the Crude Oil Desalter Market?

-

Agar Corp., Alfa Laval AB, AMR Process Inc., Axens Group, Baker Hughes Co., Canadian Petroleum Processing Equipment Inc., Croda International Plc, Desalters LLC, EN-FAB Inc, Forum Energy Technologies Inc., Frames Energy Systems BV, GEA Group AG, Komax Systems, Mackenzie Hydrocarbons Australia Pty Ltd., McDermott International Ltd., Petro Techna International, Schlumberger Ltd., TechnipFMC plc, Veolia Environment SA and VME Process Inc.

-

Market Research Insights

- The market is shaped by dynamic forces including the need for opportunity crude processing and specialized bitumen desalting. Advances in modular engineering packages and skid-mounted systems are facilitating brownfield retrofit projects, driving operational expenditure reduction. The implementation of a digital twin for desalters, leveraging the industrial internet of things (IIoT) and advanced process control (APC), enables real-time optimization.

- Refiners are achieving refinery margin improvement of over 5% through better crude oil conditioning and hydrocarbon recovery systems. Asset integrity management is enhanced by solutions for dehydration and desalting on FPSO topside modules. Stricter wastewater effluent quality standards are pushing the adoption of zero-liquid discharge (ZLD) technologies and other regulatory compliance tools, which can improve water recycling rates by 20%.

- This focus on energy efficiency in refining and heavy oil upgrading is validated by predictive maintenance models that reduce downtime.

We can help! Our analysts can customize this crude oil desalter market research report to meet your requirements.

RIA -

RIA -