Data Center General Construction Market Size 2026-2030

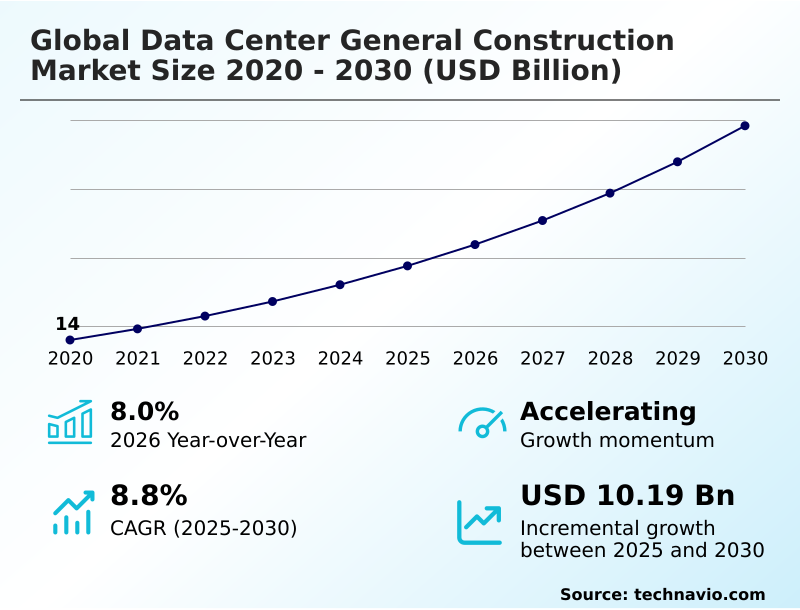

The data center general construction market size is valued to increase by USD 10.19 billion, at a CAGR of 8.8% from 2025 to 2030. Unprecedented surge in global data generation and consumption will drive the data center general construction market.

Major Market Trends & Insights

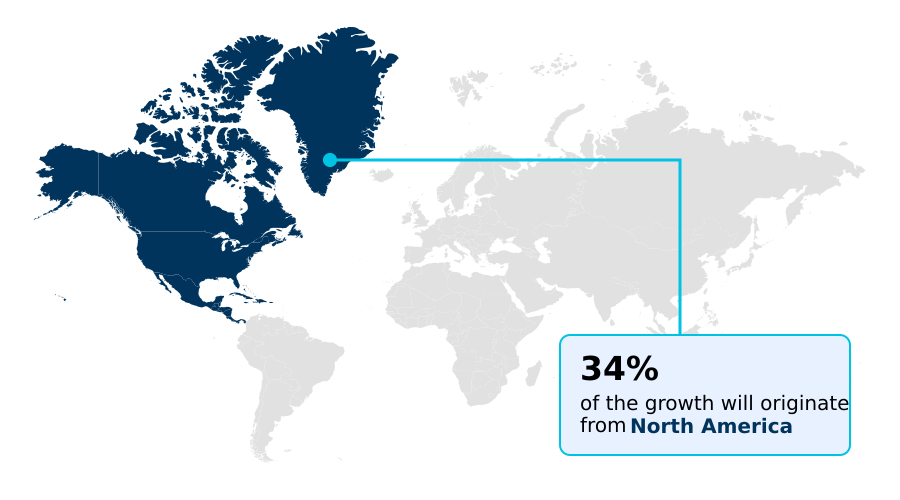

- North America dominated the market and accounted for a 33.8% growth during the forecast period.

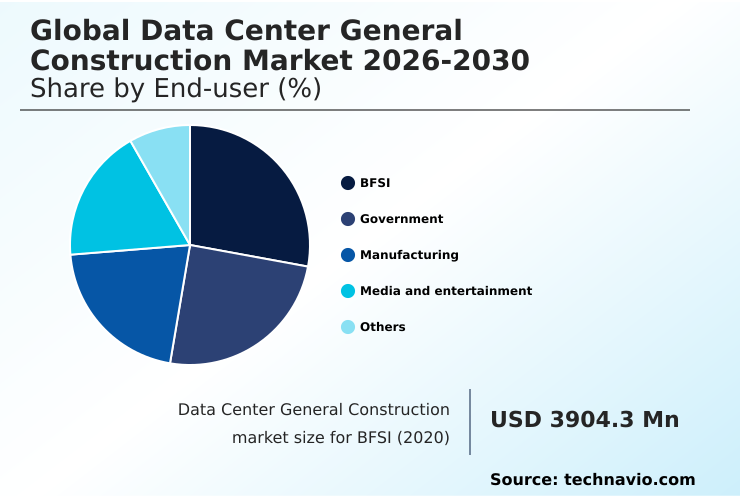

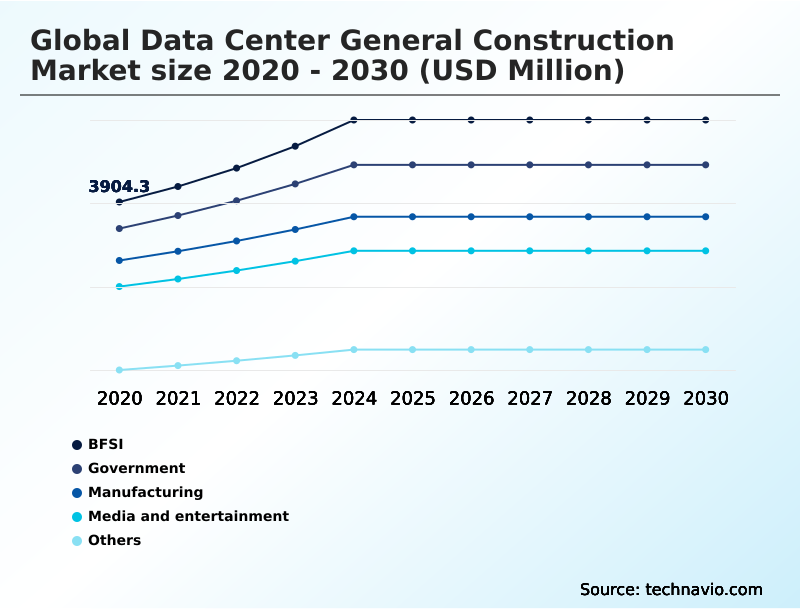

- By End-user - BFSI segment was valued at USD 5.24 billion in 2024

- By Type - Base building shell construction segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 15.58 billion

- Market Future Opportunities: USD 10.19 billion

- CAGR from 2025 to 2030 : 8.8%

Market Summary

- The data center general construction market is expanding rapidly, driven by the global economy's inexorable shift toward digitalization. The proliferation of AI, cloud computing, and the Internet of Things generates enormous data volumes, creating a relentless demand for facilities capable of storing and processing this information. This is not just about building more space; it is about constructing highly specialized environments.

- For instance, a hyperscaler planning a new cloud region must orchestrate a complex development process involving everything from site acquisition to the commissioning of mission-critical systems. This scenario highlights the need for advanced construction techniques like modularization and prefabrication to accelerate deployment.

- Simultaneously, there is a strong emphasis on sustainability, with new builds incorporating energy-efficient cooling technologies and designs that accommodate renewable power sources. Navigating challenges such as supply chain volatility for critical equipment and skilled labor shortages is now integral to project success, making strategic planning and robust project management more critical than ever.

- The industry is building the foundational infrastructure for the digital future, requiring a blend of speed, resilience, and environmental responsibility.

What will be the Size of the Data Center General Construction Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Center General Construction Market Segmented?

The data center general construction industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- BFSI

- Government

- Manufacturing

- Media and entertainment

- Others

- Type

- Base building shell construction

- Architecture planning and designing

- Product type

- Hyperscale data centers

- Colocation data centers

- Enterprise data centers

- Edge data centers

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Colombia

- Argentina

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By End-user Insights

The bfsi segment is estimated to witness significant growth during the forecast period.

The BFSI segment demands the highest standards in data center construction, driven by non-negotiable requirements for security and regulatory compliance. Construction for this sector focuses on mission-critical facilities engineered for exceptional fault tolerance, often pursuing tier iv certification to achieve 99.995% availability.

The physical security measures integrated into the structural framework and building envelope are extensive. The data center project lifecycle involves meticulous planning for redundant power distribution and advanced cooling infrastructure to support continuous operations.

The data center design principles emphasize robust network connectivity and a secure perimeter. These high-specification projects, vital for processing sensitive financial data, serve as a benchmark for resilience and security in the industry, impacting overall data center construction costs.

The BFSI segment was valued at USD 5.24 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Center General Construction Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is diversifying beyond traditional hubs. While North America leads in incremental growth, contributing over 33%, the APAC region is expanding at the fastest rate, with a regional CAGR of 10.0%.

This growth is driven by massive investments in hyperscale data centers and increasing data sovereignty mandates. Key markets like India and China are witnessing intense construction of carrier-neutral facility projects and subsea cable landings to support their digital economies.

European development is heavily influenced by green building practices and the need for data center energy efficiency, while emerging markets in South America and the Middle East are building out foundational cooling infrastructure and power distribution networks.

This global expansion demands sophisticated data center construction management and expertise in navigating varied data center permitting processes.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the industry is being defined by a response to increasingly complex demands. The construction for high-density AI workloads is a primary focus, necessitating a re-evaluation of traditional building methods. This has accelerated the adoption of modular construction in hyperscale projects, where prefabrication benefits for data center speed are undeniable.

- The liquid cooling impact on building design is profound, influencing everything from the structural requirements for multi-story data centers to the integration of advanced PUE and WUE optimization techniques. Concurrently, the push for sustainability is evident in the selection of sustainable materials in data center builds and innovative approaches like waste heat reuse in data center design.

- BIM integration in data center projects has become standard, with firms leveraging it reporting up to 25% fewer on-site modifications compared to traditional methods. However, significant hurdles persist. Data center construction labor shortages and persistent supply chain risks in data center construction threaten project timelines globally.

- Navigating the challenges in data center power sourcing and complex regulatory compliance for data center builds requires strategic foresight. From designing carrier-neutral colocation facilities to retrofitting legacy data centers for efficiency, and from edge data center deployment strategies to specialized underground data center construction methods, the industry must innovate across the board.

- Addressing cooling solutions for tropical climates and ensuring robust seismic design for data center buildings are critical regional considerations, while building out power infrastructure for giga-scale data centers remains a global priority.

What are the key market drivers leading to the rise in the adoption of Data Center General Construction Industry?

- An unprecedented surge in global data generation and consumption serves as the foundational driver for the market's continuous expansion and demand for new capacity.

- Market growth is propelled by the exponential rise in data and the demanding nature of new workloads.

- The proliferation of AI and high-performance computing (HPC) is a primary driver, with AI data center construction requiring facilities that can handle power densities up to 10 times higher than traditional enterprise applications.

- This shift necessitates a focus on high-density power consumption and innovative liquid cooling infrastructure. The global expansion of hyperscalers, combined with strengthening data sovereignty laws, creates a consistent demand pipeline.

- This results in the development of new data center power infrastructure and subsea cable landings in emerging regions.

- These deployments aim to reduce latency for end-users, with edge data center design capable of improving application response times by more than 50%.

What are the market trends shaping the Data Center General Construction Industry?

- The ascendancy of sustainable and green construction principles is a defining market trend, shaping project lifecycles from design and material selection to long-term operational efficiency.

- Market trends are driven by sustainability and efficiency imperatives. The move toward sustainable data center construction is reshaping the industry, with green data center certification becoming a key objective. Projects incorporating advanced green building practices can lower long-term operational energy costs by over 15%.

- A strategic bifurcation is also occurring, with simultaneous investment in massive hyperscale data centers and distributed edge data centers. This duality requires versatile data center scalability design. The industrialization of building through modularization and prefabrication is another dominant trend.

- Using prefabricated components and industrialized construction methods can shorten project schedules by up to 30%, a critical advantage in a time-sensitive market. This manufacturing-led approach improves quality control and cost predictability across the entire data center project lifecycle.

What challenges does the Data Center General Construction Industry face during its growth?

- Pervasive skilled labor shortages, compounded by escalating labor costs, present a significant challenge that affects project timelines and overall industry growth potential.

- The market faces significant operational and logistical challenges that constrain growth. A pervasive shortage of skilled labor, especially for mission-critical construction, is a primary concern. The data center supply chain logistics are fragile, with disruptions for critical equipment like switchgear and generators extending project lead times by over 52 weeks in some instances.

- This volatility complicates data center construction management and elevates project risk. Furthermore, an increasingly stringent regulatory environment creates significant hurdles. The data center permitting process has become more complex, adding 12 to 18 months to project timelines in some key markets before ground can even be broken. These factors demand more sophisticated data center risk management and strategic planning.

Exclusive Technavio Analysis on Customer Landscape

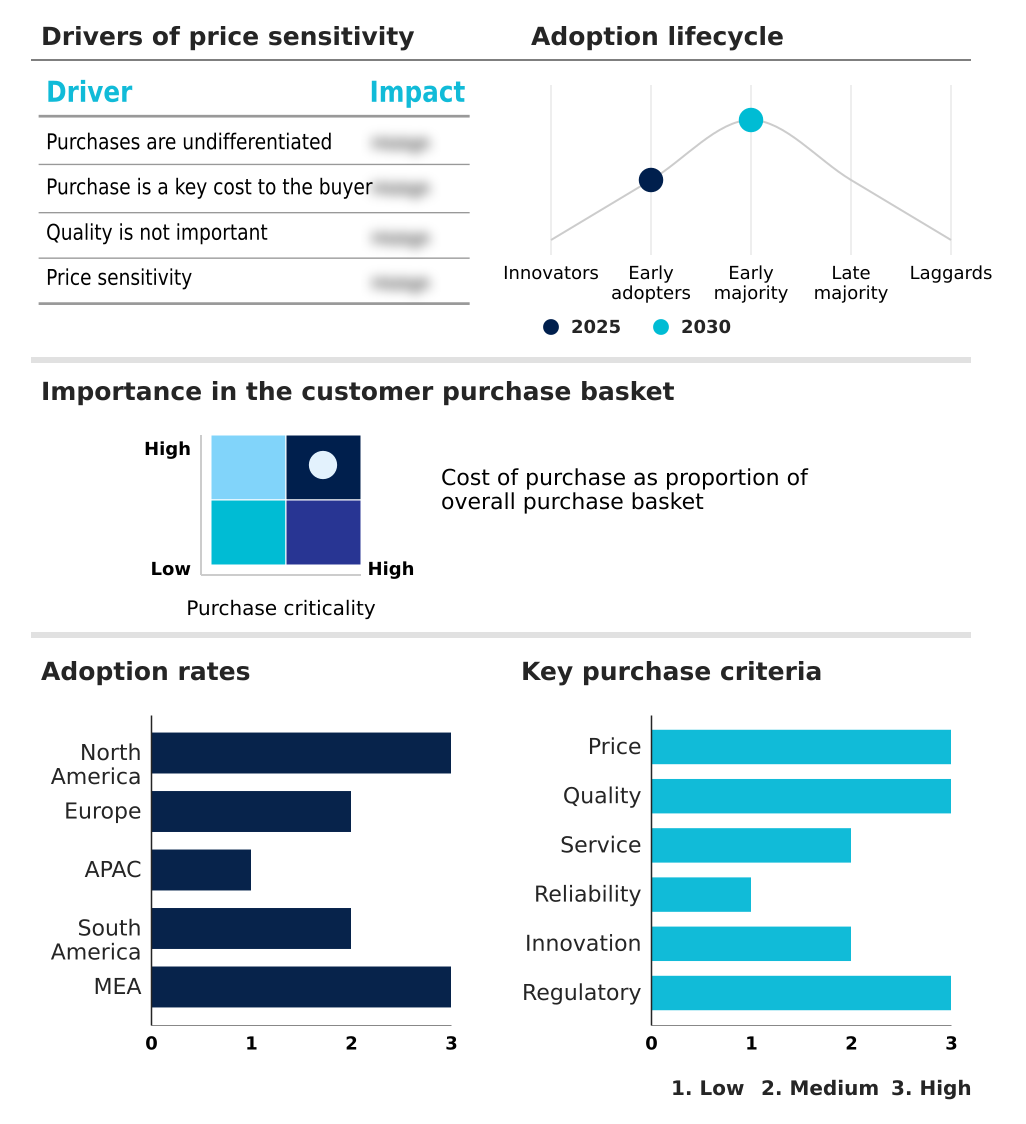

The data center general construction market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center general construction market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Center General Construction Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data center general construction market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Key offerings include integrated power distribution, smart automation, and complete server room implementation solutions vital for modern, high-performance data center environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AECOM

- Arup Group Ltd.

- Brasfield and Gorrie LLC

- CORGAN

- Digital Realty Trust Inc.

- DPR Construction

- HDR Inc.

- Jacobs Solutions Inc.

- Jones Engineering Holdings Ltd.

- Legrand SA

- M. A. Mortenson Co.

- Page Southerland Page Inc.

- Schneider Electric SE

- Skanska AB

- STO Building Group

- The Walsh Group

- Turner Construction Co.

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data center general construction market

- In December 2024, Schneider Electric partnered with Nvidia to release reference designs for AI data centers, aiming to optimize infrastructure for high-density computing.

- In January 2025, Schneider Electric announced the acquisition of APower, a data center infrastructure solutions provider, for approximately $1.2 billion, expanding its capabilities in the mission-critical sector.

- In January 2025, V.tal, a major Brazilian digital infrastructure company, announced it had secured land to develop a 200-megawatt hyperscale data center campus in Sao Paulo.

- In February 2025, Vertiv Holdings Co. launched a new portfolio of liquid cooling services to support the growing deployment of AI and other high-performance computing applications globally.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center General Construction Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 342 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 10194.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, Australia, Singapore, South Korea, Brazil, Colombia, Argentina, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's trajectory is shaped by the need to build sophisticated mission-critical facilities at an unprecedented scale. Core activities revolve around base building shell construction, which includes creating a resilient structural framework and building envelope. The complexity escalates with the integration of high-density power consumption systems and advanced cooling infrastructure, such as direct-to-chip liquid cooling and immersion cooling.

- Boardroom decisions are now heavily influenced by data sovereignty requirements, mandating investments in in-country hyperscale data centers and colocation data centers. This trend also drives demand for smaller enterprise data centers and distributed edge data centers. The adoption of modularization and prefabrication, including prefabricated components, is critical for speed.

- Designs increasingly feature seismic resilience and rely on building information modeling and computational fluid dynamics for optimization. Achieving low power usage effectiveness and water usage effectiveness through green building practices, waste heat recovery, and the use of low-carbon concrete and recycled steel is now a competitive differentiator, often supported by power purchase agreements.

- Facilities with waste heat recovery can improve overall energy reuse by over 20%. The design of a carrier-neutral facility prioritizes robust network connectivity with secure meet-me rooms, often near subsea cable landings, ensuring high-performance computing with absolute fault tolerance and achieving tier iii certification or tier iv certification through stringent physical security.

What are the Key Data Covered in this Data Center General Construction Market Research and Growth Report?

-

What is the expected growth of the Data Center General Construction Market between 2026 and 2030?

-

USD 10.19 billion, at a CAGR of 8.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (BFSI, Government, Manufacturing, Media and entertainment, and Others), Type (Base building shell construction, and Architecture planning and designing), Product Type (Hyperscale data centers, Colocation data centers, Enterprise data centers, and Edge data centers) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Unprecedented surge in global data generation and consumption, Pervasive skilled labor shortages and escalating labor costs

-

-

Who are the major players in the Data Center General Construction Market?

-

ABB Ltd., AECOM, Arup Group Ltd., Brasfield and Gorrie LLC, CORGAN, Digital Realty Trust Inc., DPR Construction, HDR Inc., Jacobs Solutions Inc., Jones Engineering Holdings Ltd., Legrand SA, M. A. Mortenson Co., Page Southerland Page Inc., Schneider Electric SE, Skanska AB, STO Building Group, The Walsh Group, Turner Construction Co. and Vertiv Holdings Co.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push toward operational excellence and rapid deployment. The adoption of industrialized construction methods is a key factor, with modular data center deployment accelerating project timelines by up to 40% compared to traditional builds. This approach is critical for meeting the aggressive expansion goals of hyperscalers.

- Concurrently, the need to manage high-density cooling solutions for AI workloads has spurred innovation in data center cooling efficiency, where advanced liquid cooling infrastructure can reduce related energy consumption by over 50%. This focus on efficiency aligns with stringent data center uptime standards.

- Furthermore, effective data center risk management, incorporating robust data center security design and comprehensive fire suppression system design, is paramount for ensuring business continuity and regulatory compliance, directly impacting the total cost of ownership.

We can help! Our analysts can customize this data center general construction market research report to meet your requirements.

RIA -

RIA -