Dermatology Endoscopy Devices Market Size 2024-2028

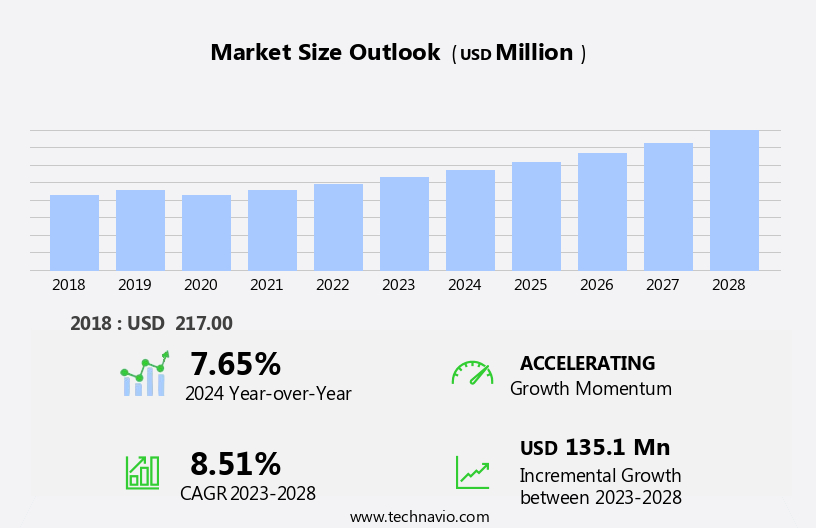

The dermatology endoscopy devices market size is forecast to increase by USD 135.1 million, at a CAGR of 8.51% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing prevalence of melanoma and autoimmune skin diseases. The rising incidence of these conditions necessitates the adoption of advanced diagnostic and therapeutic tools, thereby fueling market expansion. Furthermore, technological advancements continue to shape the market landscape, with innovations in imaging technologies, miniaturization, and integration of Artificial Intelligence (AI) and robotics enhancing the diagnostic accuracy and efficiency of dermatology endoscopy devices. However, the market faces challenges as well. The presence of substitutes, such as traditional diagnostic methods and non-invasive imaging techniques, may limit the adoption of dermatology endoscopy devices. Additionally, the high cost of these devices and the need for specialized training to operate them pose challenges for market penetration, particularly in developing regions.

- Companies in the market must address these challenges by focusing on cost reduction strategies, collaborating with healthcare providers to offer training programs, and continuously innovating to differentiate their offerings from competitors. By capitalizing on the growing demand for advanced diagnostic tools and navigating these challenges effectively, market participants can seize opportunities and maintain a competitive edge in the dynamic market.

What will be the Size of the Dermatology Endoscopy Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market is characterized by continuous evolution and innovation, driven by the growing demand for advanced diagnostic tools in the field of dermatology. Dermoscopy imaging plays a crucial role in skin cancer detection, enabling healthcare professionals to examine skin lesions in greater detail than traditional methods. Dermoscopic features extraction and digital image analysis enhance the diagnostic accuracy of these tools, while real-time visualization and endoscopic camera systems provide improved lesion border definition. Patient comfort is a significant consideration in the development of these devices, with features such as fiber optic illumination, image enhancement filters, and disposable endoscopy ensuring a more pleasant experience for patients.

Endoscopic dermatology and teledermatology platforms enable remote consultation and diagnosis, expanding access to expert care for patients in remote locations. Skin lesion visualization and vascular pattern assessment are essential components of these devices, with high-resolution endoscopy and confocal microscopy providing detailed images of the skin. Light source technology and image processing software enable accurate diagnosis, while optical coherence tomography offers non-invasive imaging capabilities. Clinical workflow integration, data management systems, and medical image storage solutions facilitate efficient and effective use of these devices in a clinical setting. Sterilization protocols and endoscopic probe design ensure the highest standards of hygiene and safety.

The ongoing unfolding of market activities and evolving patterns in the market reflect the dynamic nature of this field, with ongoing advancements in technology and applications across various sectors.

How is this Dermatology Endoscopy Devices Industry segmented?

The dermatology endoscopy devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Traditional

- Digital

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Product Insights

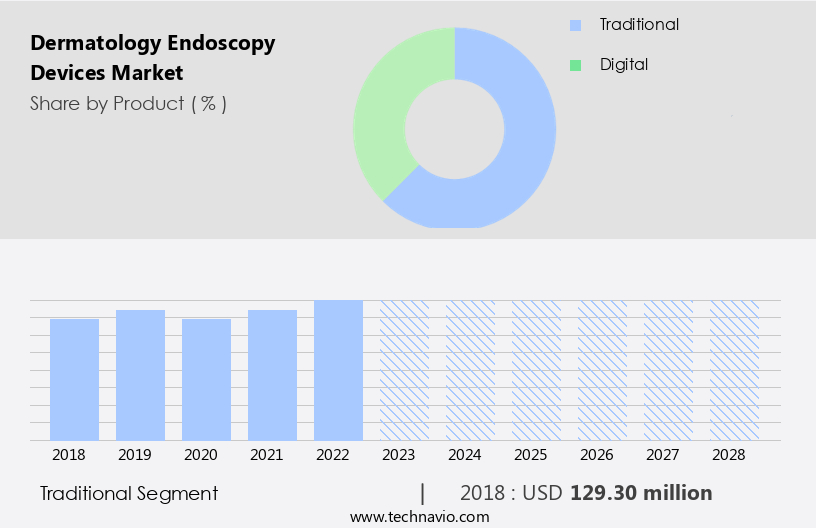

The traditional segment is estimated to witness significant growth during the forecast period.

The market encompasses innovative technologies that enhance skin cancer detection and lesion visualization. Traditional dermatology endoscopy devices, comprised of a magnifier, transparent plate, light source, and liquid medium, dominate the market due to their long-standing use in diagnostics and cost-effectiveness. These devices offer real-time visualization, enabling dermatologists to examine skin lesions in detail. However, the rise of digital image analysis and teledermatology platforms is transforming the landscape. Advanced features such as lesion border definition, vascular pattern assessment, and pigment network analysis facilitate more accurate melanoma diagnosis. Endoscopic camera systems with high-resolution imaging and image processing software offer improved image quality and clinical workflow integration.

Confocal microscopy and optical coherence tomography provide non-invasive, high-resolution imaging for better diagnosis and dermatopathology correlation. Sterilization protocols ensure hygiene and patient safety. Companies focus on endoscopic probe design for enhanced patient comfort and remote consultation capabilities. The integration of data management systems and image archiving solutions streamlines clinical workflows and facilitates efficient medical image storage. Overall, the market is driven by the evolving need for advanced, non-invasive imaging technologies in skin cancer detection and diagnosis.

The Traditional segment was valued at USD 129.30 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

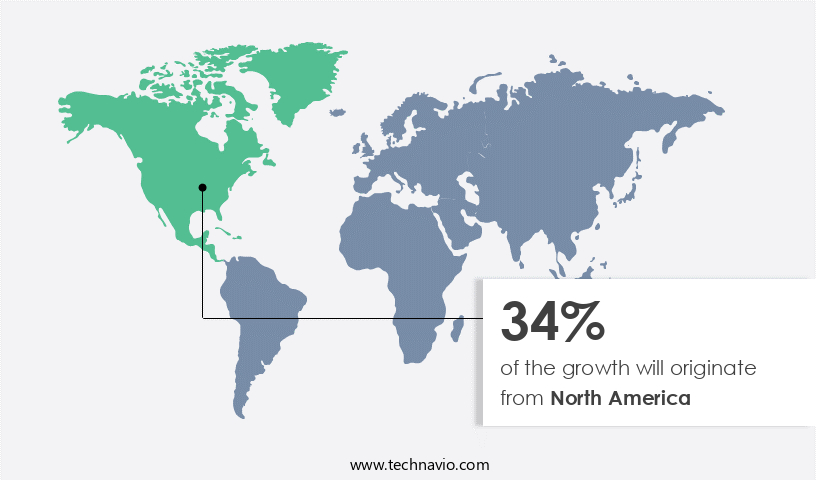

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the Americas is experiencing steady growth, driven by advancements in technologies such as dermoscopic features extraction, real-time visualization, and high-resolution endoscopy. In 2023, North America led the market, with the US and Canada being significant contributors due to the presence of prominent companies like Canfield Scientific and MetaOptima Technology. These companies showcase their innovative products at scientific events and conferences, fueling market expansion. Moreover, organizations like the American Academy of Dermatology are promoting awareness and providing training to professionals, ensuring effective utilization of these devices. Technological innovations include image processing software, digital image analysis, and optical coherence tomography, which facilitate accurate melanoma diagnosis and pigment network analysis.

Endoscopic probe design, sterilization protocols, and clinical workflow integration are other crucial factors driving market growth. The integration of teledermatology platforms and remote dermatology consultation services enhances patient convenience and accessibility, further boosting market demand. Vascular pattern assessment, video dermoscopy systems, and disposable endoscopy devices cater to the need for non-invasive imaging and improved patient comfort.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Dermatology Endoscopy Devices Industry?

- The prevalence of melanoma and autoimmune skin diseases is the primary driving factor behind the market's growth. These conditions have seen a significant increase in incidence, leading to a heightened demand for diagnostic tools, treatments, and therapeutic interventions in the healthcare industry.

- Dermatology endoscopy devices have gained significant traction in the healthcare industry due to the rising prevalence of skin disorders and abnormalities. Skin conditions are among the most common health issues worldwide, surpassing the prevalence of conditions such as hypertension, cancer, and obesity. Autoimmune skin disorders, which result from the body's abnormal immune response against foreign substances, are a subset of these conditions. Examples of autoimmune disorders include psoriasis, scleroderma, epidermolysis bullosa, and dermatomyositis. To effectively diagnose and manage these disorders, advanced dermatology diagnostic tools are essential. Dermatology endoscopy devices, which utilize non-invasive imaging techniques, play a crucial role in this regard.

- These devices enable dermatologists to visualize the skin's internal structures, facilitating accurate diagnosis and treatment. Moreover, advanced features such as data management systems, image archiving systems, and dermatopathology correlation enhance the functionality of these devices. Medical image storage and pigment network analysis are critical components of these systems, allowing for efficient data organization and analysis. Endoscopic probe design continues to evolve, with innovations aimed at improving image quality and user experience. In conclusion, the increasing prevalence of autoimmune skin disorders and the advancements in dermatology endoscopy devices are driving market growth. The integration of advanced features, such as data management systems and image archiving, further enhances the value proposition of these devices.

What are the market trends shaping the Dermatology Endoscopy Devices Industry?

- Advances in technology are currently shaping market trends. This significant evolution in technology is a mandatory factor for businesses seeking to remain competitive.

- Dermatology endoscopy devices are witnessing significant advancements as companies introduce innovative and lightweight solutions for skin cancer detection. These devices enable dermoscopy imaging with real-time visualization of skin lesions, improving the accuracy of diagnosis. Companies are focusing on developing endoscopic dermatology systems that are compatible with smartphones and tablets for enhanced convenience. For instance, Pixience's C-Cube 2 device offers high-quality imaging with a USB 3.0 connection for data transfer. It provides detailed observation of skin lesions up to 12 mm in diameter and weighs around 410 grams.

- Similarly, 3Gen's DermLite DL1 device is compatible with Apple and Samsung smartphones and tablets, offering ease of use and portability. These advancements aim to provide a more comfortable experience for patients while ensuring accurate skin cancer detection. Additionally, the integration of these devices with teledermatology platforms enables remote consultation, expanding access to specialized dermatological care.

What challenges does the Dermatology Endoscopy Devices Industry face during its growth?

- The presence of substitutes poses a significant challenge to the industry's growth, as it increases competition and puts pressure on companies to innovate and differentiate themselves in order to maintain market share.

- Dermatology endoscopy devices, which include fiber optic illumination and video dermoscopy systems, play a crucial role in defining lesion borders and assessing vascular patterns for accurate diagnosis in dermatology. These devices offer magnification capabilities and image enhancement filters for clearer visualization, enabling remote dermatology consultations. However, full-body imaging systems and microscopes serve as substitutes, providing high-quality images for tracking, comparing, and monitoring lesions. The increasing prevalence of skin cancer drives the demand for these tools in disease diagnosis.

- Companies offer digital image analysis support for case-to-case assessments, ensuring harmonious and immersive experiences for healthcare professionals. Despite these advantages, the global market for dermatology endoscopy devices faces competition from alternative diagnostic methods, restricting market growth.

Exclusive Customer Landscape

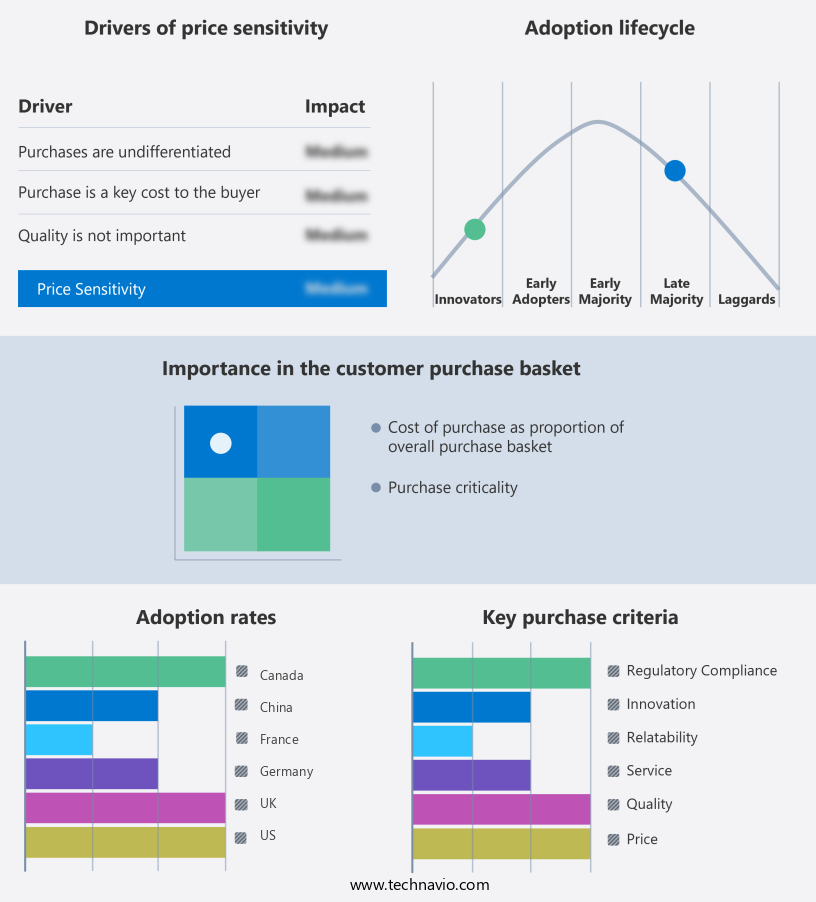

The dermatology endoscopy devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dermatology endoscopy devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, dermatology endoscopy devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMD Global Telemedicine Inc. - The company specializes in the development and commercialization of advanced dermatology endoscopy devices, including the innovative DermaScope product.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMD Global Telemedicine Inc.

- AnMo Electronics Corp.

- Bausch Health Companies Inc.

- Caliber Imaging and Diagnostics Inc

- Canfield Scientific Inc.

- DermLite LLC

- DermoScan GmbH

- Firefly Global

- HEINE Optotechnik GmbH and Co. KG

- ILLUCO Corp. Ltd.

- Jedmed

- KIRCHNER and WILHELM plus GmbH Co. KG

- MetaOptima Technology Inc.

- Optilia Instruments AB

- Pixience Healthcare Technology Solutions

- Rudolf Riester GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dermatology Endoscopy Devices Market

- In January 2024, Merivaara Corporation, a leading provider of medical technology solutions, announced the launch of its new dermatology endoscopy system, EndoSight Dermascope, designed for the diagnosis and treatment of various skin conditions. This innovative device features high-definition imaging and advanced lighting systems, enabling clear visualization of skin lesions (Merivaara Corporation Press Release).

- In March 2024, Olympus Corporation, a global medical technology company, entered into a strategic partnership with SkinAnalytics, a leading digital health company. The partnership aimed to integrate SkinAnalytics' AI-powered dermatology analysis platform into Olympus' endoscopy systems, enhancing diagnostic accuracy and efficiency (Olympus Corporation Press Release).

- In May 2024, Fujifilm Corporation received FDA approval for its new dermatology endoscopy system, the Fujifilm IntelliScope NM-430. This system combines narrow band imaging technology with advanced image processing capabilities, offering enhanced visualization of skin lesions for improved diagnosis and treatment (Fujifilm Corporation Press Release).

- In February 2025, Siemens Healthineers, a leading medical technology company, announced a significant investment in its dermatology endoscopy business. The company plans to expand its production capacity and invest in research and development, aiming to capture a larger market share and stay competitive in the rapidly growing market (Siemens Healthineers Press Release).

Research Analyst Overview

- The dermatology endoscopy market is witnessing significant advancements with the integration of minimally invasive surgery techniques and diagnostic algorithms into dermatoscopy equipment. Endoscopy accessories, such as image annotation tools and surgical guidance systems, are essential for enhancing procedural efficiency and skin lesion classification. Clinical validation data plays a crucial role in system performance testing, ensuring cost effectiveness and patient safety. Subcutaneous imaging and skin surface imaging are transforming dermatological endoscopy, enabling real-time visualization of skin lesions. Service contracts and technical specifications are key considerations for businesses seeking to invest in this market. Software upgrades and data acquisition methods are essential for maintaining image quality metrics and improving image capture devices.

- Training and support are vital components of the dermatology endoscopy market, ensuring that healthcare professionals can effectively utilize epidermal imaging tools for skin lesion analysis. Maintenance protocols and patient safety measures are also critical for ensuring the longevity and reliability of these devices. Overall, the dermatology endoscopy market is evolving rapidly, driven by advancements in technology and the growing demand for minimally invasive diagnostic and treatment solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dermatology Endoscopy Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.51% |

|

Market growth 2024-2028 |

USD 135.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.65 |

|

Key countries |

US, UK, Canada, Germany, China, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Dermatology Endoscopy Devices Market Research and Growth Report?

- CAGR of the Dermatology Endoscopy Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the dermatology endoscopy devices market growth of industry companies

We can help! Our analysts can customize this dermatology endoscopy devices market research report to meet your requirements.

RIA -

RIA -