Dicing Equipment Market Size 2026-2030

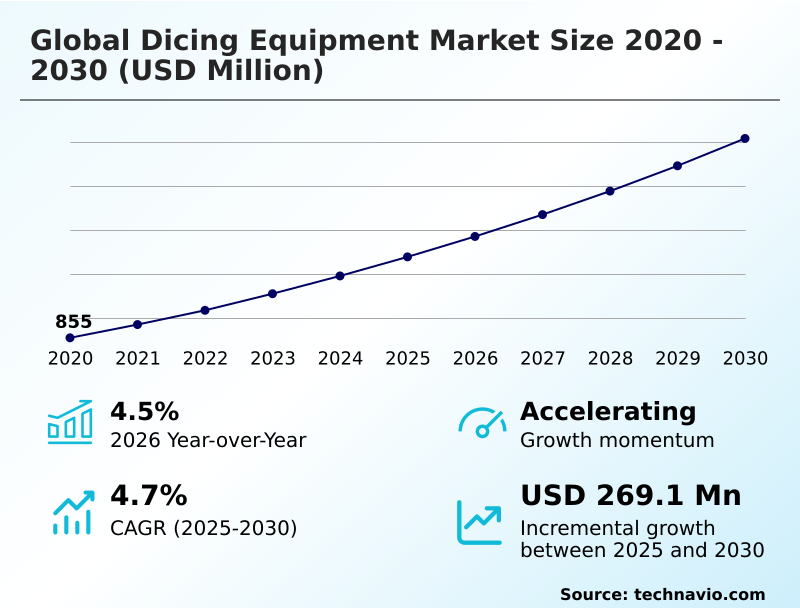

The dicing equipment market size is valued to increase by USD 269.1 million, at a CAGR of 4.7% from 2025 to 2030. Growing investment in fabrication facilities will drive the dicing equipment market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 86.1% growth during the forecast period.

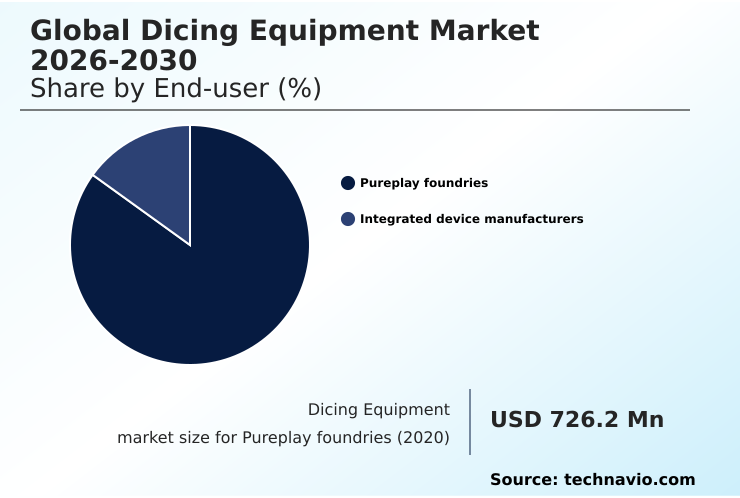

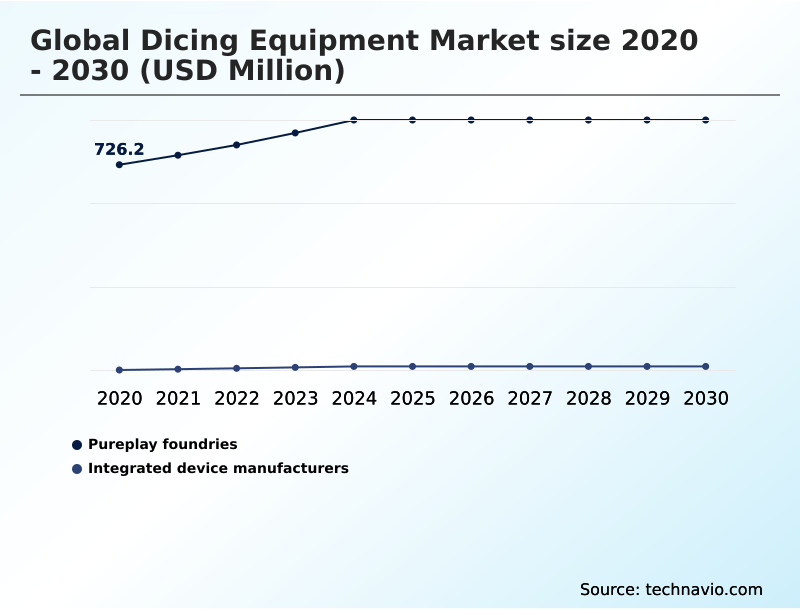

- By End-user - Pureplay foundries segment was valued at USD 856.4 million in 2024

- By Type - Blade dicing equipment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 453 million

- Market Future Opportunities: USD 269.1 million

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The dicing equipment market is integral to modern electronics production, enabling the critical step of wafer singulation in semiconductor manufacturing. This process is evolving rapidly, driven by the relentless pursuit of miniaturization and the adoption of new compound semiconductors like silicon carbide (SiC) and gallium nitride (GaN).

- As devices shrink, the precision required from dicing technologies, whether blade dicing, laser dicing, or plasma dicing, intensifies. A primary focus is on minimizing kerf loss and the heat affected zone (HAZ) to maximize the number of functional dies per wafer while preventing chipping.

- For instance, a fab producing components for electric vehicles must perfect its dicing before grind (DBG) process for ultra-thin wafers. This involves optimizing spindle speed and coolant flow to maintain die strength and avoid micro-cracks, ensuring the reliability needed for high-power applications.

- This constant need for innovation in die separation and process control underscores the market's dynamic nature, with advancements directly impacting the feasibility of next-generation electronics.

What will be the Size of the Dicing Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Dicing Equipment Market Segmented?

The dicing equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Pureplay foundries

- Integrated device manufacturers

- Type

- Blade dicing equipment

- Laser dicing equipment

- Plasma dicing equipment

- Technology

- Automated dicing systems

- Manual dicing

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The pureplay foundries segment is estimated to witness significant growth during the forecast period.

The pureplay foundries segment is pivotal to the semiconductor manufacturing ecosystem, operating high-volume production for third-party clients. Demand for precise and reliable equipment for die singulation is critical, as this process directly impacts yield and device integrity.

As designs advance toward heterogeneous integration and advanced packaging, foundries require high-performance solutions for wafer singulation that maintain tight tolerances, ensure high die strength, and reduce micro-cracks.

Innovations in plasma dicing and laser dicing are essential for handling diverse materials and achieving dicing process optimization.

Operational efficiency is paramount, driving adoption of automation to maximize throughput while maintaining consistent quality, with some foundries achieving a 3% improvement in overall yield by refining their scribing and dicing fluid management processes.

The Pureplay foundries segment was valued at USD 856.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 86.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dicing Equipment Market Demand is Rising in APAC Request Free Sample

The geographic landscape is dominated by the APAC region, which is set to account for over 86% of the market's incremental growth.

This concentration is due to the extensive network of semiconductor manufacturing facilities and a robust supply chain supporting advanced packaging and die separation activities.

Regional growth is fueled by significant investments in fabrication capacity to meet global demand for high-precision electronics. North America is the second-largest contributor, driven by strategic initiatives to bolster domestic production and R&D in singulation technologies.

The need for effective thermal management and wafer bonding techniques in this region reinforces demand for sophisticated equipment.

In contrast, Europe's market share is smaller but shows steady growth, particularly in specialized sectors requiring advanced MEMS dicing and 3D IC integration capabilities.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of modern semiconductor production requires a deep understanding of advanced singulation methods. A blade dicing vs laser dicing comparison often reveals distinct advantages based on material and application, with laser ablation techniques for brittle materials gaining traction.

- For manufacturers, reducing kerf loss in wafer dicing is a primary objective, leading many to adopt stealth dicing for thin silicon wafers to maximize die output. The dicing before grind process advantages include enhanced die strength, which is critical for advanced packaging dicing challenges. Concurrently, managing heat affected zone in laser dicing remains a key focus to prevent thermal damage.

- For high-volume operations, dicing saw maintenance best practices and dicing tape selection for fragile substrates are essential for consistent performance. Process control for high yield singulation is achieved by integrating technologies like wafer mapping for dicing accuracy improvement and automating the die separation process flow.

- As applications for compound semiconductors expand, dicing solutions for silicon carbide wafers are becoming standard, requiring strategies for preventing chipping during wafer singulation. Evaluating dicing equipment cost of ownership analysis is crucial for long-term investment planning, alongside optimizing coolant flow for dicing process and understanding the impact of spindle speed on dicing quality.

- Furthermore, plasma dicing for MEMS device fabrication represents a specialized field with unique requirements. In this competitive environment, systems that offer a 2x improvement in defect detection speed over previous generations provide a significant operational edge.

What are the key market drivers leading to the rise in the adoption of Dicing Equipment Industry?

- Growing investment in fabrication facilities is a key driver for the market, fueling demand for advanced semiconductor manufacturing equipment.

- Substantial investments in new fabrication facilities are a primary driver, creating sustained demand for high-performance dicing equipment. As manufacturers scale up to meet the needs of the automotive and data center sectors, the focus is on maximizing throughput and yield.

- This requires sophisticated die singulation systems capable of high-precision cutting with minimal downtime. New fabs are being designed to increase wafer starts by over 25%, compelling equipment suppliers to deliver solutions that enhance throughput enhancement by a comparable margin.

- Furthermore, the adoption of automation and advanced process control has led to a 10% reduction in cycle times for some backgrinding and dicing sequences, demonstrating a clear return on investment for companies upgrading their production lines.

What are the market trends shaping the Dicing Equipment Industry?

- The increasing demand for Internet of Things (IoT) connected devices is emerging as a significant trend, driving complexity in semiconductor design and production scale.

- The market is experiencing a significant shift driven by the demand for miniaturization in connected devices, which necessitates higher precision in semiconductor manufacturing. This trend is accelerating the adoption of laser grooving and other advanced singulation technologies to handle increasingly complex and fragile materials. As a result, equipment that enhances yield and throughput is paramount.

- For example, the integration of automated defect inspection systems has been shown to improve detection accuracy by over 20% compared to manual methods, while optimizing the wafer dicing process for specific substrates can reduce material waste by up to 15%.

- This focus on efficiency and quality control is critical for supporting next-generation applications in wafer-level packaging (WLP) and system-in-package (SiP) designs.

What challenges does the Dicing Equipment Industry face during its growth?

- The complexity of dicing patterns and the risk of functional defects during manufacturing processes present a key challenge to industry growth.

- A significant challenge lies in managing the growing complexity of dicing patterns and minimizing functional defects, especially with the adoption of ultra-thin wafers and delicate compound semiconductors. The risk of chipping or inducing micro-cracks during die separation can reduce final yields by as much as 5% in sensitive applications.

- Furthermore, the intricacies of thin wafer handling and dicing fluid management require advanced automation and process control to maintain stability. Equipment that offers real-time blade wear monitoring can extend consumable life by up to 30%, mitigating a key operational cost. Addressing these challenges is crucial for enabling high-volume manufacturing of next-generation devices for fan-out wafer-level packaging (FOWLP).

Exclusive Technavio Analysis on Customer Landscape

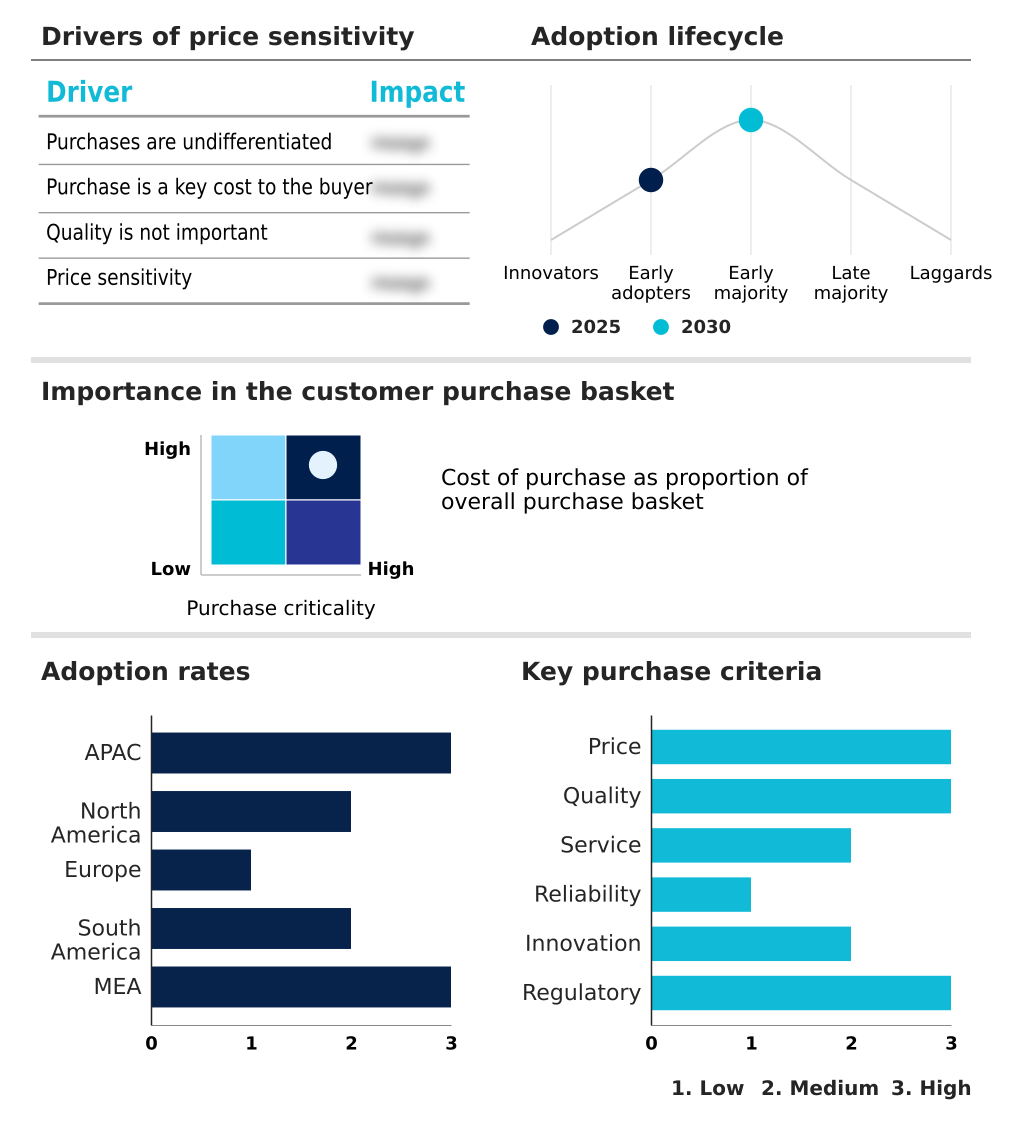

The dicing equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dicing equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dicing Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dicing equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Micromac AG - Specializes in laser-based micro-machining systems, delivering high-precision dicing and structuring solutions for the semiconductor and photovoltaic industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Micromac AG

- Advanced Dicing Technologies

- ASMPT ALSI

- DISCO Corp.

- Jiangsu Jing Chuang Co. Ltd.

- KLA Corp.

- Marposs Spa

- MTINC Machines

- Neon Tech Co. Ltd.

- Panasonic Connect Co. Ltd.

- PLASMA THERM

- Shenyang Heyan Technology

- SLTL Group

- Suzhou Delphi Laser Co. Ltd.

- Synova SA

- TOKYO SEIMITSU CO. LTD.

- Veeco Instruments Inc.

- GL Tech Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dicing equipment market

- In January 2025, Digi International announced new solutions at the Consumer Electronics Show and celebrated shipping over 25 million Digi XBee modules, highlighting the expansion of IoT connectivity.

- In January 2025, Tokyo Seimitsu Co., Ltd. and Asahi Diamond Industrial Co., Ltd. announced a memorandum of understanding to form a joint venture focused on advanced dicing and cutting technologies.

- In March 2025, Panasonic Connect announced its NPM-GW modular placement machine, showcasing a flexible platform designed to enhance precision, throughput, and scalability in electronics manufacturing.

- In March 2025, TSMC announced a USD 100 billion investment for three new semiconductor fabs, advanced packaging facilities, and an R&D center in Arizona to reinforce US chip manufacturing.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dicing Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 278 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 269.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dicing equipment market is evolving from a focus on mechanical cutting to a sophisticated landscape of high-precision technologies essential for next-generation semiconductor manufacturing. Key advancements in laser dicing, plasma dicing, and stealth dicing are enabling the wafer singulation of complex devices that use compound semiconductors such as silicon carbide (SiC) and gallium nitride (GaN).

- This shift requires meticulous process control to manage the heat affected zone (HAZ), minimize micro-cracks, and prevent chipping, thereby ensuring die strength. For boardroom consideration, investing in equipment capable of dicing before grind (DBG) is a strategic decision that directly supports the production of ultra-thin wafers for advanced packaging and heterogeneous integration.

- Optimizing the entire workflow—from the wafer mounter and dicing tape to the final die separator—is critical for maximizing throughput and yield. Systems integrating technologies that reduce dicing-related defects by over 20% are becoming indispensable.

- Success depends on mastering variables like spindle speed and coolant flow in blade dicing, as well as the intricate parameters of plasma etching and scribing for complete die separation and effective backgrinding, all guided by precise wafer mapping and automation.

What are the Key Data Covered in this Dicing Equipment Market Research and Growth Report?

-

What is the expected growth of the Dicing Equipment Market between 2026 and 2030?

-

USD 269.1 million, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Pureplay foundries, and Integrated device manufacturers), Type (Blade dicing equipment, Laser dicing equipment, and Plasma dicing equipment), Technology (Automated dicing systems, and Manual dicing) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing investment in fabrication facilities, Complexity of patterns and functional defects in manufacturing processes

-

-

Who are the major players in the Dicing Equipment Market?

-

3D Micromac AG, Advanced Dicing Technologies, ASMPT ALSI, DISCO Corp., Jiangsu Jing Chuang Co. Ltd., KLA Corp., Marposs Spa, MTINC Machines, Neon Tech Co. Ltd., Panasonic Connect Co. Ltd., PLASMA THERM, Shenyang Heyan Technology, SLTL Group, Suzhou Delphi Laser Co. Ltd., Synova SA, TOKYO SEIMITSU CO. LTD., Veeco Instruments Inc. and GL Tech Co. Ltd.

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for greater manufacturing efficiency and yield improvement. The adoption of advanced singulation technology and automated process control has demonstrated the ability to reduce defect rates by over 15%, directly enhancing profitability.

- As manufacturers confront the challenges of brittle material cutting, particularly for glass wafer dicing and ceramic substrate dicing, a clear shift toward specialized solutions is evident. This transition is not merely about new hardware but involves a holistic dicing process optimization approach, which has been shown to improve throughput by up to 20% in high-volume settings.

- The emphasis on thin wafer handling and blade wear monitoring further reflects a strategic focus on maximizing asset utilization and reducing the total cost of ownership across production lines.

We can help! Our analysts can customize this dicing equipment market research report to meet your requirements.