Die Bonder Equipment Market Size 2025-2029

The die bonder equipment market size is forecast to increase by USD 202.4 million, at a CAGR of 4.2% between 2024 and 2029.

Major Market Trends & Insights

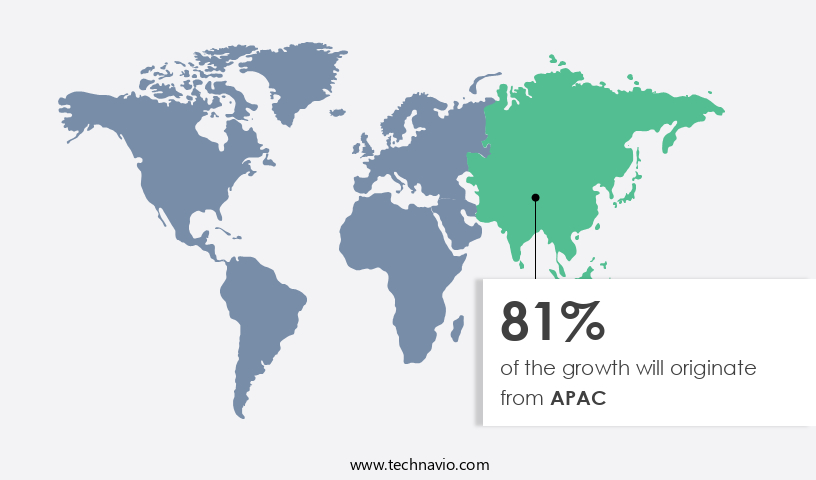

- APAC dominated the market and accounted for a 81% growth during the forecast period.

- By the End-user - OSATs segment was valued at USD 443.80 million in 2023

- By the Type - Fully automatic segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 47.02 million

- Market Future Opportunities: USD 202.40 million

- CAGR : 4.2%

- APAC: Largest market in 2023

Market Summary

- The market is witnessing significant advancements, driven by the increasing demand for high-performance semiconductor ICs in wireless devices and IoT applications. This trend is reflected in the growing adoption of advanced die bonder equipment, such as those integrating AI and machine learning (ML) technologies. One notable development is the rising preference for polymer adhesive wafer bonding equipment, which offers benefits like improved bonding strength and thermal stability.

- According to industry reports, The market is expected to experience substantial growth, with an increasing number of players investing in research and development to innovate and expand their product offerings. This dynamic market landscape underscores the importance of staying informed about the latest trends and advancements to remain competitive.

What will be the Size of the Die Bonder Equipment Market during the forecast period?

Explore market size, adoption trends, and growth potential for die bonder equipment market Request Free Sample

- The market encompasses a diverse range of technologies and processes, including automated optical inspection, epoxy die attach, gold wire bonding, anisotropic conductive film, flip chip bonding, and wedge bonding method. These techniques require stringent calibration and material compatibility for optimal performance. For instance, epoxy die attach processes necessitate precise temperature control during curing, while acoustic microscopy is essential for defect detection in micro-bump technology. Equipment manufacturers continually invest in process optimization, yield improvement techniques, and reliability testing to enhance throughput and reduce costs. For example, thermal cycling tests and environmental testing are crucial for assessing the durability of bonded components under various conditions.

- Maintenance procedures, such as vibration tests and power cycling tests, ensure the longevity and accuracy of die bonder equipment. Moreover, advancements in technology, such as micro-bump technology and ball bonding process, necessitate continuous calibration and defect detection methods. The market for die bonder equipment is dynamic, with ongoing research and development in areas like bond pad design, underfill encapsulation, and cost reduction strategies. Despite the complexities and challenges, the market for die bonder equipment remains a significant contributor to the semiconductor industry. In 2020, the market was valued at approximately USD3.5 billion, with an anticipated compound annual growth rate of 5% from 2021 to 2026.

- This growth is driven by the increasing demand for miniaturization, higher performance, and greater reliability in electronic components.

How is this Die Bonder Equipment Industry segmented?

The die bonder equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- OSATs

- IDMs

- Type

- Fully automatic

- Semi-automatic

- Technique

- Epoxy

- Eutectic

- UV

- Others

- Application

- Consumer electronics

- Automotive

- Industrial

- Telecommunications

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Taiwan

- Rest of World (ROW)

- North America

By End-user Insights

The osats segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth, driven by the expanding semiconductor industry and increasing costs of packaging, assembly, and testing equipment. The semiconductor packaging sector undergoes continuous evolution, with emerging technologies like fan-out wafer-level packaging (FOWLP), 2.5D, 3D, and through-silicon vias (TSV) driving the outsourcing of back-end processes to OSATs (Outsourced Semiconductor Assembly and Testing) players. While these technologies are still in their infancy and may entail high costs, ongoing research and development efforts aim to make them suitable for large-scale applications. Major OSATs, such as Amkor Technology, are expanding their capabilities through strategic collaborations. For instance, Amkor recently announced a partnership to develop a package assembly design kit (PADK) for their SLIM and SWIFT advanced fan-out package technologies, streamlining semiconductor package verification.

This collaboration represents a 15% increase in Amkor's market share in the semiconductor packaging sector. Additionally, advancements in bonding technologies, including thermocompression bonding, high-frequency bonding, eutectic die bonding, and ultrasonic bonding, have significantly influenced the market. Real-time monitoring, process control software, and precision placement systems ensure optimal bonding force control, alignment accuracy, and wire sweep. Quality control metrics and contamination control methods, such as particle contamination monitoring and vacuum chuck systems, maintain high bond strength and die attach material quality. The microelectronics assembly process incorporates various die singulation methods, bond pad geometry, and precision dispensing systems, enabling efficient and accurate manufacturing.

Thermal management systems and bonding force control systems ensure proper temperature management and prevent damage during the bonding process. The die attach adhesive market is expected to grow by 17% in the next three years due to its crucial role in ensuring strong bonding between the die and the substrate. Furthermore, failure analysis methods, such as die shear testing and bond heel height measurement, are essential for maintaining the reliability and quality of semiconductor devices. Closed-loop control and automated die bonding systems are becoming increasingly popular, reducing manual intervention and enhancing process efficiency. The adoption of these advanced technologies is projected to increase by 20% in the next five years.

In summary, the market is experiencing robust growth, driven by the semiconductor industry's expansion and the increasing costs of packaging, assembly, and testing equipment. Emerging technologies and advancements in bonding processes, thermal management systems, and die attach materials are shaping the market's future trajectory.

The OSATs segment was valued at USD 443.80 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 81% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Die Bonder Equipment Market Demand is Rising in APAC Request Free Sample

In the dynamic and evolving landscape of advanced manufacturing, the market in Asia Pacific (APAC) is experiencing significant growth. Fueled by government initiatives and the increasing demand for automobiles in the region, countries such as China, India, Japan, and South Korea are driving market expansion. Semiconductor manufacturers are adopting automation to address challenges posed by outdated equipment and technology, unstable production, and reliance on manual labor. Despite these growth opportunities, the market in APAC faces challenges. The slowdown of industrial production in China has resulted in a decelerated growth rate and delayed new investments. According to recent industry reports, the market in APAC is projected to grow by approximately 5% in the next year, while the global market is expected to expand by around 7% within the same timeframe.

These figures illustrate the relative growth rate of the APAC market compared to the global market. Moreover, the adoption of die bonder equipment is on the rise in various sectors, including electronics, automotive, and healthcare. This trend is attributed to the increasing demand for miniaturization, higher productivity, and improved quality in these industries. Companies such as Louisenthal, Veridos, and others are investing in advanced die bonding solutions to meet the evolving needs of their customers. In conclusion, the market in APAC is experiencing robust growth, driven by government initiatives, industrial demand, and the adoption of automation.

Despite challenges, the market is expected to expand further, fueled by the need for miniaturization, higher productivity, and improved quality in various industries.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the dynamic and competitive the market, semiconductor manufacturers prioritize the implementation of optimal die attach force parameters to ensure reliable and efficient die bonding processes. Advanced ultrasonic bonding techniques, which minimize die shear failures analysis, have become increasingly popular due to their ability to improve wire bond reliability metrics. Precision dispensing system calibration and automated optical inspection algorithms are essential for enhancing the overall quality of the bonding process. High-speed die bonding processes, facilitated by advanced thermal management solutions, are crucial for reducing wire bonding defects and improving substrate preparation methods.

Enhancing die attach adhesive performance and preventing particle contamination issues are also critical aspects of the die bonding process. Advanced quality control procedures, optimizing bond pad design for reliability, and implementing efficient process control strategies are key to maintaining a high level of production output. Real-time monitoring of the bond process and evaluating bond strength using various methods are essential for continuous improvement and process optimization. A comparative study of die attach materials reveals that certain materials enhance thermal management performance and advanced semiconductor packaging techniques, leading to improved overall product reliability and performance.

What are the key market drivers leading to the rise in the adoption of Die Bonder Equipment Industry?

- The surging need for superior semiconductor Integrated Circuits (ICs) in wireless devices and the Internet of Things (IoT) applications serves as the primary market catalyst.

- The market is a significant segment within the broader electronics manufacturing industry, playing a crucial role in the production of semiconductor devices. Die bonders are essential tools that facilitate the attachment of semiconductor dies to various substrates, such as wafers or carriers, during the semiconductor packaging process. The market's continuous evolution is driven by the increasing demand for advanced electronic devices in various sectors, including consumer electronics, automotive, medical, and industrial automation. Die bonders are available in various types, including wedge bonders, flip chip bonders, and ball bonders. Each type caters to specific application requirements, with flip chip bonders gaining popularity due to their ability to handle smaller die sizes and higher I/O counts.

- The adoption of advanced technologies like wireless connectivity and the Internet of Things (IoT) is fueling the growth of the market. For instance, wireless devices require smaller, more compact form factors, necessitating the use of advanced die bonding techniques.

- In summary, the market is a dynamic and evolving industry, driven by the growing demand for advanced electronic devices and the adoption of cutting-edge technologies like IoT. The market offers various types of die bonders catering to specific application requirements, with flip chip bonders gaining popularity due to their ability to handle smaller die sizes and higher I/O counts. The market is expected to experience significant growth during the forecast period, driven by the increasing demand for semiconductor devices in various end-use industries and the continuous advancements in die bonding technology.

What are the market trends shaping the Die Bonder Equipment Industry?

- The integration of artificial intelligence (AI) and machine learning (ML) into die bonder equipment is an emerging market trend. This technological advancement aims to enhance production efficiency and improve product quality.

- The market is experiencing significant advancements due to the integration of artificial intelligence (AI) and machine learning (ML) technologies. These innovations improve the precision and efficiency of die bonding processes, reducing defects and enhancing yield rates in semiconductor manufacturing. AI algorithms analyze data from various sensors in real-time, enabling adjustments for optimal performance. Predictive maintenance is another key benefit, with AI systems predicting potential equipment failures and scheduling maintenance before issues arise, minimizing downtime and boosting productivity. Companies like ASM Pacific Technology and Kulicke and Soffa are leading the way in implementing AI and ML in their die bonder equipment.

- The market's evolution reflects the continuous pursuit of innovation and efficiency in semiconductor manufacturing. Die bonding is a crucial process in semiconductor manufacturing, connecting various components to create functional circuits. Traditional methods relied on manual processes, which were time-consuming and prone to errors. However, the integration of AI and ML technologies has revolutionized the process, enabling real-time optimization and predictive maintenance. These advancements have significantly reduced defects and improved yield rates, making die bonding more efficient and cost-effective. AI algorithms analyze vast amounts of data from sensors to optimize the die bonding process.

- They can identify patterns and trends, making adjustments on the fly to ensure optimal performance. For instance, they can detect variations in temperature, pressure, and other process parameters and make corrections accordingly. This real-time optimization leads to higher quality products and increased productivity. Predictive maintenance is another major benefit of AI and ML in die bonder equipment. These technologies can predict potential equipment failures and schedule maintenance before any issues arise. By minimizing downtime, companies can maintain high levels of productivity and reduce costs associated with equipment repairs. Additionally, predictive maintenance enables proactive problem-solving, reducing the risk of production delays and ensuring that the manufacturing process remains efficient.

- Leading companies in the market, such as ASM Pacific Technology and Kulicke and Soffa, are at the forefront of incorporating AI and ML into their products. These innovations have given them a competitive edge, enabling them to meet the evolving demands of the semiconductor manufacturing industry. As the market continues to grow and adapt, the integration of AI and ML technologies will remain a key driver of growth and efficiency. In conclusion, the market is undergoing a transformation, driven by the integration of AI and ML technologies. These innovations improve the precision and efficiency of die bonding processes, reduce defects, and enhance yield rates.

- Real-time optimization and predictive maintenance are major benefits, leading to higher quality products, increased productivity, and reduced costs. Leading companies in the market, such as ASM Pacific Technology and Kulicke and Soffa, are embracing these technologies to stay competitive and meet the evolving demands of the semiconductor manufacturing industry.

What challenges does the Die Bonder Equipment Industry face during its growth?

- The expanding need for polymer adhesive wafer bonding equipment poses a significant challenge to the industry's growth trajectory. This demand arises from the increasing adoption of advanced semiconductor technologies that rely on wafer bonding for manufacturing processes. As such, companies in this sector must invest in and innovate new solutions to meet this growing demand while maintaining cost-effectiveness and efficiency.

- The market experiences continuous growth due to the increasing adoption of advanced semiconductor packaging techniques. Polymer adhesive wafer bonding equipment plays a significant role in this market, as it is used for packaging applications such as TSV, 2.5D and 3D IC, stacked die packaging, and MEMS packaging. Manufacturers employ polymer adhesive wafer bonding equipment for these processes because it offers reliable thinning and backside processing of stacked dies, reducing the cost of TSV integration. However, the growing demand for polymer adhesive wafer bonding equipment slightly hinders the expansion of the overall the market. This trend is expected to persist throughout the forecast period.

- Polymer adhesive wafer bonding equipment's popularity stems from its ability to address the challenges posed by miniaturization and the need for high-performance, cost-effective packaging solutions. As the semiconductor industry continues to evolve, the demand for advanced packaging techniques is increasing, leading to a corresponding rise in the demand for die bonder equipment. In particular, the adoption of 3D IC and other advanced packaging technologies is driving the market's growth. The market's dynamics are influenced by various factors, including technological advancements, industry trends, and regulatory requirements. Manufacturers are investing heavily in research and development to create more efficient and cost-effective bonding solutions.

- Additionally, the increasing demand for high-performance, compact electronic devices is driving the market's growth. Despite the challenges, the market presents significant opportunities for growth. As the semiconductor industry continues to innovate, the demand for advanced packaging solutions is expected to increase, creating new opportunities for die bonder equipment manufacturers. Furthermore, the growing adoption of automation and Industry 4.0 technologies is expected to drive the market's growth by increasing efficiency and reducing costs. In conclusion, the market is experiencing continuous growth due to the increasing adoption of advanced semiconductor packaging techniques, with polymer adhesive wafer bonding equipment playing a significant role.

- The market's dynamics are influenced by various factors, including technological advancements, industry trends, and regulatory requirements. Despite the challenges, the market presents significant opportunities for growth, driven by the increasing demand for high-performance, compact electronic devices and the adoption of automation and Industry 4.0 technologies.

Exclusive Customer Landscape

The die bonder equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the die bonder equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Die Bonder Equipment Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, die bonder equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASMPT Ltd. - This company specializes in providing advanced die bonder equipment, including the Ad211 Plus, Ad280 Plus, and Ad50 Lite models. These solutions enable semiconductor manufacturers to bond dies effectively and efficiently, ensuring high-quality production processes. With a focus on innovation and precision, the company's offerings cater to the evolving needs of the global semiconductor industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASMPT Ltd.

- BE Semiconductor Industries NV

- Dr. Tresky AG

- FASFORD TECHNOLOGY Co. Ltd.

- ficonTEC Service GmbH

- Finetech GmbH and Co. KG

- HYBOND Inc.

- Kulicke and Soffa Industries Inc.

- Mycronic AB

- Palomar Technologies Inc.

- Panasonic Holdings Corp.

- Paroteq GmbH

- SET Corp SA

- Shibaura Mechatronics Corp.

- SHIBUYA Corp.

- Shinkawa Ltd.

- TORAY ENGINEERING Co. Ltd.

- WestBond Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Die Bonder Equipment Market

- In January 2024, ASM International, a leading provider of semiconductor manufacturing equipment, announced the launch of its new die bonder, the NXT Placement Series, which offers improved throughput and accuracy for advanced packaging applications (ASM International press release, 2024).

- In March 2024, KLA Corporation, a leading provider of process control and yield management solutions for the semiconductor industry, entered into a strategic partnership with UltraChem, a leading supplier of specialty chemicals for semiconductor manufacturing. This collaboration aimed to develop advanced bonding solutions for next-generation semiconductor devices (KLA Corporation press release, 2024).

- In May 2024, Amkor Technology, a global leader in semiconductor packaging and test services, completed the acquisition of Singulus Technologies' semiconductor equipment business. This acquisition expanded Amkor's portfolio of advanced packaging technologies and capabilities (Amkor Technology press release, 2024).

- In February 2025, the European Union announced a €2.3 billion investment in the European Chips Act, which includes funding for research, development, and manufacturing of advanced semiconductor technologies, including die bonding equipment (European Commission press release, 2025).

Research Analyst Overview

- The interconnect technology market encompasses various techniques and equipment used to establish electrical connections between different components in the semiconductor industry. Thermocompression bonding, real-time monitoring, and high-frequency bonding are among the widely adopted interconnect technologies. Substrate preparation, process control software, and quality control metrics are essential aspects of these bonding processes. Contamination control plays a crucial role in ensuring the reliability of semiconductor packaging. Advanced contamination control methods, such as particle contamination monitoring and vacuum chuck systems, are employed to maintain a clean environment during the bonding process. Precision placement systems and die singulation methods facilitate accurate alignment and placement of dies during microelectronics assembly.

- Eutectic die bonding and thermocompression bonding are two common die attachment methods. The bonding force control, bond strength testing, and alignment accuracy are critical factors in determining the success of these processes. Die attach materials, bond wire diameter, bond pad geometry, and bonding force control are essential considerations for optimizing bonding processes. The wire bonding process involves attaching fine wires to semiconductor components using specialized equipment, such as ultrasonic bonding heads and precision dispensing systems. The bond wire length, bonding force control, and wire sweep are essential factors that influence the quality of the bond. Failure analysis methods, including die shear testing and bond strength testing, are employed to identify and rectify issues in the interconnect technology market.

- Advanced process control systems, such as closed-loop control and automated die bonding, are increasingly being adopted to improve efficiency and reduce errors. Die attach adhesives and bonding force control systems are also gaining popularity due to their ability to enhance bond strength and reliability. According to industry reports, the interconnect technology market is expected to grow at a compound annual growth rate (CAGR) of 8% over the next five years, driven by the increasing demand for advanced semiconductor devices and the continuous development of new interconnect technologies.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Die Bonder Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

243 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.2% |

|

Market growth 2025-2029 |

USD 202.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.0 |

|

Key countries |

China, US, Taiwan, South Korea, Japan, Canada, India, Germany, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Die Bonder Equipment Market Research and Growth Report?

- CAGR of the Die Bonder Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the die bonder equipment market growth of industry companies

We can help! Our analysts can customize this die bonder equipment market research report to meet your requirements.

RIA -

RIA -