Diisocyanates And Polyisocyanates Market Size 2026-2030

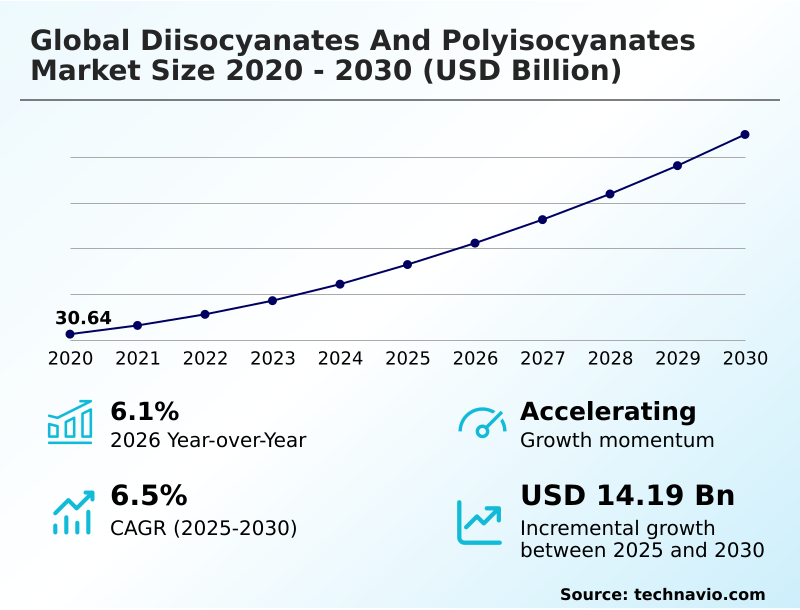

The diisocyanates and polyisocyanates market size is valued to increase by USD 14.19 billion, at a CAGR of 6.5% from 2025 to 2030. Exponential growth in construction sector will drive the diisocyanates and polyisocyanates market.

Major Market Trends & Insights

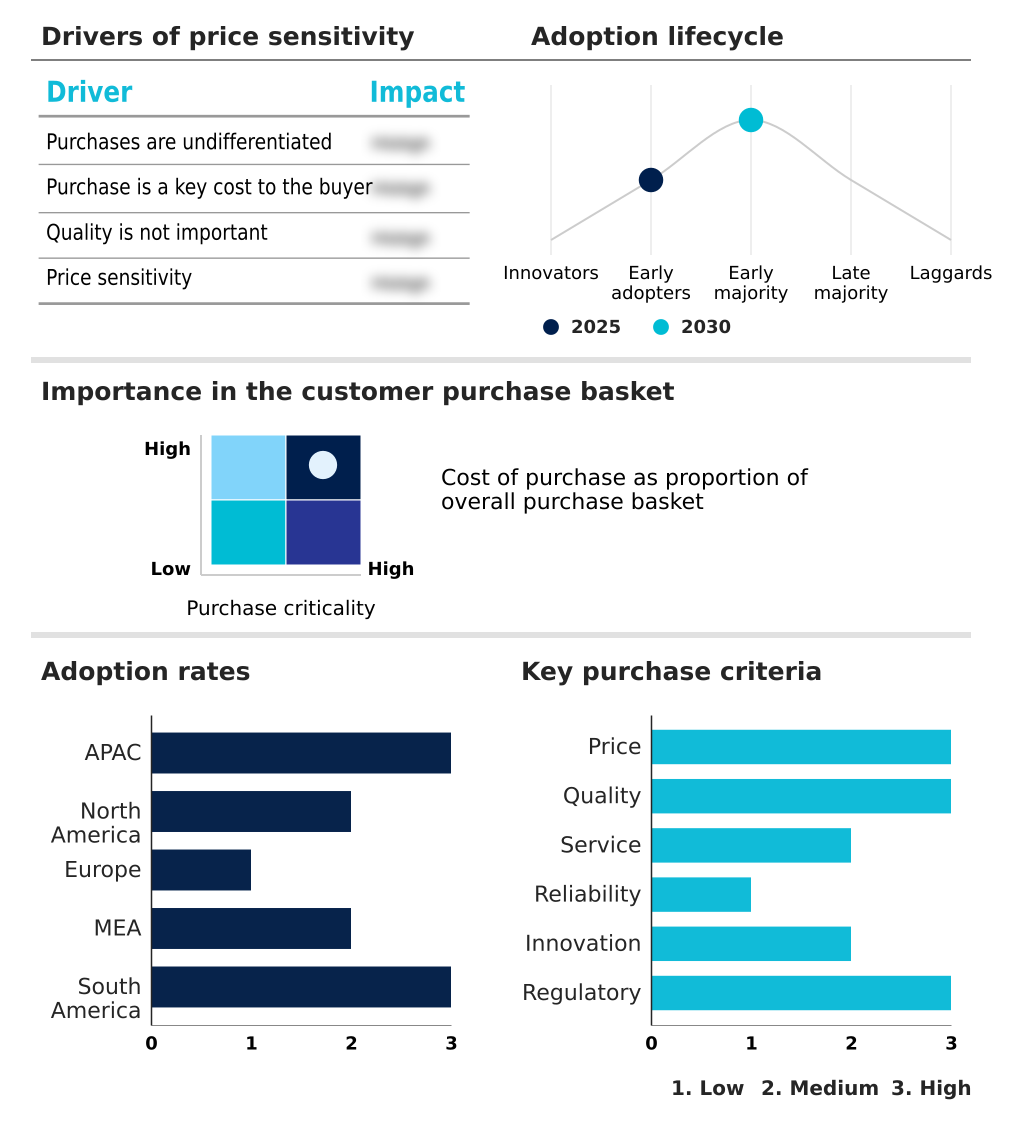

- APAC dominated the market and accounted for a 55% growth during the forecast period.

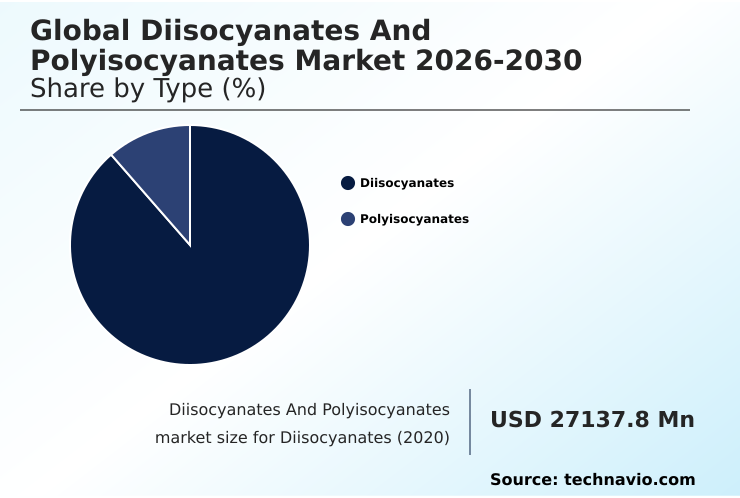

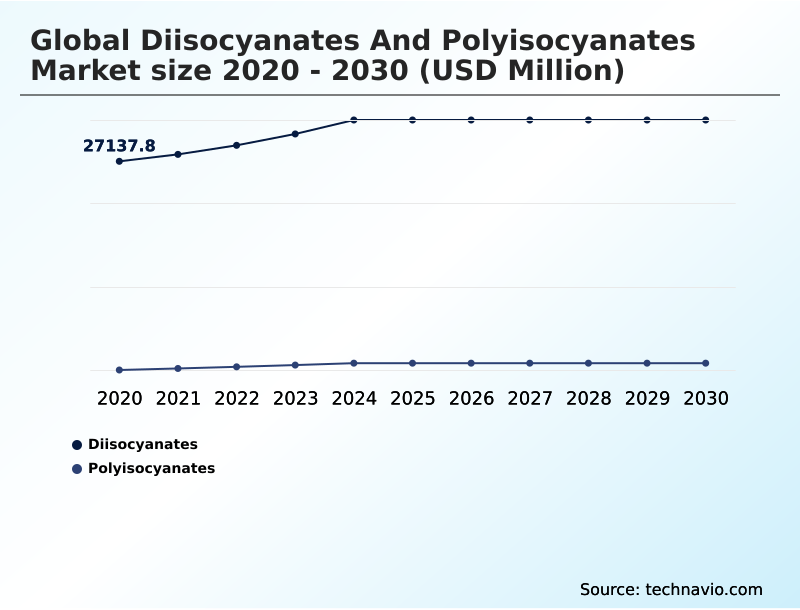

- By Type - Diisocyanates segment was valued at USD 31.82 billion in 2024

- By Application - Coating segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 21.78 billion

- Market Future Opportunities: USD 14.19 billion

- CAGR from 2025 to 2030 : 6.5%

Market Summary

- The diisocyanates and polyisocyanates market is foundational to modern manufacturing, providing the essential building blocks for polyurethane-based materials used across automotive, construction, and consumer goods. Growth is propelled by the increasing demand for lightweight, durable, and energy-efficient products. For instance, the automotive industry relies on polyurethane foams and composites to reduce vehicle weight and meet stringent emission standards.

- A primary trend involves the shift toward sustainability, with significant R&D focused on bio-based feedstocks and phosgene-free synthesis to mitigate environmental impact and health concerns associated with traditional isocyanate-terminated prepolymers. As a business scenario, an automotive OEM must balance the performance benefits of polycarbodiimide chemistry in high-strength adhesives with the supply chain risks tied to volatile petrochemical feedstock prices.

- This dynamic is complicated by stringent regulations governing workplace exposure to monomeric diisocyanates. Consequently, optimizing the isocyanate index to achieve desired properties while ensuring cost-effectiveness and compliance remains a critical challenge for producers and end-users, influencing innovation around the core urethane linkage and overall polymer backbone structure.

What will be the Size of the Diisocyanates And Polyisocyanates Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Diisocyanates And Polyisocyanates Market Segmented?

The diisocyanates and polyisocyanates industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Diisocyanates

- Polyisocyanates

- Application

- Coating

- Foam

- Adhesive

- Others

- Grade type

- Industrial grade

- Specialty grade

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The diisocyanates segment is estimated to witness significant growth during the forecast period.

The diisocyanates and polyisocyanates market is segmented based on chemical structure, end-use application, and performance grade. Key distinctions are made between diisocyanates such as methylene diphenyl diisocyanate and polyisocyanates, which define the final properties of polyurethane polymers.

Applications including high-performance coatings and flexible and rigid foams represent major consumption channels, driven by industries seeking durable adhesive solutions and superior thermal insulation materials.

The market is further delineated by grade, with industrial grades for large-scale uses and specialty grades for niche requirements like non-yellowing aliphatic coatings.

APAC accounts for 55% of the incremental growth, underscoring its dominance in manufacturing lightweight automotive components and energy-efficient building materials that rely on advanced isocyanate chemistry and polyurethane synthesis reaction. These segments collectively influence supply chain strategies.

The Diisocyanates segment was valued at USD 31.82 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 55% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Diisocyanates And Polyisocyanates Market Demand is Rising in APAC Request Free Sample

The market's geographic landscape is led by APAC, which accounts for 55% of the growth and is expanding at a regional rate of 6.8%.

This dominance is fueled by robust manufacturing in construction and automotive sectors, demanding vast quantities of polyurethane dispersion and one-component foam. North America focuses on high-performance applications, including casting polyurethanes for industrial parts and reaction injection molding for complex components.

The region prioritizes polyurethane potting compounds and advanced adhesive bonding technology. Europe, with its stringent regulations, drives innovation in waterborne polyurethane adhesives and cycloaliphatic diisocyanates for eco-friendly surface coating formulation.

Established supply chains for two-component systems and blocked isocyanates in these developed regions contrast with emerging markets where infrastructure for specialty chemicals is still developing.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic application of diisocyanates and polyisocyanates is becoming highly specialized, driving innovation across multiple sectors. The use of MDI applications in rigid foam insulation is a cornerstone of energy-efficient construction, with advancements in spray foam insulation for building envelopes allowing for superior air sealing.

- For consumer products, TDI use in flexible foam cushioning continues to evolve for enhanced comfort and durability. In high-performance sectors, the focus is on specialized formulations, such as aliphatic polyisocyanate for automotive coatings, which provides exceptional UV resistance. Concurrently, the industry is proactively developing bio-based alternatives to isocyanates and reducing VOCs in polyurethane coatings to meet regulations.

- This includes formulating high-solids polyurethane systems and developing blocked isocyanates for one-component coatings. The versatility is evident in diverse uses, from polyurethane elastomers for industrial applications to thermoplastic polyurethane in medical devices. Adhesion science is also advancing with polyurethane adhesives for composite bonding. Formulators are using polyols to modify polyurethane properties and deploying isocyanate prepolymers for cast elastomers.

- Furthermore, waterborne polyurethane dispersions for wood finishes are gaining share, while polyisocyanates as crosslinkers for sealants enhance durability. Manufacturers are also improving fire retardancy of polyurethane foams and using polyurethane potting compounds for electronics. Ensuring safety measures for handling diisocyanates remains paramount across all applications, including polyurethane binders for reconstituted wood.

- Companies adopting these solutions report product failure rates up to 50% lower than those using generic formulations.

What are the key market drivers leading to the rise in the adoption of Diisocyanates And Polyisocyanates Industry?

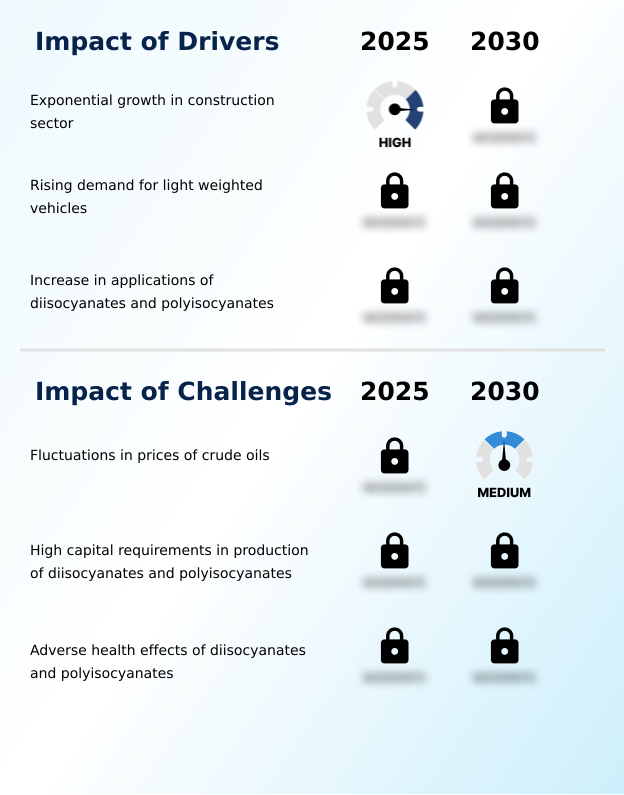

- The exponential growth of the global construction sector is a key driver for the diisocyanates and polyisocyanates market.

- Market growth is fundamentally driven by expanding applications in core industrial sectors. The construction industry's demand for spray polyurethane foam for insulation contributes significantly, with proper application reducing building energy consumption by up to 30%.

- In the automotive sector, the push for lightweighting has increased the use of polyurethane composites and foams, where a 10% weight reduction can improve fuel efficiency by nearly 7%.

- The versatility of aromatic isocyanates and polyol components enables the creation of materials for everything from flexible foam cushioning in furniture to robust structural adhesives.

- This broad utility, combined with the superior performance of chemical resistant polymers in automotive refinish coatings and footwear sole manufacturing, ensures sustained demand and drives ongoing material development.

What are the market trends shaping the Diisocyanates And Polyisocyanates Industry?

- Technological advancements in the production of diisocyanates and polyisocyanates are emerging as a significant market trend, shaping both manufacturing efficiency and product innovation.

- Key market trends are driven by innovation in production and formulation, with a strong focus on sustainability. The development of bio-based isocyanates is gaining momentum, with new processes improving yields by up to 15% compared to conventional methods. This shift addresses both regulatory pressures and demand for sustainable polyurethane solutions.

- Companies are also adopting phosgene-free synthesis and other advanced prepolymer technology to enhance safety and efficiency. Collaborations are accelerating the adoption of low-VOC formulations and high-solids coatings, with joint ventures reporting a 20% faster path to commercialization for new industrial coating systems.

- These advancements in polyurethane recycling processes and the creation of epoxy-polyurethane hybrids are reshaping the competitive landscape, pushing the industry toward a circular economy model.

What challenges does the Diisocyanates And Polyisocyanates Industry face during its growth?

- Fluctuations in crude oil prices present a key challenge affecting the growth of the diisocyanates and polyisocyanates industry.

- Significant challenges confront the market, led by raw material cost volatility. As petrochemical feedstocks are the primary source, crude oil price swings can alter production costs by over 20% in a single quarter, compressing margins on products like toluene diisocyanate and hexamethylene diisocyanate.

- High capital expenditure for new facilities and stringent safety regulations surrounding monomeric diisocyanates act as barriers to entry. Developing safer handling protocols and isocyanate hardeners adds complexity. Moreover, the industry faces scrutiny over the lifecycle of elastomeric materials, pushing for better elastomer processing and end-of-life solutions.

- Firms that successfully navigate these issues, perhaps by optimizing foam density control or adopting solventborne polyurethane coatings with better environmental profiles, can gain a competitive edge.

Exclusive Technavio Analysis on Customer Landscape

The diisocyanates and polyisocyanates market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the diisocyanates and polyisocyanates market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Diisocyanates And Polyisocyanates Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, diisocyanates and polyisocyanates market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anhui Sinograce Chemical - The market provides essential diisocyanates and polyisocyanates, foundational for high-performance coatings, durable adhesives, and versatile polyurethane foams across key industrial sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anhui Sinograce Chemical

- Asahi Kasei Corp.

- BASF SE

- BorsodChem

- Cosmos Plastics and Chemicals

- Covestro AG

- DIC Corp.

- Dow Chemical Co.

- Evonik Industries AG

- Huntsman International LLC

- Jiahua Chemical Co. Ltd.

- Merck KGaA

- Mitsui Chemicals Inc.

- N Shashikant and Co.

- Prakash Chemicals Intl. Ltd.

- Prasol Chemicals Ltd.

- Shandong INOV Polyurethane Co.

- Super Urecoat Industries

- Tosoh Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Diisocyanates and polyisocyanates market

- In September 2024, InnovaChem Solutions launched a new line of bio-based polyisocyanates derived from renewable feedstocks, aiming to reduce the carbon footprint of polyurethane coatings by up to 30%.

- In December 2024, PolyVantage Group and EcoResin Technologies announced a strategic partnership to build a pilot plant for the chemical recycling of post-consumer polyurethane foam, with an initial capacity of 5,000 metric tons per year.

- In February 2025, Global Materials Inc. completed its acquisition of specialty chemicals firm Adhesives & Polymers Co. for USD 150 million, expanding its portfolio of high-performance structural adhesives for the automotive and aerospace industries.

- In May 2025, DuraCoat Technologies received regulatory approval for its new phosgene-free synthesis process for aliphatic diisocyanates, enabling cleaner production and reducing workplace hazards at its European manufacturing sites.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Diisocyanates And Polyisocyanates Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2026-2030 | USD 14185.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The diisocyanates and polyisocyanates market is defined by its critical role in producing versatile polyurethane polymers. Core to this are isocyanate functional groups that form a strong urethane linkage upon reaction. Key chemicals include methylene diphenyl diisocyanate and toluene diisocyanate for flexible and rigid foams, and aliphatic polyisocyanate and aromatic isocyanates for high-performance coatings.

- Boardroom decisions are increasingly influenced by the shift away from traditional petrochemical feedstocks toward sustainable alternatives. This strategic pivot involves significant investment in phosgene-free synthesis and prepolymer technology for creating isocyanate-terminated prepolymers. Advanced low-VOC formulations, such as waterborne polyurethane adhesives and moisture-curing adhesives, are becoming standard.

- Formulators utilize isocyanate hardeners and crosslinking agents for coatings to develop robust two-component systems and structural adhesives. Innovation is also seen in thermoplastic polyurethane, casting polyurethanes, and elastomeric materials using specialized polyol components. Products like one-component foam and spray polyurethane foam are optimized through reaction injection molding.

- The development of blocked isocyanates and polycarbodiimide chemistry has improved chemical resistant polymers and polyurethane dispersion. This focus on R&D, exploring materials from hexamethylene diisocyanate to novel polyurethane binders with a controlled isocyanate index, has led to operational gains, with some advanced processes reducing waste by 15%.

What are the Key Data Covered in this Diisocyanates And Polyisocyanates Market Research and Growth Report?

-

What is the expected growth of the Diisocyanates And Polyisocyanates Market between 2026 and 2030?

-

USD 14.19 billion, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Diisocyanates, and Polyisocyanates), Application (Coating, Foam, Adhesive, and Others), Grade Type (Industrial grade, and Specialty grade) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Exponential growth in construction sector, Fluctuations in prices of crude oils

-

-

Who are the major players in the Diisocyanates And Polyisocyanates Market?

-

Anhui Sinograce Chemical, Asahi Kasei Corp., BASF SE, BorsodChem, Cosmos Plastics and Chemicals, Covestro AG, DIC Corp., Dow Chemical Co., Evonik Industries AG, Huntsman International LLC, Jiahua Chemical Co. Ltd., Merck KGaA, Mitsui Chemicals Inc., N Shashikant and Co., Prakash Chemicals Intl. Ltd., Prasol Chemicals Ltd., Shandong INOV Polyurethane Co., Super Urecoat Industries and Tosoh Corp.

-

Market Research Insights

- Market dynamics are shaped by a convergence of demand for high-performance materials and a push for sustainability. Industries are leveraging durable adhesive solutions and weather-resistant coatings to extend product lifecycles, with some advanced formulations improving weatherability by up to 40% over conventional products.

- The adoption of thermal insulation materials in construction has demonstrated a reduction in building energy costs by as much as 25%. Concurrently, isocyanate chemistry is evolving, with bio-based isocyanates emerging as viable alternatives that support corporate sustainability mandates.

- This transition is supported by advancements in polyurethane synthesis reaction processes, enabling the creation of lightweight automotive components and energy-efficient building materials that meet both performance and environmental criteria, driving innovation across the value chain.

We can help! Our analysts can customize this diisocyanates and polyisocyanates market research report to meet your requirements.