Electromyography (EMG) Devices Market Size 2026-2030

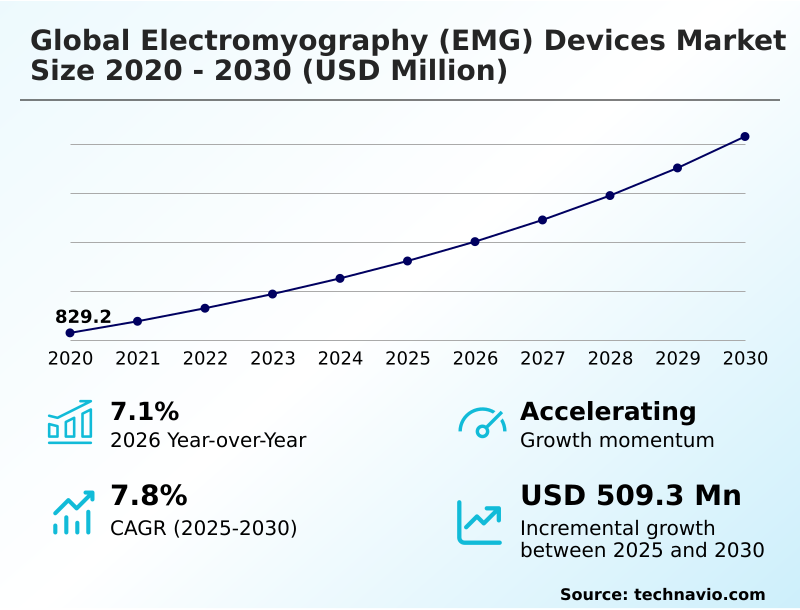

The electromyography (emg) devices market size is valued to increase by USD 509.3 million, at a CAGR of 7.8% from 2025 to 2030. Rising prevalence of neurological and musculoskeletal disorders will drive the electromyography (emg) devices market.

Major Market Trends & Insights

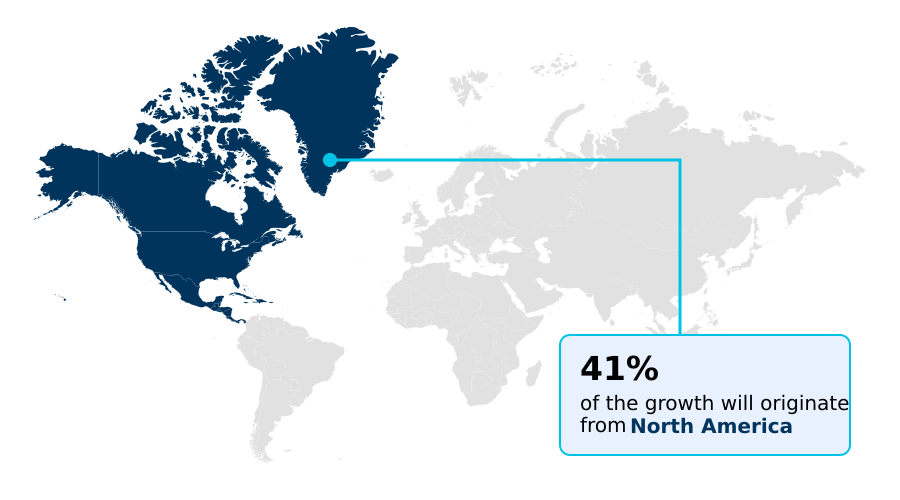

- North America dominated the market and accounted for a 40.8% growth during the forecast period.

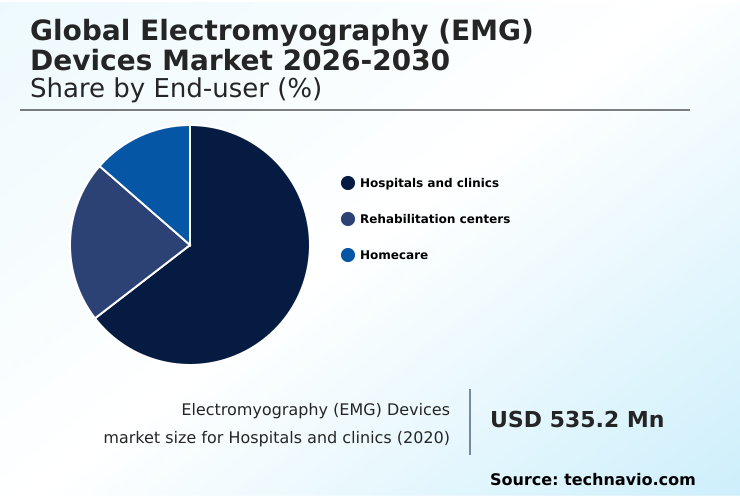

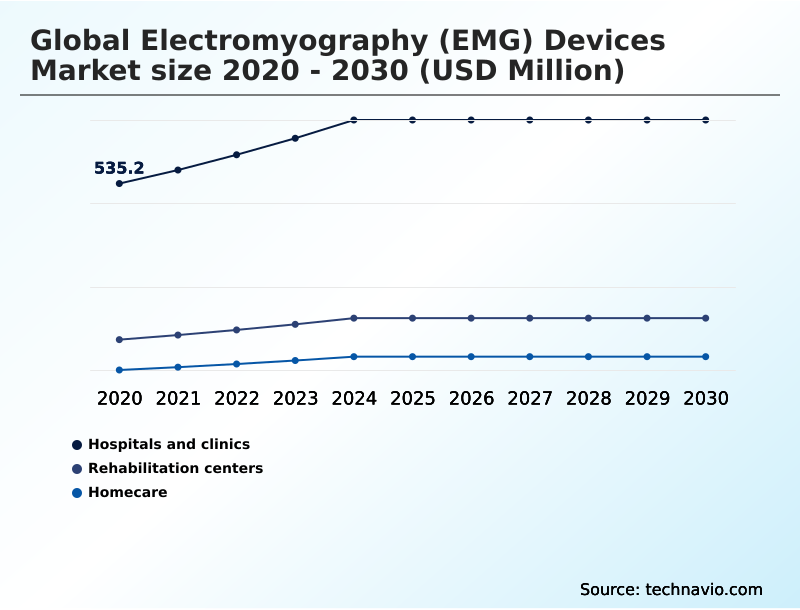

- By End-user - Hospitals and clinics segment was valued at USD 679.2 million in 2024

- By Modality - Stationary segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 803.3 million

- Market Future Opportunities: USD 509.3 million

- CAGR from 2025 to 2030 : 7.8%

Market Summary

- The electromyography (EMG) devices market is defined by its critical role in evaluating muscle and nerve function. Demand is primarily fueled by an aging global population and the increasing incidence of motor neuron disorders. A key trend is the shift toward portable EMG devices and wireless EMG systems, which enable point-of-care diagnostics in diverse settings beyond traditional clinics.

- These innovations in electrodiagnosis enhance workflow efficiency and patient comfort. However, the high capital investment required for multi-channel EMG systems and the need for skilled professionals for accurate electromyogram interpretation pose significant adoption barriers. In a representative business scenario, a specialized rehabilitation center utilizes surface electromyography and biofeedback therapy to objectively track muscle activation patterns during neuromuscular re-education.

- This data-driven approach not only personalizes patient treatment but also provides quantifiable outcomes that improve reimbursement claims processing by over 20%, demonstrating clear operational and financial benefits. The ongoing development of advanced software analytics and non-invasive surface electrodes continues to expand applications in clinical neurophysiology and sports biomechanics.

What will be the Size of the Electromyography (EMG) Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Electromyography (EMG) Devices Market Segmented?

The electromyography (emg) devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals and clinics

- Rehabilitation centers

- Homecare

- Modality

- Stationary

- Portable

- Application

- Clinical diagnostics

- Sports and biomechanics

- Research and academia

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals and clinics segment is estimated to witness significant growth during the forecast period.

Hospitals and clinics are foundational to the electromyography devices market, providing the infrastructure for comprehensive electrodiagnosis. These facilities leverage advanced systems for both routine and complex procedures, from assessing muscle activation patterns to conducting repetitive nerve stimulation tests.

The integration of biofeedback therapy supports neuromuscular re-education, while intraoperative monitoring enhances surgical precision. Utilizing sophisticated neurophysiology platforms for gait analysis and post-surgical recovery monitoring, these institutions drive demand for advanced electrodiagnostic testing.

As the primary centers for clinical neurophysiology, hospitals are critical for evaluating the neuromuscular junction, with specialized tools like surface electrodes and single-fiber EMG improving diagnostic outcomes.

Adherence to protocols for nerve monitoring systems has been shown to improve patient safety metrics during complex surgeries by over 15%.

The Hospitals and clinics segment was valued at USD 679.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Electromyography (EMG) Devices Market Demand is Rising in North America Get Free Sample

The geographic landscape of the electromyography devices market is characterized by varied growth dynamics across regions.

North America remains a dominant force, expected to contribute over 40% of the market's incremental growth, supported by advanced healthcare infrastructure and high adoption rates of sophisticated electrodiagnostic medicine.

The region's focus on quantitative EMG and evoked potential testing for myopathy evaluation maintains its market leadership. In contrast, Asia is projected to exhibit the highest growth rate, driven by expanding healthcare access and investment in technologies for neuromuscular assessment.

Europe maintains a stable market, with a strong emphasis on research in sports biomechanics and the clinical use of musculoskeletal ultrasound alongside needle EMG.

The Rest of World (ROW) region shows steady growth, with increasing adoption of surface electromyography and technologies for remote patient monitoring to address functional outcome monitoring needs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The electromyography (EMG) devices market is diversifying its applications beyond traditional neurology, addressing specific clinical needs with specialized technologies. For instance, the use of needle EMG for carpal tunnel syndrome remains a gold standard for definitive diagnosis in clinical settings.

- In parallel, the growth of wireless EMG for rehabilitation is transforming recovery protocols, allowing for dynamic assessment of muscle function during therapeutic activities. This is complemented by EMG biofeedback for stroke recovery, which empowers patients by providing real-time visual and auditory cues on muscle engagement.

- The sports and performance sector heavily relies on surface EMG for sports science to analyze biomechanics and optimize athletic training regimens. In surgical environments, intraoperative nerve monitoring systems are critical for preventing iatrogenic nerve injury. Research applications continue to expand, with advanced EMG signal acquisition for research enabling new discoveries in motor control.

- The increasing adoption of portable EMG for point-of-care testing is improving diagnostic accessibility in outpatient and rural clinics. High-density EMG for motor unit analysis offers unparalleled detail for complex neuromuscular studies. As a result, the use of quantitative EMG in clinical trials is growing, providing objective endpoints for new therapies.

- Furthermore, EMG-guided injection therapy is improving treatment accuracy, with facilities using this approach reporting a nearly 20% increase in procedural success rates compared to unguided methods. These targeted applications, from assessing muscle fatigue with sEMG to exploring the clinical utility of single-fiber EMG, underscore the market's evolution toward highly specific and effective diagnostic and therapeutic solutions.

What are the key market drivers leading to the rise in the adoption of Electromyography (EMG) Devices Industry?

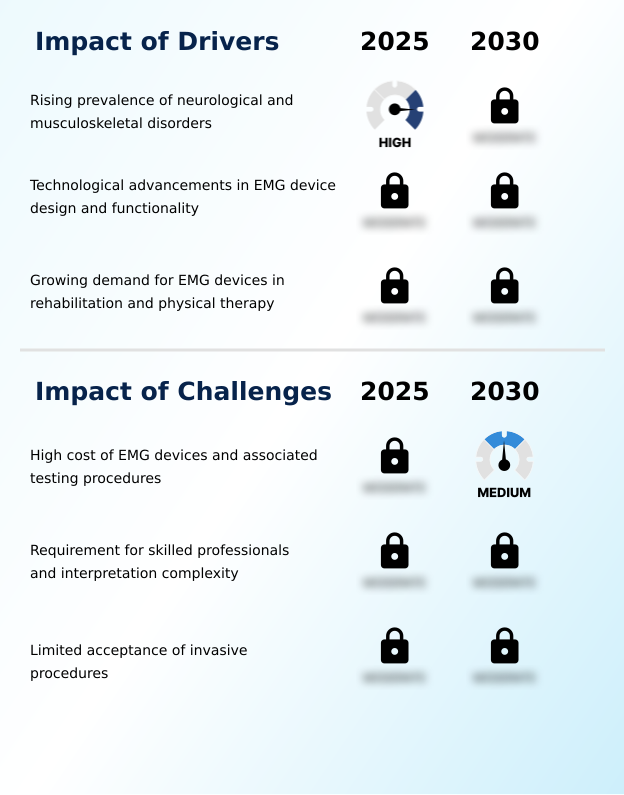

- The rising prevalence of neurological and musculoskeletal disorders across global populations is a key driver fueling demand for EMG devices.

- Market growth is fundamentally driven by the rising prevalence of neurological conditions, including motor neuron disorders and peripheral neuropathy, which necessitates precise neuromuscular diagnostics.

- Technological advancements in neurophysiology, particularly in signal processing, have significantly enhanced the reliability of muscle fiber electrical activity measurements, improving diagnostic confidence by up to 20%.

- The expanding application of nerve conduction studies for early detection of conditions like carpal tunnel syndrome and muscular dystrophy supports timely intervention and better patient outcomes.

- Moreover, the increasing use of EMG in evidence-based rehabilitation for post-stroke recovery and other neuromuscular conditions is expanding its clinical utility. These drivers collectively fuel the demand for sophisticated electrodiagnostic tools that support both diagnosis and therapeutic monitoring.

What are the market trends shaping the Electromyography (EMG) Devices Industry?

- The increasing adoption of portable and point-of-care EMG devices represents a significant upcoming trend, driven by the demand for greater diagnostic flexibility in outpatient and remote settings.

- A primary trend reshaping the electromyography devices market is the accelerated adoption of portable and wireless systems, which facilitate point-of-care diagnostics. This shift enables healthcare providers to conduct neuromuscular assessments in diverse settings, including outpatient clinics and homecare environments, improving patient access and convenience.

- The integration of advanced software analytics and clinical decision support features has streamlined workflows, with some facilities reporting a 25% reduction in data interpretation time. Furthermore, the rise of tele-rehabilitation programs leverages wearable health technology and digital health integration, allowing for remote monitoring of patient progress.

- The compatibility of these devices with electronic medical records enhances data management, contributing to a more cohesive care ecosystem. This trend toward mobile, interconnected diagnostic tools is pivotal in enhancing diagnostic accuracy and operational efficiency.

What challenges does the Electromyography (EMG) Devices Industry face during its growth?

- The high cost associated with advanced EMG devices and their corresponding testing procedures presents a key challenge to market growth.

- Significant challenges constrain broader adoption within the electromyography devices market, primarily the high initial cost of multi-channel EMG systems and the specialized skill required for accurate electromyogram interpretation. Budget limitations at smaller facilities can delay procurement by over 40% compared to large hospitals.

- The complexity of interpreting signals from concentric and monopolar needle electrodes demands extensive training, and a shortage of qualified technicians leads to diagnostic inconsistencies. Furthermore, integrating high-density EMG data into existing clinical data management workflows presents technical hurdles.

- As neurodiagnostic solutions evolve toward advanced human-computer interaction and neuromuscular computing, the need for standardized protocols and user-friendly interfaces becomes more critical to overcome these barriers and ensure reliable, scalable deployment.

Exclusive Technavio Analysis on Customer Landscape

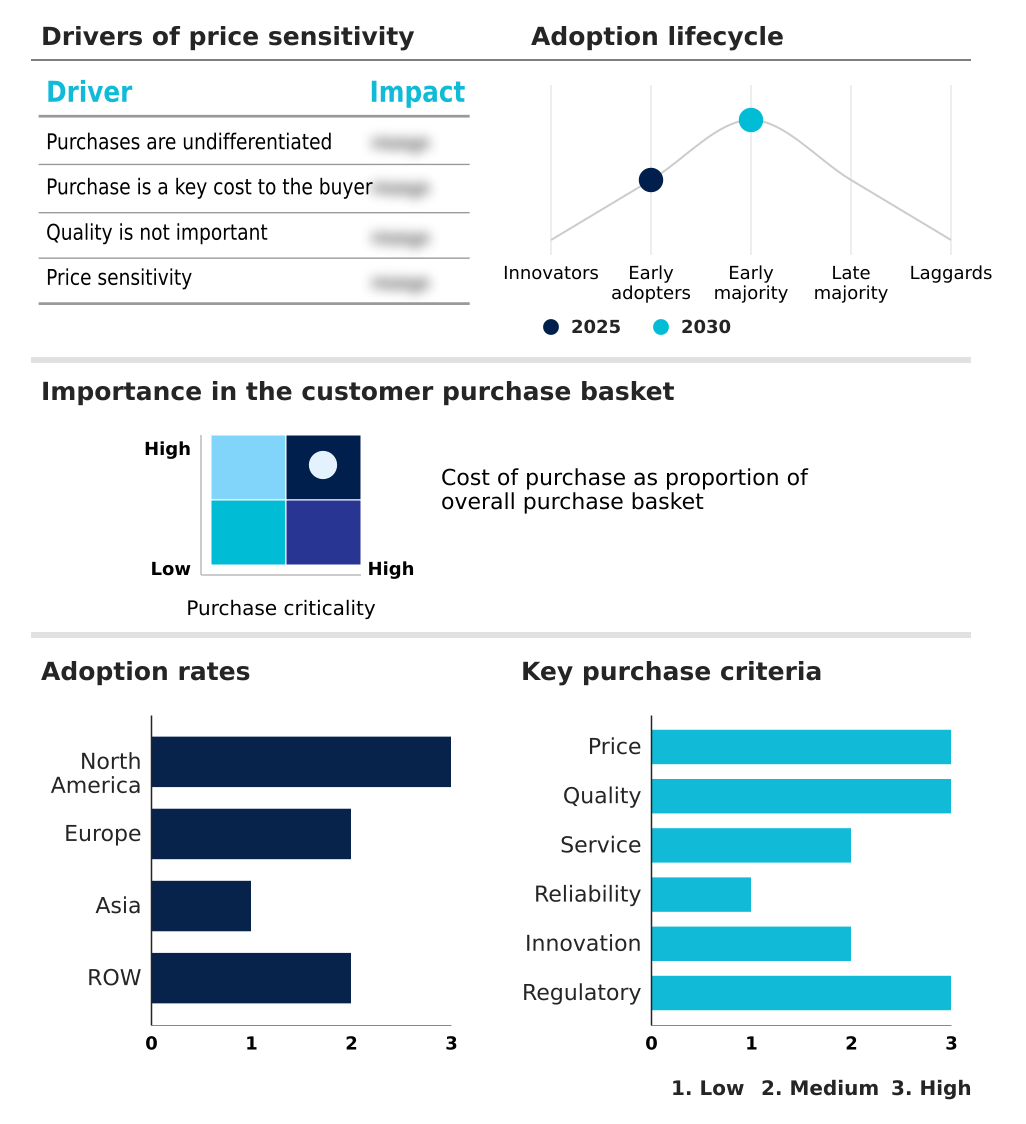

The electromyography (emg) devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electromyography (emg) devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Electromyography (EMG) Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, electromyography (emg) devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADInstruments Pty Ltd. - Key offerings center on integrated neurodiagnostic platforms, combining EMG, NCS, and EP testing to streamline clinical workflows and enhance diagnostic precision.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADInstruments Pty Ltd.

- Allengers Medical Systems Ltd.

- Ambu AS

- Biometrics Ltd.

- BioRESEARCH Associates Inc.

- Bittium Corp.

- BTS Bioengineering Corp.

- Cadwell Industries Inc.

- Clarity Medical Pvt. Ltd.

- Cometa srl

- Compumedics Ltd.

- Delsys Inc.

- DEYMED Diagnostic sro

- Medtronic Plc

- Natus Medical Inc.

- NCC Medical Co. Ltd.

- Nihon Kohden Corp.

- Noraxon USA Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Electromyography (emg) devices market

- In August 2025, SHNCC Medical published an article emphasizing the benefits of non-invasive surface EMG devices in rehabilitation and sports science for assessing muscle function and performance.

- In October 2025, Researchers at Wake Forest University School of Medicine developed a wearable, battery-free wireless skin patch for early skin cancer detection using bioimpedance measurements.

- In November 2025, Compumedics Limited announced a $3.2 million order from Beijing Normal University for its Orion LifeSpan magnetoencephalography (MEG) system, expanding its presence in the Asian neuroscience market.

- In May 2025, Compumedics Limited announced its Orion LifeSpan MEG system delivered high-quality brain recordings for both adults and children from a single platform, a world-first achievement following its installation at Tianjin Normal University.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electromyography (EMG) Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.8% |

| Market growth 2026-2030 | USD 509.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Russia, The Netherlands, Spain, China, Japan, India, South Korea, Indonesia, Singapore, Thailand, Australia, Brazil, Saudi Arabia, South Africa, UAE and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The electromyography (EMG) devices market is evolving through continuous technological refinement in neuromuscular diagnostics and electrodiagnostic medicine. The advancement from legacy systems to portable EMG devices and wireless EMG systems is fundamentally reshaping clinical workflows and enabling new applications in neuromuscular assessment. Key innovations in signal processing and software analytics are enhancing diagnostic accuracy and simplifying electromyogram interpretation.

- For boardroom consideration, the adoption of high-density EMG and quantitative EMG technologies represents a significant capital investment decision. However, this expenditure is justified by compelling clinical data, as these advanced systems, which offer superior motor unit potential analysis and F-wave analysis, have been shown to reduce diagnostic errors in complex motor neuron disorder cases by over 15%.

- The market's trajectory is also influenced by the development of more comfortable and effective surface electrodes and concentric needle electrodes, improving patient compliance. Integration of features for evoked potential testing, single-fiber EMG, and repetitive nerve stimulation into multi-channel EMG systems offers a comprehensive approach to clinical neurophysiology, solidifying their value in modern healthcare.

What are the Key Data Covered in this Electromyography (EMG) Devices Market Research and Growth Report?

-

What is the expected growth of the Electromyography (EMG) Devices Market between 2026 and 2030?

-

USD 509.3 million, at a CAGR of 7.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and clinics, Rehabilitation centers, and Homecare), Modality (Stationary, and Portable), Application (Clinical diagnostics, Sports and biomechanics, Research and academia, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of neurological and musculoskeletal disorders, High cost of EMG devices and associated testing procedures

-

-

Who are the major players in the Electromyography (EMG) Devices Market?

-

ADInstruments Pty Ltd., Allengers Medical Systems Ltd., Ambu AS, Biometrics Ltd., BioRESEARCH Associates Inc., Bittium Corp., BTS Bioengineering Corp., Cadwell Industries Inc., Clarity Medical Pvt. Ltd., Cometa srl, Compumedics Ltd., Delsys Inc., DEYMED Diagnostic sro, Medtronic Plc, Natus Medical Inc., NCC Medical Co. Ltd., Nihon Kohden Corp. and Noraxon USA Inc.

-

Market Research Insights

- Market dynamics are shaped by the push toward decentralized healthcare, with point-of-care diagnostics enhancing clinical efficiency. The adoption of wearable health technology for tele-rehabilitation programs has reduced patient follow-up appointments by up to 30%, optimizing resource allocation. Furthermore, the integration of neurodiagnostic solutions with electronic medical records improves clinical data management and supports evidence-based rehabilitation.

- In surgical settings, intraoperative monitoring has become a standard of care, with facilities reporting a 15% reduction in nerve-related complications. Innovations in neuromuscular computing and human-computer interaction are expanding applications into ergonomic assessment and gesture recognition, while digital health integration facilitates remote patient monitoring and robust clinical decision support, driving a more connected and efficient diagnostic ecosystem.

We can help! Our analysts can customize this electromyography (emg) devices market research report to meet your requirements.

RIA -

RIA -