EMEA IT Professional Services Market Size 2026-2030

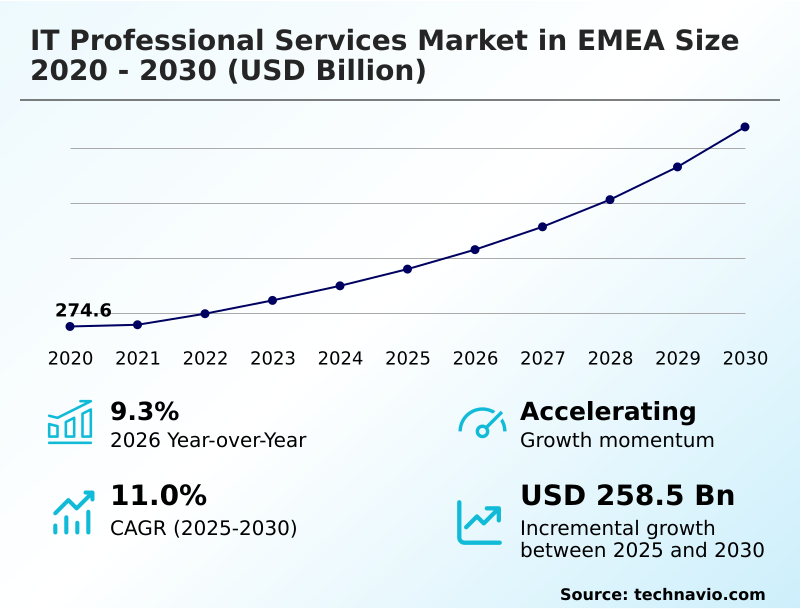

The EMEA IT Professional Services Market size was valued at USD 378.9 billion in 2025, growing at a CAGR of 11% during the forecast period 2026-2030.

Major Market Trends & Insights

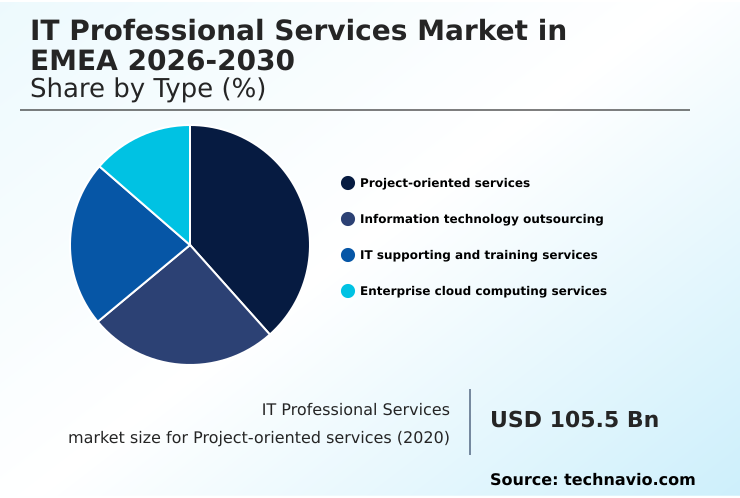

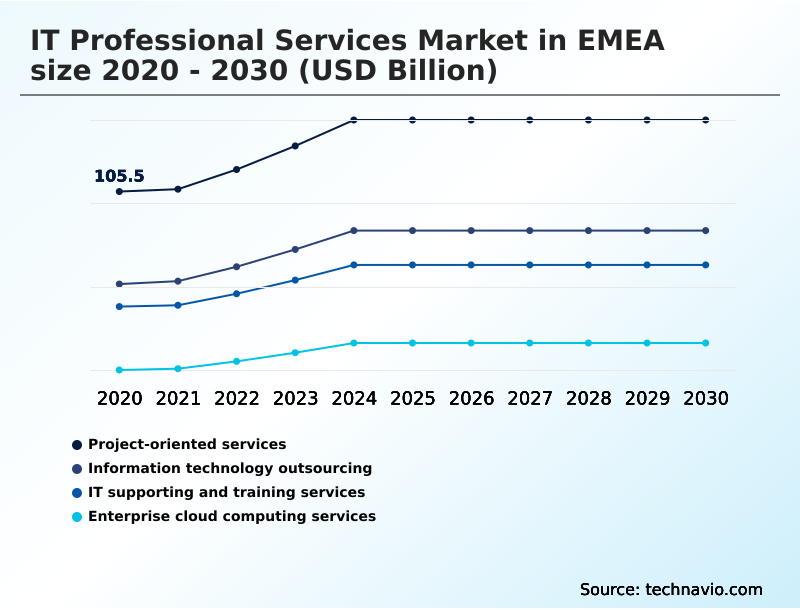

- By Type - Project-oriented services segment was valued at USD 132.8 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 362.8 billion

- Market Future Opportunities 2025-2030: USD 258.5 billion

- CAGR from 2025 to 2030 : 11%

Market Summary

- The IT professional services market in EMEA is defined by its role in enabling large-scale digital transformation, with a year-over-year growth of 9.3% underscoring its momentum. Cloud adoption, a key driver, has led to a 25% increase in demand for specialized fintech and e-commerce IT support following a surge in digital transaction volumes.

- As a real-world business scenario, a manufacturing firm might engage professional services to integrate IoT sensors into its assembly line, which can reduce production errors by 15%. However, this progress is tempered by a significant challenge: a persistent shortage of skilled talent, with nearly 70% of technology firms facing recruitment delays.

- This scarcity directly constrains the ability of service providers to execute complex transformation projects, creating a bottleneck that impacts the pace of innovation and market expansion across the region.

What will be the Size of the EMEA IT Professional Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the EMEA IT Professional Services Market Segmented?

The emea it professional services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Project-oriented services

- Information technology outsourcing

- IT supporting and training services

- Enterprise cloud computing services

- End-user

- Large enterprises

- Small and medium enterprises

- Deployment

- Cloud

- On-premises

- Geography

- EMEA

How is the EMEA IT Professional Services Market Segmented by Type?

The project-oriented services segment is estimated to witness significant growth during the forecast period.

Project-oriented services represent a highly strategic market segment, where successful engagements in software development reduce project delivery cycles by more than 15% compared to non-specialized approaches.

This segment is characterized by bespoke solutions in cybersecurity management and distributed computing, where firms help clients navigate the complexities of hybrid environments.

The adoption of hyper-converged infrastructure within these projects delivers a 20% improvement in resource utilization for on-premises deployment.

These services are essential for organizations undertaking large-scale transformations, utilizing augmented reality and cloud orchestration to deliver finite, high-impact technical milestones aligned with long-term commercial goals.

The focus remains on outcome-based delivery, making project-oriented services a cornerstone of the regional technology ecosystem by providing critical expertise.

The Project-oriented services segment was valued at USD 132.8 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the EMEA IT Professional Services Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises evaluating IT professional services are increasingly focused on measurable outcomes, leading to deeper inquiries about specific use cases. Many small and medium-sized enterprises (SMEs) explore the it professional services cost for smes, seeking to balance budget constraints with the need for digital transformation.

- These businesses often find that investing in managed services can reduce their operational overhead by over 15% compared to maintaining an in-house team. In specialized sectors, the benefits of managed it services for healthcare are particularly scrutinized, where compliance and data security are paramount.

- Decision-makers are also concerned with execution risk, closely examining the cloud migration project timeline factors to avoid costly delays and business disruption. For instance, projects with clearly defined scopes are completed up to 25% faster than those with ambiguous requirements.

- Furthermore, a significant challenge lies in contract governance, which prompts questions on how to improve service level agreement quality to ensure accountability and performance. Addressing the challenges of legacy modernization projects remains a central theme, as organizations seek to upgrade core systems without compromising operational stability.

- These detailed considerations reflect a mature market where buyers demand transparency and a clear return on investment.

What are the key market drivers leading to the rise in the adoption of EMEA IT Professional Services Industry?

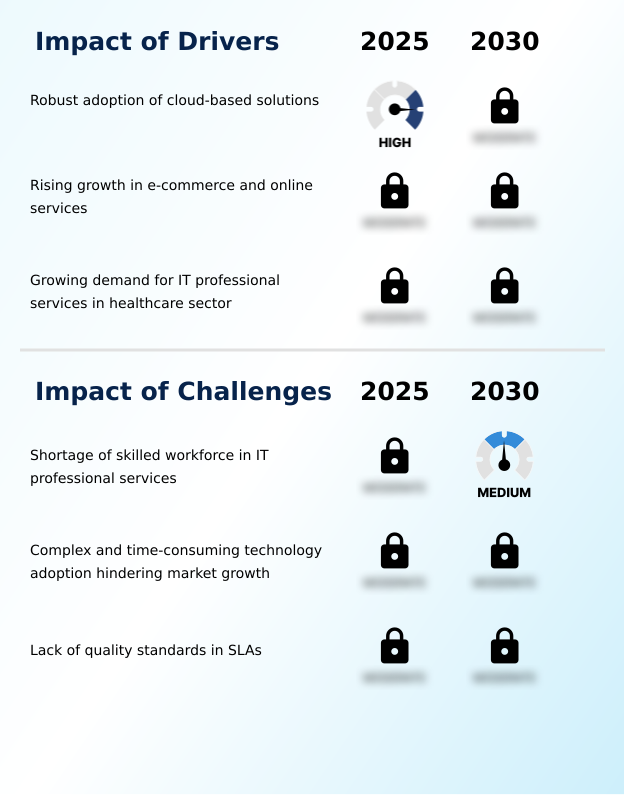

- The robust adoption of cloud-based solutions is a primary driver, compelling businesses to enhance agility and reduce their reliance on on-premises hardware footprints.

- The robust adoption of cloud-based solutions, which can increase operational agility by up to 40%, is the primary market driver for IT professional services in EMEA.

- This shift toward infrastructure as a service and platform as a service is a non-negotiable requirement for modern businesses.

- The expansion of b2b e-commerce and digital payment platforms has directly resulted in a 25% increase in demand for specialized IT support to build integrated supply chains and customer portals.

- This technology transformation is compelling traditional retailers to become technology companies. Consequently, the demand for professional services to implement hybrid IT solutions and ERP implementation for managing this transition is surging.

- The adoption of cloud-native solutions underpins the fundamental redesign of business logic to leverage distributed computing, cementing the role of professional services in driving growth.

What are the market trends shaping the EMEA IT Professional Services Industry?

- The market is shaped by the pervasive trend of digital transformation across IT platforms. This evolution involves a move toward technology-enabled, data-driven ecosystems.

- Digital transformation is reshaping the IT professional services market in EMEA, with a notable trend being the adoption of generative AI, which has been shown to increase coding efficiency by up to 25%. This internal evolution is moving the industry from a traditional consulting model to a data-driven ecosystem.

- The application of blockchain technology is also growing, particularly for enhancing security in digital transactions and identity management. Service providers are actively building proprietary software platforms, incorporating technologies like edge computing and IoT integration to offer intelligent industry solutions. This shift toward consulting-as-a-service, accessible via integrated digital dashboards, has reduced digital audit costs by over 30%.

- As part of this ai-driven reinvention, there is also a move toward sovereign cloud and on-demand learning to meet regional data laws and address skill gaps.

What challenges does the EMEA IT Professional Services Industry face during its growth?

- A significant challenge affecting industry growth is the persistent shortage of a skilled workforce in IT professional services, impeding the rapid expansion of digital initiatives.

- The most significant challenge for the IT professional services market in EMEA is a structural talent shortage, with nearly 70% of technology firms reporting severe recruitment delays. This lack of skilled professionals, particularly in cloud architecture and data governance, acts as a direct ceiling on growth.

- Another major hurdle is the complexity of legacy modernization, where the average cloud migration project duration has increased by 15% due to unforeseen issues with multi-cloud interoperability. This friction slows down digital transformation initiatives. Furthermore, the lack of standardized quality benchmarks in a service level agreement complicates client-vendor relationships.

- This creates an environment where providers who invest in a digital center of excellence and robotic process automation to standardize managed IT services can gain a competitive advantage.

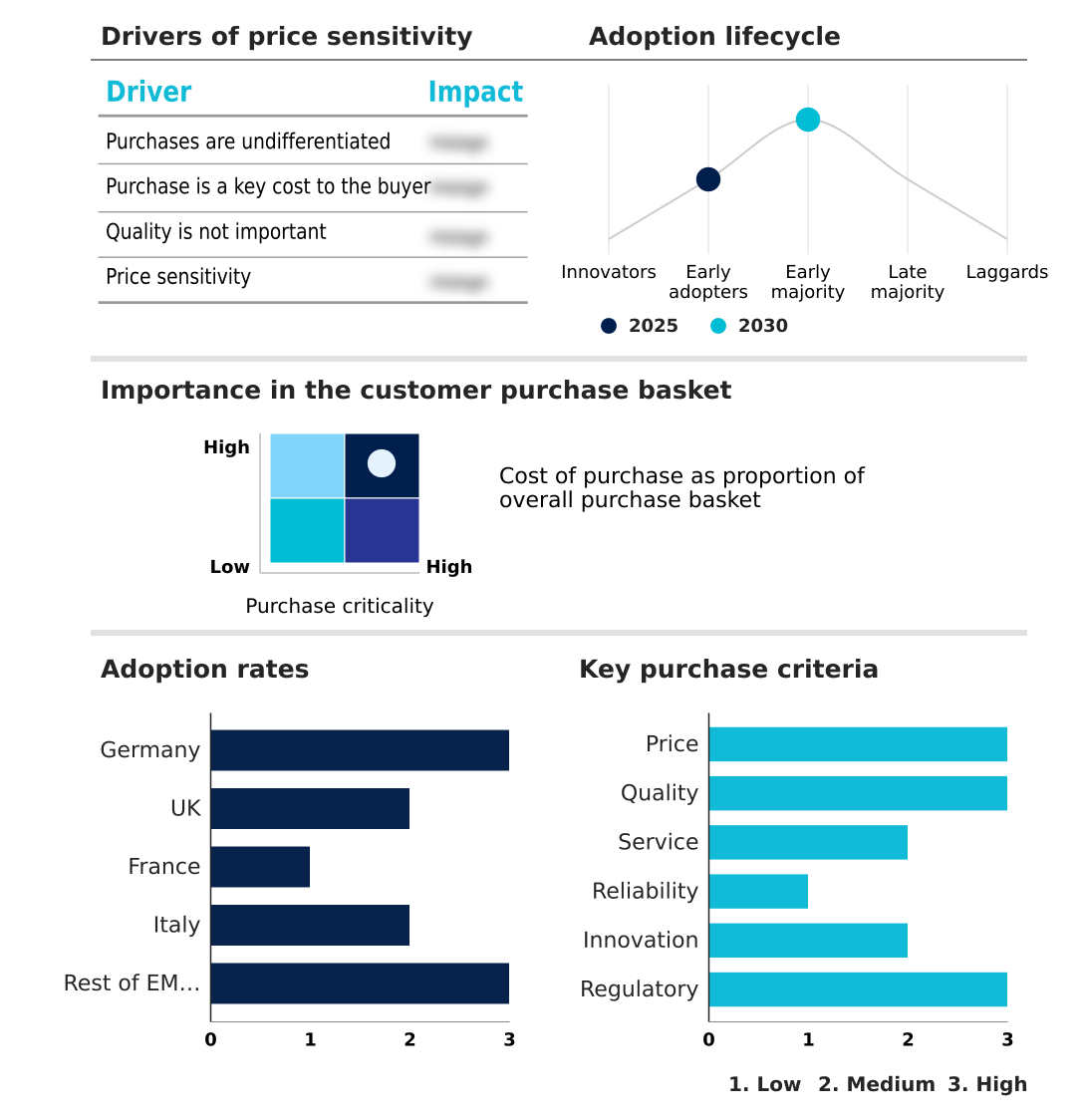

Exclusive Technavio Analysis on Customer Landscape

The emea it professional services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the emea it professional services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of EMEA IT Professional Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, emea it professional services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Offerings include strategy, consulting, technology transformation, and AI-driven reinvention, focusing on cloud migration, cybersecurity, and digital operations to drive business growth.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Amadeus IT Group SA

- Amazon.com Inc.

- Atos SE

- Capgemini SE

- Dassault Systemes SE

- Datto Holdings Corp.

- Deloitte Touche Tohmatsu Ltd.

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hewlett Packard Entp. Co.

- Hexagon AB

- IBM Corp.

- Infosys Ltd.

- Microsoft Corp.

- Oracle Corp.

- SAP SE

- Siemens AG

- Tata Consultancy Services

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the IT Consulting and Other Services industry, the enterprise shift toward platform-based business models has intensified demand for IT professional services focused on API management and ecosystem integration, requiring a higher level of digital consulting.

- The enforcement of stringent data sovereignty and privacy regulations, such as GDPR, has created a substantial market for IT professional services specializing in compliance audits, data localization strategies, and building sovereign cloud environments.

- Widespread enterprise adoption of multi-cloud and hybrid IT solutions has spurred demand for specialized professional services in cloud orchestration, cost optimization, and ensuring interoperability across disparate platforms.

- The move toward Industry 4.0 in manufacturing sectors is driving demand for IT professional services that can implement and manage IoT integration, edge computing, and digital twin technology to optimize production lines.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled EMEA IT Professional Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 221 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11% |

| Market growth 2026-2030 | USD 258.5 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.3% |

| Key countries | Germany, UK, France, Italy and Rest of EMEA |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ecosystem of the IT professional services market in EMEA is a complex network where technology suppliers, including cloud hyperscalers and software vendors, provide the foundational platforms. These inputs enable service providers, from global system integrators to boutique consultancies, to deliver solutions, with project-oriented services holding a 38% share of the market.

- These firms deliver a range of offerings, from digital consulting to legacy modernization. End-users, segmented into large enterprises and SMEs, consume these services to drive digital transformation, with enterprise adoption rates for cloud services being 25% higher than for SMEs. Regulatory bodies, especially within the EU, heavily influence data governance and security standards, shaping service delivery models.

- Supporting entities, such as R&D centers and training institutions, are critical for fostering innovation and addressing the persistent skills gap, ensuring the long-term vitality of the value chain.

What are the Key Data Covered in this EMEA IT Professional Services Market Research and Growth Report?

-

What is the expected growth of the EMEA IT Professional Services Market between 2026 and 2030?

-

The EMEA IT Professional Services Market is expected to grow by USD 258.5 billion during 2026-2030, registering a CAGR of 11%. Year-over-year growth in 2026 is estimated at 9.3%%. This acceleration is shaped by robust adoption of cloud-based solutions, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Project-oriented services, Information technology outsourcing, IT supporting and training services, and Enterprise cloud computing services), End-user (Large enterprises, and Small and medium enterprises), Deployment (Cloud, and On-premises) and Geography (EMEA). Among these, the Project-oriented services segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers EMEA. Country-level analysis includes Germany, UK, France, Italy and Rest of EMEA, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is robust adoption of cloud-based solutions, which is accelerating investment and industry demand. The main challenge is shortage of skilled workforce in it professional services, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the EMEA IT Professional Services Market?

-

Key vendors include Accenture Plc, Amadeus IT Group SA, Amazon.com Inc., Atos SE, Capgemini SE, Dassault Systemes SE, Datto Holdings Corp., Deloitte Touche Tohmatsu Ltd., DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., Hewlett Packard Entp. Co., Hexagon AB, IBM Corp., Infosys Ltd., Microsoft Corp., Oracle Corp., SAP SE, Siemens AG and Tata Consultancy Services. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for IT professional services in EMEA is intensely fragmented, with the top vendors like Accenture and IBM collectively accounting for less than 20% of the market share. These leaders are focusing on strategic acquisitions to bolster their capabilities in high-growth areas, particularly AI and cybersecurity.

- For instance, recent investments in developing sovereign cloud solutions aim to meet regional data residency requirements, a move that directly addresses enterprise demand for GDPR-compliant platforms. This innovation push has reduced audit-related project costs by over 30% through the use of automated project management tools.

- However, firms continue to grapple with the challenge of migrating legacy systems, where the average full-scale cloud migration project duration has increased by 15% due to unforeseen data governance complexities.

We can help! Our analysts can customize this emea it professional services market research report to meet your requirements.

RIA -

RIA -