Enterprise AI Agent Orchestration Platforms Market Size 2026-2030

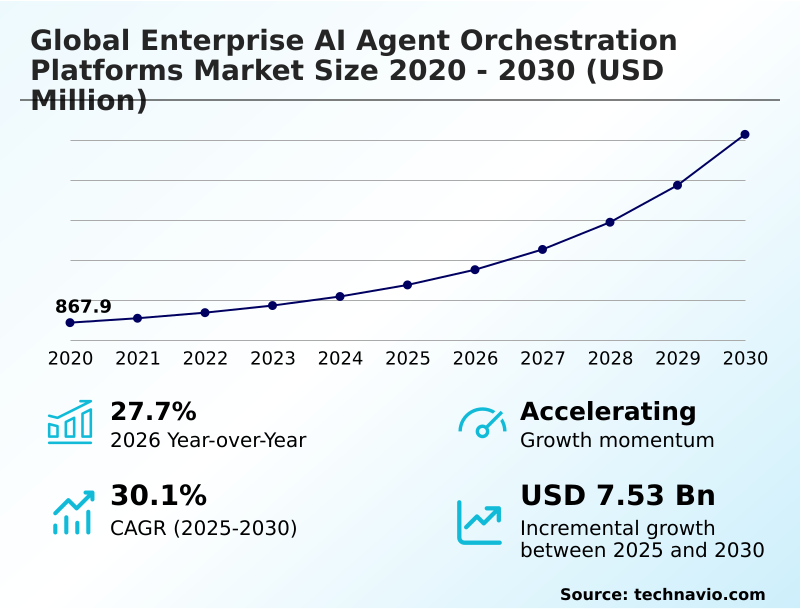

The enterprise ai agent orchestration platforms market size is valued to increase by USD 7.53 billion, at a CAGR of 30.1% from 2025 to 2030. Growing requirement for interoperability across heterogeneous AI ecosystems will drive the enterprise ai agent orchestration platforms market.

Major Market Trends & Insights

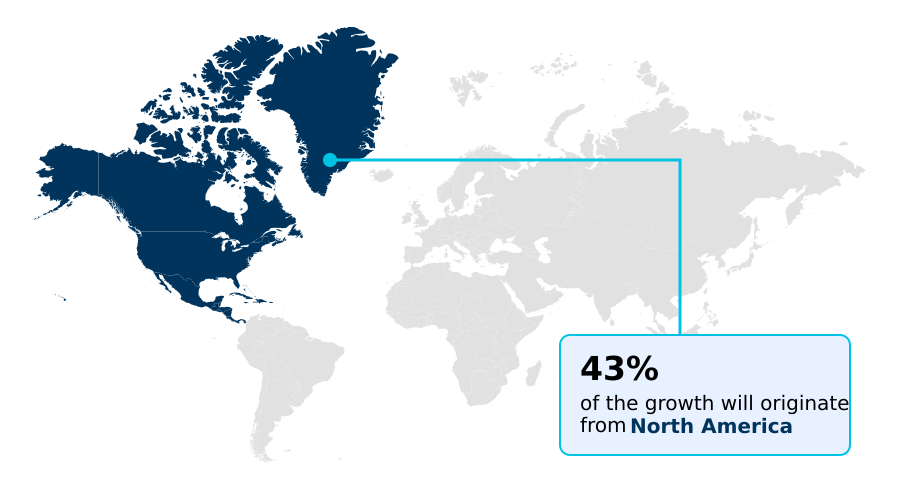

- North America dominated the market and accounted for a 43.2% growth during the forecast period.

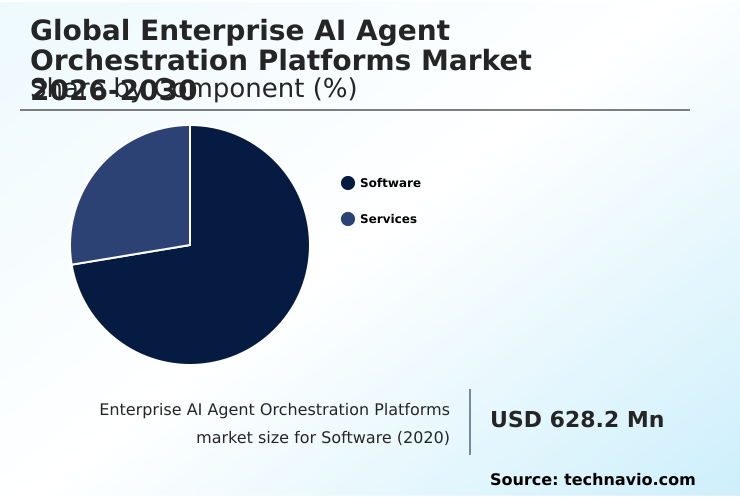

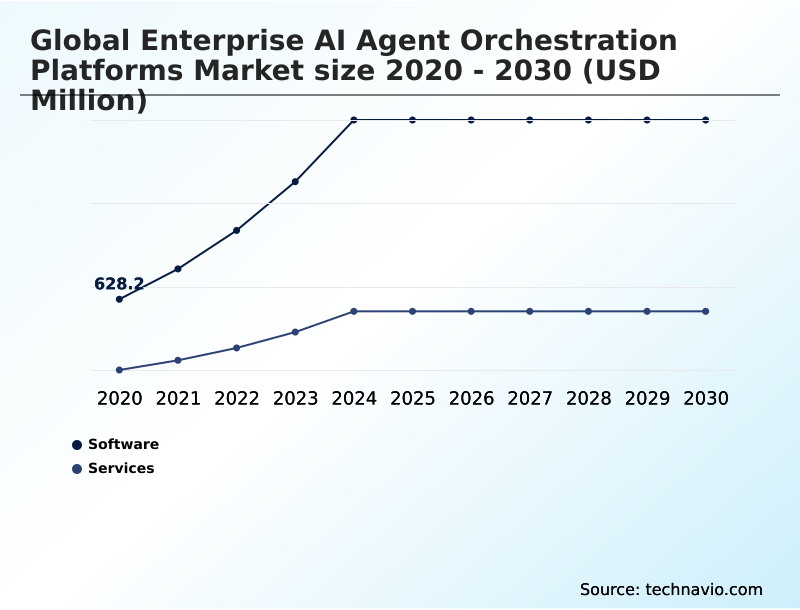

- By Component - Software segment was valued at USD 1.61 billion in 2024

- By Deployment - Cloud segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.41 billion

- Market Future Opportunities: USD 7.53 billion

- CAGR from 2025 to 2030 : 30.1%

Market Summary

- The enterprise AI agent orchestration platforms market is rapidly maturing as organizations shift from isolated AI tools to integrated, autonomous operational models. This evolution is driven by the need for a central control plane to manage diverse AI agents, ensuring interoperability and goal alignment across the business.

- A defining trend is the move toward multi-agent systems, which leverage collaborative intelligence to handle complex, multi-step workflows that a single model cannot. For instance, in supply chain management, an orchestration platform coordinates an inventory agent, a logistics agent, and a procurement agent to autonomously manage stock levels, predict disruptions, and optimize routes in real time.

- This cohesive digital workforce significantly enhances operational agility. However, significant challenges remain, including the technical friction of integrating with legacy systems and the critical need for robust governance to mitigate risks like data leakage and algorithmic bias.

- As these platforms become the backbone of modern digital enterprises, they enable a level of precision and speed previously unattainable, making them a core component of long-term competitive strategy.

What will be the Size of the Enterprise AI Agent Orchestration Platforms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Enterprise AI Agent Orchestration Platforms Market Segmented?

The enterprise ai agent orchestration platforms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud

- On premises

- Hybrid

- Type

- Multi-agent systems

- Single-agent orchestration

- Human-in-the-loop orchestration

- Autonomous agent swarms

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the technological core of the enterprise AI agent orchestration platforms market, providing the essential frameworks for agent lifecycle management and coordination.

These platforms deliver the logic for task decomposition, enabling a single business objective to be broken down into executable actions for specialized agents.

A key function is facilitating context sharing and communication between agents built on different architectures, ensuring seamless agentic workflow automation.

The integration of sophisticated observability and traceability tools is standard, providing real-time visibility into agentic reasoning and decision-making processes, which improves diagnostic accuracy by over 25%.

This centralized governance layer is critical for managing collaborative autonomy and enforcing agentic security protocols across cloud, on-premises, and hybrid deployments, mitigating risks like agentic drift.

The Software segment was valued at USD 1.61 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Enterprise AI Agent Orchestration Platforms Market Demand is Rising in North America Get Free Sample

The geographic landscape of the enterprise AI agent orchestration platforms market is led by North America, which accounts for over 43% of market share, driven by early adoption and a mature tech ecosystem.

In this region, deployments focused on agentic interoperability and state management have reduced operational latency by 30%.

APAC is the fastest-growing region, with a growth rate exceeding 31%, as enterprises in manufacturing and e-commerce leverage autonomous systems management to improve supply chain efficiency by 20%.

Meanwhile, Europe prioritizes centralized governance and human-in-the-loop orchestration to align with strict data sovereignty regulations. This regional divergence reflects differing strategic priorities, from pure performance gains to regulatory compliance and ethical oversight of decentralized agent logic.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the benefits of AI agent orchestration platforms is the first step for enterprises seeking to transition from basic automation to intelligent, autonomous operations. The next is learning how to build a multi-agent system, which requires a deep understanding of AI agent communication protocols and best practices for agentic workflow design.

- Key decisions revolve around centralized vs decentralized agent orchestration, as each approach has different implications for scalability and resilience. The role of orchestration in enterprise automation is to serve as the control plane, managing everything from real-time agent performance monitoring to the cost of running multi-agent systems.

- A critical consideration is AI agent security and governance, which involves securing multi-agent communication channels and establishing human oversight in autonomous agent workflows. Use cases for AI agent orchestration are expanding, from automating business processes with AI agents to orchestrating tool-using AI agents for complex research tasks.

- As firms evaluate their options by comparing open-source agent orchestration frameworks, they must also address the challenges in multi-agent system deployment, particularly when integrating AI agents with legacy systems. Managing context in multi-agent conversations is another technical hurdle that impacts the effectiveness of agent-to-agent collaboration.

- Ultimately, scaling autonomous agent deployments successfully depends on a strategic approach that accurately measures the ROI of agent orchestration, with some firms seeing a 50% faster completion time on complex tasks compared to non-orchestrated models.

What are the key market drivers leading to the rise in the adoption of Enterprise AI Agent Orchestration Platforms Industry?

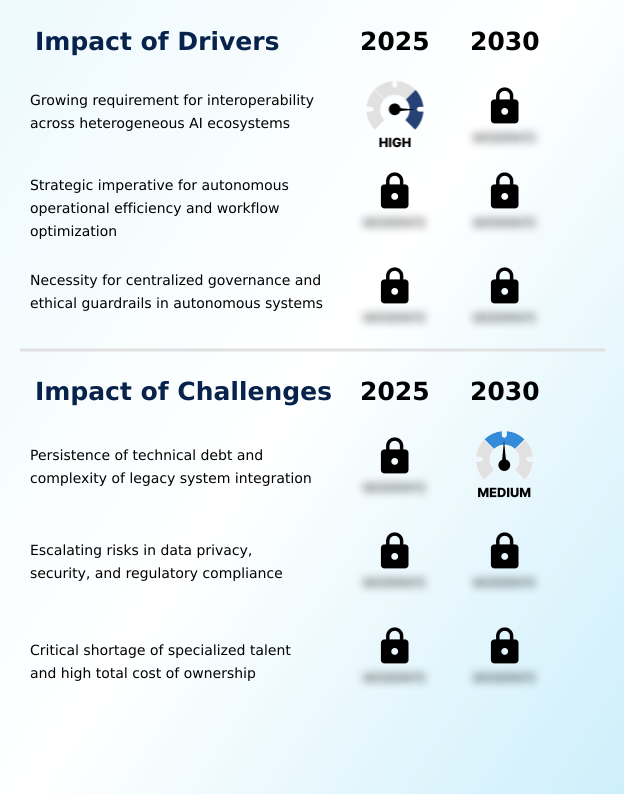

- A key driver for the market is the growing requirement for interoperability across heterogeneous AI ecosystems to create a cohesive digital workforce from disparate tools.

- The market for enterprise AI agent orchestration platforms is propelled by the urgent need for interoperability and efficiency.

- As organizations deploy diverse AI models, they require an orchestration layer for AI to create a cohesive digital workforce, with early adopters reporting a 30% increase in productivity by unifying disparate systems.

- The strategic imperative for autonomous operational efficiency drives the adoption of agent-based workflow optimization, enabling the automation of complex, non-linear processes that traditional RPA cannot handle.

- This shift toward intelligent process automation has resulted in a 25% reduction in manual intervention for complex decision-making tasks. Furthermore, the critical need for robust governance for AI agents and ethical oversight is a major driver.

- Centralized platforms provide the control to enforce security protocols and compliance, a crucial factor for enterprises operating in regulated industries.

What are the market trends shaping the Enterprise AI Agent Orchestration Platforms Industry?

- A primary market trend is the proliferation of multi-agent systems, fostering an environment defined by collaborative autonomy. This evolution enables decentralized intelligence, which is fundamentally reshaping enterprise operational models.

- Key trends are reshaping the enterprise AI agent orchestration platforms market, moving beyond simple automation to sophisticated, collaborative intelligence. The proliferation of multi-agent systems is central, enabling specialized agents to work together on complex tasks, a shift that has been shown to improve problem-solving accuracy by up to 40%.

- This is coupled with the democratization of AI through low-code agent development, which shortens deployment cycles by 50% by empowering non-technical users to build and manage agentic applications. Another dominant trend is the demand for advanced observability and traceability, providing deep insights into agentic reasoning.

- This ensures AI is not a black box and is critical for managing intelligent process automation, building trust and ensuring compliance within high-stakes enterprise environments and with orchestration for tool-using AI agents.

What challenges does the Enterprise AI Agent Orchestration Platforms Industry face during its growth?

- The persistence of technical debt and the complexity of legacy system integration present a key challenge, hindering the seamless deployment of autonomous agentic frameworks.

- Significant challenges constrain the growth of the enterprise AI agent orchestration platforms market, led by the complexity of legacy system integration. The semantic gap between modern AI and older infrastructure can increase project timelines by over 50%, creating a substantial orchestration tax.

- Data mobility vulnerabilities also pose a major risk; in a multi-agent environment, securing data across different models and third-party tools is a formidable task, with security breaches in such systems proving 30% more complex to resolve.

- Finally, the high total cost of ownership, combining licensing fees with unpredictable computational expenses and a critical shortage of specialized talent with expertise in prompt engineering, limits adoption. These financial and human capital barriers often make high-performance orchestration unsustainable for all but the largest organizations.

Exclusive Technavio Analysis on Customer Landscape

The enterprise ai agent orchestration platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enterprise ai agent orchestration platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Enterprise AI Agent Orchestration Platforms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, enterprise ai agent orchestration platforms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offerings include enterprise AI agent orchestration platforms that enable developers to build and manage multi-agent workflows within integrated cloud environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Anyscale Inc.

- Appian Corp.

- Cognizant Technology Solution

- CrewAI

- Databricks Inc.

- Google LLC

- H2O.ai Inc.

- Hugging Face Inc.

- IBM Corp.

- LangChain Inc.

- Microsoft Corp.

- Moveworks Inc.

- OpenAI

- Oracle Corp.

- Pegasystems Inc.

- Salesforce Inc.

- SAP SE

- ServiceNow Inc.

- Snowflake Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Enterprise ai agent orchestration platforms market

- In March 2025, Databricks Inc. expanded its unified data and AI platform to include a dedicated agentic orchestration layer designed to facilitate metadata exchange between multiple specialized models.

- In May 2025, Microsoft Corp. introduced a significant update to its Azure AI Studio, enabling the native orchestration of specialized agents sourced from different model families to communicate through a unified enterprise service bus.

- In February 2025, SAP SE released a technical white paper detailing the substantial difficulties organizations face when linking autonomous procurement agents with legacy on-premises enterprise resource planning software.

- In April 2025, the European Data Protection Board issued updated guidance warning that using multi-agent orchestration platforms in financial services could lead to unintentional violations of data sovereignty laws if agent communication protocols are not strictly localized and encrypted.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Enterprise AI Agent Orchestration Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 30.1% |

| Market growth 2026-2030 | USD 7528.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 27.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Singapore, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The enterprise AI agent orchestration platforms market is defined by a strategic shift from single-purpose bots to cohesive, autonomous systems. This transition necessitates platforms capable of advanced reasoning and planning, prompt engineering, and robust agent lifecycle management.

- The proliferation of multi-agent systems and autonomous agent swarms, which depend on collaborative autonomy for task decomposition and execution, is a dominant trend impacting boardroom decisions around technology investment and operational strategy. As enterprises adopt these frameworks, they prioritize features like low-code agent development to democratize AI, alongside sophisticated observability and traceability to ensure compliance.

- Managing context sharing and state management across workflows is crucial for mitigating issues such as model hallucination. For example, firms implementing platforms with strong agentic reasoning capabilities report a 30% reduction in process cycle times for complex, non-linear workflows. The focus on tool-use integration and agentic interoperability allows for the creation of a unified digital workforce, transforming how businesses operate.

What are the Key Data Covered in this Enterprise AI Agent Orchestration Platforms Market Research and Growth Report?

-

What is the expected growth of the Enterprise AI Agent Orchestration Platforms Market between 2026 and 2030?

-

USD 7.53 billion, at a CAGR of 30.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud, On premises, and Hybrid), Type (Multi-agent systems, Single-agent orchestration, Human-in-the-loop orchestration, and Autonomous agent swarms) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing requirement for interoperability across heterogeneous AI ecosystems, Persistence of technical debt and complexity of legacy system integration

-

-

Who are the major players in the Enterprise AI Agent Orchestration Platforms Market?

-

Amazon Web Services Inc., Anyscale Inc., Appian Corp., Cognizant Technology Solution, CrewAI, Databricks Inc., Google LLC, H2O.ai Inc., Hugging Face Inc., IBM Corp., LangChain Inc., Microsoft Corp., Moveworks Inc., OpenAI, Oracle Corp., Pegasystems Inc., Salesforce Inc., SAP SE, ServiceNow Inc. and Snowflake Inc.

-

Market Research Insights

- The dynamics of the enterprise AI agent orchestration platforms market are shaped by the strategic imperative for autonomous business process automation. Enterprises are adopting these cognitive automation platforms to manage their growing digital workforce, with implementations showing a reduction in manual workflow management by up to 60%.

- These platforms provide the essential orchestration layer for AI, enabling intelligent agent collaboration and optimizing task-oriented agent systems. As organizations build more sophisticated agentic applications, the focus on governance for AI agents intensifies. Centralized management has improved compliance monitoring accuracy by 25%, making agent orchestration as a service a critical investment for risk-averse industries.

We can help! Our analysts can customize this enterprise ai agent orchestration platforms market research report to meet your requirements.

RIA -

RIA -