Enterprise Mobile Application Development Services Market Size 2024-2028

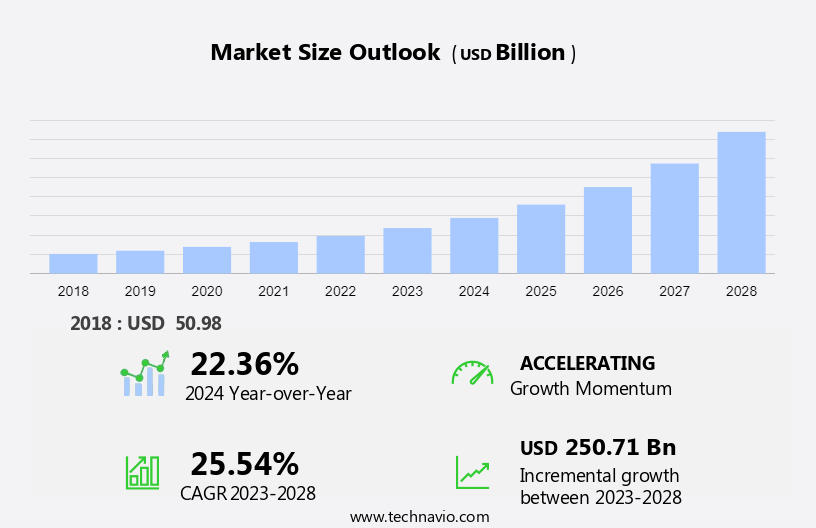

The enterprise mobile application development services market size is forecast to increase by USD 250.71 billion, at a CAGR of 25.54% between 2023 and 2028.

- The market is experiencing significant growth, driven by several key trends. The increasing demand for cloud-native development solutions is a major growth factor, as businesses seek to leverage the benefits of agility, scalability, and cost savings. Another trend is the rise of hybrid application integration technology, which enables seamless integration of mobile applications with enterprise systems and data. The market is witnessing a rise in demand for app development services for connected gadgets, including wearable devices and IoT devices, as well as for mobile applications in sectors such as smart homes and the mobile workforce. Additionally, device fragmentation and application performance optimization issues continue to challenge developers, necessitating innovative solutions to ensure optimal user experience. Overall, these trends are shaping the market and driving demand for advanced, integrated, and high-performing mobile solutions.

What will be the Size of the Enterprise Mobile Application Development Services Market During the Forecast Period?

- The market is experiencing strong growth, fueled by the increasing adoption of mobile technology among businesses worldwide. With the proliferation of smartphones, mobility has become a key driver for digital transformation, enabling mobile enterprise applications to streamline business processes and enhance interaction with customers. The integration of mobile technology with cloud-based services, broadband, and wireless technology is further expanding the market's potential. mobile phone users and businesses are increasingly relying on mobile applications for productivity, communication, and brand engagement, making app makers an essential partner for organizations undergoing digital transformation. The market's size is significant and continues to grow, as mobile technology becomes an integral part of business operations and strategies.

How is this Enterprise Mobile Application Development Services Industry segmented and which is the largest segment?

The enterprise mobile application development services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Large enterprises

- SMEs

- Platform

- Native

- Hybrid

- Web

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

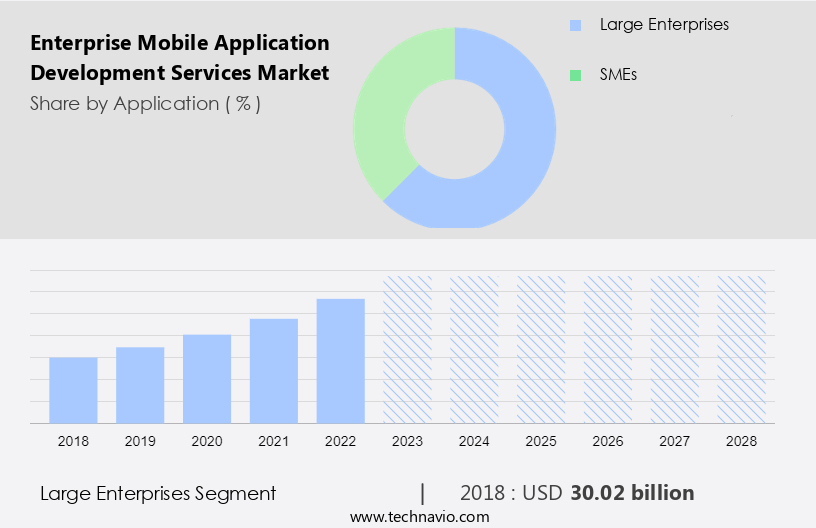

By Application Insights

- The large enterprises segment is estimated to witness significant growth during the forecast period.

Enterprises are accelerating their digital transformation initiatives, integrating mobile applications to modernize business processes, boost efficiency, and enhance customer experiences. Mobile technology, including smartphones, mobility, mobile phones, tablets, and wearable devices, is revolutionizing business operations. mobile apps facilitate real-time interaction, enabling enterprises to engage customers, deliver personalized content, and provide seamless omnichannel experiences.

Applications cater to various industries such as IT & telecommunication, healthcare & life sciences, manufacturing & automotive, and media & entertainment, among others. Enterprise mobile application development services, like those offered by Tech Mahindra Ltd., enable businesses to leverage platforms like OutSystems for low-code development, mobile application development, high productivity PaaS, and multi-experience development. These services ensure cross-platform compatibility, address data security concerns, and provide cloud-based services, including web-based and hybrid applications. Mobile applications are integral to digital transformation, driving business growth and innovation.

Get a glance at the Enterprise Mobile Application Development Services Industry report of share of various segments Request Free Sample

The large enterprises segment was valued at USD 30.02 billion in 2018 and showed a gradual increase during the forecast period.

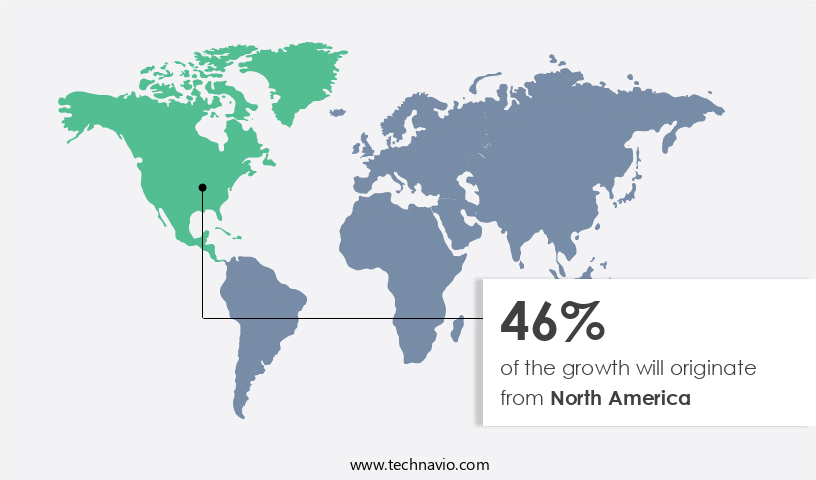

Regional Analysis

- North America is estimated to contribute 46% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

In North America, the prevalence of smartphones and mobile Internet usage is substantial, fueling a significant demand for enterprise mobile applications. These applications serve to enhance communication, collaboration, and productivity for businesses in various sectors. The region's industries are undergoing digital transformation to maintain competitiveness and cater to evolving customer needs. Mobile applications play a crucial role in this process, enabling modernization, increased efficiency, and enhanced customer and employee experiences. Furthermore, North America's technological innovation hub status, driven by advancements in cloud computing, artificial intelligence, and the Internet of Things (IoT), fosters the creation of sophisticated mobile applications.

Enterprise mobile applications facilitate business automation solutions, including human capital management, accounting and finance, supply chain management, customer relationship management, machine learning, communication and collaboration, enterprise resource planning, e-commerce, business analytics, transport & logistics, manufacturing & automotive, energy & utilities, media & entertainment, and healthcare & life sciences. Cloud-based services, mobile phone users, tablets, and PCs are integral to these applications, which interact with web-based services, native, and hybrid applications, and various operating systems such as iOS, Android, and Windows. Data security concerns and cross-platform implementation complexities are addressed through consulting skills and advanced technologies like artificial intelligence and generative AI.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Enterprise Mobile Application Development Services Industry?

Growing demand for cloud-native development is the key driver of the market.

- Cloud-native mobile application development refers to constructing and deploying apps that utilize cloud computing infrastructure, services, and architectures for scalable, resilient, and agile solutions. This approach allows mobile applications to adapt to varying user traffic and workloads without downtime or performance concerns. Enterprises opt for cloud-native mobile app development services to capitalize on cloud platforms' flexibility and scalability, ensuring applications can manage growth and adapt to evolving business requirements. Furthermore, cloud-native development expedites the app development process through agile methodologies, automated deployment pipelines, and DevOps practices. Cloud-native mobile apps cater to diverse industries, including IT & telecommunication, healthcare & life sciences, and media & entertainment, among others.

- Applications for human capital management, accounting and finance, supply chain management, customer relationship management, and enterprise resource planning are popular use cases. Additionally, cloud-native development supports the development of cross-platform applications, online shopping apps, social networking, games apps, and business automation solutions. Cloud-native mobile app development addresses data security concerns through strong security measures and web-based services. It also supports machine learning, communication and collaboration, and business analytics. Wearable devices, IoT devices, and smart home applications are increasingly integrated into cloud-native mobile app development, further expanding its reach and utility.

What are the market trends shaping the Enterprise Mobile Application Development Services Industry?

The rise of hybrid application integration technology is the upcoming market trend.

- Hybrid application integration technology is gaining significance in today's organizations as they adopt both on-premises and cloud-based enterprise mobile applications. The integration of diverse organizational applications and systems presents complexities and data security concerns, necessitating advanced integration platforms. Traditional integration solutions face challenges due to the frequent alterations in enterprise systems across industries. Consequently, there is a growing demand for hybrid integration platforms that combine conventional integration tools with new technologies like API management software, iPaaS, and iSaaS. These advanced solutions facilitate seamless interaction between business processes on different operating systems, such as iOS, Android, and Windows. The integration of mobile technologies, including smartphones, mobility, mobile apps, wearable devices, IoT devices, and connected gadgets, is transforming industries like human capital management, accounting and finance, supply chain management, customer relationship management, machine learning, communication and collaboration, enterprise resource planning, eCommerce, business analytics, transport & logistics, manufacturing & automotive, energy & utilities, media & entertainment, and healthcare & life sciences.

What challenges does the Enterprise Mobile Application Development Services Industry face during its growth?

Device fragmentation and application performance optimization issues is a key challenge affecting the industry growth.

- The market is driven by the increasing use of smartphones and mobility in business processes. Connected gadgets, including mobile phones, tablets, wearable devices, and IoT devices, have become essential tools for business automation solutions, online shopping apps, social networking, games apps, and more. Mobile technology, including wireless technology, broadband services, cloud-based services, and internet services, has become integral to IT & Telecommunication and various industries such as human capital management, accounting and finance, supply chain management, customer relationship management, machine learning, communication and collaboration, enterprise resource planning, eCommerce, business analytics, transport & logistics, manufacturing & automotive, energy & utilities, media & entertainment, healthcare & life sciences, and more.

- App makers face complexities in implementing cross-platform mobile applications due to varying hardware specifications, screen sizes, resolutions, and operating systems (iOS, Android, Windows). For instance, Android mobile phones face challenges related to OS version compatibility, feature support, and platform-specific optimizations, making it difficult to create consistent experiences across devices. In addition, data security concerns and web-based services further complicate the development process. companies must possess consulting skills, artificial intelligence, creative advertising, visual brand expression, generative AI, and other advanced technologies to meet the demands of businesses In the digital transformation era.

Exclusive Customer Landscape

The enterprise mobile application development services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enterprise mobile application development services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, enterprise mobile application development services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Capgemini Service SAS

- CGI Inc.

- Cognizant Technology Solutions Corp.

- Deloitte Touche Tohmatsu Ltd.

- DXC Technology Co.

- HCL Technologies Ltd.

- Hexaware Technologies Ltd.

- Infosys Ltd.

- International Business Machines Corp.

- ITC Ltd.

- Larsen and Toubro Ltd.

- Netguru S.A

- PricewaterhouseCoopers LLP

- Siemens AG

- Tata Consultancy Services Ltd.

- Tech Mahindra Ltd.

- Virtusa Corp.

- Wipro Ltd.

- Zensar Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Enterprise mobile application development services have gained significant traction in today's digital landscape, driven by the increasing adoption of mobility solutions in various industries. The proliferation of smartphones and connected gadgets, including wearable devices and IoT devices, has led to a rise in demand for mobile applications that enable business automation, online shopping, social networking, and entertainment. The IT and telecommunication sector has been a key player in this market, providing consulting skills and expertise to help businesses navigate the complexities of mobile enterprise application development. These services encompass the development of applications for mobile workforces, as well as the integration of artificial intelligence, creative advertising, and visual brand expression into mobile applications.

Further, the use of mobile technology in business processes has led to a digital transformation, with businesses seeking to improve interaction with their customers, streamline operations, and enhance productivity. Mobile applications have become essential tools for human capital management, accounting and finance, supply chain management, customer relationship management, and enterprise resource planning. The adoption of cloud-based services, including global hybrid clouds, has also played a significant role In the growth of enterprise mobile application development services. These services enable businesses to leverage machine learning and communication and collaboration tools to enhance their mobile applications and improve their overall digital strategy.

However, the market for enterprise mobile application development services is not without its challenges. Cross-platform implementation complexities and data security concerns continue to pose challenges for developers. The use of web-based services and the integration of mobile applications with IoT devices and smart home systems add to the complexity of mobile application development. Despite these challenges, the market for enterprise mobile application development services is expected to continue growing, driven by the increasing use of mobile technology in various industries and the need for businesses to remain competitive In the digital landscape. The integration of emerging technologies, such as generative AI, into mobile applications is also expected to drive innovation and growth In the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.54% |

|

Market Growth 2024-2028 |

USD 250.71 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

22.36 |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Enterprise Mobile Application Development Services Market Research and Growth Report?

- CAGR of the Enterprise Mobile Application Development Services industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the enterprise mobile application development services market growth of industry companies

We can help! Our analysts can customize this enterprise mobile application development services market research report to meet your requirements.

RIA -

RIA -