External Urine Management Products Market Size 2024-2028

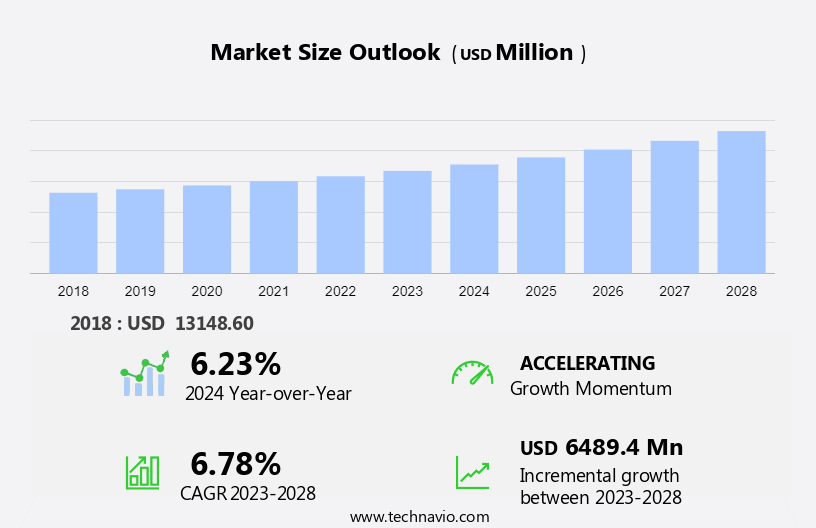

The external urine management products market size is forecast to increase by USD 6.49 billion, at a CAGR of 6.78% between 2023 and 2028.

- The market is witnessing significant growth due to several key factors. The adoption of these products in hospitals is on the rise, as they offer numerous advantages such as improved patient comfort, reduced risk of urinary tract infections, and enhanced patient dignity. Moreover, the increasing prevalence of chronic disease, particularly among the elderly population, is driving the demand for external urine management devices. However, the market growth is hampered by the rising cases of urinary tract infections, which can lead to complications if not treated promptly. Despite this challenge, the market is expected to continue its growth trajectory, as the benefits of external urine management products far outweigh the risks. Overall, the market trends indicate a positive outlook for external urine management products, with increasing awareness and acceptance among healthcare providers and patients.

What will be the Size of the External Urine Management Products Market During the Forecast Period?

- The market encompasses a range of solutions designed to address urinary issues for men and women, including urinary incontinence, bladder dysfunctions, and urinary retention. This market caters to various end-users, including hospitals, diagnostic laboratories, and home care settings. The aging population, with its increased prevalence of urological disorders such as benign prostate hyperplasia, bladder cancer, and bladder capacity issues, significantly contributes to market growth. The feeling of fullness and residual urine volume are common concerns for individuals experiencing bladder control issues, leading to a demand for effective external urine management solutions.

- The market is also influenced by the increasing hospital admission rate due to urologic diseases and the emergence of teleconsultation services for remote diagnosis and management. Overall, the market is expected to continue expanding, driven by the growing need for effective solutions to manage various urinary conditions.

How is this External Urine Management Products Industry segmented and which is the largest segment?

The external urine management products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Diagnostic laboratories and clinics

- Homecare settings

- Product

- Male external catheters

- Female external catheters

- Urine collection accessories

- Geography

- North America

- US

- Europe

- Germany

- France

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

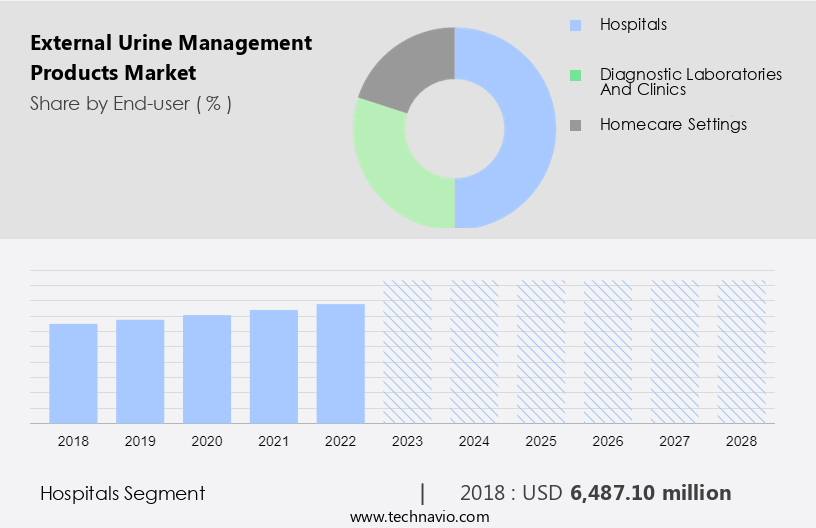

- The hospitals segment is estimated to witness significant growth during the forecast period.

The market is significantly influenced by the hospital segment due to the increasing prevalence of urological disorders and the importance of effective urinary management in healthcare facilities. This segment caters to a large patient population, particularly those with long-term care needs, such as post-urological surgery patients, who may experience urinary incontinence or other urinary issues. Key market players, including Hollister, Stryker (Sage Products LC), and Becton Dickinson (C. R. Bard), cater to this demand by providing a range of products, including urinary catheters and female external catheters, to manage urinary dysfunctions. The market is further driven by the growing geriatric population, who are more susceptible to bladder control issues and urinary incontinence due to aging and various urological disorders like urinary retention, benign prostate hyperplasia, bladder cancer, and post-operative complications.

The market is segmented into disposable and non-disposable products, with the disposable segment dominating due to its convenience and hygiene benefits. The market is also expanding in home care settings and diagnostic laboratories, driven by the increasing prevalence of urinary incontinence and the growing acceptance of teleconsultation services and online counseling. The market is expected to grow due to the increasing prevalence of conditions like hypertension and diabetes, which are associated with an increased risk of urinary incontinence. The International Continence Society and the Canadian Urological Association have reported that urinary incontinence affects approximately 25 million adults In the US, highlighting the significant market potential.

Get a glance at the External Urine Management Products Industry report of share of various segments Request Free Sample

The hospitals segment was valued at USD 6.49 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

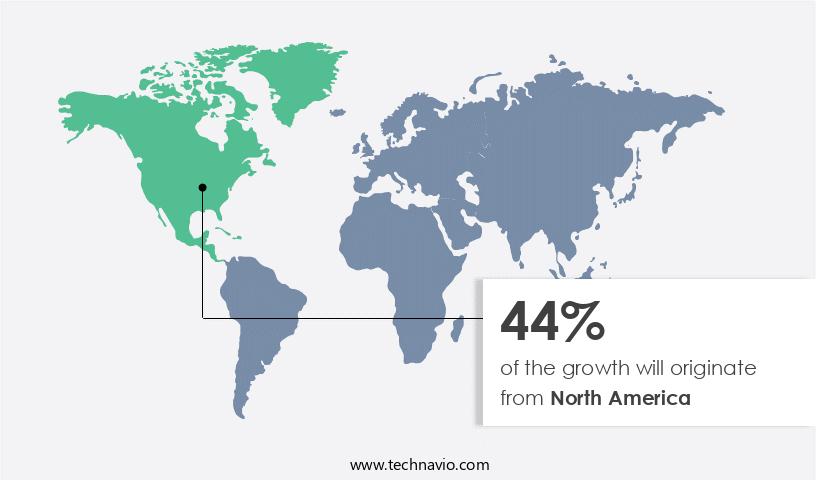

- North America is estimated to contribute 44% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America accounted for the largest revenue share in 2023, with the US being the primary contributor. The market growth can be attributed to the increasing geriatric population, the prevalence of urological disorders such as bladder dysfunctions and urinary retention, and the presence of major industry players. The aging population in North America is expanding, leading to significant implications for public health systems. In 2020, the COVID-19 pandemic resulted in a surge in demand for these products, particularly among long-term hospitalized patients and those in intensive care units. Key conditions driving market growth include benign prostate hyperplasia, bladder cancer, urinary incontinence, and post-operative complications.

In addition, hospitals, diagnostic laboratories, and home care settings are the major end-users. The market includes disposable and non-disposable products, such as pads, diapers, and urinary catheters. Online and offline channels are used for distribution. The market is served by prominent players, including Cardinal Health, Female segment focuses on stress incontinence, pregnancy, and menopause, while Men's segment addresses urinary incontinence, prostate glands, and bladder capacity issues. The market is influenced by factors like hygiene, industry trends, and the prevalence of conditions like hypertension, diabetes, and end-stage kidney disease. The International Continence Society and the Canadian Urological Association are key organizations In the field.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of External Urine Management Products Industry?

The adoption of external urine management products in hospitals is the key driver of the market.

- The market is experiencing significant growth due to the increasing prevalence of urinary incontinence and related conditions, particularly in hospitals. Urinary incontinence, which includes various bladder dysfunctions, affects both men and women, and can result from various urological disorders such as urinary retention, benign prostate hyperplasia, bladder cancer, post-operative complications, and other health issues. External urine management products, including pads, urinary catheters, and external urine collection devices, are essential tools for managing these conditions. Hospitals are major consumers of these products due to the high prevalence of urinary incontinence and related conditions among patients.

- The adoption of these products in hospitals depends on several factors, including hospital policies and protocols, availability of trained staff, and patient preferences. The development of advanced urinary incompatibility devices and the increasing prevalence of urological disorders are expected to drive market expansion. The global population is aging, and the geriatric population is more susceptible to bladder control issues, leakage, and other urinary-related problems. Chronic conditions such as hypertension, diabetes, and kidney diseases, including end-stage kidney disease and dialysis, also contribute to the rising prevalence of urinary incontinence. The market for external urine management products is further segmented into disposable and non-disposable segments, with the disposable segment dominating the market due to its convenience and ease of use.

What are the market trends shaping the External Urine Management Products Industry?

The rising prevalence of chronic conditions is the upcoming market trend.

- The market caters to the needs of men and women experiencing urinary incontinence due to various bladder dysfunctions, urological disorders, and post-operative complications. Conditions such as urinary retention, benign prostate hyperplasia, bladder cancer, and end-stage kidney disease contribute significantly to the market's growth. The aging population, particularly those with bladder control issues, also drives demand for these products. External urine management products include urinary catheters, condom catheters, pads, and diapers. The diapers segment, specifically, dominates the market due to its widespread use in home care settings and hospitals. The non-disposable segment is also gaining traction due to its cost-effectiveness and environmental sustainability.

- The increasing prevalence of chronic conditions, such as diabetes, hypertension, and multiple sclerosis, which can lead to urinary incontinence, is a primary market driver. According to the World Health Organization (WHO), chronic diseases accounted for over 70% of global deaths in 2022, and this percentage is projected to rise during the forecast period. As a result, the demand for external urine management products is expected to increase significantly. Moreover, the market is further fueled by the growing acceptance of teleconsultation services and online counseling, which enable remote diagnosis and treatment, thereby reducing hospital admission rates. The industry players continue to innovate, introducing new products and technologies to cater to the diverse needs of consumers.

What challenges does the External Urine Management Products Industry face during its growth?

Increasing cases of urinary infection is a key challenge affecting the industry growth.

- External urine management products, including pads, urinary catheters, and condom catheters, are essential solutions for men and women dealing with urine incontinence due to bladder dysfunctions. However, these products carry risks, particularly for those requiring long-term use. Complications include urinary tract infections (UTIs), skin irritation, bladder spasms, and catheter blockage or leakage. UTIs can occur when bacteria enter the urinary tract through the catheter, leading to infection. Leakage around the catheter can cause skin irritation and potential infection. Bladder dysfunctions can stem from various causes, such as urological disorders like urinary retention, benign prostate hyperplasia, bladder cancer, and post-operative complications.

- The aging population, with its increased prevalence of incontinence due to conditions like stress incontinence during pregnancy and delivery, menopause, and female anatomy, is a significant market for these products. The industry caters to various segments, including disposable pads and diapers, and non-disposable products. The market serves diverse end-users, including hospitals, diagnostic laboratories, and home care settings. Conditions like end-stage kidney disease, end-stage renal disease, dialysis, kidney transplant, and lower urinary system issues also contribute to the demand for these products. The hygiene concerns associated with incontinence and the need for effective urine management solutions drive the market.

Exclusive Customer Landscape

The external urine management products market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the external urine management products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, external urine management products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- B.Braun SE

- Becton Dickinson and Co.

- BioDerm Inc.

- Boehringer Laboratories LLC

- Cardinal Health Inc.

- Coloplast AS

- Consure Medical

- ConvaTec Group Plc

- GPC Medical Ltd.

- GWS Surgicals LLP

- Hollister Inc.

- Hospital Equipment Manufacturing Co.

- Manish Medi Innovation

- Medevis Rubplast India Pvt. Ltd.

- Medline Industries LP

- Spectrum Plastics Group

- Sterimed Medical Devices Pvt. Ltd.

- Stryker Corp.

- Teleflex Inc.

- Tilla Care Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of products designed to address various bladder dysfunctions and urinary incontinence issues. These conditions, which can affect both men and women, can result from a multitude of factors including urological disorders, aging, pregnancy, and delivery, among others. Urinary incontinence, characterized by the involuntary leakage of urine, is a common condition that affects millions worldwide. It can be caused by several factors, including stress, urinary retention, and certain medical conditions such as benign prostate hyperplasia, bladder dysfunctions, and cystitis. The market for external urine management products caters to the needs of various end-users, including hospitals, diagnostic laboratories, and home care settings.

Further, the aging population represents a significant portion of this market, as bladder control issues become more prevalent with age. The market offers a range of products to address the diverse needs of this population. These include pads and diapers, which are available in disposable and non-disposable forms, as well as female external catheters. The diapers segment holds a significant share of the market due to its convenience and ease of use. The industry players in this market cater to both the online and offline channels. Online channels have gained popularity due to their convenience and accessibility, while offline channels continue to dominate due to their widespread availability and the preference of some consumers for physical stores.

Moreover, hospitals represent a significant end-user segment, with a high demand for external urine management products due to the prevalence of various urological conditions and post-operative complications. End-stage kidney disease and dialysis patients also require these products due to their specific medical needs. The market is driven by several factors, including the increasing prevalence of bladder control issues, the growing aging population, and the rising awareness and acceptance of external urine management products. The market is also influenced by advancements in technology and the development of new products that offer improved comfort, hygiene, and effectiveness. The market for external urine management products is expected to grow significantly in the coming years, driven by the increasing prevalence of urinary incontinence and the growing awareness and acceptance of these products.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market Growth 2024-2028 |

USD 6.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, Germany, China, France, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this External Urine Management Products Market Research and Growth Report?

- CAGR of the External Urine Management Products industry during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the external urine management products market growth of industry companies

We can help! Our analysts can customize this external urine management products market research report to meet your requirements.

RIA -

RIA -