Fluorocarbon Coating Market Size 2024-2028

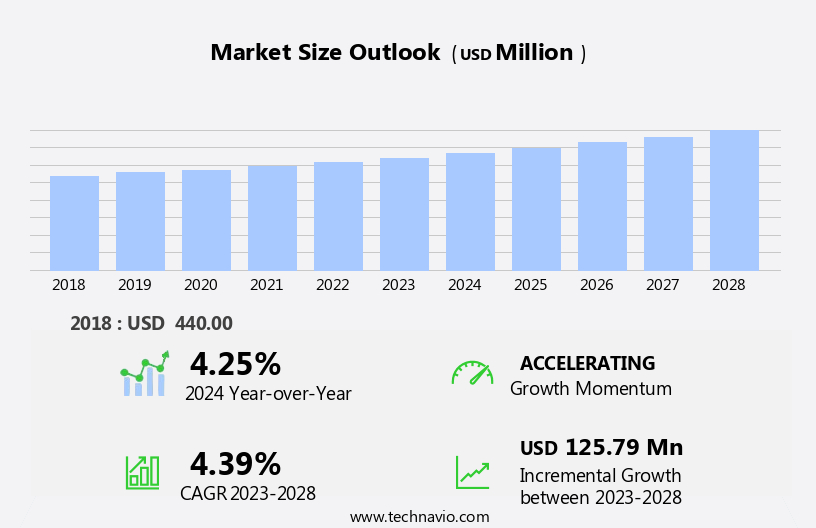

The fluorocarbon coating market size is forecast to increase by USD 125.79 million, at a CAGR of 4.39% between 2023 and 2028.

- The market is driven by the increasing demand for this coating in various industries, particularly in automotive applications due to its excellent non-stick and non-wetting properties. Another trend shaping the market is the shift towards water-based fluorocarbon coatings, which offer environmental benefits and reduce the reliance on solvents. However, the market faces challenges, including the unstable prices of fluorspar, a key raw material for PTFE coatings, which can impact the production costs and profitability of fluorocarbon coating manufacturers.

- Companies in the market must navigate these challenges while capitalizing on the growing demand for fluorocarbon coatings and the shift towards water-based alternatives to maintain a competitive edge.

What will be the Size of the Fluorocarbon Coating Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the constant demand for high-performance coatings across various sectors. The protective coating layer, which forms the basis of this market, undergoes continuous development, with solvent-based and water-based fluorocarbon options available. Polytetrafluoroethylene (PTFE) remains a key fluorocarbon polymer, but perfluoroalkoxy alkanes (PFA) and polyvinylidene fluoride (PVDF) are also gaining traction due to their unique properties. Substrate surface preparation plays a crucial role in the success of fluorocarbon coatings. Proper preparation ensures optimal adhesion and longevity. Fluorocarbon resin selection and tensile strength measurement are essential steps in the coating application process, ensuring the desired coating properties.

Chemical vapor deposition (CVD) and plasma-enhanced CVD are popular coating application methods, offering excellent uniformity and thickness control. Hydrophobic surface coating is a significant application area, with water-repellent properties essential in various industries. Coating durability assessment is ongoing, with abrasion resistance testing and corrosion protection methods critical to maintaining the performance of fluorocarbon coatings. Coating adhesion strength is another key factor, ensuring the coating remains bonded to the substrate under various conditions. High-performance coatings require stringent testing for chemical resistance, UV resistance, and fluoropolymer film thickness. Surface tension reduction and coating defect analysis are also essential to ensure the desired coating properties.

The fluorocarbon release agent market is a growing segment, with applications in various industries, including automotive, construction, and electronics. The electrostatic coating process is another application method, offering advantages in terms of efficiency and cost-effectiveness. The ongoing development of fluorocarbon coatings is a dynamic process, with new applications and technologies continually emerging. The market's evolution reflects the evolving needs of industries, with a focus on improving coating performance, durability, and sustainability.

How is this Fluorocarbon Coating Industry segmented?

The fluorocarbon coating industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Solvent-borne

- Water-borne

- Type

- PTFE

- PVDF

- FEP

- FEVE

- Others

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Technology Insights

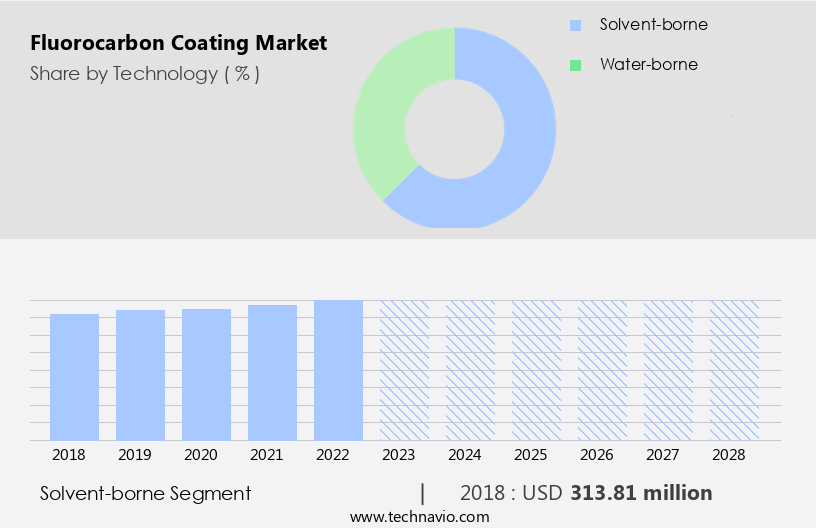

The solvent-borne segment is estimated to witness significant growth during the forecast period.

Solvent-borne fluorocarbon coatings, a type of protective coating, are applied as liquid chemicals onto various material surfaces to ensure corrosion resistance. These coatings exhibit superior performance under harsh conditions, including high temperatures and humidity during the curing process. However, they contain high levels of volatile organic compounds (VOC), making them environmentally harmful. Regulations under the Clean Air Act (CAA), such as the hazardous air pollutants (HAP) emission standards, govern the use of solvent-borne coatings in industries like aerospace, automotive, architectural and industrial, consumer products, metal parts, and dry cleaners. Despite the environmental concerns, fluorocarbon polymers like polytetrafluoroethylene (PTFE), polyvinylidene fluoride (PVDF), and others, which are major players in the market, remain solvent-borne.

Coating application methods include plasma-enhanced chemical vapor deposition (CVD), electrostatic process, thermal spray, and powder coating application. Coating properties include abrasion resistance, non-stick surface creation, hydrophobic surface coating, and chemical resistance. Coating durability assessment involves testing for tensile strength, coating adhesion strength, and fluoropolymer film thickness. UV resistance properties and fluorocarbon molecular weight are also essential factors. Coating defect analysis and corrosion protection methods are critical in ensuring the quality and effectiveness of the coatings.

The Solvent-borne segment was valued at USD 313.81 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

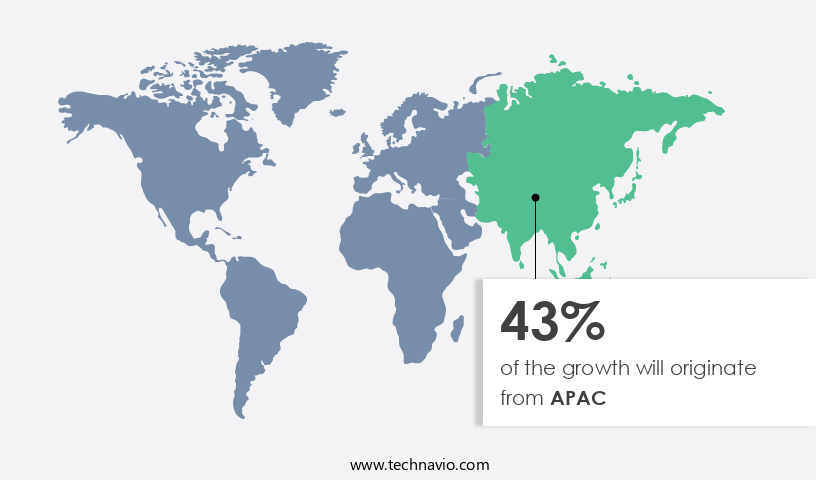

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market experienced significant growth in 2020, with APAC being the largest consumer due to increasing demands from industries such as textile and automotive. In the textile sector, polytetrafluoroethylene (PTFE) is utilized for manufacturing fiber, filament, yarn, and fabric. Countries like China and India, leading consumers of textiles in APAC, will continue driving demand for fluorocarbon coating. Additionally, the region's construction industry growth, as evidenced by Samsung's investment plan in India for a new smartphone display plant, further influences market expansion. Coating application methods include plasma-enhanced chemical vapor deposition (CVD), electrostatic, and thermal spray. Fluorocarbon polymers, such as perfluoroalkoxy alkanes (PFA) and polyvinylidene fluoride (PVDF), offer properties like high abrasion resistance, chemical resistance, hydrophobic surface coating, and UV resistance.

Coating adhesion strength, tensile strength measurement, and defect analysis are crucial factors ensuring coating durability. Fluorocarbon resin selection, substrate surface preparation, and coating application processes like water-based fluorocarbon and powder coating application are essential considerations for manufacturers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the realm of advanced material science, the market holds significant importance, particularly in the United States, where innovation and trust are paramount. This market, characterized by its continuous evolution, focuses on various applications, including aerospace, medical devices, food processing, architectural, and industrial sectors. Fluorocarbon coatings, renowned for their exceptional chemical resistance properties, are applied using techniques such as PTFE coating and fluorocarbon nanocoating. These methods offer self-cleaning surfaces, enhancing the convenience and exclusivity of the protected components. The durability of fluorocarbon coatings is a critical element, which is improved through surface energy modification and thickness control techniques. Testing methods for fluorcarbon coating adhesion and measuring abrasion resistance are essential in optimizing the curing process. Environmental effects, including the disposal of these coatings, are crucial considerations. Incorporating fluorocarbon resins appropriate for specific applications and comparing different application methods are key areas that involve ongoing research and development. Studies highlight the long-term performance of fluorocarbon coatings in various industries. For instance, in medical devices, fluorocarbon coatings ensure biocompatibility and reduce the risk of surgical site infections. In aerospace applications, they provide corrosion protection, contributing to the reliability and safety of aircraft. In food processing, fluorocarbon coatings maintain the integrity of surfaces, ensuring product purity. The impact of substrate surface preparation on fluorocarbon coatings is a critical factor in their successful application. Selecting the right fluorocarbon resins for specific applications and assessing their long-term performance are ongoing challenges that the market addresses through rigorous research and development. The trust that consumers place in these advanced coatings is well-founded, as they provide unparalleled protection and performance in various industries.

What are the key market drivers leading to the rise in the adoption of Fluorocarbon Coating Industry?

- The significant surge in demand for fluorocarbon coatings, particularly in the automotive industry, serves as the primary growth driver for this market.

- Fluorocarbon coatings play a crucial role in the automotive industry by enhancing vehicle performance and durability. These coatings, primarily in the form of polytetrafluoroethylene (PTFE), polyperfluoroalkyl ethers (PFA), and fluorinated ethylene-propylene (FEP), are applied to various components using different methods, including solvent-based and plasma-enhanced chemical vapor deposition (CVD). The protective coating layer offers several advantages, such as reducing corrosion and noise, providing controlled torque tension, and improving resistance to fuels, fluids, and lubricants. Fluorocarbon coatings are applied to components like door/window seals, solenoid and suspension components, piston skirts, connecting rods, assembly aids, and connectors.

- The coatings' unique properties, including abrasion resistance and low friction, make them ideal for withstanding extreme weather conditions and exposure to road debris. By protecting engine components from corrosion, fluorocarbon coatings extend the lifespan of vehicles and ensure optimal performance. The coatings' non-stick surface creation further enhances their value in the automotive industry.

What are the market trends shaping the Fluorocarbon Coating Industry?

- Water-based fluorocarbon coatings are experiencing significant growth in the market, representing an emerging trend in this industry. This shift towards more eco-friendly and sustainable coating solutions is a noteworthy development.

- The market is experiencing significant growth due to the increasing demand for sustainable and eco-friendly coatings. One key trend in this market is the rising use of water-based fluorocarbon coatings as an alternative to traditional solvent-based formulations. This shift is primarily driven by stringent regulatory requirements and the industry's commitment to reducing its environmental footprint. Water-based fluorocarbon coatings offer several advantages over their solvent-based counterparts. They emit fewer volatile organic compounds (VOCs), have a lower environmental impact, and provide improved worker safety during application. As a result, they are gaining popularity in various industries, including architectural coatings and automotive finishes.

- The shift towards water-based fluorocarbon coatings is an essential step in the evolution of the global market towards more sustainable and eco-friendly methods. Substrate surface preparation and fluorocarbon resin selection are critical factors in ensuring the success of these coatings. Tensile strength measurement and coating adhesion strength are essential properties that must be considered during the selection process. Perfluoroalkoxy alkanes (PFA) and polyvinylidene fluoride (PVDF) are commonly used fluorocarbon resins in the production of these coatings. Chemical vapor deposition (CVD) is a popular method for applying fluorocarbon coatings due to its ability to provide a uniform and consistent coating.

- The hydrophobic surface coating produced through this process offers excellent resistance to weathering, chemicals, and UV radiation. In conclusion, the market is undergoing a transformation as the industry embraces more sustainable and eco-friendly methods. The use of water-based fluorocarbon coatings is a significant development in this market, driven by regulatory requirements and a growing awareness of environmental concerns. Proper substrate surface preparation, fluorocarbon resin selection, and coating application techniques are essential to ensure the success of these coatings.

What challenges does the Fluorocarbon Coating Industry face during its growth?

- The instability of fluorspar prices poses a significant challenge to the growth of the PTFE coatings industry. Fluorspar is an essential raw material in the production of PTFE coatings, and its price volatility can negatively impact the industry's profitability and competitiveness. Procurement costs make up a significant portion of the overall production expenses, making it crucial for manufacturers to secure stable and predictable pricing for fluorspar to ensure sustainable business growth.

- Fluorocarbon coatings, known for their high-performance properties, accounted for a significant market share in 2020. The leading type, PTFE, is derived from the polymerization of tetrafluoroethylene (TFE), which is produced from fluorspar, hydrofluoric acid, and chloroform. Fluorspar, as a crucial raw material, has experienced a surge in demand, resulting in price increases due to its limited availability. In June 2021, China's fluorspar imports surged by over 675% compared to the previous year. This heightened demand for fluorspar has compelled major TFE manufacturers to rely on their suppliers and producers. The electrostatic coating process is widely used in the application of fluorocarbon coatings due to its ability to provide uniform film thickness.

- The coatings offer excellent chemical resistance and UV resistance properties, making them suitable for various industries such as automotive, aerospace, and electronics. Water-based fluorocarbon coatings have gained popularity due to their eco-friendly nature. They undergo rigorous testing for chemical resistance and film thickness to ensure their performance matches that of their solvent-based counterparts. Fluorocarbon release agents are also essential in the manufacturing process to prevent the coating from sticking to surfaces during application. In assessing the coating's durability, various tests are conducted to evaluate its resistance to weathering, abrasion, and temperature extremes. These tests provide valuable insights into the coatings' overall performance and longevity.

Exclusive Customer Landscape

The fluorocarbon coating market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fluorocarbon coating market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, fluorocarbon coating market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Fluorocarbon coatings are a key offering from this global technology leader, encompassing 3M's FC-4432, Easy Clean Coating ECC-1000, and FR-2025 flame retardant additive. These advanced coatings deliver enhanced performance in various industries, from automotive to construction, through improved resistance and durability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AGC Inc.

- Akzo Nobel NV

- Arkema Group

- Blinex Filter-Coat Pvt. Ltd.

- Daikin Industries Ltd.

- DuPont de Nemours Inc.

- Fluorocarbon Co. Ltd.

- Gujarat Fluorochemicals Ltd.

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- Pexco LLC

- PPG Industries Inc.

- Rollstud Ltd.

- Solvay SA

- SP Group AS

- TECHNICOAT S. R. O.

- The Chemours Co.

- Tribology India Ltd.

- Zhuhai Fute Science and Technology Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fluorocarbon Coating Market

- In January 2024, DuPont announced the launch of its new line of high-performance fluorocarbon coatings, Foralutex Xynergy, designed for the solar energy industry. These coatings are expected to enhance the efficiency of solar panels by reducing energy losses and increasing durability (DuPont Press Release, 2024).

- In March 2024, 3M and H.B. Fuller Company entered into a strategic partnership to expand their offerings in the fluorocarbon coatings market. The collaboration aimed to combine 3M's advanced coating technologies with H.B. Fuller's adhesives and sealants, creating innovative solutions for various industries (3M Press Release, 2024).

- In May 2024, PPG Industries completed the acquisition of Whitford, a leading global manufacturer of fluoropolymer coatings. This acquisition expanded PPG's presence in the high-performance coatings market and provided access to Whitford's advanced coating technologies (PPG Industries Press Release, 2024).

- In February 2025, the European Union approved the use of fluorocarbon coatings in refrigeration systems, following a comprehensive evaluation of their environmental impact. This approval marked a significant step forward in the adoption of these coatings in the European market (European Commission Press Release, 2025).

Research Analyst Overview

- The market encompasses various applications, including corrosion inhibition, self-cleaning surfaces, and anti-fouling. Coating thickness uniformity is crucial for optimal performance, while fluorocarbon recycling reduces environmental impact. Fluorocarbon nanocoatings offer enhanced properties such as increased crosslinking density and wear resistance. Gloss level determination and friction coefficient testing are essential for assessing coating quality. The curing process, including cure temperature optimization, significantly influences coating lifespan prediction. Oleophobic coatings and hydrophilic coatings cater to diverse industry needs. Surface contamination removal and anti-graffiti applications are gaining traction. Understanding the corrosion inhibition mechanism and film formation mechanism is vital for developing high-performance fluorocarbon coatings.

- Coating adhesion failure can lead to significant issues. Thermal stability testing and environmental impact assessment are crucial for assessing coating durability and sustainability. Polymeric coating blends offer versatility in addressing various application requirements. Coating color stability and surface morphology analysis provide valuable insights into coating properties. Fluorocarbon degradation and surface energy measurement are essential for understanding coating longevity and performance. Anti-graffiti coatings and anti-fouling coatings are essential in industries prone to contamination. Crosslinking density and coating wear resistance are essential factors in evaluating coating performance. Self-cleaning surfaces and anti-graffiti coatings are popular due to their ability to maintain appearance and reduce maintenance costs.

- Corrosion inhibition and anti-fouling mechanisms are critical for industrial applications, while hydrophilic and oleophobic coatings cater to consumer goods markets. Understanding the coating's properties and optimizing the application process is essential for achieving optimal performance. Fluorocarbon coatings offer various benefits, including enhanced durability, resistance to environmental factors, and improved surface properties. However, understanding the coating's properties, application process, and environmental impact is crucial for maximizing performance and sustainability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fluorocarbon Coating Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.39% |

|

Market growth 2024-2028 |

USD 125.79 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.25 |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Fluorocarbon Coating Market Research and Growth Report?

- CAGR of the Fluorocarbon Coating industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the fluorocarbon coating market growth of industry companies

We can help! Our analysts can customize this fluorocarbon coating market research report to meet your requirements.

RIA -

RIA -