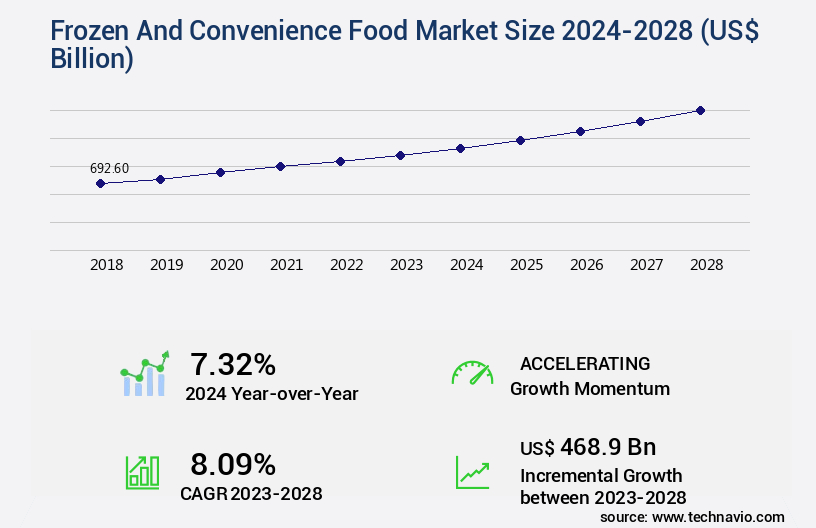

Frozen And Convenience Food Market Size 2024-2028

The frozen and convenience food market size is valued to increase USD 468.9 billion, at a CAGR of 8.09% from 2023 to 2028. Growing consumer inclination toward vegan frozen foods will drive the frozen and convenience food market.

Major Market Trends & Insights

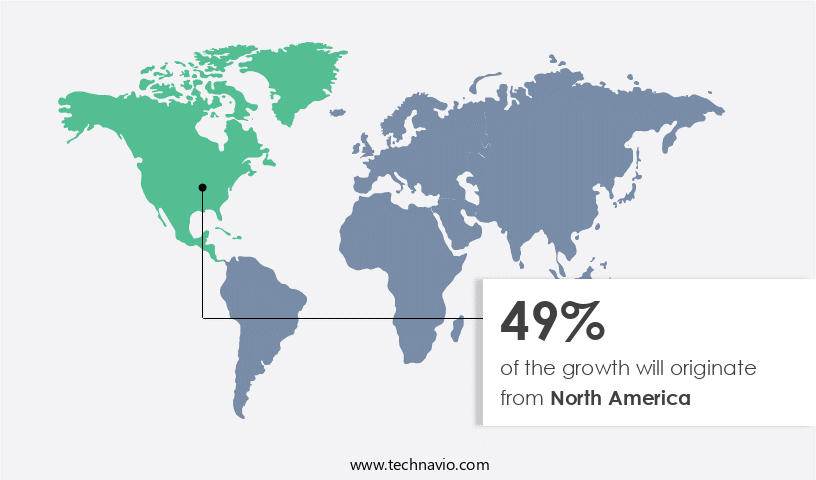

- North America dominated the market and accounted for a 49% growth during the forecast period.

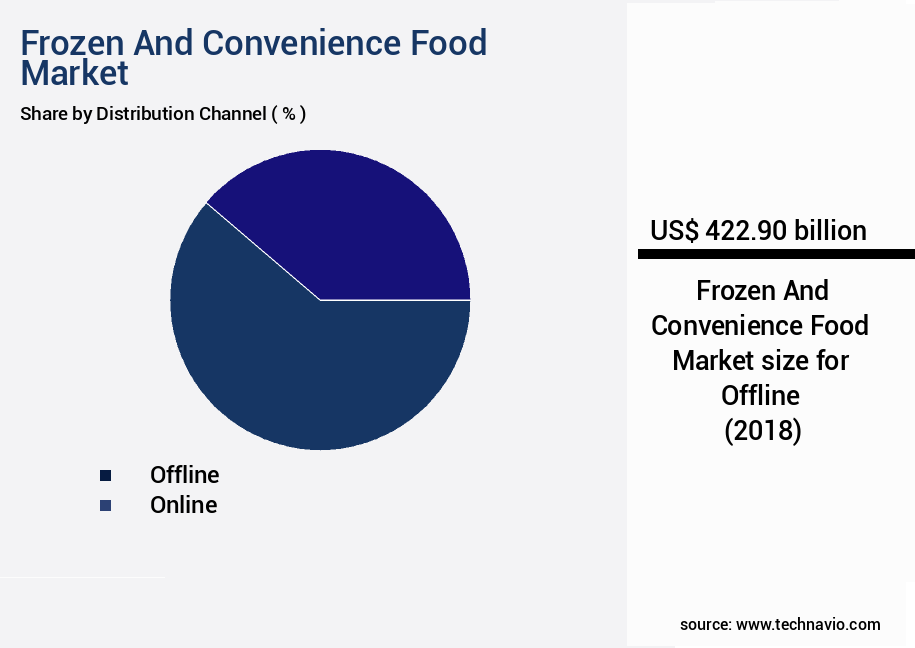

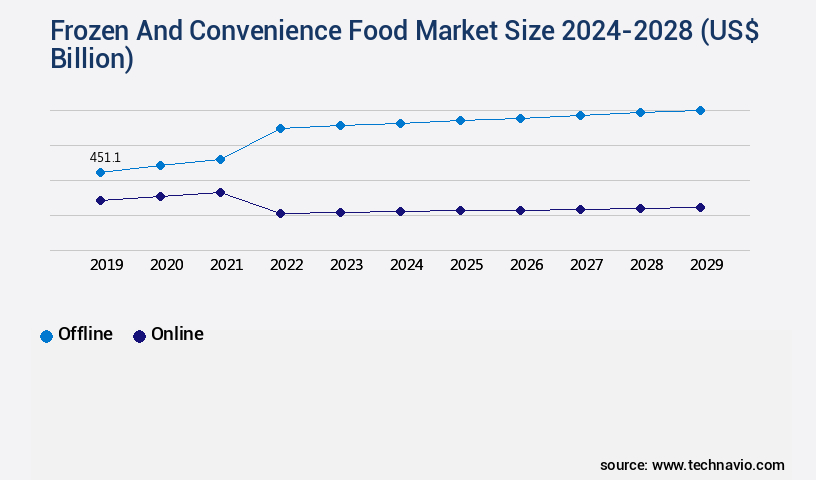

- By Distribution Channel - Offline segment was valued at USD 422.90 billion in 2022

- By Type - Convenience food segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 110.16 billion

- Market Future Opportunities: USD 468.90 billion

- CAGR from 2023 to 2028 : 8.09%

Market Summary

- The market has witnessed significant expansion in recent years, fueled by shifting consumer preferences and the increasing demand for time-saving solutions. According to market data, the global frozen food market was valued at over USD128 billion in 2020, with convenience foods accounting for a substantial portion of this figure. This trend is driven by several factors, including the escalating need for convenience in today's fast-paced world and the growing consumer inclination toward plant-based diets. The convenience food sector, which includes ready-to-eat meals, snacks, and beverages, has experienced remarkable growth due to its ability to cater to the busy lifestyles of modern consumers.

- Frozen foods, in particular, have gained popularity due to their extended shelf life and ease of preparation. However, this market segment faces challenges, such as health concerns related to the high sodium, sugar, and preservative content in many frozen food products. Despite these challenges, the market continues to evolve, with innovations in product development and manufacturing processes aimed at addressing consumer demands for healthier, more convenient options. For instance, companies are focusing on reducing sodium and sugar content, increasing the use of natural ingredients, and offering more plant-based and vegan alternatives. These efforts are expected to drive the market's future growth, as consumers increasingly seek out healthier, more convenient food solutions.

What will be the Size of the Frozen And Convenience Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Frozen And Convenience Food Market Segmented ?

The frozen and convenience food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Type

- Convenience food

- Frozen food

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with the offline segment holding a dominant position, accounting for approximately 75% of global sales. This segment includes supermarkets, hypermarkets, convenience stores, and local merchants, offering a wide variety of products such as frozen fruits, vegetables, ready meals, and snacks. Consumer preference for convenience, competitive pricing, and a vast selection of brands and stock-keeping units (SKUs) contribute to the growth of this distribution channel. In the production process, advanced technologies like IQF freezing, high-pressure processing, and vacuum packaging are employed to ensure extended shelf life and maintain food texture.

HACCP implementation, ingredient declaration standards, and food safety certifications are crucial for maintaining quality control and consumer trust. The market also prioritizes supply chain visibility and efficient refrigerated transport logistics to ensure product freshness and reduce waste. Notably, meal kit assembly lines and automated packaging systems have gained traction, streamlining production processes and optimizing costs.

The Offline segment was valued at USD 422.90 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Frozen And Convenience Food Market Demand is Rising in North America Request Free Sample

In The market, the European region held a significant market share in 2023. Key contributors to this growth include the UK, Germany, and Spain. Factors fueling the expansion of the European frozen food sector include strategic mergers and acquisitions (M&As) and innovative marketing strategies by companies. For instance, General Mills, a leading food company, bolstered its presence in the frozen food sector by acquiring TNT Crust, a prominent frozen pizza crust manufacturer.

This acquisition allowed General Mills to cater to the growing demand for healthier frozen food options. The European the market is expected to remain robust due to these trends.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market continues to experience significant growth, driven by various factors including the impact of freezing on food texture, methods for extending shelf life, and consumer preference for convenient meal solutions. Freezing plays a crucial role in preserving food's texture and taste, allowing businesses to offer a wide range of products that maintain their quality for extended periods. To optimize cold chain temperature and ensure food safety, advanced techniques in food freezing and efficient food distribution networks are essential. Sustainable food packaging choices, such as biodegradable materials, are increasingly important in addressing environmental concerns. Automated food packaging machinery streamlines production processes and reduces costs, while adhering to stringent food safety protocols and procedures.

Traceability in the frozen food supply chain is another critical factor, with the need for accurate record-keeping and transparency becoming increasingly important to consumers. Innovations in food preservation, such as high-pressure processing and vacuum microwave cooking, are improving energy efficiency in freezing and reducing food waste in processing. New trends in frozen food packaging include the use of advanced materials and designs to enhance food quality and extend shelf life. Improving energy efficiency in freezing and reducing costs in frozen food production are ongoing priorities for businesses, with ongoing research and development in these areas. Food safety standards for frozen foods are rigorously enforced, with quality control measures in freezing ensuring that products meet the highest standards for taste, texture, and safety. Optimizing the frozen food supply chain through efficient logistics and distribution networks is essential for businesses looking to remain competitive in this dynamic market.

What are the key market drivers leading to the rise in the adoption of Frozen And Convenience Food Industry?

- The increasing preference among consumers for vegan options, particularly in the frozen food sector, is the primary market trend.

- The vegan frozen food market is experiencing significant growth due to the increasing demand for plant-based options. This market encompasses a wide range of products, including plant-based food items and dairy alternatives. The rise in veganism and heightened consumer awareness of these food choices are key factors fueling market expansion. Notably, the UK and US markets exhibit substantial demand for vegan frozen foods, with consumers seeking meat alternatives.

- This trend has encouraged companies to broaden their product offerings, as evidenced by Nestle SA's introduction of plant-based sausages in Europe and the US in early 2020. The vegan frozen food market's continuous evolution reflects the dynamic nature of consumer preferences and the food industry at large.

What are the market trends shaping the Frozen And Convenience Food Industry?

- The increasing demand for convenience represents a significant market trend. A growing number of consumers prioritize ease and efficiency in their daily lives.

- The preference for ready-to-eat meals among consumers, driven by the desire for time savings and convenience, fuels the demand for frozen and convenience foods. This trend is further bolstered by advancements in refrigeration technologies, the rise of single-person and smaller households, and an increasing number of working women. Convenience is a critical factor for companies in the frozen food market, as consumers seek time-saving solutions for meal preparation and clean-up.

- Frozen food offerings provide this convenience, with easy handling and a wide array of flavorful options in various portion sizes. The flexibility and adaptability of frozen foods cater to the diverse needs of consumers, making it a continuously evolving and dynamic market.

What challenges does the Frozen And Convenience Food Industry face during its growth?

- The growth of the frozen food industry is confronted by significant health concerns associated with their consumption.

- Frozen foods, a significant segment of the processed food industry, undergo freezing to extend their shelf life and maintain freshness. However, the production process may involve substituting nutritious ingredients with less costly alternatives. For instance, olive oil, rich in antioxidants, is sometimes replaced with rapeseed oil in frozen meals. This substitution can negatively impact the nutritional value of the food. Regular consumption of frozen ready meals can pose health risks, including kidney disease, diabetes, dementia, obesity, and high blood pressure. These risks stem from the high fat and sodium content commonly found in frozen foods.

- Despite these concerns, the frozen food market continues to evolve, offering a diverse range of options catering to various dietary needs and preferences. Manufacturers are responding to consumer demands for healthier alternatives by introducing frozen meals with reduced sodium, lean proteins, and whole grains. The market's dynamic nature underscores the importance of making informed choices when selecting frozen food options.

Exclusive Technavio Analysis on Customer Landscape

The frozen and convenience food market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the frozen and convenience food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Frozen And Convenience Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, frozen and convenience food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - The company specializes in the production and distribution of frozen and convenience food products under the brands LingLing, JoseOle, and Ajinomoto. These brands cater to various cuisines, providing consumers with convenient meal solutions. The company's commitment to innovation and quality has resulted in a diverse product portfolio that caters to diverse consumer preferences.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Amys Kitchen Inc.

- Associated British Foods Plc

- Bakkavor Group PLC

- Cargill Inc.

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- EUROPASTRY SA

- General Mills Inc.

- JBS SA

- Kellogg Co.

- Lantmannen ekonomisk forening

- McCain Foods Ltd.

- MTR Foods Pvt. Ltd.

- Nestle SA

- Omar International Pvt. Ltd

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

- Vandemoortele NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Frozen And Convenience Food Market

- In January 2024, Nestle, the global food and beverage company, launched its new line of frozen meals, "Nestle FresMeals," in the US market. These meals, which cater to the growing demand for healthier and convenient food options, are made with fresh, locally-sourced ingredients and feature a microwavable packaging design for added convenience (Nestle Press Release, 2024).

- In March 2024, Unilever, another major player in the industry, announced a strategic partnership with Blue Apron Holdings, Inc., a leading meal kit company, to expand its reach in the US frozen meals market. The collaboration aimed to leverage Blue Apron's expertise in meal kit delivery and Unilever's extensive distribution network (Unilever Press Release, 2024).

- In May 2024, Conagra Brands, Inc. Completed the acquisition of Pinnacle Foods Inc. For approximately USD10.9 billion. This acquisition significantly expanded Conagra's portfolio in the frozen food segment, adding popular brands like Birds Eye, Duncan Hines, and Log Cabin to its offerings (Conagra Brands Press Release, 2024).

- In February 2025, the European Commission approved the acquisition of Ragu and Bertolli pasta sauces from Unilever by Mizkan Group, a Japanese food company. This approval marked the entry of Mizkan into the European frozen convenience food market and expanded its global footprint (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Frozen And Convenience Food Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.09% |

|

Market growth 2024-2028 |

USD 468.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and shifting consumer preferences. Ingredient sourcing strategies have become more sophisticated, with a focus on traceability and sustainability. For instance, a leading frozen food manufacturer increased sales by 15% by sourcing locally grown fruits and vegetables. Food texture analysis and modified atmosphere packaging are essential for maintaining product quality and extending shelf life. HACCP implementation and automated packaging lines ensure food safety and efficiency. Blast chilling systems and vacuum packaging methods enable longer shelf life extension, while inventory management systems optimize production and reduce waste. Sensory evaluation methods and nutritional labeling requirements cater to consumers' increasing focus on health and wellness.

- Frozen fruit and vegetable processing, using IQF freezing technology and high-pressure processing, ensures nutrient retention. Energy-efficient refrigeration and thermal processing techniques minimize environmental impact. Meal kit assembly and portion control packaging cater to the growing demand for convenience. Product traceability systems and supply chain visibility enable transparency and build consumer trust. Food safety certifications and ready meals production ensure regulatory compliance and meet evolving consumer expectations. The market is projected to grow by 3% annually, driven by these trends and innovations. Consumer preference testing and process optimization strategies continue to shape the industry landscape.

What are the Key Data Covered in this Frozen And Convenience Food Market Research and Growth Report?

-

What is the expected growth of the Frozen And Convenience Food Market between 2024 and 2028?

-

USD 468.9 billion, at a CAGR of 8.09%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline and Online), Type (Convenience food and Frozen food), and Geography (Europe, North America, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing consumer inclination toward vegan frozen foods, Health risks associated with consumption of frozen foods

-

-

Who are the major players in the Frozen And Convenience Food Market?

-

Ajinomoto Co. Inc., Amys Kitchen Inc., Associated British Foods Plc, Bakkavor Group PLC, Cargill Inc., Conagra Brands Inc., Corporativo Bimbo SA de CV, EUROPASTRY SA, General Mills Inc., JBS SA, Kellogg Co., Lantmannen ekonomisk forening, McCain Foods Ltd., MTR Foods Pvt. Ltd., Nestle SA, Omar International Pvt. Ltd, The Kraft Heinz Co., Tyson Foods Inc., Unilever PLC, and Vandemoortele NV

-

Market Research Insights

- The market for frozen and convenience food continues to evolve, with innovations in cost optimization modeling and retail display strategies driving growth. For instance, a leading food manufacturer achieved a 15% sales increase by optimizing its recipe formulation processes and implementing individual quick freezing techniques. Industry experts anticipate a 5% annual growth rate for this sector over the next five years, fueled by advancements in product lifecycle management, ingredient standardization, and storage temperature monitoring.

- Additionally, the industry is focusing on process efficiency improvements, e-commerce fulfillment, and distribution channel management to meet evolving consumer demands. Product quality assessment, sensory attribute profiling, and packaging material selection are also critical areas of focus to maintain consumer trust and preference.

We can help! Our analysts can customize this frozen and convenience food market research report to meet your requirements.

RIA -

RIA -