India Frozen Food Market Size 2026-2030

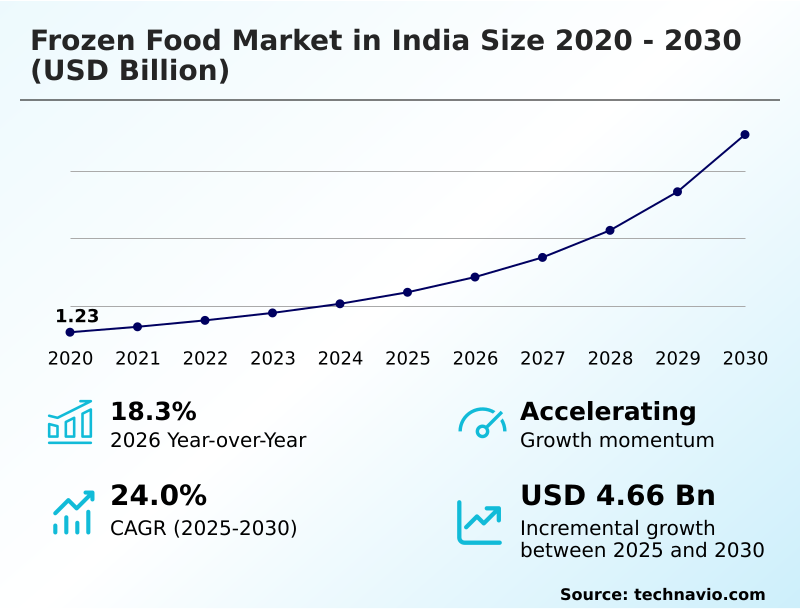

The india frozen food market size is valued to increase by USD 4.66 billion, at a CAGR of 24% from 2025 to 2030. Standardization of quick commerce and last mile cold chain integration will drive the india frozen food market.

Major Market Trends & Insights

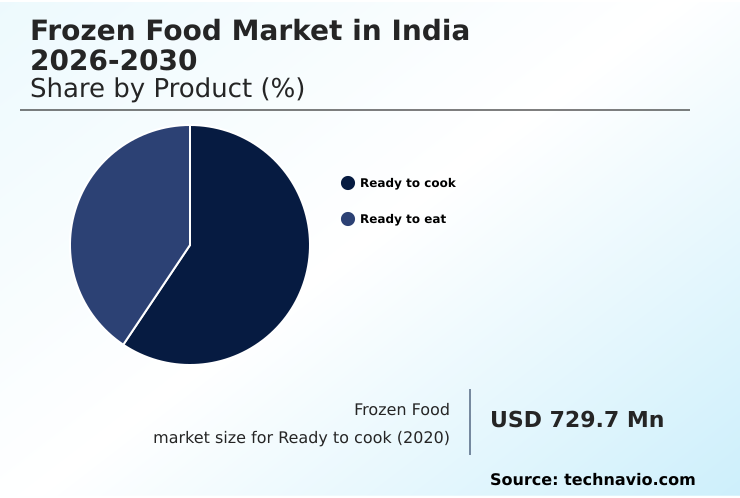

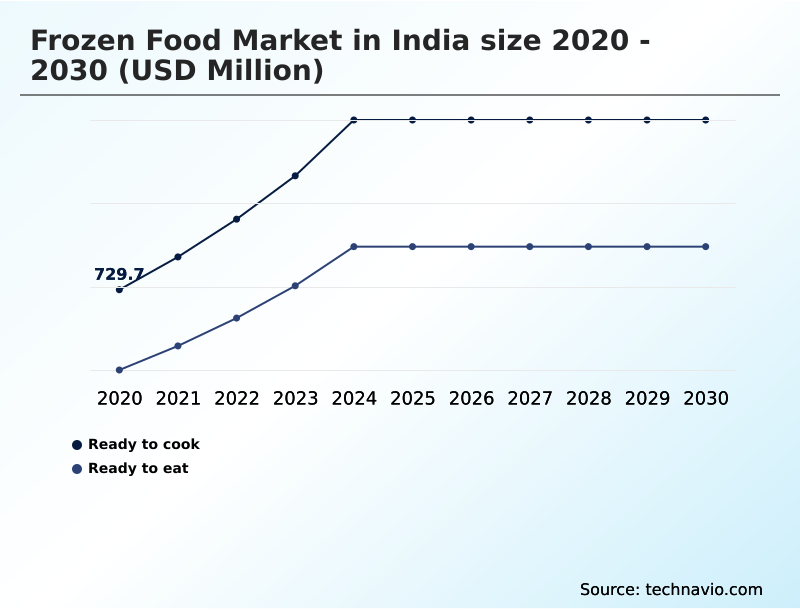

- By Product - Ready to cook segment was valued at USD 1.22 billion in 2024

- By Distribution Channel - Online segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.84 billion

- Market Future Opportunities: USD 4.66 billion

- CAGR from 2025 to 2030 : 24%

Market Summary

- The frozen food market in India is undergoing a significant transformation, driven by a confluence of evolving consumer lifestyles, technological advancements in food preservation, and infrastructural development. The market is moving beyond basic frozen vegetables to a sophisticated ecosystem of value-added products.

- This includes a wide array of ready-to-cook and ready-to-eat meals, snacks, and protein products designed for the urban consumer who prioritizes convenience without compromising on nutrition or taste. The proliferation of the organized retail sector and the rise of quick-commerce platforms have dramatically improved accessibility, addressing historical challenges of last-mile delivery.

- For instance, a logistics provider can leverage IoT-enabled cooling solutions to monitor and maintain temperature integrity across its fleet, ensuring that perishable goods arrive at micro-fulfillment centers in optimal condition, thereby reducing spoilage and building consumer trust.

- This integration of technology and logistics is pivotal, as is the industry's focus on clean-label products and sustainable sourcing to align with modern consumer values.

What will be the Size of the India Frozen Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the India Frozen Food Market Segmented?

The india frozen food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Ready to cook

- Ready to eat

- Distribution channel

- Online

- Offline

- Type

- Fruits and vegetables

- Meat and seafood products

- Dairy products

- Convenience food and ready meals

- Others

- Technique

- Individual quick freezing (IQF)

- Blast freezing

- Belt freezing

- Geography

- APAC

- India

- APAC

By Product Insights

The ready to cook segment is estimated to witness significant growth during the forecast period.

The ready-to-cook segment is a cornerstone of the market, balancing convenience with the tradition of freshly prepared meals. The growth is fueled by time-constrained professionals in urban centers who seek authentic flavors without extensive preparation.

This demand has spurred innovation in preservative-free formulations and products optimized for modern cooking methods. The category now includes diverse items from plant-based meats to artisanal frozen desserts.

In parallel, the ready-to-eat category is expanding with advanced heat-and-serve meal solutions and high-protein frozen snacks. The adoption of retort technology allows for complex dual-texture frozen snacks.

This segment's growth is accelerated by the high-velocity retail model of digital procurement, with some platforms seeing a 40% increase in repeat purchases for these items, challenging traditional food delivery services.

This evolution is supported by distribution through both modern brick-and-mortar networks and transformed traditional kirana stores, which now cater to diverse regional flavor profiles.

The Ready to cook segment was valued at USD 1.22 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the market reveals complex interdependencies between technology, infrastructure, and consumer perception. The impact of quick commerce on frozen food sales is undeniable, but it brings forth challenges in frozen food last-mile delivery, where maintaining thermal integrity is paramount.

- A significant hurdle remains the consumer perception of frozen vs fresh food, a deep-seated cultural bias against frozen foods that educational marketing must address. Highlighting the role of iqf in preserving nutritional value and promoting clean-label trends in the frozen food sector are key strategies.

- Furthermore, government incentives for the food processing industry are critical for managing energy costs in cold chain operations and encouraging strategies for reducing post-harvest losses. Success hinges on mastering advancements in ready-to-eat meal technology and understanding the market potential for ethnic frozen food varieties, such as by developing dual-texture gourmet frozen snacks.

- The integration of IoT in cold chain monitoring and technological advancements in blast freezing tunnels are enabling better quality control, crucial for improving texture of frozen meat products. For instance, firms using real-time monitoring have reported spoilage rates nearly 50% lower than those using traditional methods.

- Ultimately, the industry's future depends on a holistic approach that combines trends in plant-based frozen alternatives, addresses challenges of power reliability for cold storage, and emphasizes the importance of transparent sourcing in frozen foods and the role of packaging in maintaining thermal integrity.

What are the key market drivers leading to the rise in the adoption of India Frozen Food Industry?

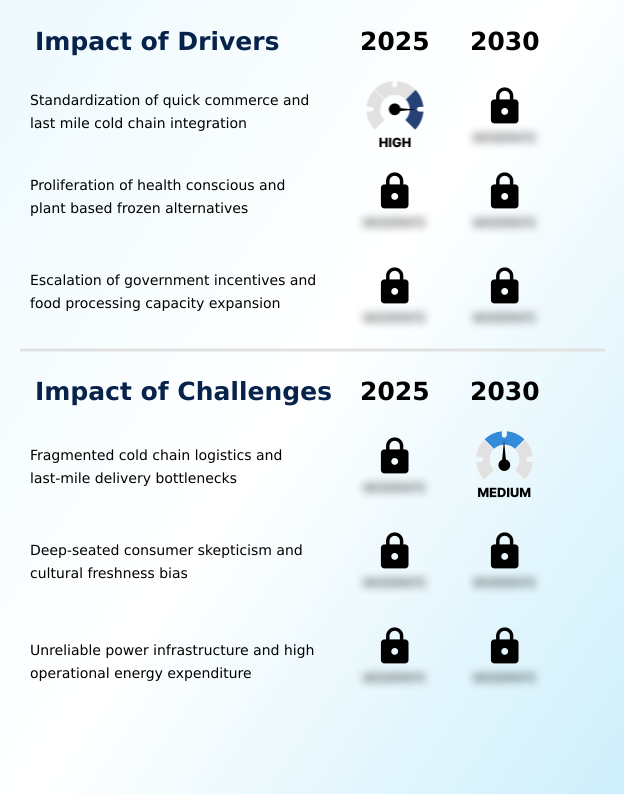

- The standardization of quick commerce and the integration of last-mile cold chain infrastructure are key drivers propelling market growth.

- The institutionalization of quick-commerce is a primary driver, integrating dark stores and micro-fulfillment centers into the urban fabric. These facilities depend on flash-freezing technology and robust refrigerated transport to maintain product temperature integrity and thermal integrity from storage to delivery.

- One major platform reported a 99.8% success rate in maintaining temperature thresholds. This logistical framework supports the growth of clean-label frozen produce.

- Consumers are increasingly demanding traceable sourcing and high hygiene standards, which manufacturers are addressing through advanced culinary engineering and precise recipe standardization.

- This focus ensures consistent sensory appeal and quality, with products offering standardized portioning to meet the needs of modern households seeking both convenience and nutritional transparency.

What are the market trends shaping the India Frozen Food Industry?

- The industrialization of clean-label frozen produce is an emerging market trend, driven by consumer demand for transparent and minimally processed food options.

- Market evolution is driven by technological adoption and shifting consumer attitudes. While techniques like individual quick freezing and blast freezing are becoming standard for quality preservation, the primary focus is on overcoming logistical hurdles. Efficient cold chain logistics, especially for last-mile delivery, is critical.

- This is where quick commerce platforms are making a significant impact, with adoption rates in metropolitan areas increasing by over 60% in the last two years. This helps counter deep-seated consumer skepticism and cultural freshness bias against both ready-to-cook and ready-to-eat products.

- However, the success of this model is challenged by unreliable power infrastructure and the high cost of energy-intensive operations, which can disrupt the entire process from warehouse to consumer and require significant supply chain verticalization.

What challenges does the India Frozen Food Industry face during its growth?

- Fragmented cold chain logistics and bottlenecks in last-mile delivery present a key challenge affecting industry growth.

- A key challenge is aligning government initiatives with on-ground operational realities. While the production linked incentive scheme aims to boost food processing capacity and reduce post-harvest losses, its effectiveness is hampered by logistical gaps. The goal is to create a seamless farm-gate to consumer journey, but this requires significant investment in cost-effective cold storage and infrastructure to achieve audit-grade sustainability.

- Advanced techniques such as individual quick freezing technology, vacuum-sealing, and nitrogen-flushing are crucial for producing high-quality ethnic frozen food and other value-added products like portion-controlled entrees and calorie-mapped entrees. Creating this efficient farm-to-freezer ecosystem remains a complex undertaking that impacts the industry's ability to scale efficiently and compete globally.

Exclusive Technavio Analysis on Customer Landscape

The india frozen food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india frozen food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Frozen Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india frozen food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADF Foods Ltd. - Offers a diversified portfolio of frozen food products, including ready meals, ethnic foods, seafood, and bakery items, catering to global consumer and foodservice segments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADF Foods Ltd.

- Ajinomoto Co. Inc.

- Apex Frozen Foods Ltd.

- Associated British Foods Plc

- Conagra Brands Inc.

- Corporativo Bimbo SA de CV

- General Mills Inc.

- Godrej Agrovet Ltd.

- ITC Ltd.

- McCain Foods Ltd.

- Meatzza

- Mother Dairy Pvt. Ltd.

- Nestle SA

- PAL Frozen Foods

- Pepizo Foods

- Pyramid EATS

- Swadhika Foods

- Tanvi Foods India Ltd

- Unilever PLC

- VH Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India frozen food market

- In May 2025, HyFun Foods announced its entry into the domestic retail market with a line of specialized ready-to-cook products, including Mumbai Aloo Vada, to address urban supply chain demands.

- In March 2025, ITC Ltd. secured regulatory approval for a new integrated food processing park in North India, focusing on expanding its capacity for its Master Chef range of frozen snacks and meals.

- In December 2024, McCain Foods Ltd. entered into a strategic partnership with a leading quick-commerce platform to ensure exclusive placement and 15-minute delivery for its premium line of appetizers across metropolitan areas.

- In September 2024, Mother Dairy Pvt. Ltd. launched a new line of organic frozen vegetables, leveraging blockchain-enabled traceability to provide consumers with verifiable farm-to-freezer sourcing information.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Frozen Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 211 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24% |

| Market growth 2026-2030 | USD 4657.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.3% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's structural evolution is defined by the industrial-scale adoption of advanced preservation and distribution technologies. The integration of individual quick freezing technology, flash-freezing technology, blast freezing, and belt freezing is foundational to creating clean-label frozen produce and other value-added items.

- This technological push is coupled with infrastructural investments in cold chain logistics, including dark stores, micro-fulfillment centers, and sophisticated refrigerated transport, to ensure temperature integrity during last-mile delivery. For boardroom decisions, the focus is on achieving a seamless farm-to-freezer ecosystem through cold-chain digitalization, utilizing smart refrigeration, IoT-enabled cooling solutions, and temperature-sensitive labeling.

- Companies are achieving a 30% reduction in spoilage through such systems. This addresses critical issues like post-harvest losses and enhances food processing capacity.

- The strategic pivot is toward high-value products like high-protein frozen snacks, plant-based meats, and artisanal frozen desserts, which demand advanced techniques like vacuum-sealing, nitrogen-flushing, and retort technology to create dual-texture frozen snacks and convenient heat-and-serve meal solutions while maintaining preservative-free formulations. This requires navigating a complex landscape involving solar-powered cooling, automated warehousing, and efficient hub-and-spoke distribution models.

What are the Key Data Covered in this India Frozen Food Market Research and Growth Report?

-

What is the expected growth of the India Frozen Food Market between 2026 and 2030?

-

USD 4.66 billion, at a CAGR of 24%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Ready to cook, and Ready to eat), Distribution Channel (Online, and Offline), Type (Fruits and vegetables, Meat and seafood products, Dairy products, Convenience food and ready meals, and Others), Technique (Individual quick freezing (IQF), Blast freezing, and Belt freezing) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Standardization of quick commerce and last mile cold chain integration, Fragmented cold chain logistics and last-mile delivery bottlenecks

-

-

Who are the major players in the India Frozen Food Market?

-

ADF Foods Ltd., Ajinomoto Co. Inc., Apex Frozen Foods Ltd., Associated British Foods Plc, Conagra Brands Inc., Corporativo Bimbo SA de CV, General Mills Inc., Godrej Agrovet Ltd., ITC Ltd., McCain Foods Ltd., Meatzza, Mother Dairy Pvt. Ltd., Nestle SA, PAL Frozen Foods, Pepizo Foods, Pyramid EATS, Swadhika Foods, Tanvi Foods India Ltd, Unilever PLC and VH Group

-

Market Research Insights

- The market's dynamism is driven by a significant consumer behavior shift toward convenience-led nutrition, facilitated by the rise of quick commerce platforms. This has created a high-velocity retail model where digital procurement is paramount. However, this growth is tempered by consumer skepticism and a strong cultural freshness bias.

- To succeed, companies must focus on traceable sourcing and high hygiene standards to build trust. The expansion of the organized retail sector into new regions and the modernization of traditional kirana stores via brick-and-mortar networks are also crucial. One study shows that brands with transparent sourcing saw a 15% higher retention rate compared to competitors.

- Success depends on navigating these dynamics, from managing energy-intensive operations to perfecting the sensory appeal of products through advanced culinary engineering and recipe standardization.

We can help! Our analysts can customize this india frozen food market research report to meet your requirements.

RIA -

RIA -