Generative AI In Life Sciences Market Size 2026-2030

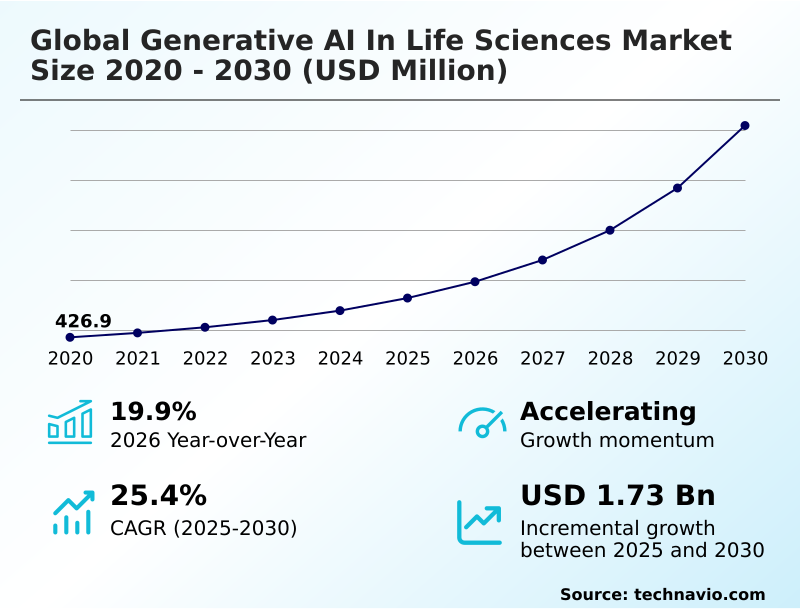

The generative ai in life sciences market size is valued to increase by USD 1.73 billion, at a CAGR of 25.4% from 2025 to 2030. Acceleration of De novo molecular design and therapeutic discovery will drive the generative ai in life sciences market.

Major Market Trends & Insights

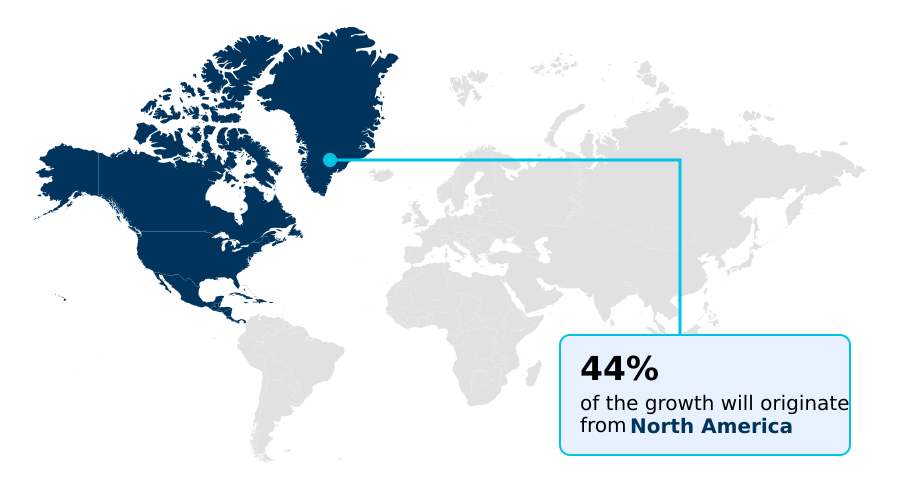

- North America dominated the market and accounted for a 43.8% growth during the forecast period.

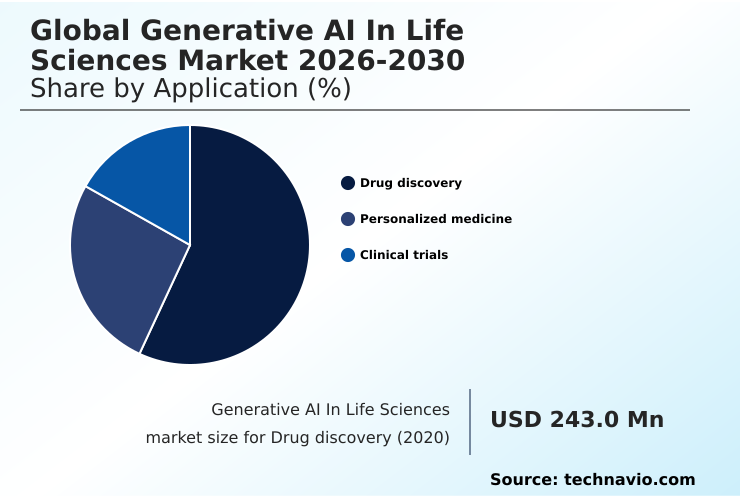

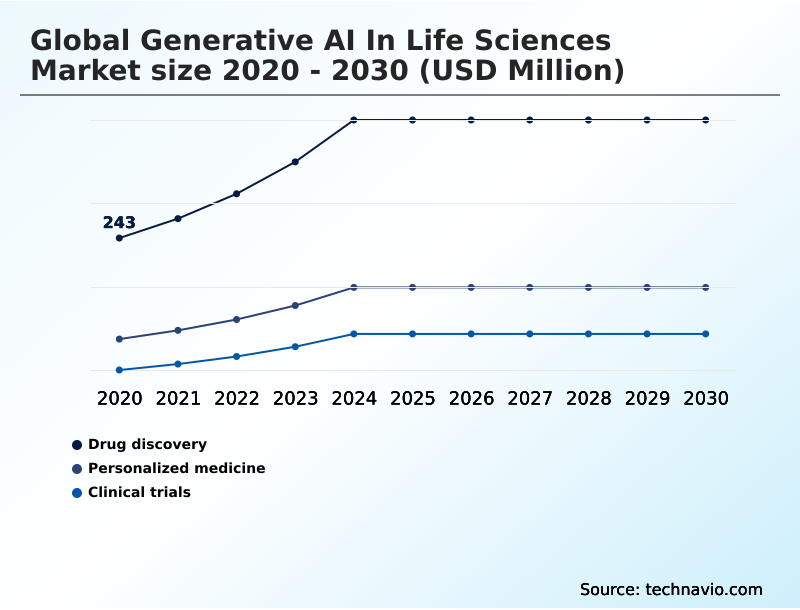

- By Application - Drug discovery segment was valued at USD 396.1 million in 2024

- By Technology - Novel molecule generation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.12 billion

- Market Future Opportunities: USD 1.73 billion

- CAGR from 2025 to 2030 : 25.4%

Market Summary

- The generative AI in life sciences market is redefining therapeutic development by enabling the autonomous generation of novel biological and chemical data. This technology leverages biological foundation models and multi-omics data integration to accelerate preclinical development and enhance molecular modeling.

- A key driver is the radical compression of discovery timelines through de novo molecular design, allowing for rapid therapeutic candidate discovery. However, the sector faces challenges related to the need for curated training data and ensuring model interpretability to avoid algorithmic hallucinations.

- In a typical scenario, a pharmaceutical firm utilizes a generative platform with a synthetic control arm to simulate clinical trial outcomes, reducing patient recruitment costs and accelerating regulatory submissions. This is driven by autonomous agentic workflows and synthetic digital twins, which are becoming central to modern drug discovery and precision oncology.

- The industry is moving towards a future where computational biology and generative chemistry shorten the path from lab to clinic, supported by robust machine learning operations and algorithmic guardrails to ensure safety and efficacy.

What will be the Size of the Generative AI In Life Sciences Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative AI In Life Sciences Market Segmented?

The generative ai in life sciences industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Drug discovery

- Personalized medicine

- Clinical trials

- Technology

- Novel molecule generation

- Protein sequence design

- Synthetic gene design

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Israel

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The drug discovery segment is estimated to witness significant growth during the forecast period.

The drug discovery segment is undergoing a fundamental paradigm shift, moving from traditional trial-and-error to a structured, predictive design process. This evolution is centered on de novo molecular design and advanced computational chemistry.

Generative AI accelerates lead optimization and the entire hit-to-lead journey through sophisticated in silico modeling and predictive analytics. Instead of relying solely on high-throughput screening, these systems perform rapid compound screening for target identification, dramatically compressing discovery timelines.

One key performance indicator shows that this structure-based drug discovery approach has reduced the need for physical validation by over 90% in certain preclinical phases.

This efficiency is achieved through deep learning algorithms that guide therapeutic candidate discovery, ensuring a more focused and resource-effective pathway for novel treatments.

The Drug discovery segment was valued at USD 396.1 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Life Sciences Market Demand is Rising in North America Get Free Sample

The global generative AI in life sciences market exhibits distinct regional dynamics, with North America leading, accounting for 43.8% of incremental growth. This is fueled by a mature ecosystem for biomedical research and access to high-performance computing.

Europe, representing 24.5% of the opportunity, focuses on precision oncology and drug repurposing within a stringent regulatory environment that prizes real-world evidence and explainable AI.

The APAC region is the fastest-growing, driven by national initiatives supporting synthetic gene design and the modernization of healthcare. This region leverages diffusion models and generative adversarial networks to innovate.

Across all regions, the use of variational autoencoders in trial protocol optimization and the development of a data-liquid ecosystem for analyzing cell painting assays and biomedical ontologies are becoming critical for maintaining a competitive edge.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of generative AI in the life sciences sector is revolutionizing therapeutic development from inception to clinical application. A core application is the use of generative AI for protein structure prediction, which provides the foundational data necessary for more advanced tasks like generative AI for de novo drug design.

- This capability directly supports generative AI for novel molecule generation, enabling researchers to explore chemical spaces that were previously inaccessible. The insights gained are then applied to generative AI for therapeutic antibody design and in drug repurposing strategies.

- Further down the pipeline, generative AI in clinical trial optimization is transforming how studies are designed and executed, with generative AI for clinical trial data synthesis creating realistic patient cohorts. This also aids generative AI for biomarker identification and generative AI for multi-omics data analysis.

- The technology's reach extends to generative AI for biomedical research, where it powers generative AI for automated lab experiments and generative AI in high-content imaging analysis. For instance, one platform demonstrated the ability to reduce lead optimization timelines by over 85%, condensing an 18-month process into less than 60 days.

- This acceleration is also seen in generative AI in computational chemistry and generative AI for predictive toxicology modeling, improving safety profiles. Other key applications include generative AI for synthetic biology applications, generative AI for real-world evidence generation, and generative AI for pharmacovigilance automation, all managed through specialized generative AI platforms for life sciences.

What are the key market drivers leading to the rise in the adoption of Generative AI In Life Sciences Industry?

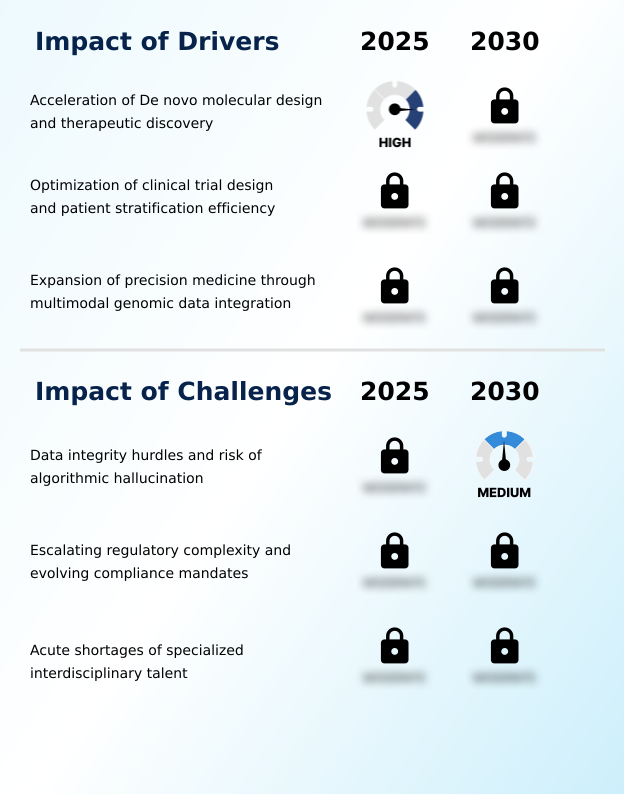

- A key market driver is the acceleration of de novo molecular design and therapeutic discovery, enabled by generative AI.

- Market growth is primarily driven by the capacity of generative AI to radically accelerate therapeutic discovery and enable a new tier of precision medicine.

- The use of advanced multimodal architectures for genomic analysis and protein sequence design allows for a deeper understanding of disease mechanisms.

- This is exemplified by the application of computational biology to perform molecular modeling and molecular dynamics simulation, which has been shown to increase the success rate of preclinical development candidates by over 25%.

- These technologies facilitate automated hypothesis generation and the construction of detailed knowledge graphs from vast datasets.

- As a result, AI-driven diagnostics and clinical decision support tools are becoming more sophisticated, leveraging insights from cell painting assays and biomedical ontologies to guide treatment strategies and streamline pharmacokinetics studies.

What are the market trends shaping the Generative AI In Life Sciences Industry?

- A key trend is the industrialization of autonomous agentic research workflows. This marks a shift from passive assistive tools to systems capable of multi-step scientific task execution.

- Key market trends are centered on the industrialization of autonomous agentic workflows and the adoption of synthetic digital twins for clinical development. This shift is powered by biological foundation models and large action models that facilitate automated hypothesis generation and complex scientific tasks.

- Organizations are increasingly using synthetic control arms in trials, which has been shown to reduce recruitment needs by up to 40% in certain rare disease studies. This approach, supported by digital biomarkers and federated learning, enables more efficient patient stratification. Furthermore, the practice of digital twin creation allows for predictive modeling of patient outcomes.

- The trend is toward integrated platforms where human-in-the-loop validation remains a critical checkpoint for ensuring the quality of generative biology outputs, especially in novel binder design and other high-stakes applications.

What challenges does the Generative AI In Life Sciences Industry face during its growth?

- A primary challenge affecting industry growth involves data integrity hurdles and the inherent risk of algorithmic hallucination in high-stakes biological research.

- A primary challenge restraining market growth is the need for high-quality, curated training data and the immense difficulty in performing multi-omics data integration at scale. While generative chemistry and protein structure prediction show great promise, their reliability is contingent on robust bio-data repositories and phenomic datasets, which are often siloed.

- The risk of algorithmic hallucination necessitates strong algorithmic guardrails and high model interpretability, especially within regulated GxP workflows. This is compounded by data sovereignty concerns and the complexity of evolving regulatory compliance frameworks. Furthermore, a critical talent shortage persists, with industry reports indicating that 77% of life sciences firms struggle to hire professionals skilled in both AI and biology.

- This scarcity impedes the effective use of digital pathology and other clinical data platforms, slowing the transition to a fully functional data-liquid ecosystem.

Exclusive Technavio Analysis on Customer Landscape

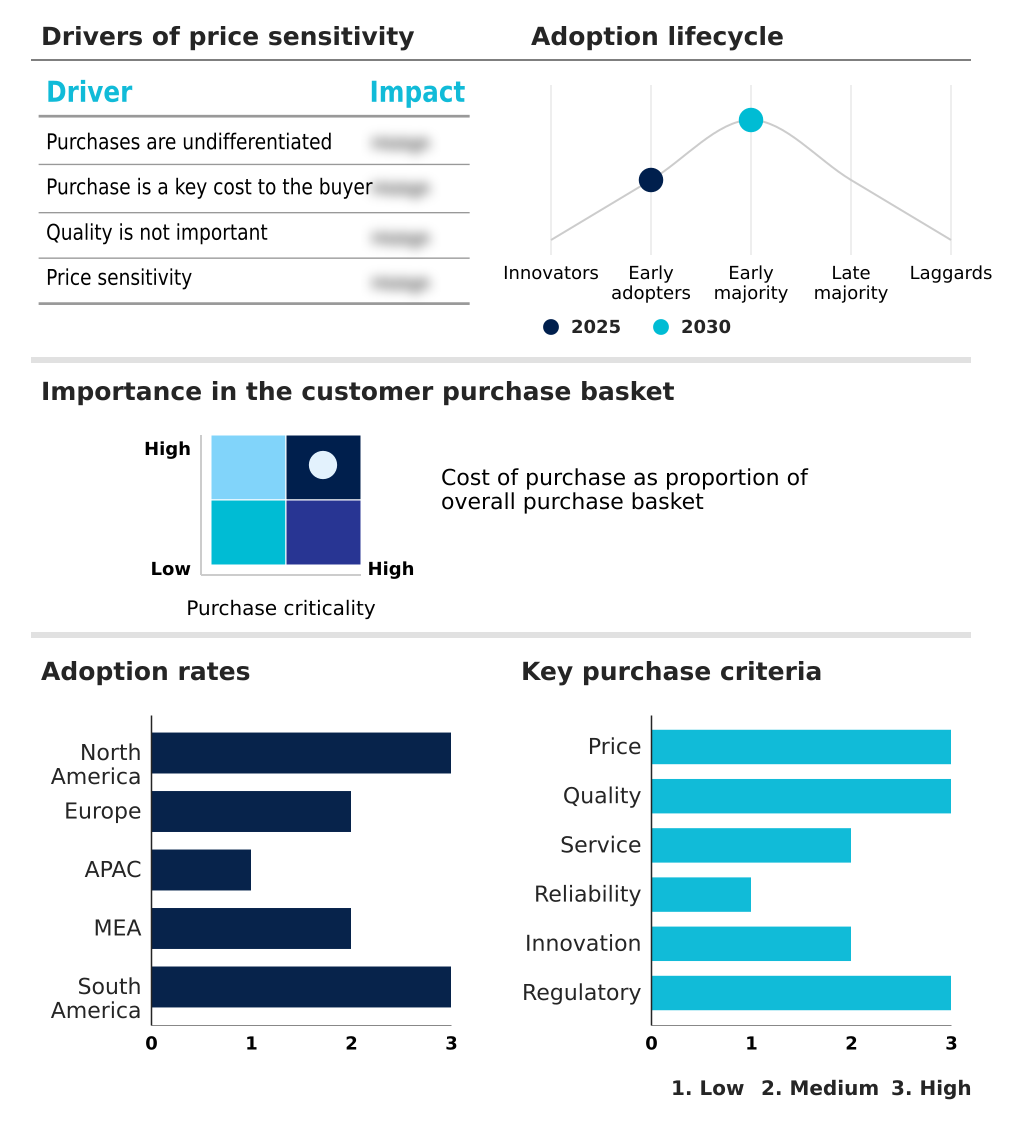

The generative ai in life sciences market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in life sciences market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Life Sciences Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in life sciences market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atomwise Inc. - Delivering AI-powered platforms that accelerate structure-based drug discovery by designing and screening novel molecules using advanced deep learning algorithms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atomwise Inc.

- BenchSci Analytics Inc.

- Deep Genomics Inc.

- Evogene Ltd.

- Iktos SA

- Indegene Ltd

- Insilico Medicine

- insitro

- IQVIA Holdings Inc.

- Isomorphic Labs

- NVIDIA Corp.

- Owkin Inc.

- PathAI Inc.

- Recursion Pharmaceuticals Inc.

- Schrodinger Inc.

- Tempus AI Inc.

- Valo Health

- Veeva Systems Inc.

- Verge Analytics Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in life sciences market

- In June, 2025, Pfizer expanded its strategic research collaboration with XtalPi to develop an advanced cloud-based molecular modeling platform designed to enhance predictive tools and throughput for small-molecule drug discovery.

- In November, 2025, Teva launched its Rise platform, a global open innovation initiative created to accelerate smart manufacturing solutions by leveraging a unified hybrid architecture to address production and supply chain challenges.

- In January, 2026, Anthropic introduced Claude for Healthcare, a specialized platform equipped with HIPAA-ready infrastructure and models specifically optimized for complex healthcare tasks, including the analysis of medical and genomic datasets.

- In March, 2026, Insilico Medicine announced a significant global research and development collaboration with Eli Lilly, utilizing its proprietary generative AI platform to expedite the discovery of therapeutic candidates across multiple disease areas.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Life Sciences Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.4% |

| Market growth 2026-2030 | USD 1725.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Israel, Saudi Arabia, UAE, South Africa, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in life sciences market is transitioning from theoretical modeling to industrial-scale application, fundamentally altering preclinical development. The focus is now on production-grade generative biology platforms capable of end-to-end therapeutic discovery, from target identification to binder design. Boardroom decisions increasingly involve balancing the high capital expenditure for in-house high-performance computing against the adoption of cloud-based molecular modeling.

- This is driven by data showing sixty-two percent of life sciences organizations prioritize generative AI for drug discovery. The technology enables advanced patient stratification, pharmacokinetics prediction, and streamlined hit-to-lead processes. The success of these systems relies on sophisticated machine learning operations and federated learning to leverage distributed bio-data repositories without compromising data security.

- As autonomous agentic workflows become standard, the ability to conduct molecular dynamics simulation and rapid lead optimization will define competitive positioning in the industry.

What are the Key Data Covered in this Generative AI In Life Sciences Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Life Sciences Market between 2026 and 2030?

-

USD 1.73 billion, at a CAGR of 25.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Drug discovery, Personalized medicine, and Clinical trials), Technology (Novel molecule generation, Protein sequence design, and Synthetic gene design), Deployment (Cloud-based, On-premises, and Hybrid) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Acceleration of De novo molecular design and therapeutic discovery, Data integrity hurdles and risk of algorithmic hallucination

-

-

Who are the major players in the Generative AI In Life Sciences Market?

-

Atomwise Inc., BenchSci Analytics Inc., Deep Genomics Inc., Evogene Ltd., Iktos SA, Indegene Ltd, Insilico Medicine, insitro, IQVIA Holdings Inc., Isomorphic Labs, NVIDIA Corp., Owkin Inc., PathAI Inc., Recursion Pharmaceuticals Inc., Schrodinger Inc., Tempus AI Inc., Valo Health, Veeva Systems Inc. and Verge Analytics Inc.

-

Market Research Insights

- The generative AI in life sciences market dynamics are shaped by a push for efficiency, where sixty-two percent of firms cite drug discovery as the primary use case, and a significant talent gap, with seventy-seven percent of employers struggling to find skilled professionals. This environment drives the adoption of multimodal architectures and biological foundation models to automate complex tasks.

- Success depends on leveraging large action models for automated hypothesis generation and knowledge graph construction to navigate complex data. Clinical decision support systems are being enhanced by AI-driven diagnostics, while the need for human-in-the-loop validation remains critical for regulatory acceptance and ensuring the reliability of digital biomarkers. The market's evolution is a balance between technological ambition and practical implementation challenges.

We can help! Our analysts can customize this generative ai in life sciences market research report to meet your requirements.

RIA -

RIA -