Helicopter Blades Market Size 2024-2028

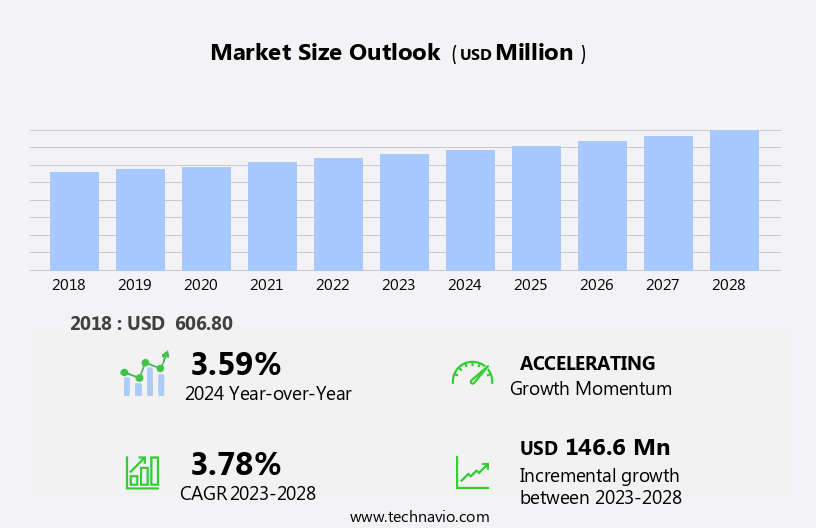

The helicopter blades market size is forecast to increase by USD 146.6 billion at a CAGR of 3.78% between 2023 and 2028.

- The market is witnessing significant growth due to the adoption of advanced composite materials in blade manufacturing. These materials offer superior strength, lightweight, and durability, making them an ideal choice for helicopter blade production. Another trend driving market growth is the development of 3D-printed soluble cores, which are used to create complex blade shapes with high precision and reduced production time. However, the market faces challenges such as the high cost of these advanced materials and the complexity of blade manufacturing processes. Additionally, the failure of helicopter blade systems due to fatigue and other factors poses a significant risk to safety and can lead to costly repairs and downtime for operators.

- Despite these challenges, the market is expected to continue growing due to the increasing demand for more efficient and reliable helicopter blade systems.

What will be the Size of the Helicopter Blades Market During the Forecast Period?

- The market encompasses the production and sale of rotor systems for both commercial and military helicopters, including those used in offshore traffic. Market dynamics are driven by advancements in technology, with a focus on lightweight materials, improved control systems, and increased efficiency to reduce carbon emissions. Three-dimensional (3D) printing is revolutionizing manufacturing processes, offering potential for customization and cost savings. Military applications prioritize durability, with rigorous testing and stringent material standards to ensure longevity and a competitive edge. Helicopter rotors and blades undergo extensive fatigue testing to ensure safety and reliability, with airborne testing providing real-world data for continuous improvement.

- Sikorsky, a leading helicopter manufacturer, is known for its Black Hawk helicopters, showcasing the industry's commitment to innovation and progress.

How is this Helicopter Blades Industry segmented and which is the largest segment?

The helicopter blades industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

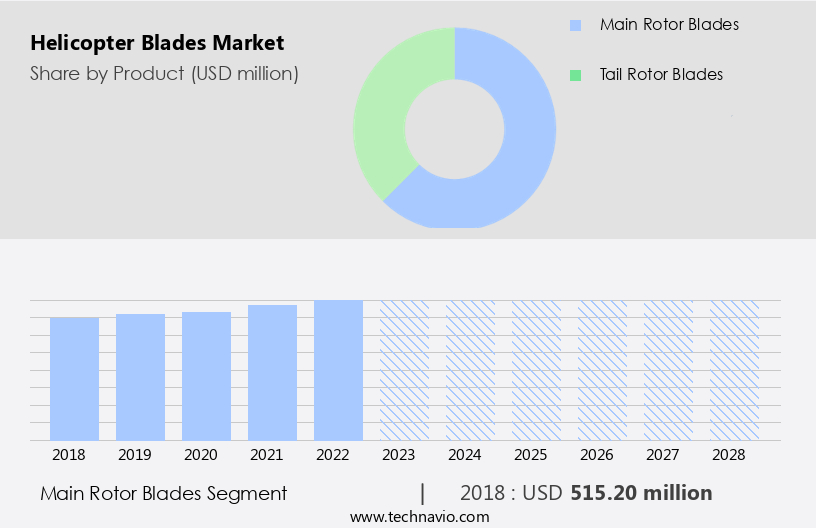

- Product

- Main rotor blades

- Tail rotor blades

- Geography

- North America

- Canada

- US

- Europe

- Germany

- France

- APAC

- China

- Middle East and Africa

- South America

- North America

By Product Insights

- The main rotor blades segment is estimated to witness significant growth during the forecast period.

The main rotor system in helicopters is a crucial component responsible for generating lift and enabling vertical takeoff and landing. Each blade In the system contributes equally to the lifting force, ensuring balance and even distribution. The main rotor system comprises the mast, hub, and blades. The mast, a hollow cylindrical metal shaft, connects to the gearbox. The hub attaches the rotor blades to the mast, while the blades generate lift. Classified as rigid, semirigid, or fully articulated, these systems differ based on the hub's attachment to the blades and rotor motion relative to the mast. Incorporating offshore helicopter traffic, commercial helicopters, and military helicopters, advancements in rotor systems include lightweight materials, improved control systems, and 3D printing technologies.

Sikorsky's Black Hawk helicopters, for instance, employ innovative blade systems with active blades and newer variants. These enhancements focus on efficiency, reducing carbon emissions, and improving performance during military, emergency medical services, and utility purposes. The integration of smart helicopter technologies, such as aerodynamic properties, blade flows, and flight travel, also minimizes vibrations, turbulence, and harshness, resulting in quieter operations. Manufacturing processes, including additive manufacturing technologies and rapid prototyping, provide a competitive edge through cost savings and faster production. Continuous testing and fatigue analysis ensure the durability and reliability of these systems, meeting the demands of defense budgets and diverse helicopter applications, such as attack, combat, and rescue operations.

Get a glance at the Helicopter Blades Industry report of share of various segments Request Free Sample

The Main rotor blades segment was valued at USD 515.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

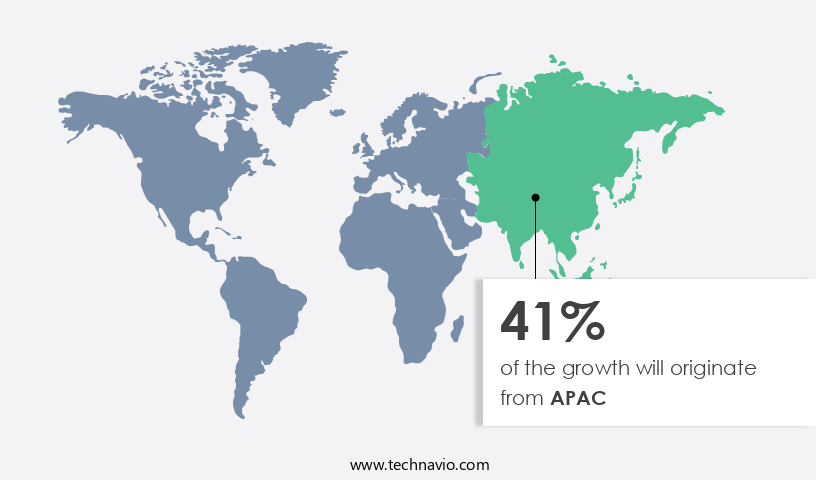

- APAC is estimated to contribute 41% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The growth of the helicopter blades market in the Asia-Pacific (APAC) region is expected to be significantly driven by the development of multi-functional rotorcraft. As rotorcraft technology advances, the introduction of helicopters that offer diverse capabilities such as improved performance, versatility, and adaptability for various missions will create increased demand for high-quality, innovative helicopter blades. These multi-functional rotorcraft are designed to meet a wide range of operational needs, from search and rescue to medical evacuation and cargo transport, making them highly valuable across different sectors. As a result, manufacturers and operators in the APAC region will seek advanced helicopter blades that enhance the performance and efficiency of these versatile rotorcraft. This trend towards multi-functional rotorcraft, coupled with the increasing investment in helicopter technology and infrastructure in APAC, will drive substantial growth in the helicopter blades market throughout the forecast period.

Market Dynamics

Our helicopter blades market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Helicopter Blades Industry?

Use of advanced composite materials in helicopter blades is notably driving the market growth. Helicopter blades encounter significant challenges in flight due to turbulence and harsh environmental conditions. These factors lead to noise generation and potential damage to the blades. To mitigate these issues, manufacturers focus on improving blade design and materials. Advanced composite materials and aerodynamic shapes are used to enhance blade durability and reduce noise levels.

Additionally, blade manufacturers continue to invest in research and development to create blades that can better withstand extreme weather conditions and minimize the impact of turbulence. These efforts aim to ensure optimal helicopter performance and passenger comfort. Thus, such factors are driving the growth of the market during the forecast period.

What are the market trends shaping the Helicopter Blades Industry?

Development of 3D-printed soluble cores is the key trend in the market. Helicopter blades encounter significant challenges in harsh operating environments, including turbulence and noise. These factors can negatively impact the performance and durability of helicopter blades. To mitigate these issues, manufacturers focus on designing blades with advanced materials and aerodynamic shapes. These innovations help improve blade efficiency, reduce noise levels, and enhance resistance to fatigue.

Despite these advancements, the development of quieter and more durable helicopter blades remains a priority for industry leaders to meet the evolving demands of the aviation sector. Thus, such trends will shape the growth of the market during the forecast period.

What challenges does the Helicopter Blades Industry face during its growth?

Failure of helicopter blade system is the major challenge that affects the growth of the market. Helicopter blades are a crucial component of helicopter design, enabling vertical takeoff and landing capabilities. However, operating in turbulent environments and enduring harsh conditions can lead to challenges. These include increased noise levels and potential damage from wind gusts and vibrations. To mitigate these issues, manufacturers focus on enhancing blade materials and aerodynamics. Advanced composites, such as carbon fiber-reinforced polymers, offer improved strength and flexibility.

Additionally, innovative blade designs reduce noise and improve efficiency. These advancements are expected to drive the helicopter blades market in the coming years. Despite these advancements, continued research and development efforts are necessary to further minimize the impact of turbulence and noise on helicopter operations. Hence, the above factors will impede the growth of the market during the forecast period

Exclusive Customer Landscape

The helicopter blades market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the helicopter blades market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, helicopter blades market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Airbus SE - Our company specializes In the production of helicopter blades for both civil and military applications. We are committed to delivering high-performance, reliable, and innovative blade solutions to meet the unique requirements of our clients. Our expertise spans from design and development to manufacturing, ensuring a comprehensive approach to meeting the needs of the helicopter industry In the US market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Bell Textron Inc.

- Carson Helicopters Inc.

- Ducommun Inc.

- Eagle Aviation Technologies LLC

- Erickson Inc.

- Helicopter Technology Co.

- Hindustan Aeronautics Ltd.

- Karman Space & Defense

- Lisi Aerospace SAS

- Lockheed Martin Corp.

- Melrose Industries Plc

- Robinson Aerospace Systems PTY LTD

- Textron Inc.

- The Boeing Co.

- Van Horn Aviation LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a vital segment of the aerospace industry, supplying rotor components for both commercial and military applications. Helicopter blades are essential for generating lift and thrust, enabling these aircraft to perform various functions, including offshore traffic transport, emergency medical services, military operations, and utility purposes. The market is witnessing significant advancements, driven by the integration of technologies and the pursuit of lightweight materials to enhance efficiency and reduce carbon emissions. Traditional manufacturing processes are being supplemented with 3D printing and additive manufacturing technologies, offering a competitive edge through rapid prototyping and customization. Helicopter rotor systems are subjected to rigorous testing to ensure their durability and performance under extreme conditions.

Fatigue testing is a crucial aspect of the development process, assessing the material's ability to withstand the cyclic loading experienced during flight. Airborne testing is employed to evaluate blade flows, vibrations, turbulence, and harshness in real-world environments. Military helicopters, such as those used for attack, combat, and rescue operations, require robust blade systems capable of enduring harsh conditions. Innovative blade systems, including active blades and newer variants with multiple rotors, are being developed to improve aerodynamic properties and optimize blade flows for enhanced flight travel and reduced noise. The defense budget remains a significant driver for the market, as military applications continue to demand high-performance, reliable rotor components.

However, the market is also experiencing diversification, with commercial applications in utility and emergency medical services growing in importance. The pursuit of lighter, more efficient materials and the integration of smart helicopter technologies are key trends shaping the market. Carbon fiber composites are increasingly being used due to their high strength-to-weight ratio and resistance to fatigue. Additionally, active blade systems and smart technologies are being integrated to improve control and reduce maintenance requirements. In conclusion, the market is undergoing significant transformation, driven by advancements in materials, manufacturing processes, and the integration of technologies. These developments are aimed at enhancing efficiency, reducing carbon emissions, and improving performance, making helicopters a vital component of various industries, including military and commercial applications.

|

Helicopter Blades Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.78% |

|

Market growth 2024-2028 |

USD 146.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.59 |

|

Key countries |

US, China, France, Germany, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Helicopter Blades Market Research and Growth Report?

- CAGR of the Helicopter Blades industry during the forecast period

- Detailed information on factors that will drive the Helicopter Blades growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the helicopter blades market growth of industry companies

We can help! Our analysts can customize this helicopter blades market research report to meet your requirements.

RIA -

RIA -