HVAC Air Ducts Market Size 2024-2028

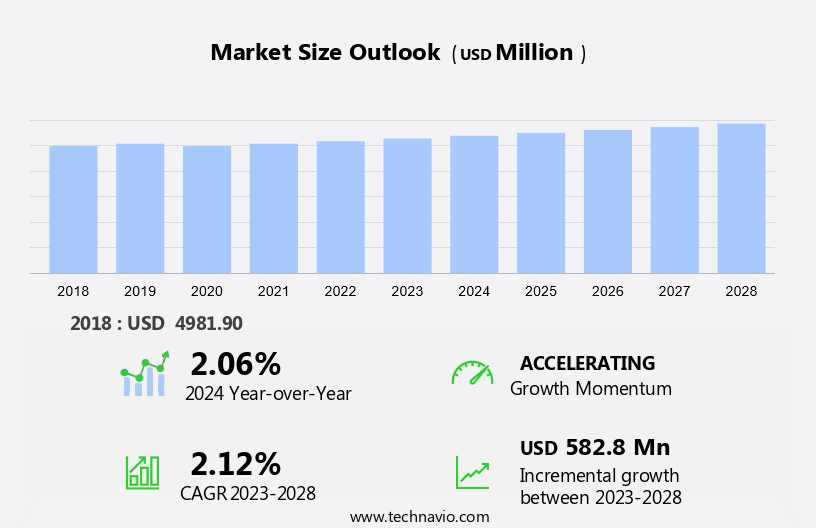

The HVAC air ducts market size is forecast to increase by USD 582.8 million at a CAGR of 2.12% between 2023 and 2028.

- The HVAC air duct market is experiencing significant growth due to several key trends and challenges. Stringent energy consumption and environmental regulations are driving the market, as there is a growing emphasis on energy efficiency and reducing carbon emissions. The demand for energy-efficient and sustainable indoor comfort solutions drives market growth, with a focus on green building technology and the integration of advanced materials like aluminum, polymers, and fiberglass in ductwork manufacturing. Innovative sealing solutions are being adopted to prevent HVAC air duct leakages, which can lead to significant energy loss and decreased indoor air quality. However, the lack of a skilled workforce poses a challenge to the market, as proper installation and maintenance of HVAC air ducts require specialized knowledge and expertise. These factors, among others, are shaping the future of the HVAC air duct market.

What will be the Size of the HVAC Air Ducts Market During the Forecast Period?

- The market encompasses the production and supply of ductwork systems used in building infrastructure for distributing conditioned air from HVAC units, such as furnaces, air conditioners, heat pumps, and geothermal systems. This market caters to various sectors, including residential and commercial buildings, data centers, and industrial applications. The construction sector continues to be a significant contributor to market expansion, with architects increasingly incorporating HVAC air ducts into designs for optimal indoor environmental quality.

- Market size is anticipated to grow steadily, driven by the increasing need for efficient and reliable HVAC systems in various industries, including manufacturing, semiconductor & electronics, oil & gas, and others. Market trends include the development of innovative ductwork components, such as stack boots & heads, turning vanes, terminal units, plenums, and air terminals, to enhance system performance and reduce energy consumption.

How is this HVAC Air Ducts Industry segmented and which is the largest segment?

The HVAC air ducts industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

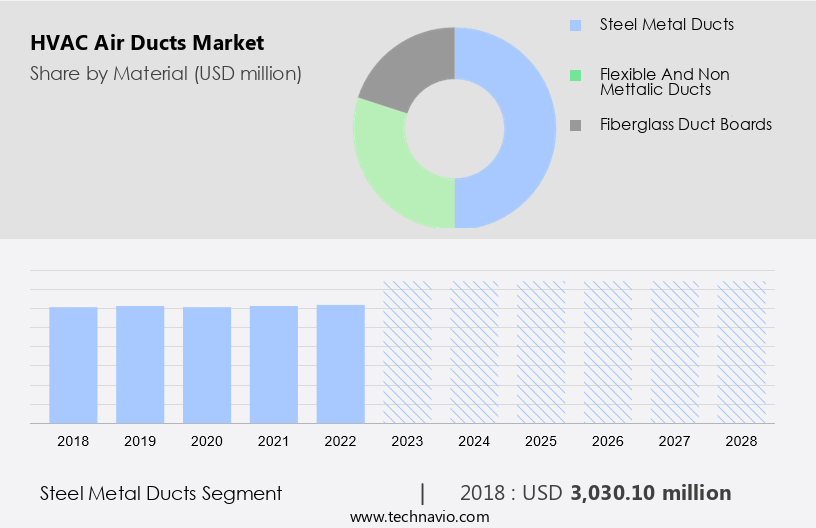

- Material

- Steel metal ducts

- Flexible and Non mettalic ducts

- Fiberglass duct boards

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

By Material Insights

- The steel metal ducts segment is estimated to witness significant growth during the forecast period.

HVAC air ducts are an essential component of conditioned air distribution systems in residential and commercial buildings. Sheet metal ducts, constructed from galvanized steel or aluminum, are the most commonly used type due to their durability and versatility. These ducts are available in various shapes, including round, rectangular, and spiral oval, and offer high air leakage standards and lower noise levels. In the metal sheet segment, galvanized mild steel ductwork dominates due to its rust resistance and elimination of painting costs. Energy efficiency and indoor air quality are crucial factors driving the demand for HVAC systems and air ducts in building renovations, retrofits, and new construction projects.

Regulatory standards and codes, such as ASHRAE and ENERGY STAR, influence the design and implementation of HVAC systems and air ducts. Green building practices, including the use of eco-friendly materials and smart technologies like IoT and HVAC technology, are also increasing in popularity. Other types of air ducts include fiberglass ducts, flexible non-metallic ducts, and fiberglass-reinforced panels. Applications span various industries, including office buildings, shopping malls, hospitals, hotels, restaurants, and real estate projects.

Get a glance at the HVAC Air Ducts Industry report of share of various segments Request Free Sample

The steel metal ducts segment was valued at USD 3.03 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

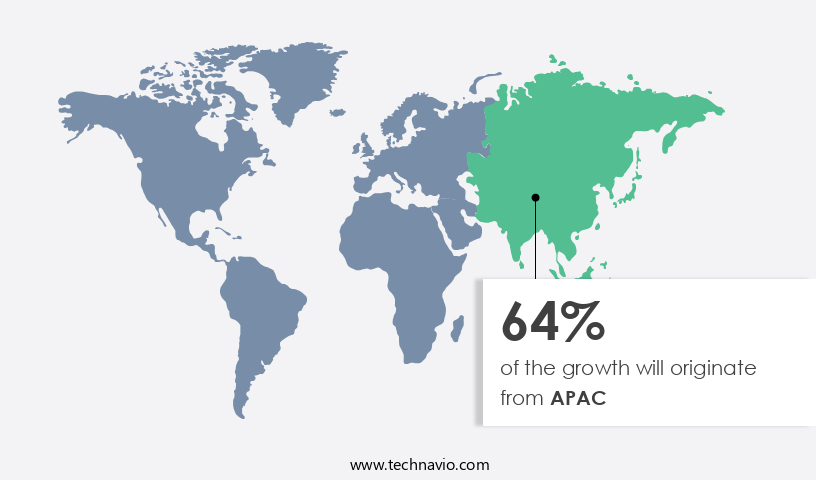

- APAC is estimated to contribute 64% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in APAC is projected to expand moderately over the forecast period, fueled by increasing investments In the real estate sector. The real estate industry's growth is driven by substantial investments in urban development, particularly in Tier 1 and Tier 2 cities, where infrastructure development is prioritized, notably In the residential sector. With approximately 200 million people expected to move to urban areas In the next decade, urbanization and infrastructure development will significantly contribute to the growth of the market in APAC. This market expansion is essential for providing conditioned air in buildings, including offices, shopping malls, hospitals, hotels, restaurants, and various other commercial and industrial structures.

Renovation and retrofit projects, driven by regulatory standards, codes, and energy efficiency concerns, will further boost market growth. The use of eco-friendly materials, smart technologies, and IoT in HVAC systems, such as sheet metal ducts, flexible non-metallic ducts, fiberglass ducts, and high-efficiency equipment, will cater to the demand for improved indoor comfort, energy efficiency, and indoor air quality.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of HVAC Air Ducts Industry?

Stringent energy consumption and environmental regulations is the key driver of the market.

- The market is experiencing significant growth due to increasing demand for energy-efficient and eco-friendly building solutions. Strict environmental regulations, such as those set by the EU to reduce greenhouse gas emissions, are driving the adoption of advanced HVAC systems. Approximately 45% of buildings in Europe were constructed between 1960 and 1990, and the need to upgrade outdated HVAC systems to meet new regulations is creating opportunities for market growth. Indoor comfort solutions, including HVAC units, furnaces, air conditioners, and heat pumps, are essential for both residential and commercial buildings. Renovations and retrofits of existing structures are a significant market for HVAC air ducts.

- Energy efficiency and indoor air quality are key considerations for consumers and businesses, leading to the use of innovative technologies such as smart HVAC systems, IoT, and green building practices. Eco-friendly materials like sheet metal ducts, flexible non-metallic ducts, fiberglass ducts, and fiberglass-reinforced panels are gaining popularity due to their energy efficiency and reduced environmental impact. Industrial construction projects, office buildings, shopping malls, hospitals, hotels, restaurants, and real estate industry renovation and retrofit projects are major consumers of HVAC air ducts. Government regulations and codes play a significant role In the market, driving demand for energy-efficient systems and compliance with indoor air quality standards.

- Incentives for energy-efficient HVAC systems and consumer trust in brand recognition and innovative designs are also market growth factors. Market dynamics include the use of high-efficiency equipment, data center cooling, mission-critical applications, and specialized applications. Green building technology, such as geothermal heat pumps and insulation, is also driving market growth. Materials like aluminum, polymers, and fiberglass are used In the production of HVAC air ducts. In summary, the market is growing due to increased environmental concerns, strict regulations, and consumer demand for energy-efficient and eco-friendly solutions. Technological advancements, innovative designs, and smart features are key market trends.

What are the market trends shaping the HVAC Air Ducts Industry?

Innovative sealing solutions to prevent HVAC air duct leakages is the upcoming market trend.

- HVAC air duct leaks are a significant issue in both residential and commercial buildings In the US, leading to energy losses, indoor air quality (IAQ) concerns, and building code violations. According to various studies, including those conducted by the US Department of Energy (DOE), the Environment Protection Agency (EPA), and the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE), an average of 30% of conditioned air escapes from duct systems due to leaks. This results in increased energy consumption for ventilation systems, which must compensate for the inefficiencies. A staggering 80% of US buildings experience duct leakage of 20-40% or more, leading to health risks, energy wastage, and potential regulatory issues.

- Building owners and managers can address this problem through various methods, including energy-efficient HVAC systems, incentives, and innovative designs utilizing smart technologies, IoT, eco-friendly materials, and advanced insulation and sealing methods. The real estate industry, including office buildings, shopping malls, hospitals, hotels, restaurants, and more, can benefit significantly from implementing these solutions to improve indoor comfort, energy efficiency, and consumer trust.

What challenges does the HVAC Air Ducts Industry face during its growth?

Lack of skilled workforce is a key challenge affecting the industry growth.

- The market is experiencing significant technological advancements, driving the demand for upgrades in building systems. End-users, including those in residential and commercial sectors, are increasingly retrofitting their existing HVAC systems instead of replacing them entirely. This approach incurs lower costs and allows the integration of innovative technologies, such as energy efficiency, indoor air quality enhancements, and smart features. The HVAC industry is responding with eco-friendly materials, IoT integration, and smart technologies. Regulatory standards and codes play a crucial role in construction projects, pushing the market towards energy-efficient HVAC systems and green building practices. Market competition is leading to continuous innovation, with new designs, insulation methods, and sealing techniques.

- The market caters to various applications, including office buildings, shopping malls, hospitals, hotels, restaurants, and industrial construction. Key players focus on brand recognition, consumer trust, and loyalty, offering bespoke air-handling equipment and high-efficiency equipment for data center cooling, mission-critical applications, and specialized applications.

Exclusive Customer Landscape

The HVAC air ducts market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the HVAC air ducts market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, HVAC air ducts market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Airmake Cooling Systems - The HVAC (Heating, Ventilation, and Air Conditioning) industry encompasses various duct systems, including manual duct systems. These systems facilitate the distribution of conditioned air throughout buildings, ensuring thermal comfort and indoor air quality. Manual duct systems, a type of HVAC ductwork, allow for manual adjustments to temperature and airflow, offering flexibility for occupants. This duct system category caters to diverse applications, contributing significantly to the HVAC market's growth and innovation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airmake Cooling Systems

- Airtrace Sheet Metal Ltd.

- Alan Manufacturing Inc.

- CMS Group of Companies

- DuctSox Corp.

- FabricAir AS

- Imperial Manufacturing Group

- KAD Airconditioning LLC

- Lindab AB

- M and M Manufacturing Co.

- Masterduct Inc.

- Naudens Sheet Metal Manufacturers

- Saudi Akhwan Ducting Factory Co. Ltd.

- SFP Ltd.

- Texas Duct Systems LLC

- Thermaflex

- TurnKey Duct Systems

- VK Steel

- Waves Aircon Pvt. Ltd.

- ZEN Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market plays a significant role In the building sector, as conditioned air distribution systems are essential for indoor comfort in both residential and commercial buildings. These systems, which include HVAC units, furnaces, air conditioners, and heat pumps, are integral to maintaining optimal indoor environments for occupants. The demand for HVAC air ducts is driven by the construction and renovation of buildings, as well as retrofitting existing structures to improve energy efficiency and indoor air quality. In the context of the building industry, HVAC air ducts are utilized in various types of structures, ranging from office buildings and shopping malls to hospitals, hotels, and restaurants. Renovation and retrofit projects are particularly important for the market, as they provide opportunities to upgrade existing systems with more energy-efficient and eco-friendly technologies. Regulatory standards and codes play a crucial role In these projects, ensuring that new installations meet stringent requirements for energy efficiency and indoor air quality.

Construction projects in various industries, including industrial construction, green building practices, and the real estate industry, also contribute to the demand for HVAC air ducts. In the realm of green building technology, there is a growing trend towards the use of eco-friendly materials, such as fiberglass ducts, and smart technologies, such as IoT and smart features, to enhance energy efficiency and indoor air quality. The market is diverse, encompassing a range of materials, including sheet metal ducts, flexible non-metallic ducts, fiberglass ducts, galvanized steel, aluminum, flexible plastic, foil, fiberglass-reinforced panels, and more. The choice of material depends on various factors, such as cost, durability, and insulation properties. The applications for HVAC air ducts are vast and varied, from office buildings and shopping malls to hospitals, hotels, restaurants, and more. In the case of mission-critical applications, such as data centers and laboratories, high-efficiency equipment and specialized applications, such as geothermal heat pumps and vibration isolators, are often employed to ensure optimal performance and reliability.

Thus, the market is influenced by several factors, including regulatory standards, consumer trends, and technological advancements. Energy efficiency and indoor air quality are key considerations for building owners and operators, leading to the adoption of energy-efficient HVAC systems and innovative designs. Brand recognition and consumer trust are also important factors In the market. Consumers and businesses seek reliable and high-quality products, leading to a focus on bespoke air-handling equipment and smart features. Rapid transportation infrastructure, such as airports and multiplexes, also require specialized HVAC solutions to maintain optimal indoor conditions for large numbers of occupants. Thus, the market is a dynamic and diverse sector that plays a crucial role In the building industry. Driven by factors such as energy efficiency, indoor air quality, and regulatory standards, the market is constantly evolving to meet the changing needs of various industries and applications. From residential and commercial buildings to industrial and specialized applications, HVAC air ducts are an essential component of modern indoor environments.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

144 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.12% |

|

Market growth 2024-2028 |

USD 582.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.06 |

|

Key countries |

China, US, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this HVAC Air Ducts Market Research and Growth Report?

- CAGR of the HVAC Air Ducts industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the HVAC air ducts market growth of industry companies

We can help! Our analysts can customize this HVAC air ducts market research report to meet your requirements.

RIA -

RIA -