Hydrocolloid Dressing Market Size 2024-2028

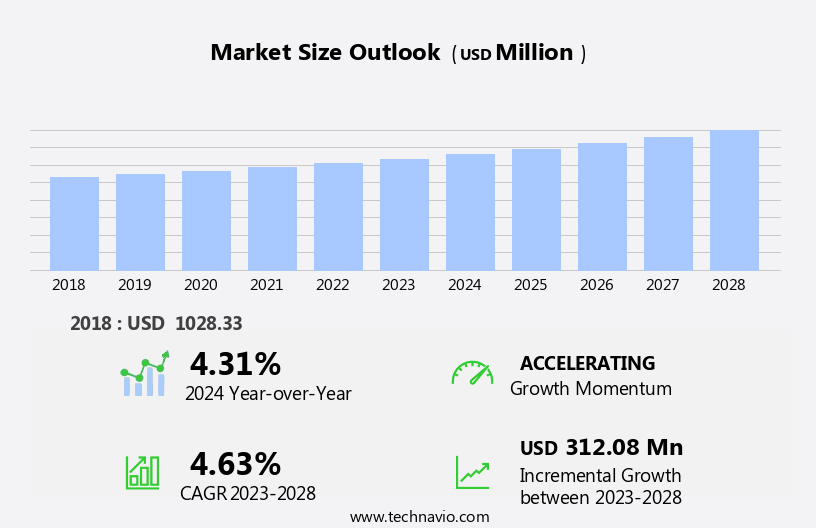

The hydrocolloid dressing market size is forecast to increase by USD 312.08 million at a CAGR of 4.63% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing incidence and prevalence of acute and chronic wounds worldwide. According to the World Health Organization, an estimated 6.5 million people require wound care each year, creating a substantial demand for advanced wound healing solutions. Hydrocolloid dressings, known for their ability to absorb exudate and maintain a moist wound healing environment, are gaining popularity in the healthcare industry. Moreover, the emergence of nanoparticles in hydrocolloid wound dressings is a notable trend in the market. These advanced dressings offer enhanced properties, such as improved adhesion, better moisture retention, and increased biocompatibility, making them an attractive option for healthcare professionals and patients alike.

- However, the market is not without challenges. Inherent issues, such as the risk of skin irritation, potential for dressing detachment, and the need for frequent dressing changes, can impact patient compliance and overall market growth. Companies seeking to capitalize on market opportunities and navigate challenges effectively must focus on addressing these issues through product innovation and improved patient education.

What will be the Size of the Hydrocolloid Dressing Market during the forecast period?

- The market encompasses a range of advanced wound care solutions designed to promote healing in various types of wounds, including miscellaneous burns, venous leg ulcers, pressure injuries, and acute wounds. These dressings employ hydrocolloid technology, which facilitates autolytic debridement and maintains a moist wound environment, enhancing the body's natural healing process. Hydrocolloid dressings are applicable to diverse wound categories, such as thermal burns, electrical burns, and trauma-induced injuries. The market's growth is driven by the increasing prevalence of chronic wounds, particularly in populations with diabetes and the aging demographic. Furthermore, the rising number of surgical procedures and road traffic crashes contribute to the market expansion.

- Advanced wound care products, such as nonwoven hydrocolloid dressings and polyurethane films, are gaining popularity due to their ability to manage exudate and provide a protective barrier against bacterial infections. E-sources like eBMEDICINE and NCBI provide valuable insights into the latest research and developments in hydrocolloid dressing technology. Overall, the market is poised for continued growth, addressing the unmet needs of healthcare providers and patients alike.

How is this Hydrocolloid Dressing Industry segmented?

The hydrocolloid dressing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Chronic wound

- Acute wound

- End-user

- Hospitals

- Clinics

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

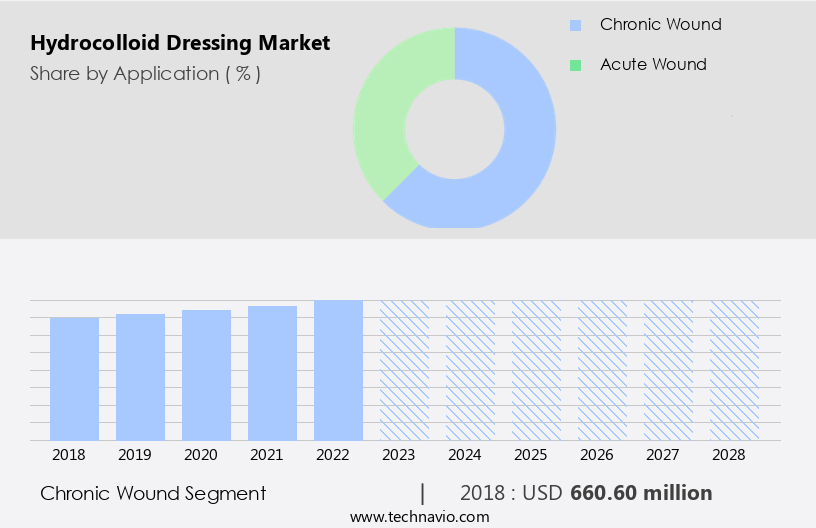

The chronic wound segment is estimated to witness significant growth during the forecast period.

The market is driven by the significant demand for advanced wound care solutions, particularly for chronic wounds. According to , the chronic wound segment is expected to dominate the market due to the increasing global prevalence of chronic wounds, such as ulcers, traumatic wounds, and surgical wounds. Approximately 6.7 million people currently live with chronic wounds, and this number is projected to grow by more than two percent in the next decade. Moreover, both surgical incisions and traumatic wounds caused by accidents account for over 150 million cases annually, with road traffic accidents contributing to a rising number of injuries.

Advanced wound care products, including hydrocolloid dressings, are essential for managing various types of wounds, such as SSIs (Surgical Site Infections), thermal burns, diabetic foot ulcers, and pressure injuries. Hydrocolloid dressings offer advantages like skin barrier protection, moisture retention, and autolytic debridement, making them an ideal choice for wound treatment. Additionally, they are suitable for various applications, including acute wounds, chronic wounds, and traumatic wounds. Absorbent dressings, transparent dressings, adhesive dressings, and hydrogel dressings are some popular types of hydrocolloid dressings. These dressings cater to diverse wound care needs, such as managing blood loss, providing thermal burn protection, and promoting skin healing solutions.

In the healthcare supplies industry, companies like Smith & Nephew offer a wide range of hydrocolloid dressings for hospitals, home healthcare, and independent diabetes care. The market for hydrocolloid dressing materials also includes nonwovens, polyurethane films, and medical tape. These materials contribute to the production of various wound care products, including surgical wound care, ostomy care products, and pressure ulcer management solutions. Furthermore, hydrocolloid dressings are effective in treating miscellaneous burns, such as chemical burns and electric burns, making them an essential component of burn care. In summary, the market is expected to grow significantly due to the increasing demand for advanced wound care solutions for chronic and acute wounds, as well as trauma injuries.

The market caters to various wound types, including SSIs, thermal burns, diabetic foot ulcers, and pressure injuries, using materials like nonwovens, polyurethane films, and medical tape. The market is driven by the rising global prevalence of chronic wounds and the growing number of surgical and traumatic wounds.

Get a glance at the market report of share of various segments Request Free Sample

The Chronic wound segment was valued at USD 660.60 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

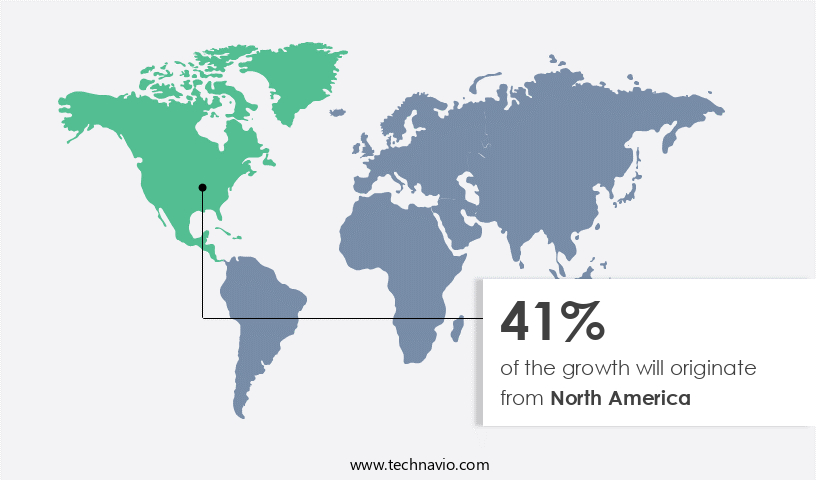

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in North America is experiencing significant growth due to the rising prevalence of acute and chronic wounds, particularly among the geriatric population. Advanced wound care treatments, such as hydrocolloid and hydrogel dressings, are increasingly being adopted to promote skin barrier protection and skin healing solutions for various types of wounds, including SSIs, thermal burns, diabetic foot ulcers, and pressure injuries. The use of hydrocolloid dressings facilitates autolytic debridement and moist wound healing, making them an effective option for chronic wound management. Major revenue contributors to the North American the market include hospitals, home healthcare, and independent diabetes care.

Leading companies, such as Smith & Nephew, offer a wide range of hydrocolloid dressing products for different wound types and sizes. The increasing adoption of advanced wound care technologies, such as transparent dressings, medical tape, and absorbent dressings, is further driving market growth. Moreover, the growing awareness of advanced wound care treatments and the availability of various wound dressing materials, including nonwovens and polyurethane films, are expected to provide significant opportunities for market expansion. The market in North America is expected to witness substantial growth during the forecast period, primarily due to the increasing number of surgical procedures, road traffic crashes, and ICU admissions resulting in acute and chronic wounds.

Additionally, the rising prevalence of severe burn injuries and the availability of advanced wound care products, such as electric burn dressings and miscellaneous burn dressings, are further expected to fuel market growth. Overall, the market in North America is poised for expansion due to the increasing demand for effective wound care solutions and the strong presence of leading companies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Hydrocolloid Dressing Industry?

- Increasing incidence and prevalence of acute and chronic wounds is the key driver of the market.

- The rising prevalence of chronic and acute wounds, including diabetic foot ulcers, venous ulcers, pressure ulcers, burns, and traumatic ulcers, is driving the demand for hydrocolloid dressings. Diabetes, a global health concern, is a significant contributor to the increasing incidence of diabetic foot ulcers. Diabetic patients, due to poor blood circulation and neuropathy, are prone to developing blisters that can easily progress into ulcers, increasing the risk of infection. With the growing number of diabetic patients worldwide, the demand for hydrocolloid dressings is anticipated to rise.

- These dressings provide an ideal environment for wound healing by maintaining a moist environment, promoting granulation, and preventing infection. The market for hydrocolloid dressings is expected to experience steady growth due to the increasing burden of chronic and acute wounds.

What are the market trends shaping the Hydrocolloid Dressing Industry?

- Emergence of nanoparticles to treat wounds is the upcoming market trend.

- Wound treatment is a critical field of research due to the skin's essential physiological and aesthetic functions. In recent years, nanoparticles have emerged as promising platforms for treating both acute and chronic wounds. Copper, silver, gold titanium, and zinc oxide nanoparticles have demonstrated therapeutic effects on wound healing. The unique properties of nanoparticles, such as solid lipid nanoparticles, nanocapsules, polymersomes, and polymeric nanocomplexes, make them excellent vehicles for enhancing the efficacy of drugs used in wound healing.

- By incorporating nanoparticles into various pharmaceutical materials, the beneficial properties of formulations can be amplified, and better dose control can be achieved. These advancements offer significant potential for improving wound care treatments.

What challenges does the Hydrocolloid Dressing Industry face during its growth?

- Inherent challenges associated with hydrocolloid wound dressings is a key challenge affecting the industry growth.

- Hydrocolloid dressings are a popular choice in modern wound care due to their ability to maintain a moist environment and promote healing. These interactive dressings are widely used for various types of wounds, excluding neuropathic ulcers and highly exudative wounds. However, their use comes with certain complications and limitations. One such limitation is the potential for tissue damage in areas prone to friction. Additionally, hydrocolloid dressings can accumulate exudate, leading to maceration and bacterial proliferation, resulting in a foul smell.

- Despite these challenges, hydrocolloid dressings remain a significant option in wound care, offering benefits such as maintaining an optimal moisture balance and protecting the wound from external factors. It is essential for healthcare professionals to consider the specific needs of each patient and the type of wound before selecting a dressing to ensure optimal healing and minimize potential complications.

Exclusive Customer Landscape

The hydrocolloid dressing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hydrocolloid dressing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, hydrocolloid dressing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Hydrocolloid dressings, including 3M Tegaderm, deliver a superior moisture vapor transmission rate, thereby minimizing the risk of shear and friction. These advanced wound coverings optimize healing environments by maintaining a moist wound condition while preventing maceration. The consistent transmission of moisture vapor facilitates the exchange of gases and promotes a healthy wound microclimate. By reducing friction and shear forces, hydrocolloid dressings protect the delicate tissue from damage, ultimately enhancing the overall effectiveness of the wound care treatment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- AMERX Health Care Corp.

- B.Braun SE

- Cardinal Health Inc.

- ConvaTec Group Plc

- Covalon Technologies Ltd.

- DermaRite Industries LLC

- Essity AB

- Hollister Inc.

- Integra Lifesciences Corp.

- Johnson and Johnson

- Lohmann and Rauscher GmbH and Co. KG

- McKesson Corp.

- Medline Industries LP

- Medtronic Plc

- Molnlycke Health Care AB

- Paul Hartmann AG

- Roosin Medical Co. LtdÂ

- Smith and Nephew plc

- Coloplast AS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a broad range of advanced wound care solutions, with hydrocolloids being a prominent type. These dressings are characterized by their ability to absorb exudate and maintain a moist wound environment, promoting autolytic debridement and enhancing the healing process. Hydrocolloid dressings are particularly effective in managing various types of wounds, including those in the geriatric population, diabetic foot ulcers, and thermal burns. Advanced dressings, including hydrocolloids, have gained significant traction in healthcare settings due to their superior capabilities compared to traditional absorbent dressings. Hospitals and home healthcare providers increasingly rely on these advanced wound care solutions for acute and chronic wound treatment.

Surgical wound care and pressure ulcer management are among the primary applications for hydrocolloid dressings. The market caters to diverse wound types, such as miscellaneous burns, electrical burns, and road traffic crash injuries. These dressings offer skin barrier protection and facilitate skin healing solutions, making them essential in Intensive Care Unit (ICU) settings for severe burn injuries. Hydrocolloid dressings are available in various forms, including transparent options, which enable continuous monitoring of the wound healing process. Adhesive dressings, medical tape, and polyurethane films are alternative wound dressing materials used in conjunction with hydrocolloids for optimal wound management. The market for hydrocolloid dressings is driven by the increasing prevalence of chronic wounds and the growing need for effective wound care solutions.

The aging population and the rising incidence of diabetes contribute significantly to the demand for advanced wound care products. The market is expected to grow steadily due to ongoing research and development efforts aimed at improving the efficacy and functionality of hydrocolloid dressings. Healthcare suppliers offer a wide range of hydrocolloid dressing products to cater to diverse wound care needs. Smith & Nephew, for instance, is a leading player in the market, providing innovative wound care solutions. Other market participants focus on niche applications, such as ostomy care products and surgical procedures. In summary, the market represents a dynamic and growing segment of the advanced wound care industry.

These dressings offer numerous benefits, including exudate management, skin barrier protection, and enhanced wound healing. The market is driven by the increasing prevalence of chronic wounds and the aging population, with ongoing research and development efforts contributing to its growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.63% |

|

Market growth 2024-2028 |

USD 312.08 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.31 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Hydrocolloid Dressing Market Research and Growth Report?

- CAGR of the Hydrocolloid Dressing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the hydrocolloid dressing market growth of industry companies

We can help! Our analysts can customize this hydrocolloid dressing market research report to meet your requirements.

RIA -

RIA -