Hydrogen Fuel Market 2024-2028

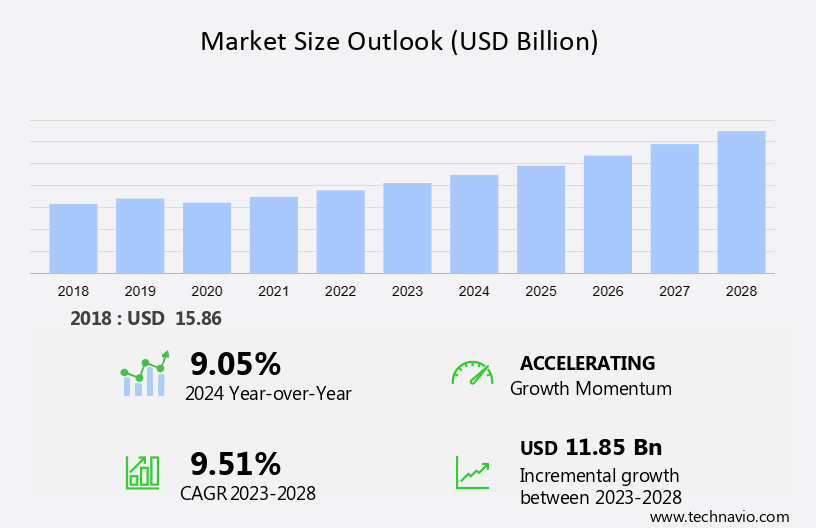

The hydrogen fuel market size is forecast to increase by USD 11.85 billion and is estimated to grow at a CAGR of 9.51% between 2023 and 2028. The report includes historic market data from 2018-2022. The market is experiencing a significant rise in demand for green hydrogen, driven by the global push towards sustainability and renewable energy sources. Alongside this, there's an increasing focus on low-carbon and blue hydrogen, as industries look for cleaner alternatives to traditional fossil fuels. These developments are further complemented by the emergence of power-to-X technologies, which convert surplus renewable energy into other forms of energy carriers like hydrogen, fuels, and chemicals. Together, these trends are shaping a more sustainable future for energy production and consumption, marking a pivotal shift in the global energy landscape

Hydrogen Fuel Market Overview :

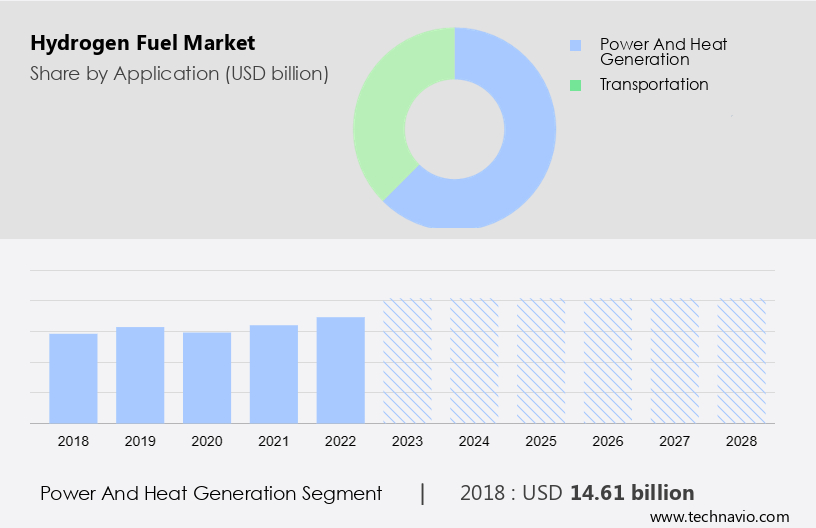

- The market segmentation by Application is categorized as power and heat generation and transportation

- The market segmentation by Source categorized as grey, green, and blue

- Power and heat generation is the fastest-growing segment during the forecast year

- The power and heat generation was the largest segment and was valued at USD 14.61 billion in 2018

- The Regional Analysis consists of APAC, Europe, North America, Middle East and Africa, and South America

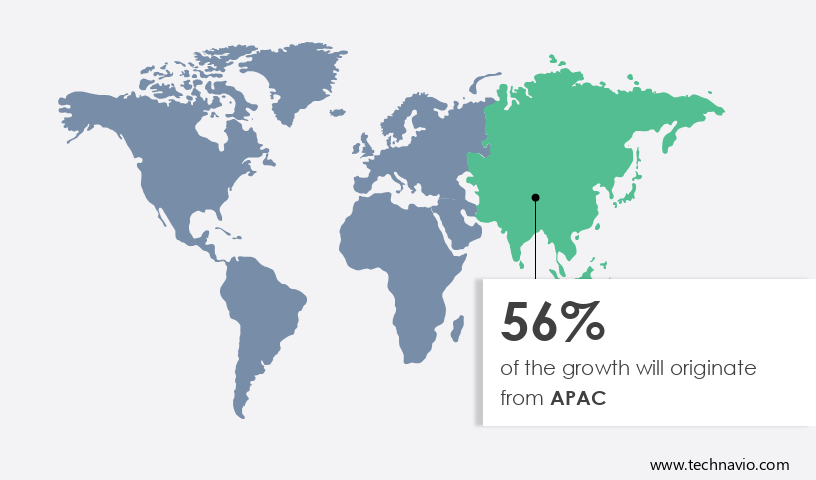

- APAC is is most dominating region during the forecast period

- It also includes an in-depth analysis of advancements in hydrogen technologies, growing interest in green hydrogen, and concerns associated with hydrogen purity and quality.

Download Free Sample in a Minute

The Hydrogen Fuel Market is rapidly evolving, driven by the demand for sustainable and energy-efficient technologies and the global push for energy transition towards climate-neutral targets. Clean hydrogen hubs are emerging, focusing on reducing carbon footprints through green hydrogen plants and innovations like steam methane reforming and coal gasification. The market is also seeing growth in methanol and ammonia manufacturing, vital for sectors like chemical and refineries. As electricity demand rises, hydrogen refueling stations and hydrogen transport systems are expanding, supported by governments and their net-zero CO2 emissions and zero-energy buliding initiatives. The shift to low-carbon hydrogen and green hydrogen strategy underpins the development of hydrogen-based economies, aiming to reduce GHG emissions and drive decarbonization.

Hydrogen Fuel Market Trends

Growing interest in green hydrogen is an emerging trend shaping the market growth. Green hydrogen is produced using renewable energy sources, making it a carbon-free and environmentally sustainable energy carrier. Increasing awareness of climate change and the need for decarbonization drive the interest in green hydrogen as a clean alternative. Further, industries with high hydrogen demand seek sustainable alternatives to support their supply chains and meet environmental goals. Hydrogen fuel is also increasingly being utilized in solid oxide fuel cells due to its efficiency and environmental benefits. Investments are being made to expand hydrogen infrastructure, including the development of refuelling stations for fuel cell vehicles and the establishment of hydrogen pipelines.

For instance, in October 2023, the Ministry of New and Renewable Energy of India published a research and development (R&D) roadmap for the National Green Hydrogen Mission. The roadmap has a budget of Rs 400 crore. Similarly, in March 2023, the European Commission committed an additional Euro 200 million to the Clean Hydrogen Joint Undertaking to speed up the deployment of hydrogen valleys. This is part of the REPowerEU Plan, which seeks to increase Europe's number of hydrogen valleys. Thus, the growing interest in green hydrogen will drive the growth of the market during the forecast period.

Market Segmentation

The hydrogen fuel market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

- Application Outlook

- Power and heat generation

- Transportation

- Source Outlook

- Grey

- Green

- Blue

- Region Outlook

- North America

- The U.S.

- Canada

- South America

- Chile

- Brazil

- Argentina

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

Power and heat generation

The power and heat generation is estimated to witness significant growth during the forecast period. Hydrogen fuel cells convert hydrogen gas and oxygen from the air into electricity through an electrochemical reaction. This process generates electricity, water vapour, and heat. Fuel cells are used in various applications, including stationary power generation, transportation (fuel cell vehicles), and portable power devices.

Get a glance at the market contribution of various segments Download the PDF Sample

The fuel cells use hydrogen fuel and oxygen from the air to generate power, water, and heat. The heat can be utilized to keep the battery compartment or cabin warm in temperatures as low as -30 degrees Celsius. Hydrogen fuel cells can be integrated into combined heat and power systems. In these systems, the heat produced as a byproduct of the electrochemical reaction can be captured and utilized for heating purposes, increasing the overall energy efficiency. Hydrogen fuel cells can provide power for remote or off-grid locations, acting as microgrid energy sources or backup power systems. Hydrogen can be used as a fuel in boilers for industrial heating applications. This can be an alternative to natural gas or conventional fuels. Thus, the use of hydrogen in power and heat generation offers several advantages, including high energy efficiency, low emissions (especially if produced through green or blue hydrogen methods), and versatility in applications, which will drive the growth of the power and heat generation segment and the market during the forecast period.

Hydrogen Fuel Market Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

APAC is estimated to contribute 56% to the growth of the global market during the forecast period. Technavioâs analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The regional hydrogen fuel market is expected to increase significantly during the forecast period. The emphasis on producing hydrogen through renewable methods, such as electrolysis powered by renewable energy sources (solar, wind), was a key factor. The APAC region's abundant renewable energy resources make it well-suited for sustainable hydrogen production. The industrial sector in the APAC region, including sectors such as steel, chemicals, and refining, was exploring the use of hydrogen as a clean energy source. Hydrogen's potential for decarbonizing industrial processes was a driving force for its adoption.

For instance, the Government of India has set a target of producing 5 million metric tons of green hydrogen per year by 2030. As a result, India would become a significant global producer of green hydrogen. In addition, the Government of India intends to cut carbon emissions by 50 million metric tons and save more than USD 12 billion on fossil fuel imports by 2030. Thus, these factors will drive the growth of the hydrogen fuel market in APAC during the forecast period.

Hydrogen Fuel Market Dynamic

The market is growing, despite explosion and flammability risks. Key drivers include steel reduction and carbon footprint reduction efforts, alongside the expanding grey hydrogen market and steam methane reformation techniques. The market is boosted by renewable energy capacity expansion, especially in the chemical sectors, which seek cleaner fuel solutions. A robust hydrogen network supports energy generation and desulfurization processes, while innovations in pyrolysis and ammonia production fuel further fuel cell development. Low emission fuel alternatives are essential to combat infrared radiation, net heat energy, and greenhouse gases, including CO2 emissions from electricity and heat production. The rise of synthetic energy carrier, such as synthetic gas, through alkaline electrolysis, reflects the industry's focus on energy transformation and decarbonization choices.

Key Driver of Hydrogen Fuel Market

Advancements in hydrogen technologies are notably driving the market growth. Improvement in electrolysis technology, particularly the development of high-efficiency electrolyzers, contributes to the cost reduction of green hydrogen production. Research and development efforts are focused on enhancing the performance and durability of fuel cells, including proton exchange membrane (PEM) and solid oxide fuel cells (SOFC). The development of advanced hydrogen storage materials and methods, including solid-state hydrogen storage, contributes to improving the safety, density, and practicality of storing hydrogen.

Moreover, advancements in hydrogen infrastructure technologies, including efficient compression and transportation methods, support the development of a robust and widespread hydrogen distribution network. The incorporation of digital technologies and automation in hydrogen production and utilization processes enhances operational efficiency and reduces costs. Thus, the advancements in hydrogen technologies will drive the growth of the market during the forecast period.

Significance Challenges of Hydrogen Fuel Market

Concerns associated with hydrogen purity and quality are a significant challenge hindering the market growth. The presence of impurities and contaminants, such as moisture, oxygen, sulfur compounds, and other trace elements, can negatively affect the performance and efficiency of hydrogen-based technologies, particularly fuel cells. The lack of standardized purity levels for hydrogen can lead to variations in quality. Different applications may require different purity standards, and a lack of harmonized standards can pose challenges for industry stakeholders.

Moreover, hydrogen's reactivity with certain materials, such as metals, can lead to embrittlement and other material degradation issues. Ensuring compatibility with storage and distribution infrastructure is crucial for maintaining purity. Thus, the concerns associated with hydrogen purity and quality will hinder the growth of the market during the forecast period.

Hydrogen Fuel Market Customer Landscape

The market research report includes the adoption lifecycle of the market, covering from the innovatorâs stage to the laggardâs stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market forecast report includes key purchase criteria and drivers of price sensitivity to help companies evaluate the their growth strategies.

Global Hydrogen Fuel Market Customer Landscape

Major Hydrogen Fuel Market Companies

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Acciona SA: The company offers hydrogen fuels such as grey hydrogen, blue hydrogen, and green hydrogen.

The research report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

- Air Products and Chemicals Inc.

- Ballard Power Systems Inc.

- ENGIE SA

- Equinor ASA

- HyAxiom, Inc.

- Iberdrola SA

- Indian Oil Corp. Ltd.

- ITM Power plc

- Linde Plc

- McPhy Energy SA

- Nel ASA

- Orsted AS

- Plug Power Inc.

- Praxair Technology Inc.

- Saudi Arabian Oil Co.

- Shell plc

- TotalEnergies SE

- Woodside Energy Group Ltd.

- Air Liquide SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market is central to addressing the greenhouse effect and reducing green gas emissions like CO2 emission. The development of synthetic energy carrier from electrical energy is advancing, with innovations that compress and liquefy hydrogen to optimize its energy content. Despite inherent energy losses, this transformation of chemical energy is crucial for hydrogen programmes. The market is also focusing on the deployment of hydrogen storage tanks in transportation markets, supported by low-carbon hydrogen generating technologies that meet stringent hydrogen purity requirements. Industrial clients are demanding precise metering and consistent gas quality in local gas markets. Hydrogen manufacturers are leveraging global sales and marketing networks to expand the gray hydrogen market, especially where low-cost natural gas is available, with significant applications in chemical and refinery sectors and aerospace and defense industries.

|

Hydrogen Fuel Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.51% |

|

Market Growth 2024-2028 |

USD 11.85 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.05 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 56% |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Acciona SA, Air Products and Chemicals Inc., Ballard Power Systems Inc., ENGIE SA, Equinor ASA, HyAxiom, Inc., Iberdrola SA, Indian Oil Corp. Ltd., ITM Power plc, Linde Plc, McPhy Energy SA, Nel ASA, Orsted AS, Plug Power Inc., Praxair Technology Inc., Saudi Arabian Oil Co., Shell plc, TotalEnergies SE, Woodside Energy Group Ltd., and Air Liquide SA |

|

Market dynamics |

Parent market analysis, Market growth and Forecasting ,Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our market forecasting report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth analysis between 2024 and 2028

- Precise estimation of the market size and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- A thorough analysis of the marketâs competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -