India Auto Component Market Size 2026-2030

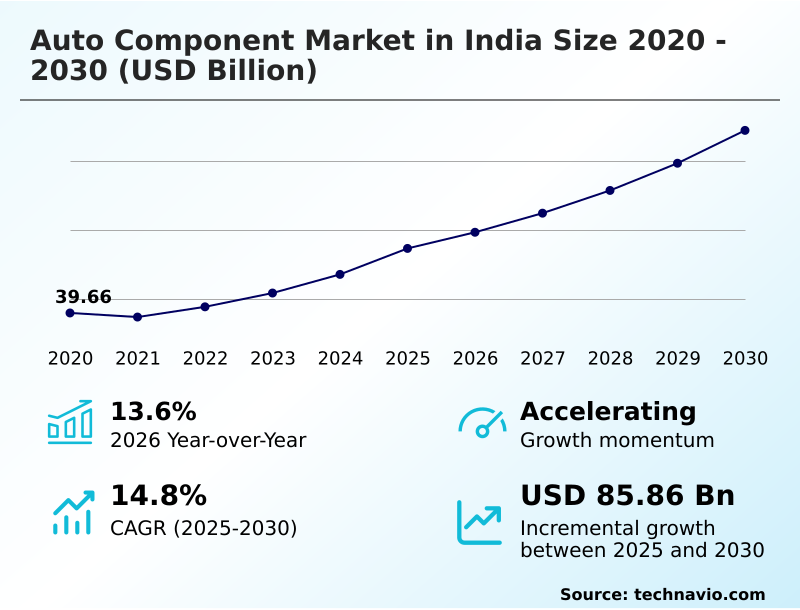

The india auto component market size is valued to increase by USD 85.86 billion, at a CAGR of 14.8% from 2025 to 2030. Growing middle-class population will drive the india auto component market.

Major Market Trends & Insights

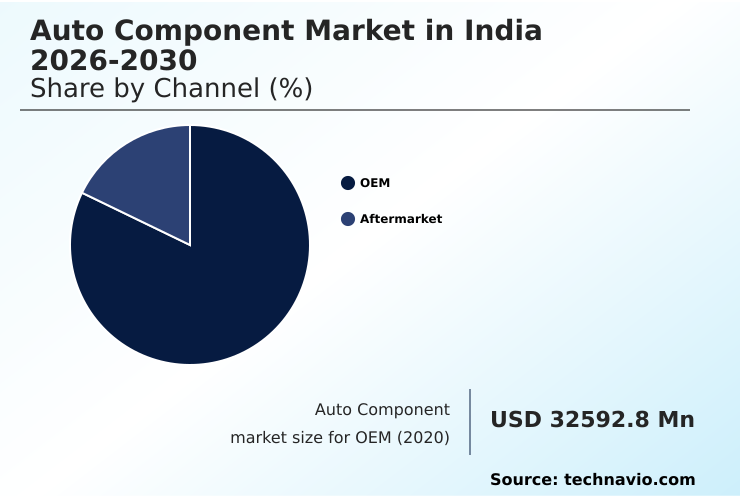

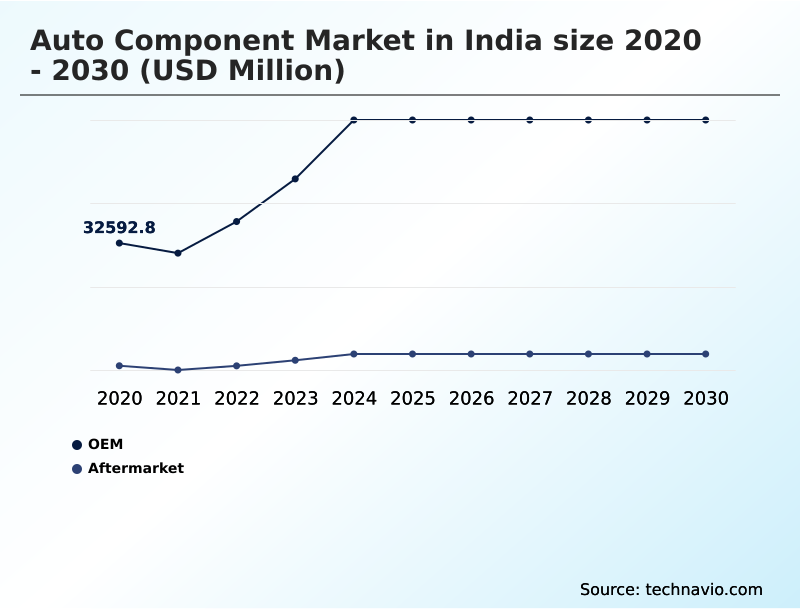

- By Channel - OEM segment was valued at USD 58.20 billion in 2024

- By Component - Engine and suspension and breaking segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 132.79 billion

- Market Future Opportunities: USD 85.86 billion

- CAGR from 2025 to 2030 : 14.8%

Market Summary

- The auto component market in India is undergoing a significant transformation driven by the concurrent trends of electrification, enhanced safety regulations, and the integration of digital technology. The industry is moving beyond traditional mechanical manufacturing to become a hub for sophisticated electronic components.

- Key drivers include a rising middle-class population boosting vehicle demand and stringent government mandates, such as BS-VI emission norms, which necessitate advanced emission control systems and fuel injection systems. This evolution creates substantial opportunities for suppliers of power electronics, battery management systems, and advanced driver assistance systems (ADAS).

- For instance, a typical business scenario involves a Tier-1 supplier collaborating with an OEM to co-develop a steer-by-wire system, which requires integrating complex sensors and electronic control units (ECU) while ensuring failsafe performance. However, the market faces challenges from a volatile global supply chain, where disruptions in semiconductor availability can halt production lines.

- To mitigate this, firms are increasingly focusing on localization of components and adopting digital supply chain solutions to improve resilience and maintain manufacturing continuity in a dynamic environment.

What will be the Size of the India Auto Component Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Auto Component Market Segmented?

The india auto component industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Channel

- OEM

- Aftermarket

- Component

- Engine and suspension and breaking

- Drive transmission and steering

- Electricals and electronics

- Body and chassis

- Others

- Vehicle type

- Passenger vehicles

- Two wheelers

- Light commercial vehicles

- Medium and heavy commercial vehicles

- Others

- Geography

- APAC

- India

- APAC

By Channel Insights

The oem segment is estimated to witness significant growth during the forecast period.

The auto component market in India is segmented primarily by channel, component, and vehicle type, with the OEM segment being a critical value driver.

The relationship between component suppliers and OEMs is transforming into a collaborative partnership, driven by the shift toward electric drivetrains and software defined vehicles (SDV).

Suppliers are no longer just providing hardware like engine parts or body and chassis structures; they are integral to developing complex systems, including advanced driver assistance systems (ADAS) and integrated infotainment systems.

This evolution demands early supplier involvement in the design phase, which now accounts for over 60% of the development cycle for critical electronic control units (ECU).

The need for high-strength steel and other lightweight materials to improve EV range further solidifies this deep integration.

The OEM segment was valued at USD 58.20 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- An in-depth review of the auto component market in India reveals a complex interplay between its primary sales channels, with the auto component market in India oem vs aftermarket dynamic defining revenue streams. The impact of electrification on indian auto components is profound, fundamentally altering demand away from traditional engine parts toward electric drivetrains and battery management systems.

- This shift concurrently exposes the industry to significant supply chain disruption in auto component manufacturing, particularly for semiconductors and raw materials for batteries. In response, firms that prioritize a localization strategy for automotive electronics in India have reported up to a 20% faster time-to-market compared to import-reliant competitors.

- The role of adas in indian passenger vehicles is expanding, driving growth in sensor and ECU manufacturing. Simultaneously, the bs-vi norms effect on engine component suppliers has forced investment in cleaner technologies. Key trends in lightweight materials for auto components, such as integrating high-strength steel in body and chassis, are crucial for improving EV range and safety.

- The growth of electronic components in two wheelers and the evolving future of powertrain systems in commercial vehicles highlight segment-specific opportunities. Challenges for aftermarket auto part retailers are mounting from e-commerce platforms, while the impact of pll scheme on auto component exports is creating new avenues for growth.

- Innovations in automotive lighting and sensor technology, advanced braking systems for electric vehicles, and nvh reduction solutions for passenger vehicles are key differentiators.

- The rise of software-defined vehicles, thermal management for high-voltage ev batteries, and advances in vehicle safety systems and regulations underscore the market's technological trajectory, supported by investment in battery management systems manufacturing and demand for connected mobility features in new cars.

What are the key market drivers leading to the rise in the adoption of India Auto Component Industry?

- The growing middle-class population is a critical structural driver, directly influencing vehicle ownership patterns and long-term demand for automotive parts.

- The expansion of India's middle class is a fundamental driver for the auto component market, fueling a consistent rise in vehicle ownership and creating sustained demand for both OEM and aftermarket parts.

- This demographic shift has led to a 15% increase in first-time vehicle purchases in non-metropolitan areas.

- The resulting growth in the vehicle parc directly boosts the aftermarket, where demand for routine replacement parts like brake systems and suspension systems has grown by over 25%.

- This trend encourages investment in the localization of components, strengthens the domestic manufacturing ecosystem for parts such as the wiring harness and starter motors, and supports long-term growth across the entire value chain, from raw material sourcing to final assembly.

What are the market trends shaping the India Auto Component Industry?

- The increasing frequency of automotive product launches is a significant trend shaping the market. This reflects the rapid evolution of consumer preferences, regulatory changes, and technological advancements.

- Increasing automotive product launches are accelerating innovation within the auto component market in India. OEMs are introducing new models with advanced features at a rapid pace, driving demand for modular architectures that allow for greater design flexibility and faster production cycles. This trend has shortened vehicle development timelines by nearly 20% for some manufacturers.

- The demand for sophisticated OEM components, particularly in the electronics domain, has surged, with the integration of connected mobility solutions increasing by 35% in new passenger car variants. This environment fosters early collaboration on components like powertrain systems and body and chassis structures, pushing suppliers to enhance their capabilities in producing advanced automotive lighting and lightweight materials.

What challenges does the India Auto Component Industry face during its growth?

- Supply chain disruption has emerged as a pressing challenge, significantly affecting production continuity, cost structures, and overall market competitiveness.

- Persistent supply chain disruption poses a significant challenge to the auto component market in India, impacting production continuity and cost stability. Global shortages of critical materials like semiconductors have led to production cutbacks affecting over 30% of high-end vehicle models, exposing vulnerabilities in the digital supply chain.

- Volatility in raw material and freight costs, which have risen by up to 40% in some cases, squeezes margins for manufacturers of parts such as engine parts and seating systems.

- These disruptions have highlighted the need for greater supply chain resilience, prompting firms to explore near-shoring strategies and invest in visibility tools to better manage inventory and mitigate risks associated with reliance on a limited number of global suppliers.

Exclusive Technavio Analysis on Customer Landscape

The india auto component market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india auto component market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Auto Component Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india auto component market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - Analysis indicates a focus on integrated systems, including advanced powertrain, chassis, and electronic solutions for next-generation mobility platforms.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Autoliv Inc.

- BorgWarner Inc.

- Brakes India Pvt. Ltd.

- Brembo SpA

- HELLA GmbH and Co. KGaA

- Hyundai Motor Group

- Lear Corp.

- Lucas TVS Ltd.

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Motherson Group

- Robert Bosch GmbH

- Schaeffler AG

- Tenneco Inc.

- Uno Minda Ltd.

- Valeo SA

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India auto component market

- In February 2025, Robert Bosch GmbH announced the completion of a state-of-the-art facility dedicated to the production of high-performance power modules for electric drivetrains.

- In September 2025, ZF Friedrichshafen AG unveiled a next-generation steer-by-wire system that eliminates mechanical connections, enhancing vehicle design freedom and safety.

- In October 2025, NDR Auto Components formed a 50:50 joint venture with Hayashi Telempu to establish NDR Hayashi Automotive India for manufacturing interior and trim components.

- In July 2025, Lumax Auto Technologies incorporated its wholly-owned subsidiary, Lumax Auto Solutions, to strengthen its automotive components portfolio and pursue new growth opportunities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Auto Component Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 199 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.8% |

| Market growth 2026-2030 | USD 85855.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.6% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The auto component market in India is advancing rapidly, driven by the integration of sophisticated technologies across all vehicle segments. The industry's core is shifting from mechanical assemblies to complex electronic systems. This evolution is evident in the rising demand for powertrain systems compatible with electric mobility, alongside advanced driver assistance systems (ADAS) that enhance vehicle safety.

- Key components such as the wiring harness, starter motors, and electronic control units (ECU) are becoming increasingly intricate to support new functionalities. Boardroom-level decisions are now heavily influenced by the need to invest in technologies like advanced thermal management systems and power electronics for electric vehicles.

- The strategic adoption of lightweight materials for the body and chassis is a prime example, with certain composite components achieving a 15% weight reduction, which directly improves electric vehicle range and performance. Furthermore, suppliers are focusing on next-generation seating systems, infotainment systems, and automotive lighting to meet consumer expectations for comfort and connectivity.

- This technological pivot requires significant R&D in areas like fuel injection systems and emission control systems to comply with stringent environmental regulations.

What are the Key Data Covered in this India Auto Component Market Research and Growth Report?

-

What is the expected growth of the India Auto Component Market between 2026 and 2030?

-

USD 85.86 billion, at a CAGR of 14.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Channel (OEM, and Aftermarket), Component (Engine and suspension and breaking, Drive transmission and steering, Electricals and electronics, Body and chassis, and Others), Vehicle Type (Passenger vehicles, Two wheelers, Light commercial vehicles, Medium and heavy commercial vehicles, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Growing middle-class population, Supply chain disruption in automotive industry

-

-

Who are the major players in the India Auto Component Market?

-

AISIN Corp., Autoliv Inc., BorgWarner Inc., Brakes India Pvt. Ltd., Brembo SpA, HELLA GmbH and Co. KGaA, Hyundai Motor Group, Lear Corp., Lucas TVS Ltd., Magna International Inc., Marelli Holdings Co. Ltd., Motherson Group, Robert Bosch GmbH, Schaeffler AG, Tenneco Inc., Uno Minda Ltd., Valeo SA and ZF Friedrichshafen AG

-

Market Research Insights

- The dynamics of the auto component market are shaped by a strategic pivot toward software-defined vehicle (SDV) architectures and connected mobility. Adoption of modular architectures has streamlined production, reducing platform development costs by up to 25% for certain OEMs.

- This transition is supported by a focus on supply chain resilience, with near-shoring strategies helping to cut lead times for critical OEM components by 15%. The implementation of the production linked incentive (PLI) scheme is another key factor, encouraging the localization of components and boosting domestic manufacturing capabilities.

- As vehicles become more complex, the emphasis on vehicle safety systems and adherence to BS-VI emission norms continue to drive innovation in both hardware and software, creating a competitive landscape where technological advancement is paramount.

We can help! Our analysts can customize this india auto component market research report to meet your requirements.

RIA -

RIA -