India Power Market Size 2024-2028

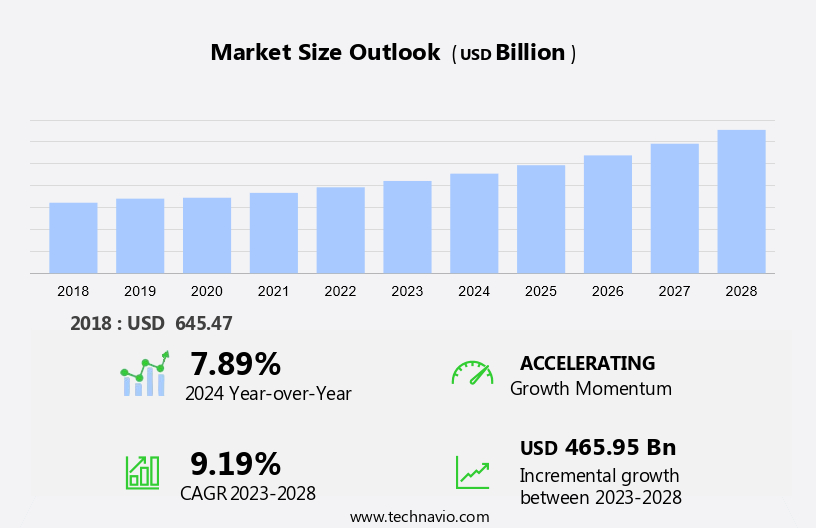

The India power market size is forecast to increase by USD 465.95 billion at a CAGR of 9.19% between 2023 and 2028. The Indian power market is witnessing significant growth, driven by government policies aimed at mitigating carbon footprints and striving for net zero emissions. The rising electricity demand, fueled by population growth and industrialization, necessitates infrastructural activities to scale up renewable energy infrastructure.

Solar energy is a key focus area, with foreign investment pouring in to capitalize on the country's abundant solar resources. However, challenges persist, including the poor financial health of DISCOMs in the power sector, which hampers the effective implementation of these initiatives. The Indian power market presents a unique opportunity for stakeholders to contribute to a sustainable energy future while addressing the pressing infrastructure needs of the country.

The Indian power market is a significant sector in the country's macroeconomics, with an annual power consumption of over 1,200 Terawatt-hours (TWh) and an installed capacity of over 380 GW as of 2021. The power generation sector is primarily driven by thermal (63%), hydro (19%), and renewable energy sources (18%). The regulatory structure plays a crucial role in shaping the power market, with policies focused on ensuring supply security and promoting generation infrastructure. Major power plants are located in various regions, including Western, Northern, Eastern, and Southern India. Asset transactions have been a significant trend in the power market, with several infrastructural activities underway to boost electricity demand and improve the overall efficiency of the sector. The market is expected to witness strong growth in the coming years due to increasing electricity demand and the government's focus on renewable energy.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

- Thermal

- Renewables

- Hydroelectric

- Nuclear

- End-user

- Industrial

- Commercial

- Residential

- Source

- Non-renewable

- Renewable

- Geography

- India

By Technology Insights

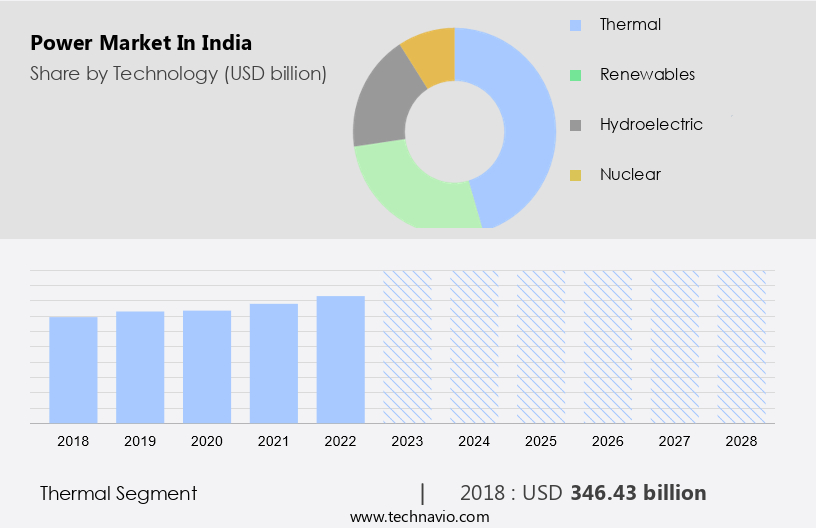

The thermal segment is estimated to witness significant growth during the forecast period. The market is significantly influenced by government policies, population growth, and infrastructure activities. Thermal power technology, which involves generating electricity through the combustion of fossil fuels, remains a crucial component of India's energy mix due to its reliability and cost-effectiveness. Abundant coal reserves in the country make it a readily available and reasonably priced fuel source for electricity generation. The Indian government's focus on increasing electricity access and meeting the rising electricity demand, particularly in rural areas, is driving infrastructural activities in the power sector. Furthermore, the government's initiatives to promote renewable energy, particularly solar energy, are also expected to supplement thermal power generation.

India's large population and rapid industrialization have led to a significant increase in electricity demand, making it an attractive destination for foreign investment in the power sector.

Get a glance at the market share of various segments Request Free Sample

The thermal segment accounted for USD 346.43 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

India Power Market Driver

Mitigating carbon footprints and striving for net zero emission is the key driver of the market. The market is experiencing significant growth as a result of the increasing focus on low-carbon and sustainable energy sources. In an effort to reduce carbon emissions in the mining sector and pursue net zero carbon targets, coal and lignite companies are expanding their energy portfolios by investing in solar projects.

Moreover, this includes both rooftop and ground-mounted installations, as well as the development of solar parks on previously mined land. As of May 26, 2023, coal and lignite public sector undertakings (PSUs) collectively boast an installed capacity of approximately 1,656 MW of solar energy and 51 MW of wind energy. Deal types in this sector include debt offerings, acquisitions, and asset transactions, as companies seek to diversify and strengthen their positions in the power market.

India Power Market Trends

Rise in investments in scaling up renewable energy infrastructure is the upcoming trend in the market. The Indian power market is witnessing a notable increase in investments aimed at expanding renewable energy infrastructure. This trend is primarily fueled by the decreasing costs of clean energy technologies, such as solar and wind power, which are now becoming more economically viable compared to traditional energy sources. Consequently, investors are increasingly drawn to the burgeoning opportunities in the renewable energy sector. One recent example is a US company's announcement in February 2023 to invest USD99.65 million in innovative technology in Uttar Pradesh, India, signing 269 letters of intent (LoI) to invest in the state's renewable energy sector prior to the Global Investors' Summit (GIS).

Furthermore, deal types in the power market include debt offerings, acquisitions, and asset transactions. For instance, in the debt offerings segment, the Indian Renewable Energy Development Agency (IREDA) issued bonds worth INR 2,000 crore in February 2023 to finance renewable energy projects.

India Power Market Challenge

Concerns on poor financial health of DISCOMS in power sector is a key challenge affecting the market growth. The market plays a pivotal role in the country's development and economic growth. It is an essential indicator of a nation's standard of living and provides energy to various sectors, with the transport sector being a significant consumer. The Indian power industry encounters several challenges, including unsustainable debt, insufficient debt servicing, inadequate electricity supply and service, and unacceptably high aggregate technical and commercial (AT&C) losses. These issues persist despite the implementation of numerous policies and reforms. The power sector value chain initiates with power generation by companies referred to as GENCOs. Subsequently, power is transmitted through lines connecting generation plants to distribution substations.

Furthermore, deal types in the power sector include debt offerings, acquisitions, and asset transactions. Debt offerings provide GENCOs with much-needed capital for expansion and maintenance. Acquisitions and asset transactions facilitate consolidation and efficiency gains within the industry. Despite the challenges, the market continues to attract significant investment due to its vast installed base and growth potential.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Adani Group - The company offers power solutions such as thermal power generation through Adani Power, and contributing to sustainable energy with renewables through Adani Green Energy

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Borosil Renewables Ltd.

- Gujarat Fluorochemicals Ltd.

- India Power Corp Ltd.

- Jindal Steel and Power Ltd.

- JSW Group

- KP Group

- NHPC Ltd.

- North Eastern Electric Power Corporation Ltd

- NTPC Ltd.

- Power Grid Corporation of India Ltd.

- Reliance Industries Ltd.

- RP Sanjiv Goenka Group

- SJVN Ltd

- Sterling and Wilson Pvt. Ltd

- Suzlon Energy Ltd.

- Tata Power Co. Ltd.

- Websol Energy System Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The Indian power market is a significant component of the country's macroeconomics, with an annual power consumption of over 1,200 TWh and an installed base of over 350 GW. The power sector's generation capacity is primarily derived from thermal sources, accounting for approximately 65% of the total capacity, with coal reserves being the primary fuel source. The regulatory scenario in the power sector is undergoing transformative changes, with a focus on supply security and infrastructure development. The power sector's future potential is immense, driven by increasing electricity demand, infrastructural activities in the transport sector, and population growth. Renewable energy, particularly solar energy, is gaining prominence, with the National Solar Mission aiming to install 100 GW of solar capacity by 2022.

Furthermore, the power market witnesses various deal types, including debt offerings, acquisitions, and asset transactions. Government policies play a crucial role in shaping the market, with financial incentives, subsidies, and concessional financing being key drivers for renewable power projects. The thermal power sector, however, faces challenges due to increasing competition from renewable energy and environmental concerns. The coal-fired generation capacity of thermal power plants is expected to remain a significant contributor to the power sector's capacity mix. The Indian power market is a dynamic and evolving sector, with significant growth potential. According to the latest power market research report, India's power sector is expected to witness robust growth, driven by various government initiatives and regulatory frameworks.

The power market regulatory structure in India is governed by the Ministry of Power, India, which sets the policy direction and regulates the sector. The transmission and distribution infrastructure is being upgraded to ensure reliable power supply and reduce losses. India's power sector deals primarily with thermal sources, which contribute to over 60% of the country's installed capacity. However, the National Wind Energy Mission and other renewable energy initiatives are pushing for a shift towards cleaner energy sources. India has an installed renewable energy capacity of over 50 GW, with plans to increase it further through ultra mega solar parks and viability gap funding. The electricity import and export scenario in India is also gaining importance, with neighboring countries like Bangladesh and Nepal emerging as potential trading partners. India's power market is witnessing several deals, including strategic partnerships, mergers and acquisitions, and foreign investments. In conclusion, the Indian power market presents a unique investment opportunity, with a favorable regulatory environment, growing demand, and a focus on renewable energy. The sector is poised for significant growth, making it an attractive destination for investors and stakeholders.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.19% |

|

Market growth 2024-2028 |

USD 465.95 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.89 |

|

Key companies profiled |

Adani Group, Borosil Renewables Ltd., Gujarat Fluorochemicals Ltd., India Power Corp Ltd., Jindal Steel and Power Ltd., JSW Group, KP Group, NHPC Ltd., North Eastern Electric Power Corporation Ltd, NTPC Ltd., Power Grid Corporation of India Ltd., Reliance Industries Ltd., RP Sanjiv Goenka Group, SJVN Ltd, Sterling and Wilson Pvt. Ltd, Suzlon Energy Ltd., Tata Power Co. Ltd., and Websol Energy System Ltd. |

|

Market dynamics |

Parent market analysis, market forecast , market growth inducers and obstacles,market forecast , fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across India

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -