Europe Industrial Waste Recycling And Services Market Size 2026-2030

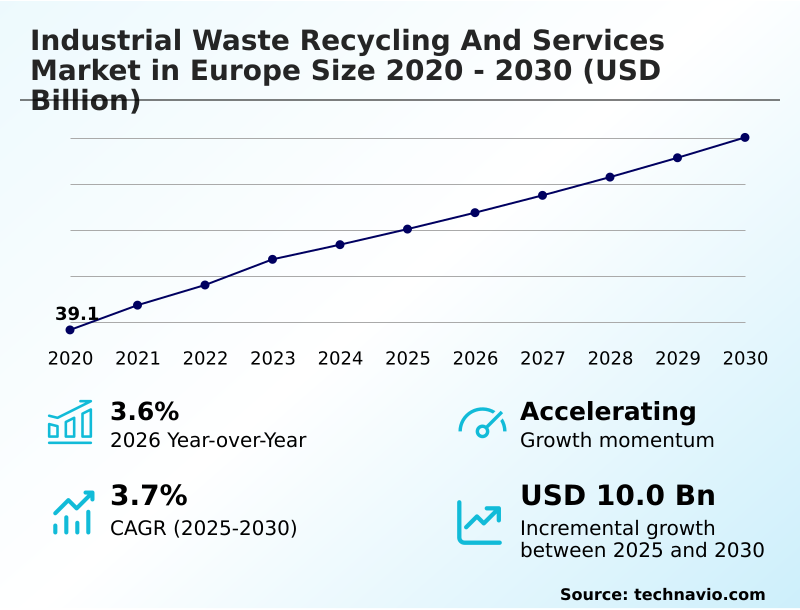

The europe industrial waste recycling and services market size is valued to increase by USD 10.00 billion, at a CAGR of 3.7% from 2025 to 2030. Growing volume of industrial waste will drive the europe industrial waste recycling and services market.

Major Market Trends & Insights

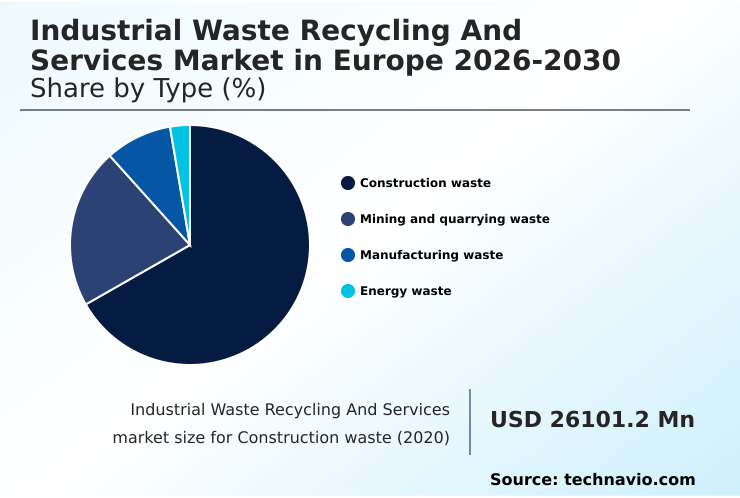

- By Type - Construction waste segment was valued at USD 31.87 billion in 2024

- By Service Type - Collection service segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 21.00 billion

- Market Future Opportunities: USD 10.00 billion

- CAGR from 2025 to 2030 : 3.7%

Market Summary

- The industrial waste recycling and services market in Europe is undergoing a significant transformation, driven by stringent regulations and a collective push toward sustainability. Adherence to circular economy principles is no longer optional, compelling industries to move beyond simple disposal and embrace comprehensive resource recovery efficiency.

- This involves the integration of advanced industrial waste treatment solutions and waste-to-energy technologies to minimize landfill use. For example, a manufacturing firm can implement a closed-loop recycling system, using digital waste tracking platforms and automated sorting systems to segregate and reprocess production scrap.

- This not only meets extended producer responsibility (EPR) mandates but also creates a new stream of secondary raw materials, reducing reliance on virgin inputs. However, the high capital expenditure for smart waste recycling infrastructure and the complexity of achieving waste segregation and treatment at scale remain persistent challenges.

- Navigating these requires a focus on integrated waste management systems (IWMS) that offer end-to-end visibility and control over the entire waste lifecycle, from collection to final recovery or disposal.

What will be the Size of the Europe Industrial Waste Recycling And Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Industrial Waste Recycling And Services Market Segmented?

The europe industrial waste recycling and services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

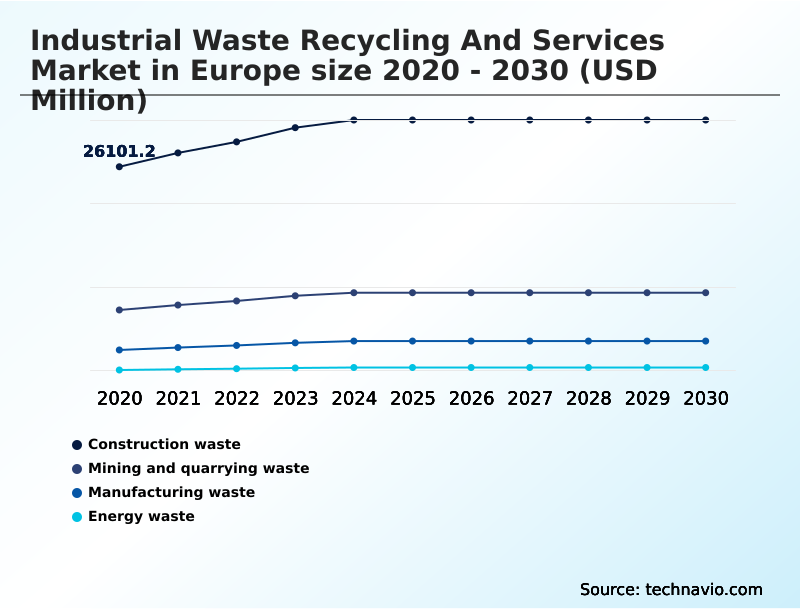

- Construction waste

- Mining and quarrying waste

- Manufacturing waste

- Energy waste

- Service type

- Collection service

- Recycling service

- Incineration service

- Landfill service

- Application

- Construction and demolition

- Mining

- Metallurgical

- Oil and gas

- Others

- Geography

- Europe

- Germany

- UK

- France

- Europe

By Type Insights

The construction waste segment is estimated to witness significant growth during the forecast period.

The construction waste segment is shaped by large-scale infrastructure development and urban renewal, compelling firms to adhere to strict landfill diversion targets.

This regulatory pressure drives the adoption of resource recovery efficiency and circular economy principles, where materials like concrete and metals are reprocessed.

Integration of automated sorting systems and smart demolition techniques is pivotal for improving recovery outcomes; for instance, advanced mobile crushing units can increase the retrieval of reusable aggregates by over 15%.

This focus on secondary raw material integration, industrial waste treatment solutions, and compliance with extended producer responsibility (EPR) frameworks defines the operational landscape. Success hinges on leveraging advanced technologies like AI-powered analytics tools to optimize waste segregation and treatment.

The Construction waste segment was valued at USD 31.87 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning for industrial waste recycling services in Europe requires a nuanced understanding of specific operational needs and regulatory pressures. For instance, developing circular economy models for construction waste is no longer a niche activity but a core competitive differentiator, with firms leveraging these models reporting higher material reuse rates than those using traditional methods.

- Similarly, the implementation of smart waste management for industrial parks involves more than just sensor-equipped bins; it demands a comprehensive look at the ROI of waste-to-energy plant investment and the integration of data analytics in European waste operations.

- The cost of implementing automated sorting systems remains a significant consideration, yet the long-term benefits in purity and throughput often justify the initial outlay, especially for handling complex streams like e-waste. Businesses are increasingly seeking specialized hazardous waste disposal solutions for manufacturing, as non-compliance with the EU waste framework directive can result in severe penalties.

- This has spurred interest in integrated waste systems for chemical plants and best practices for textile waste recycling. Moreover, managing oil and gas exploration waste and improving material recovery rates in mining are critical for resource-intensive sectors.

- The advancements in incineration emission control and the optimization of waste collection logistics with IoT are key technological enablers shaping the future of sustainable industrial operations.

What are the key market drivers leading to the rise in the adoption of Europe Industrial Waste Recycling And Services Industry?

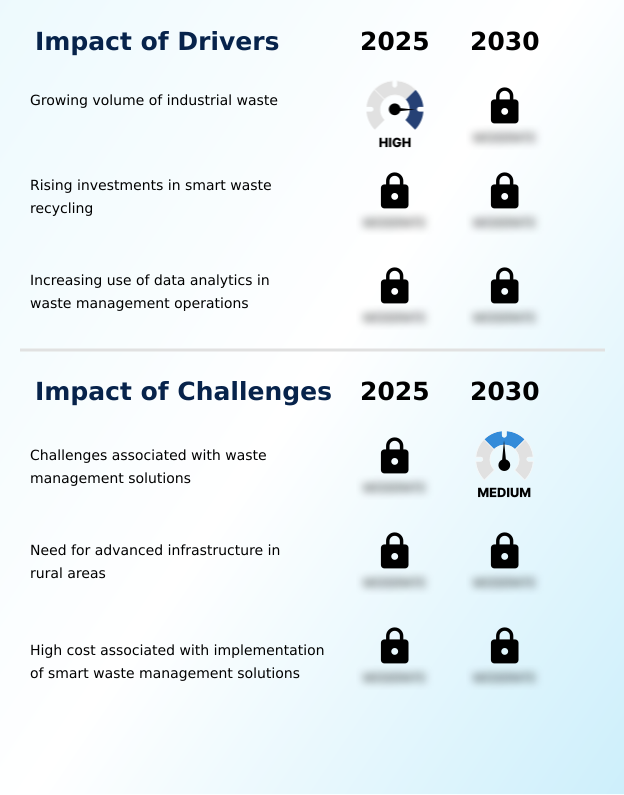

- The growing volume of industrial waste, driven by expanding industrial activities across multiple sectors, serves as a primary driver for the market.

- A primary driver for the market is the escalating volume of industrial byproducts coupled with tightening environmental regulations. The push for sustainable production practices compels industries to seek advanced industrial waste treatment solutions.

- Rising investments in smart waste recycling are a direct response, with firms leveraging these technologies to improve regulatory compliance reporting, reducing errors by over 25%.

- The increasing use of real-time monitoring systems not only enhances operational cost optimization but also supports environmental footprint reduction goals. By adopting data-driven decision making, companies can achieve better supply chain resource efficiency.

- For example, optimizing collection routes via digital platforms can lower fuel consumption by 10-15%, directly contributing to both economic and sustainability objectives across the waste management value chain.

What are the market trends shaping the Europe Industrial Waste Recycling And Services Industry?

- A growing focus on the circular economy is expediting market growth. This shift is fundamentally reshaping industrial waste management by emphasizing resource recovery and reuse.

- The market is increasingly shaped by the integration of smart technologies aimed at maximizing resource recovery. The growing adoption of circular economy principles is supported by advanced material recovery facilities (MRF) that leverage automated sorting systems, improving sorting accuracy by up to 30% over manual methods.

- This trend toward digitalization is evident in the use of AI-powered analytics tools, which enable predictive maintenance in waste management, reducing equipment downtime by 15%. Furthermore, the implementation of integrated waste management systems (IWMS) provides end-to-end visibility, helping firms meet stringent landfill diversion targets and extended producer responsibility (EPR) mandates.

- This technological shift is crucial for handling complex streams like e-waste and ensuring efficient thermal treatment of non-recyclable materials.

What challenges does the Europe Industrial Waste Recycling And Services Industry face during its growth?

- The complexities associated with managing diverse industrial waste streams present a significant challenge to the market's growth.

- A significant challenge remains the high capital expenditure in waste tech required to modernize infrastructure, particularly for specialized treatment processes. The complexity of waste segregation and treatment for mixed industrial streams often leads to contamination, which can reduce the value of recovered materials by up to 40%.

- Furthermore, logistical constraint optimization is a major hurdle in rural areas, where the lack of centralized recycling facilities increases operational costs. Ensuring robust cybersecurity for waste systems, which are increasingly connected, adds another layer of expense and complexity.

- These factors can slow the adoption of advanced solutions like high-temperature processing for metallurgical waste and thermal desorption systems for contaminated soil, posing a barrier to achieving comprehensive environmental risk mitigation.

Exclusive Technavio Analysis on Customer Landscape

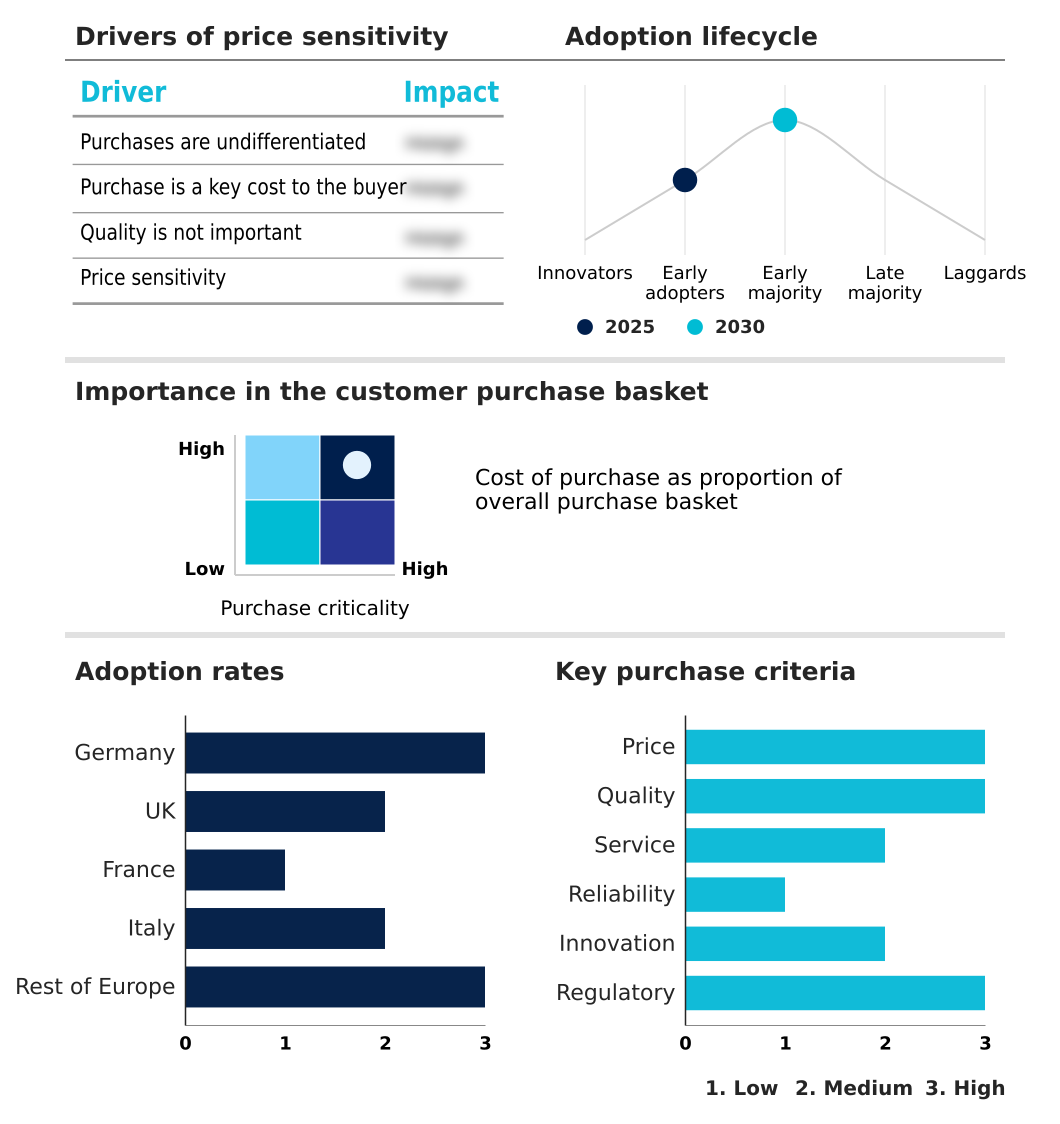

The europe industrial waste recycling and services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe industrial waste recycling and services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Industrial Waste Recycling And Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe industrial waste recycling and services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Averda - Specialized offerings include hazardous waste management, solvent recovery, and comprehensive industrial cleaning services, addressing complex environmental compliance needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Averda

- Biffa Plc

- Casella Waste Systems Inc.

- Clean Harbors Inc.

- Cleanaway Waste Management Ltd.

- Covanta Holding Corp.

- DS Smith Plc

- Ecobat LLC

- Enva

- Enviri Corp.

- GFL Environmental Inc.

- Heritage Environmental Services

- Paprec Group

- Recology Inc.

- Remondis SE and Co. KG

- Republic Services Inc.

- Saubermacher Dienstleistungs AG

- SUEZ SA

- Veolia Environment SA

- Waste Management Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe industrial waste recycling and services market

- In March 2025, Veolia Environment SA announced the completion of an upgrade to its construction waste recycling facilities in Western Europe, a move designed to enhance material recovery efficiency for large-scale infrastructure projects.

- In February 2025, SUEZ SA launched new material recovery solutions in Southern Europe aimed at improving the reuse of mineral residues from mining operations in industrial applications.

- In April 2025, Remondis SE and Co. KG reported the integration of advanced material recovery technologies at its Central European plants to boost recycling efficiency for high-volume manufacturing waste streams.

- In January 2025, Averda expanded its energy waste recovery services by deploying enhanced ash recycling systems aimed at increasing material recovery from power generation byproducts for use in the construction sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Industrial Waste Recycling And Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 235 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.7% |

| Market growth 2026-2030 | USD 10001.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.6% |

| Key countries | Germany, UK, France, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial waste recycling and services market is advancing beyond mere compliance to become a critical component of strategic operational planning. A key boardroom consideration is the adoption of circular economy principles, driven by stringent landfill diversion targets and the economic benefits of resource recovery efficiency.

- The integration of industrial waste treatment solutions, including advanced waste-to-energy technologies and material recovery facilities (MRF), is now fundamental. For example, companies deploying automated sorting systems for e-waste recycling have reported up to a 95% purity rate for recovered metals, directly impacting raw material costs.

- This shift is facilitated by smart waste recycling infrastructure and digital waste tracking platforms, which provide the data needed for effective extended producer responsibility (EPR) reporting. While navigating hazardous waste management and the complexities of waste segregation and treatment remains challenging, the use of AI-powered analytics tools and integrated waste management systems (IWMS) is enabling more proactive and efficient operations.

What are the Key Data Covered in this Europe Industrial Waste Recycling And Services Market Research and Growth Report?

-

What is the expected growth of the Europe Industrial Waste Recycling And Services Market between 2026 and 2030?

-

USD 10.00 billion, at a CAGR of 3.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Construction waste, Mining and quarrying waste, Manufacturing waste, and Energy waste), Service Type (Collection service, Recycling service, Incineration service, and Landfill service), Application (Construction and demolition, Mining, Metallurgical, Oil and gas, and Others) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Growing volume of industrial waste, Challenges associated with waste management solutions

-

-

Who are the major players in the Europe Industrial Waste Recycling And Services Market?

-

Averda, Biffa Plc, Casella Waste Systems Inc., Clean Harbors Inc., Cleanaway Waste Management Ltd., Covanta Holding Corp., DS Smith Plc, Ecobat LLC, Enva, Enviri Corp., GFL Environmental Inc., Heritage Environmental Services, Paprec Group, Recology Inc., Remondis SE and Co. KG, Republic Services Inc., Saubermacher Dienstleistungs AG, SUEZ SA, Veolia Environment SA and Waste Management Inc.

-

Market Research Insights

- The dynamics of industrial waste management are shifting toward data-driven decision making and operational cost optimization. The adoption of predictive waste volume forecasting allows service providers to improve resource allocation, leading to a 15% reduction in unnecessary collection trips.

- Furthermore, implementing proactive equipment maintenance schedules based on real-time monitoring systems has been shown to decrease facility downtime by up to 20% compared to reactive repairs. This focus on environmental footprint reduction is not just about compliance; it is about achieving greater supply chain resource efficiency.

- By leveraging these advanced platforms, companies gain enhanced waste lifecycle visibility, which is critical for meeting carbon neutrality targets and ensuring robust regulatory compliance reporting. This strategic approach transforms waste from a liability into a component of sustainable production practices.

We can help! Our analysts can customize this europe industrial waste recycling and services market research report to meet your requirements.

RIA -

RIA -