Insurance Software Market Size 2026-2030

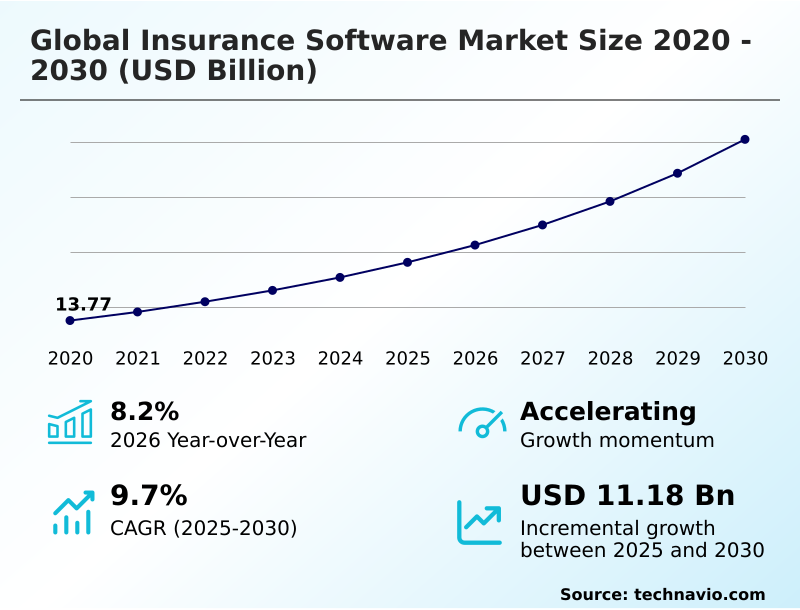

The insurance software market size is valued to increase by USD 11.18 billion, at a CAGR of 9.7% from 2025 to 2030. Digital transformation and automation driving market growth will drive the insurance software market.

Major Market Trends & Insights

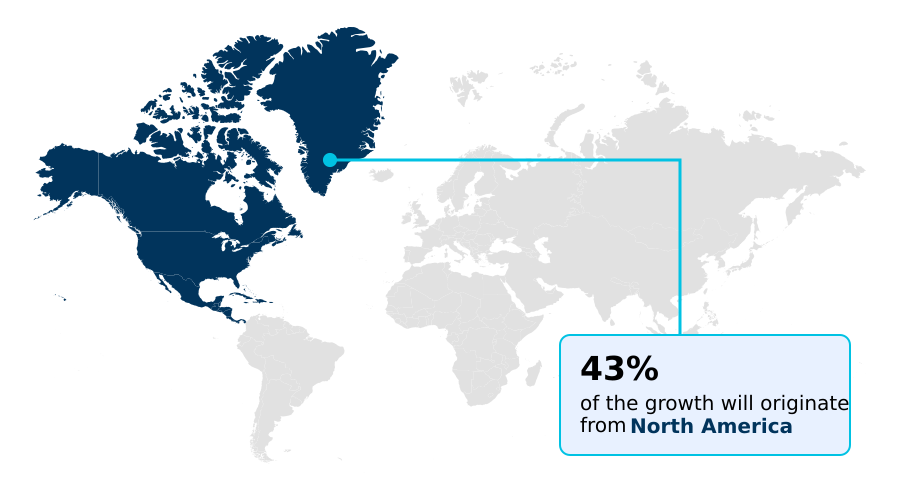

- North America dominated the market and accounted for a 42.9% growth during the forecast period.

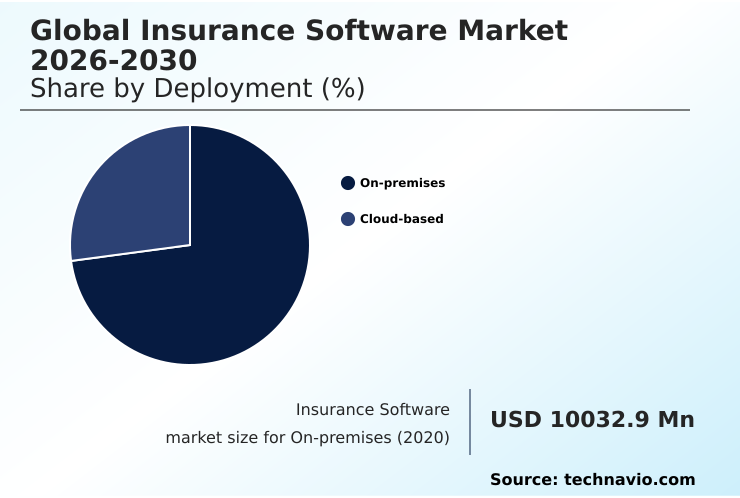

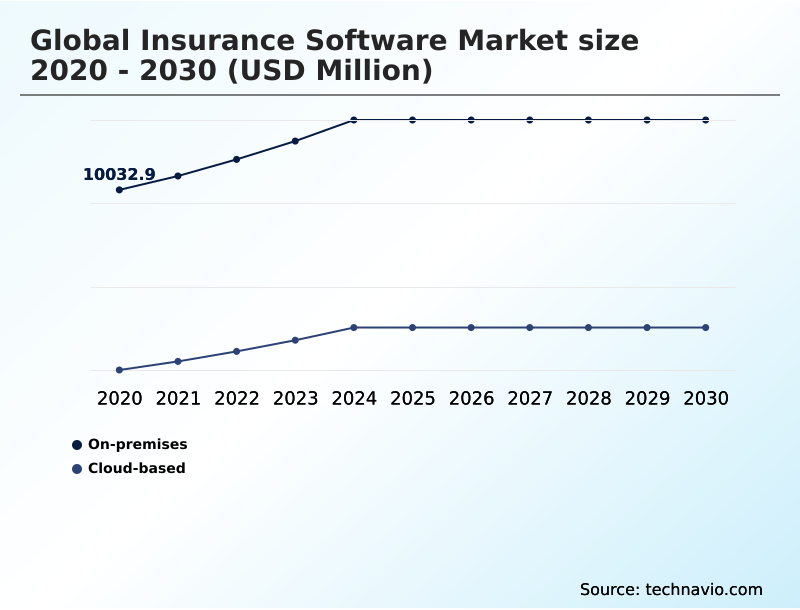

- By Deployment - On-premises segment was valued at USD 12.48 billion in 2024

- By Type - Life insurance segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 16.47 billion

- Market Future Opportunities: USD 11.18 billion

- CAGR from 2025 to 2030 : 9.7%

Market Summary

- The insurance software market is undergoing a fundamental shift from operational support to strategic enablement, driven by the convergence of advanced technologies and evolving customer expectations. The adoption of cloud-native deployment is accelerating, providing the scalability needed for sophisticated AI-driven claims automation and digital claims processing.

- For instance, an insurer can now leverage a core insurance platform that uses predictive analytics not only for underwriting accuracy but also for data-driven personalization of policies in real time. This capability, managed through integrated customer relationship management modules and delivered via omnichannel platforms, significantly enhances customer engagement.

- However, this progress is moderated by the persistent challenges of legacy system modernization and ensuring robust insurance data protection. Success hinges on a balanced strategy that embraces insurtech innovation ecosystem advancements while reinforcing regulatory compliance modules and implementing effective risk management platforms.

- The move towards intelligent automation tools and mobile-first insurance platforms is redefining how policies are administered and claims are managed, marking a new era of efficiency and customer-centricity.

What will be the Size of the Insurance Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Insurance Software Market Segmented?

The insurance software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- Type

- Life insurance

- Accident and health insurance

- Property and casualty insurance

- Others

- End-user

- Insurance companies

- Agencies

- Brokers

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises deployment model remains a cornerstone for insurers prioritizing granular control over data and security.

This approach allows for direct oversight of sensitive information and facilitates adherence to strict data protection standards, a key consideration for organizations managing vast portfolios.

Firms utilize on-premises solutions for core insurance platform functions and to run sophisticated risk management platforms, ensuring operational continuity without external dependencies.

These systems support essential tasks like claims estimation platforms and policy administration systems, with recent upgrades improving data retrieval speeds by over 25%.

Although requiring significant capital, this model offers robust capabilities for complex, secure operations, including the use of specialized P&C insurance software and wealth management platforms to serve diverse client needs.

The On-premises segment was valued at USD 12.48 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Insurance Software Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for over 42% of incremental growth, driven by mature regulatory structures and high adoption of advanced digital insurance platforms.

The region's focus on AI governance frameworks propels demand for sophisticated compliance solutions. In contrast, APAC is the fastest-growing region, where digital inclusion strategies and the rollout of mobile insurance applications are expanding market reach.

Insurers in APAC leveraging cloud-based systems have reported infrastructure cost reductions of up to 30%. Europe's market is characterized by a strong emphasis on data protection standards and sustainable risk management.

Meanwhile, emerging markets in South America and the Middle East and Africa are increasingly adopting SaaS-based solutions to modernize operations and support embedded insurance products, creating new opportunities for growth.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

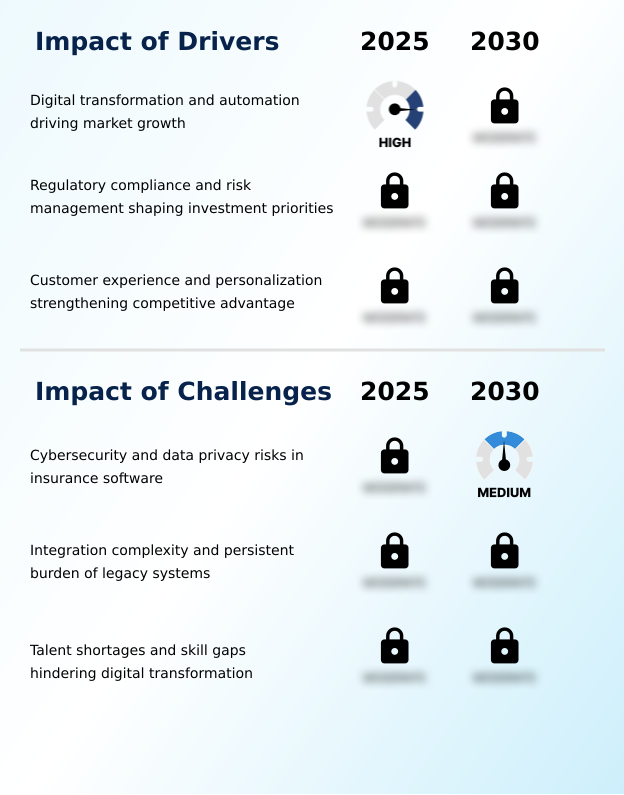

- The impact of digital transformation on insurers is profound, compelling a strategic reevaluation of core operations. Central to this is the goal of reducing costs with claims automation, a process streamlined by the benefits of cloud-native insurance platforms. These platforms are instrumental in both automating claims management for efficiency and improving underwriting accuracy with AI.

- The role of predictive analytics in insurance is expanding beyond risk assessment to power AI-driven fraud detection in insurance and inform sophisticated strategies for managing risk with insurance software. However, this technological leap introduces significant cybersecurity risks in insurance software, making best practices for insurance data privacy a boardroom-level concern.

- Consequently, insurance software for regulatory compliance is no longer optional but a foundational requirement. Organizations that successfully navigate the complexities of integrating legacy systems with modern software, often through low-code platforms for insurance workflow, see operational costs decrease at a rate twice that of their slower-moving peers.

- This transformation extends to distribution channels, with SaaS solutions for insurance agencies and the implementation of CRM for insurance brokers becoming standard. Ultimately, all these efforts converge on enhancing customer experience with digital platforms, achieved through omnichannel strategies for customer engagement and optimizing policy administration systems.

- The journey is complicated by the challenges of talent shortages in insurtech, yet the potential gains from leveraging technologies like blockchain applications in insurance claims drive the industry forward.

What are the key market drivers leading to the rise in the adoption of Insurance Software Industry?

- The primary driver propelling market growth is the widespread adoption of digital transformation and automation initiatives across the insurance sector.

- Digital transformation and automation are the primary drivers, compelling insurers to adopt modern insurance core systems and claims automation solutions.

- The need for operational efficiency is paramount; platforms that integrate digital core insurance platforms have demonstrated the ability to reduce manual processing errors by up to 90%.

- Furthermore, regulatory compliance remains a powerful catalyst, with automated reporting tools and integrated compliance modules becoming essential. Insurers using these systems have cut audit preparation times by an average of 30%.

- This is complemented by the strategic push to enhance customer engagement through CRM-based insurance solutions and life life insurance platforms that offer personalized experiences. This confluence of efficiency gains, regulatory adherence, and customer-centricity propels continuous investment in advanced software.

What are the market trends shaping the Insurance Software Industry?

- The reshaping of insurance software is significantly influenced by the integration of artificial intelligence. Predictive analytics, in particular, is emerging as a transformative force within the industry.

- Key market trends are converging to reshape the industry, led by the integration of AI-powered underwriting and advanced insurance analytics tools. These technologies are enabling a shift toward proactive risk management, with predictive models improving forecast accuracy by over 25%. Concurrently, the adoption of customer-centric platforms, built on scalable cloud insurance solutions, is redefining policyholder interactions.

- Firms that have embraced this model report a 15% increase in customer retention. The move toward automated support systems and mobile insurance applications further supports this trend by providing seamless, on-demand service.

- This digital transformation is underpinned by a strategic focus on insurance process automation and workflow management systems, ensuring that operational efficiency keeps pace with technological innovation and evolving customer expectations.

What challenges does the Insurance Software Industry face during its growth?

- A key challenge impacting the industry involves mitigating the inherent cybersecurity and data privacy risks associated with advanced insurance software.

- The industry faces significant challenges, primarily the complexity of legacy system modernization and persistent cybersecurity for insurers. Transitioning from outdated systems often leads to budget overruns, with projects exceeding initial estimates by an average of 40%. These legacy platforms are difficult to integrate with modern automated reporting systems and present vulnerabilities.

- The ongoing talent shortage exacerbates these issues, as the demand for professionals skilled in AI-powered underwriting and data privacy in insurance far outstrips supply, leaving critical roles vacant for extended periods.

- This skills gap slows the adoption of climate risk modeling and advanced insurance compliance software, hindering insurers' ability to innovate and manage emerging risks effectively, while also making insurance data protection more difficult to ensure.

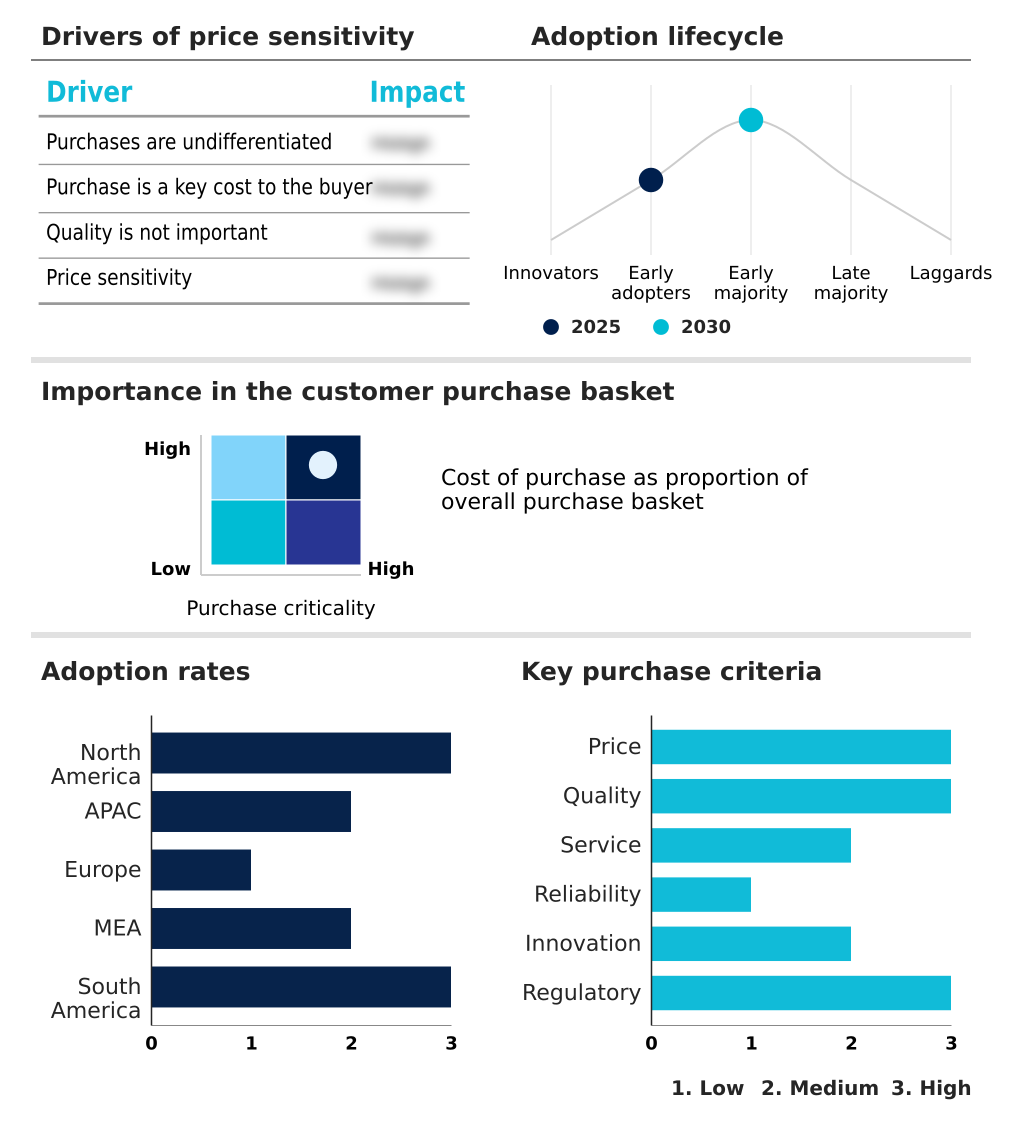

Exclusive Technavio Analysis on Customer Landscape

The insurance software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insurance software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Insurance Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, insurance software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Appian Corp. - Offerings center on a low-code automation platform, enabling streamlined claims automation and sophisticated workflow management systems for the insurance sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Appian Corp.

- Applied Systems Inc.

- CCC Intelligent Solutions

- Charles Taylor Ltd.

- Duck Creek Technologies LLC

- DXC Technology Co.

- EIS Group Inc.

- Equisoft

- Fair Isaac Corp.

- FRISS

- Guidewire Software Inc.

- Infosys Ltd.

- Insurity LLC

- Majesco

- Oracle Corp.

- Pegasystems Inc.

- Salesforce Inc.

- SAP SE

- Shift Technology

- Tata Consultancy Services

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Insurance software market

- In March 2025, Guidewire Software Inc. introduced an artificial intelligence-driven claims automation module designed to reduce claims processing times and improve operational efficiency for P&C insurers.

- In May 2025, Duck Creek Technologies LLC announced significant enhancements to its analytics suite, incorporating advanced machine learning models to improve underwriting accuracy and risk assessment.

- In April 2025, Charles Taylor Ltd. launched a blockchain-enabled compliance reporting tool for its InsureTech platform, targeting European property insurers to enhance transparency and streamline audit processes.

- In September 2024, Oracle Corp. expanded its Oracle Insurance Policy Administration system with new capabilities to support emerging microinsurance and specialty line products, particularly for the growing APAC market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insurance Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.7% |

| Market growth 2026-2030 | USD 11180.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insurance software market has evolved beyond simple digitalization, now focusing on intelligent, end-to-end process optimization. Core functions like policy administration and claims management systems are being transformed by AI-driven claims automation and advanced fraud detection analytics. This shift is built on a foundation of cloud-native deployment and increasingly, low-code automation platforms, which offer greater agility.

- Insurers are leveraging predictive analytics and sophisticated risk scoring solutions to enhance underwriting accuracy and enable data-driven personalization. For instance, the implementation of automated claims estimation platforms has been shown to reduce processing times by up to 40%. The adoption of comprehensive risk management platforms with integrated regulatory compliance modules is now standard practice.

- This technological overhaul, encompassing everything from digital core insurance platforms to CRM based insurance solutions, is critical for delivering the seamless experience customers expect from modern omnichannel platforms and ensuring long-term competitiveness in a rapidly changing landscape.

What are the Key Data Covered in this Insurance Software Market Research and Growth Report?

-

What is the expected growth of the Insurance Software Market between 2026 and 2030?

-

USD 11.18 billion, at a CAGR of 9.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud-based), Type (Life insurance, Accident and health insurance, Property and casualty insurance, and Others), End-user (Insurance companies, Agencies, and Brokers) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Digital transformation and automation driving market growth, Cybersecurity and data privacy risks in insurance software

-

-

Who are the major players in the Insurance Software Market?

-

Appian Corp., Applied Systems Inc., CCC Intelligent Solutions, Charles Taylor Ltd., Duck Creek Technologies LLC, DXC Technology Co., EIS Group Inc., Equisoft, Fair Isaac Corp., FRISS, Guidewire Software Inc., Infosys Ltd., Insurity LLC, Majesco, Oracle Corp., Pegasystems Inc., Salesforce Inc., SAP SE, Shift Technology and Tata Consultancy Services

-

Market Research Insights

- Market dynamics are shaped by the dual pressures of enhancing digital customer engagement and achieving greater operational efficiency through insurance process automation. The adoption of cloud insurance solutions is a key enabler, with implementations showing a direct correlation to a 15% improvement in claims processing efficiency.

- Insurers leveraging AI-powered underwriting and insurance analytics tools report up to a 20% gain in risk assessment accuracy compared to traditional methods. This push for innovation is balanced by the critical need for robust cybersecurity for insurers and effective data privacy in insurance protocols.

- As firms navigate these dynamics, the focus remains on delivering real-time policy adjustments and seamless omnichannel customer experiences, positioning technology as a central pillar of competitive strategy.

We can help! Our analysts can customize this insurance software market research report to meet your requirements.

RIA -

RIA -