Insurtech Market Size 2026-2030

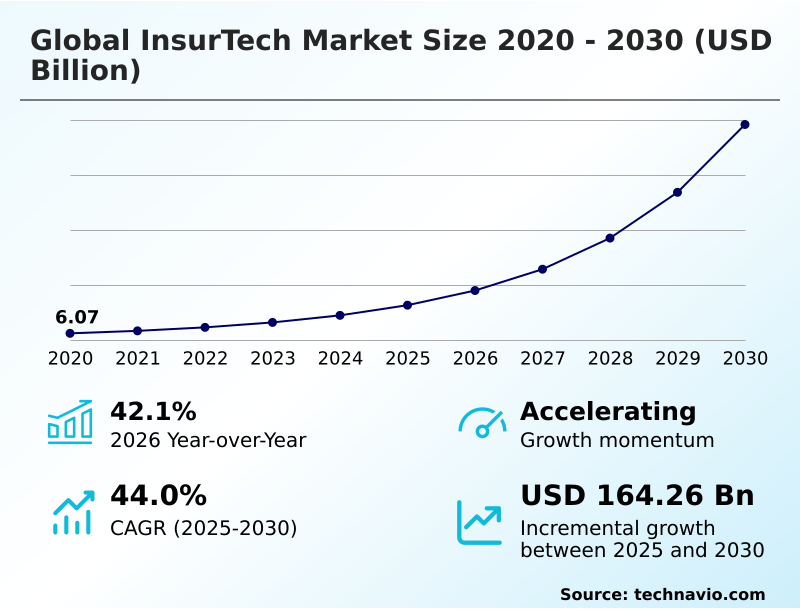

The insurtech market size is valued to increase by USD 164.26 billion, at a CAGR of 44% from 2025 to 2030. Acceleration of AI driven hyper personalization and predictive analytics will drive the insurtech market.

Major Market Trends & Insights

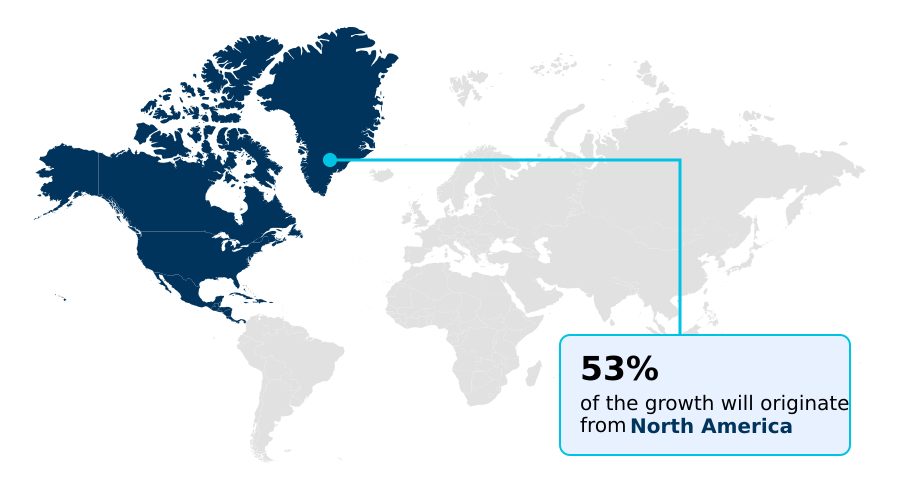

- North America dominated the market and accounted for a 52.8% growth during the forecast period.

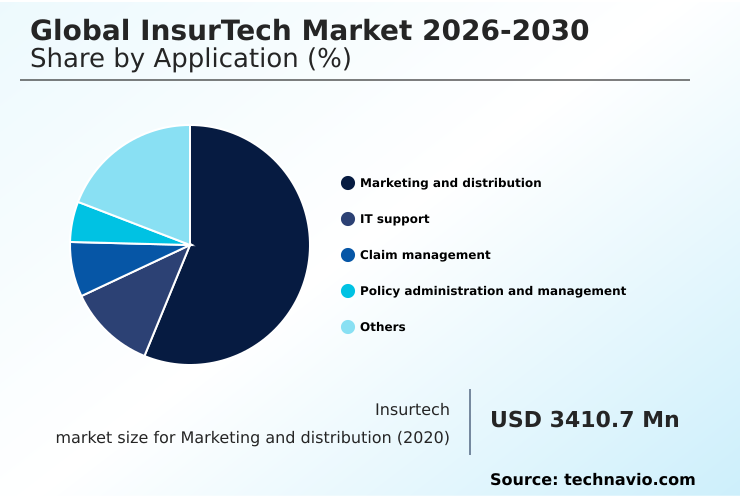

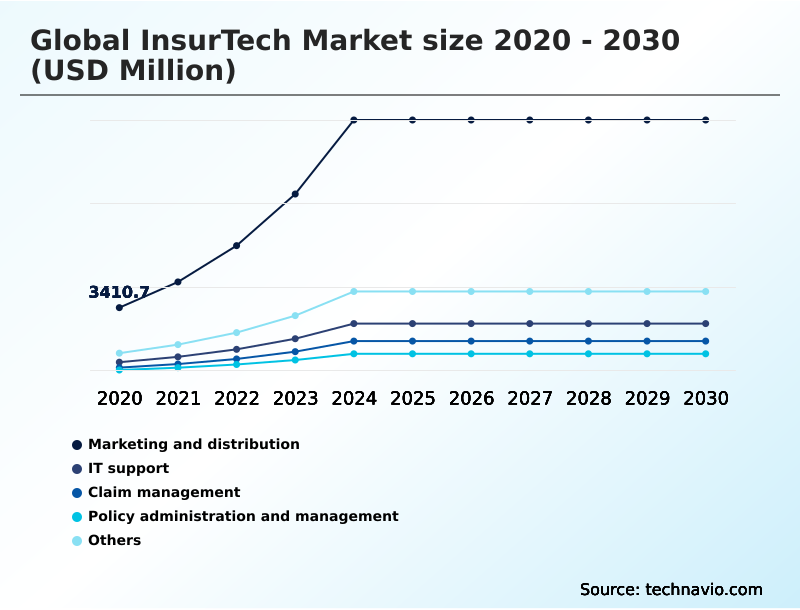

- By Application - Marketing and distribution segment was valued at USD 12.68 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 189.85 billion

- Market Future Opportunities: USD 164.26 billion

- CAGR from 2025 to 2030 : 44%

Market Summary

- The InsurTech market is undergoing a significant transformation, driven by the strategic integration of advanced technologies to enhance operational efficiency. This evolution is characterized by a shift from reactive models to proactive risk mitigation strategies, powered by AI-driven underwriting and predictive analytics.

- For example, a property and casualty carrier can now leverage computer vision for claims assessment, using automated damage assessment to analyze images of a damaged vehicle and generate a repair estimate within minutes, drastically reducing manual intervention. The adoption of cloud-native platforms is central to this change, providing the scalability needed for real-time data processing.

- However, this digitalization introduces challenges in data governance and necessitates robust cybersecurity protocols. The integration of the Internet of Things (IoT) and telematics data further refines risk assessment, enabling dynamic pricing and usage-based insurance products that align with modern consumer expectations for personalized insurance products and on-demand coverage.

What will be the Size of the Insurtech Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Insurtech Market Segmented?

The insurtech industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Marketing and distribution

- IT support

- Claim management

- Policy administration and management

- Others

- Deployment

- On-premises

- Cloud

- End-user

- Insurance companies

- Brokers

- Policyholders

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- India

- Australia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Colombia

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The marketing and distribution segment is estimated to witness significant growth during the forecast period.

The marketing and distribution segment is shifting from intermediary models to direct-to-consumer digital channels. This evolution leverages machine learning models for hyper-personalized engagement and dynamic pricing. Digital distribution strategies, supported by robust policy administration systems, are key.

By utilizing predictive modeling to identify life events, firms can deliver relevant offers at the moment of need through mobile-first insurance platforms.

API integration with non-insurance platforms creates a seamless ecosystem, improving customer experience automation and driving a 15% increase in conversion rates.

This focus on a frictionless user journey, offering personalized insurance products, is essential for fostering long-term loyalty and managing the entire customer lifecycle management.

The Marketing and distribution segment was valued at USD 12.68 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 52.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Insurtech Market Demand is Rising in North America Get Free Sample

The geographic landscape of the insurtech market is led by North America, which accounts for over 52% of incremental growth, driven by advanced risk assessment technologies and a mature venture capital ecosystem.

In this region, automated underwriting systems are standard, and firms are aggressively adopting AI for real-time risk mitigation. Europe follows, with a strong focus on regulatory compliance and data privacy, fostering innovation in areas like open insurance.

The APAC region is the fastest-growing, where a mobile-first population has allowed digital insurance platforms to leapfrog legacy systems, with AI-driven fraud detection being a key investment area.

In APAC, the use of computer vision and IoT for property insurance is expanding rapidly, especially in markets like China and India, addressing the needs of a burgeoning digital economy.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic evolution of the insurtech landscape is heavily influenced by the deepening integration of specific technologies addressing core industry challenges. The impact of AI on insurance underwriting is profound, moving carriers from static analysis to dynamic, real-time evaluations.

- A key aspect of this transformation is using telematics data for risk modeling, which has fundamentally changed auto insurance by enabling premiums based on actual driving behavior. Concurrently, the role of blockchain in parametric insurance is gaining prominence, creating transparent, automated payout systems for trigger-based events, which are over 70% faster than traditional claims processes.

- The benefits of embedded insurance API integration are also clear, as it seamlessly places coverage options at the digital point of sale, altering distribution dynamics. However, the challenges of legacy system migration remain a significant hurdle for established players. In response, many are turning to generative AI for customer service bots to improve user experience without a complete system overhaul.

- Furthermore, computer vision applications in claims and how IoT reduces property insurance claims are shifting the focus from indemnity to proactive prevention. This tech-forward environment necessitates advanced cybersecurity measures for digital insurers and strict adherence to data privacy regulations in insurtech.

- To maintain profitability, firms are heavily investing in automated fraud detection in insurance and utilizing real-time analytics for dynamic pricing, all contributing to the overarching goal of creating personalized insurance with big data. The impact of open insurance on brokers is also reshaping the intermediary landscape, favoring those who adopt tech-enabled advisory roles.

What are the key market drivers leading to the rise in the adoption of Insurtech Industry?

- The acceleration of AI-driven hyper-personalization and predictive analytics is a key driver fueling market growth.

- Key market drivers are centered on the use of technology to create highly personalized and efficient insurance products.

- The acceleration of AI-driven underwriting, supported by powerful predictive analytics, allows insurers to move beyond demographic proxies to assess risk based on individual behaviors.

- This is particularly evident in the rise of usage-based insurance (UBI) and on-demand coverage, where telematics data from vehicles provides real-time insights for auto insurance.

- This data-driven decision making has been shown to reduce claims frequency by up to 20% among participating drivers. Simultaneously, the proliferation of embedded insurance is transforming distribution, integrating protection products directly into non-insurance transactions.

- This model of proactive risk prevention not only enhances consumer convenience but also increases customer retention rates by an average of 15% for partner platforms.

What are the market trends shaping the Insurtech Industry?

- The increasing dominance of generative AI and agentic workflows represents a significant market trend. This shift is reshaping operational capabilities and customer interaction models across the industry.

- The market is being reshaped by the transition to advanced automation, with generative AI and agentic workflows at the forefront. This trend goes beyond basic chatbots, using sophisticated natural language processing (NLP) to handle nuanced customer interactions and synthesize complex policy documents.

- A significant application is in claims automation, where AI in claims processing, combined with automated damage assessment technology, can evaluate digital claims submissions and draft settlement offers. This capability has been shown to enhance adjuster productivity by over 35%. Furthermore, parametric insurance is gaining traction, particularly for climate-related risks, where blockchain for smart contracts can trigger automatic payouts.

- These systems, utilizing satellite data, can provide liquidity up to 90% faster than traditional indemnity claims, demonstrating a clear shift toward real-time, data-driven insurance solutions.

What challenges does the Insurtech Industry face during its growth?

- Escalating regulatory complexity and the need for global data governance compliance present a key challenge to industry growth.

- Significant challenges persist, primarily concerning regulatory complexity and technological resilience. Navigating the fragmented landscape of global data governance and adhering to new standards like the AI Act requires substantial investment in regulatory compliance automation. For many startups, these compliance costs can exceed 10% of their total operating budget, acting as a barrier to scale.

- Concurrently, the move to interconnected, cloud infrastructure for insurers via an open insurance framework expands the surface area for sophisticated cyber threats, necessitating robust cybersecurity protocols. The persistence of legacy systems further complicates this, as migrating to a modern cloud-native platform while ensuring blockchain technology integration is a complex and costly endeavor.

- This transition often increases IT spending by as much as 40% in the short term, straining resources and demanding a careful balance between innovation and operational stability.

Exclusive Technavio Analysis on Customer Landscape

The insurtech market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insurtech market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Insurtech Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, insurtech market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alan SA - Delivers a comprehensive cloud-based core platform enabling policy, billing, and claims management for the P&C insurance industry, fostering ecosystem integration.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alan SA

- Bolttech

- Clover Health

- Coalition Inc.

- Cover Genius

- Duck Creek Technologies LLC

- Ethos Technologies Inc

- Guidewire Software Inc.

- Hippo Enterprises Inc

- Lemonade Inc.

- Majesco

- Metromile Inc.

- MILVIK AB

- NEXT Insurance

- Oscar Insurance Corp.

- Policygenius Inc.

- Root inc

- Shift Technology

- Tractable Ltd.

- wefox Holding AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Insurtech market

- In September 2024, MetLife acquired a significant stake in the digital insurer Klimber to advance mobile-first distribution and strengthen its embedded insurance capabilities.

- In October 2024, Guidewire introduced a revamped cloud-native framework designed specifically to facilitate third-party integrations, highlighting the industry-wide focus on interoperability for embedded insurance.

- In December 2024, Brazil's government enacted a new Insurance Contract Act, a comprehensive regime designed to increase transparency and strengthen the rights of the insured, forcing an overhaul of technical systems.

- In January 2025, The Insurance Regulatory and Development Authority of India introduced revised cybersecurity guidelines that mandate quarterly risk reviews and grant greater autonomy to Chief Information Security Officers to combat digital threats.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insurtech Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 44% |

| Market growth 2026-2030 | USD 164263.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 42.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Switzerland, The Netherlands, Spain, China, India, Australia, Japan, Singapore, South Korea, UAE, Saudi Arabia, South Africa, Israel, Kenya, Brazil, Colombia and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insurtech market is defined by a strategic pivot toward integrating intelligent technologies to overhaul the entire insurance value chain. A key boardroom focus is the adoption of AI-driven underwriting and predictive analytics, which are no longer optional but essential for competitive risk assessment and dynamic pricing.

- The deployment of a cloud-native platform is fundamental, enabling the agility needed to launch innovative products like parametric insurance and usage-based insurance (UBI). The use of telematics data and Internet of Things (IoT) devices provides a continuous stream of information, refining machine learning models and enhancing fraud detection capabilities.

- For instance, the application of computer vision for claims automation has been shown to reduce claims cycle times by up to 50% in certain P&C lines. This level of efficiency directly impacts operational expenditures and capital allocation strategies.

- As the industry moves forward, success will depend on mastering API integration for embedded insurance, ensuring stringent data governance and cybersecurity protocols, and leveraging regulatory technology (regtech) to navigate complex compliance landscapes. The evolution is clear: from basic policy administration to sophisticated, AI-powered agentic workflows and digital distribution.

What are the Key Data Covered in this Insurtech Market Research and Growth Report?

-

What is the expected growth of the Insurtech Market between 2026 and 2030?

-

USD 164.26 billion, at a CAGR of 44%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Marketing and distribution, IT support, Claim management, Policy administration and management, and Others), Deployment (On-premises, and Cloud), End-user (Insurance companies, Brokers, and Policyholders) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Acceleration of AI driven hyper personalization and predictive analytics, Escalating regulatory complexity and global data governance compliance

-

-

Who are the major players in the Insurtech Market?

-

Alan SA, Bolttech, Clover Health , Coalition Inc., Cover Genius, Duck Creek Technologies LLC, Ethos Technologies Inc, Guidewire Software Inc., Hippo Enterprises Inc, Lemonade Inc., Majesco, Metromile Inc., MILVIK AB, NEXT Insurance, Oscar Insurance Corp., Policygenius Inc., Root inc, Shift Technology, Tractable Ltd. and wefox Holding AG

-

Market Research Insights

- The market's dynamics are shaped by a strategic push toward operational efficiency and enhanced customer experience automation. The adoption of digital insurance platforms is widespread, with firms leveraging data-driven decision making to refine product offerings. This technological integration yields tangible results; for instance, the implementation of automated underwriting systems reduces policy issuance times by over 60% compared to manual methods.

- Similarly, embedded insurance models that utilize an open insurance framework can lower customer acquisition costs by up to 25%. As the industry pivots to proactive risk prevention, the focus remains on leveraging technology to create more resilient and customer-centric business models that can adapt to a complex regulatory environment.

We can help! Our analysts can customize this insurtech market research report to meet your requirements.

RIA -

RIA -