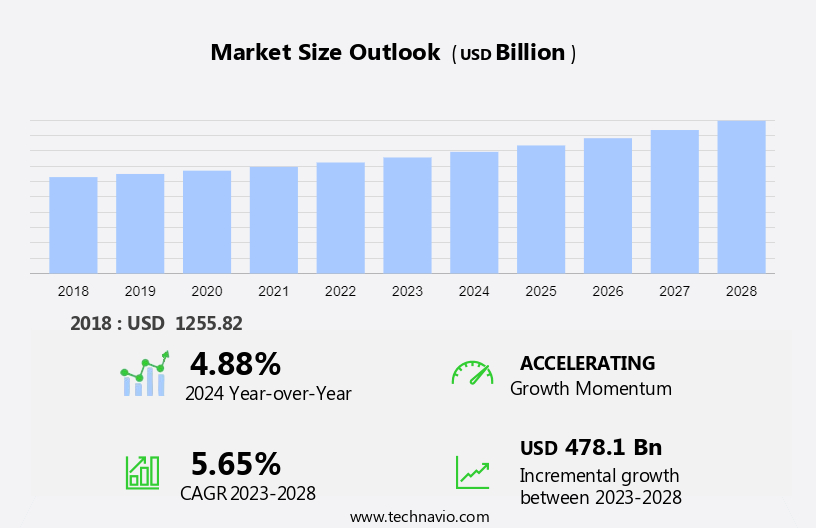

Iron and Steel Market Size 2024-2028

The iron and steel market size is forecast to increase by USD 478.1 billion, at a CAGR of 5.65% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing consumption of high-strength stainless steel. This trend is fueled by the expanding infrastructure sector, particularly in emerging economies, and the growing demand for stainless steel in various end-use industries such as construction, automotive, and packaging. Furthermore, the rising popularity of stainless steel scrap as a cost-effective alternative to primary steel production is contributing to market expansion. However, the market faces challenges as well. Carbon fiber is increasingly gaining traction in the automotive industry, posing a threat to the demand for steel and stainless steel.

- This shift is due to the lightweight and high-strength properties of carbon fiber, making it an attractive alternative for manufacturers seeking to reduce vehicle weight and improve fuel efficiency. Companies in the iron and steel industry must adapt to this trend by focusing on innovation and developing new applications for steel and stainless steel that offer superior performance or cost advantages over carbon fiber. Additionally, ensuring sustainable production methods and addressing environmental concerns will be crucial in maintaining market competitiveness and addressing regulatory pressures.

What will be the Size of the Iron and Steel Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in steel production technologies and the diverse applications of various steel types across numerous sectors. High-strength low-alloy steel, for instance, is increasingly sought after for its enhanced yield strength and hardness, making it suitable for use in automotive and construction industries. Impact testing and hardness testing are crucial in ensuring the quality and durability of these high-performance steels. Stainless steel, with its excellent corrosion resistance, is another key player in the market. The production of stainless steel involves processes such as pig iron production, coke making, and sintering, followed by electric arc furnace melting and continuous casting.

The industry anticipates a steady growth of around 4% annually, fueled by increasing demand from sectors like aerospace and healthcare. An example of this market's continuous dynamism can be seen in the implementation of advanced high-strength steel in the automotive industry. A major automaker reported a 15% increase in fuel efficiency by using this steel in vehicle production. The steel's superior properties, such as increased tensile strength and fatigue resistance, contribute to the overall improvement in vehicle performance and sustainability. Quality control systems, steel scrap recycling, and steel microstructure analysis are essential components of the steel manufacturing process.

They ensure the consistent production of steel grades that meet specific customer requirements. The integration of coating lines and galvanizing lines further enhances the versatility of steel products. Alloy steel and carbon steel undergo various processes, including blast furnace operation, basic oxygen furnace, hot rolling mill, and cold rolling mill, to achieve their desired properties. Heat treatment and pickling line processes further refine these steels for specific applications. The ongoing innovation in steelmaking technologies, such as secondary steelmaking and yield optimization techniques, continues to shape the market landscape.

How is this Iron and Steel Industry segmented?

The iron and steel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

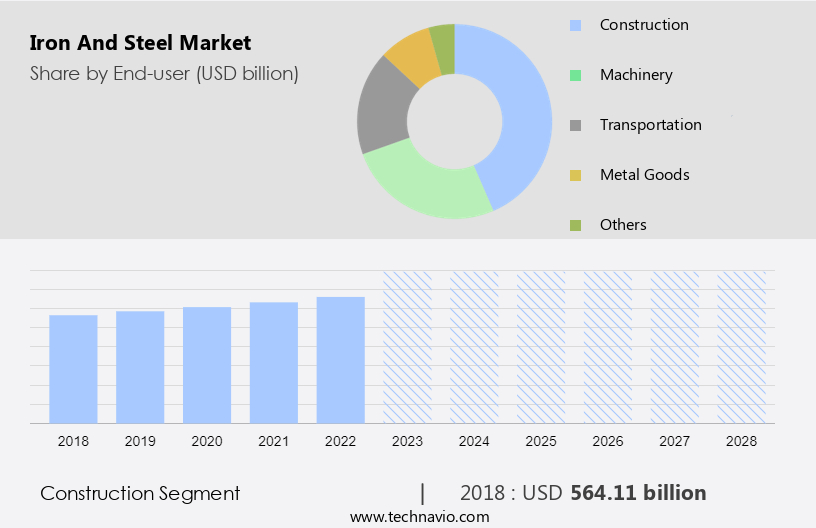

- End-user

- Construction

- Machinery

- Transportation

- Metal goods

- Others

- Type

- Steel

- Iron

- Geography

- North America

- US

- Europe

- Russia

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The construction segment is estimated to witness significant growth during the forecast period.

The market is a critical sector in the construction industry, supplying essential components for structural integrity, durability, and versatility. High-strength low-alloy steel, for instance, undergoes impact testing and hardness testing to ensure its robustness in various applications. Stainless steel, another key player, offers corrosion resistance and is extensively used in galvanizing lines and coating lines. Pig iron production and coke making are fundamental processes in steelmaking, while advanced high-strength steel is gaining popularity due to its enhanced properties. The steel industry anticipates significant growth, with expectations of a 5% increase in production by 2025. Carbon steel, produced via blast furnaces and basic oxygen furnaces, forms the backbone of the industry.

Steel scrap recycling plays a significant role in reducing production costs and minimizing environmental impact. Continuous casting, secondary steelmaking, and heat treatment are crucial processes in steel production, ensuring the desired microstructure and tensile strength. An example of steel's impact on the construction industry is the use of structural steel in the iconic Millennium Bridge in London. This bridge, with its distinctive tilting mechanism, required high-strength steel to maintain its unique design and functionality. With ongoing advancements in steel technology, the industry continues to evolve, offering innovative solutions for various applications.

The Construction segment was valued at USD 564.11 billion in 2018 and showed a gradual increase during the forecast period.

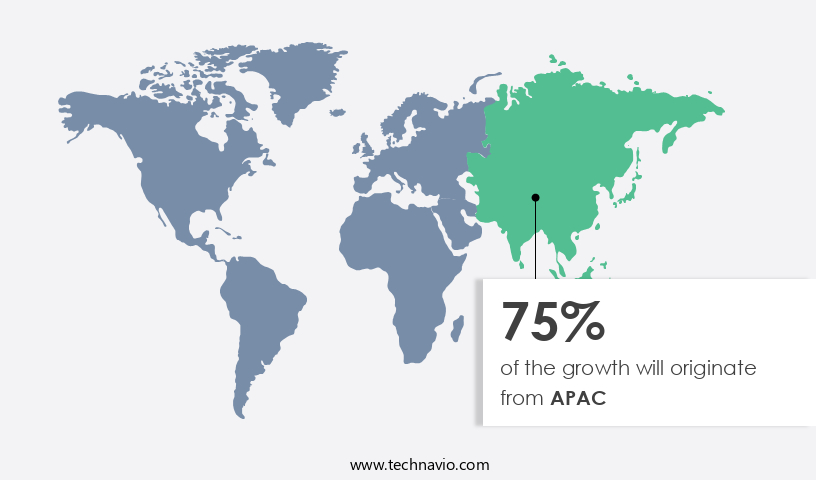

Regional Analysis

APAC is estimated to contribute 75% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, particularly in the Asia Pacific region. The construction industry's expansion, driven by the aging infrastructure and rising demand, is a major factor fueling this growth. In the energy sector, the continuous increase in oil production and drilling activities is leading to increased demand for iron and steel in the manufacturing of pipes and tubes. Additionally, the automotive and construction industries' growth is boosting market demand. However, the market's expansion is being challenged by fluctuations in oil prices and the shortage of iron and steel-based pipes and tubes. The iron and steel industry's production processes include pig iron production through the blast furnace, coke making, and the sintering process.

Advanced high-strength steel production involves electric arc furnaces, continuous casting, secondary steelmaking, and heat treatment. Quality control systems ensure the production of steel with specific properties, such as yield strength, tensile strength, and hardness. Stainless steel, an alloy steel with excellent corrosion resistance, is a significant market segment. The galvanizing line and coating line are used to protect steel from corrosion. Steel scrap recycling plays a crucial role in the iron and steel industry's sustainability efforts. According to recent industry reports, The market is expected to grow at a steady rate, with APAC accounting for over 50% of the global production.

For instance, China, the world's largest steel producer, produced approximately 1.2 billion metric tons of steel in 2020. The market's growth is attributed to the increasing demand for steel in various industries, including construction, automotive, and energy.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and complex industry, characterized by continuous innovation and advancements in steel production technologies. High-strength low-alloy steels (HSLA) have gained significant traction in various applications due to their enhanced properties, including improved tensile strength and weldability. In the realm of advanced high-strength steels (AHSS), corrosion resistance mechanisms in stainless steel are of paramount importance, ensuring longevity in harsh environments. To optimize electric arc furnace (EAF) power consumption, producers employ sophisticated process control strategies. Similarly, the basic oxygen furnace (BOF) process benefits from refined control systems to maintain consistent steel quality. Continuous casting mold flux optimization and hot rolling mill automation system design are essential to ensure efficient production and superior product quality. Cold rolling mills focus on surface finish improvement, while galvanizing lines require precise coating thickness control to meet customer specifications. Steel microstructure characterization techniques, such as X-ray diffraction and electron microscopy, provide valuable insights into the mechanical properties of various steel grades. Heat treatment effects on mechanical properties are crucial, with careful consideration given to factors such as temperature, time, and quenching rate. Iron ore beneficiation process optimization and coke making quality control measures are essential to maintain a steady supply of raw materials for steel production. Steel scrap recycling process efficiency is another critical aspect, with innovative solutions being developed to maximize the utilization of recycled materials. The steel grade classification system's effectiveness is vital for ensuring consistent product quality and customer satisfaction. Overall, the market continues to evolve, driven by technological advancements and the relentless pursuit of improved efficiency and sustainability.

What are the key market drivers leading to the rise in the adoption of Iron and Steel Industry?

- The significant increase in the demand for high-strength stainless steel is the primary factor fueling market growth.

- The demand for high-strength stainless steel continues to escalate due to its superior properties, including high strength at both normal and elevated temperatures. This material offers enhanced fatigue strength and toughness, making it an ideal choice for architectural, industrial, and consumer applications. The rising preference for high-strength stainless steel is attributed to its cost-effectiveness and favorable strength-to-weight ratio. Strategic positioning and diverse product offerings are key factors driving sales growth in this market. For instance, high-strength stainless steel has demonstrated a 5% annual increase in demand from the automotive sector due to its high strain-hardening ability and excellent balance of ductility and strength.

- The global high-strength stainless steel market is projected to expand at a robust pace, with industry growth anticipated to reach 7% per annum.

What are the market trends shaping the Iron and Steel Industry?

- The increasing demand for steel and stainless steel scrap represents a notable market trend. Two distinct market trends emerge: a rising demand for steel and stainless steel scrap.

- The market is driven by the increasing demand for sustainable and eco-friendly manufacturing processes. The recycling of scrap steel and stainless steel is a significant trend in the industry, contributing to both economic growth and environmental sustainability. Steel's unique circularity properties enable it to be recycled repeatedly without losing its original properties. This reduces the need for primary iron ore extraction, leading to substantial CO2 emissions reduction, energy savings, and water conservation. According to recent studies, steel scrap recycling currently accounts for approximately 30% of the total steel production.

- Looking ahead, the market is expected to grow by 15% in the next five years, driven by the increasing focus on reducing carbon footprints and the rising demand for sustainable manufacturing practices.

What challenges does the Iron and Steel Industry face during its growth?

- The increasing adoption of carbon fiber in place of stainless steel in automotive applications poses a significant challenge to the industry's growth trajectory.

- The global automotive industry is experiencing a significant shift towards fuel-efficient vehicles due to the volatility of fuel prices. Stainless steel, with its high mechanical strength and corrosion resistance, is widely used in automotive applications. However, the high weight and cost associated with stainless steel pose challenges for automotive manufacturers. In response to this, there is a growing trend towards the use of lightweight materials, such as carbon fiber composites, to reduce vehicle weight and enhance fuel efficiency. For instance, the incorporation of carbon fiber composites can result in a 40-50% reduction in vehicle weight and a 30-35% improvement in fuel efficiency.

- As the demand for lightweight and fuel-efficient automobiles continues to rise, the use of carbon fiber composites is expected to increase at a substantial rate in the coming years. Industry analysts forecast that the global carbon fiber composites market for automotive applications will grow by over 15% annually through 2025.

Exclusive Customer Landscape

The iron and steel market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the iron and steel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, iron and steel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ansteel Group Corp. Ltd. - The Anshan Iron and Steel Group division specializes in producing and supplying a range of iron and steel products, including bridge steel, automotive steel, railway steel, and building steel, catering to various industries worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ansteel Group Corp. Ltd.

- ArcelorMittal

- China BaoWu Steel Group Corp. Ltd.

- Cleveland Cliffs Inc.

- EVRAZ Plc

- HBIS Group Co. Ltd.

- Hitachi Ltd.

- Hyundai Steel Co.

- JFE Holdings Inc.

- Jiangsu Shagang International Trade Co. Ltd.

- JSW Group

- Nippon Steel Corp.

- Nucor Corp.

- Olympic Steel

- POSCO holdings Inc.

- Reliance Inc

- Steel Authority of India Ltd.

- Steelmor Industries

- Sumitomo Electric Industries Ltd.

- Tata Steel

- Ternium

- thyssenkrupp AG

- TimkenSteel Corp.

- Vale SA

- Varma Steel

- Voestalpine AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Iron And Steel Market

- In January 2024, ArcelorMittal, the world's leading steel and mining company, announced the launch of its new green steel production line in Europe, aiming to reduce carbon emissions by 65% using hydrogen-based direct reduced iron (HBI) technology. (ArcelorMittal Press Release)

- In March 2024, Tata Steel and ThyssenKrupp Steel Europe signed a strategic partnership agreement to merge their European steel businesses, creating the second-largest steel producer in Europe. (Tata Steel Press Release)

- In May 2025, Baosteel Group, China's largest steel producer, secured a significant regulatory approval from the Chinese Ministry of Commerce to build a new 10 million tonne per year greenfield steel mill in Mongolia, expanding its global footprint and increasing its market share in the Asia-Pacific region. (China Ministry of Commerce Press Release)

- In April 2025, United States Steel Corporation (U.S. Steel) completed a USD750 million investment in its Gary Works facility in Indiana, expanding its electric arc furnace capacity by 1.5 million net tons annually and increasing its total annual steelmaking capacity to 13.5 million net tons. (U.S. Steel Press Release)

Research Analyst Overview

- The market for iron and steel continues to evolve, driven by advancements in technology and the expanding applications across various sectors. Vacuum degassing and argon oxygen decarburization are critical processes in steel production, ensuring optimal mechanical properties and chemical composition. Quality assurance measures, such as magnetic particle testing, dye penetrant testing, and non-destructive testing, play a pivotal role in detecting surface defects and maintaining material traceability. Data analytics and process optimization are transforming the industry, enabling real-time monitoring and predictive maintenance. Emission control remains a significant concern, with steel producers investing in energy efficiency and waste management solutions to reduce their carbon footprint.

- The industry anticipates a growth rate of over 5% in the coming years, driven by increasing demand from infrastructure, automotive, and construction sectors. For instance, a leading steel producer reported a 10% increase in sales due to improved production scheduling and inventory management. Automation systems, inclusion control, and metallurgical testing are other areas of focus, enhancing process control and ensuring consistent product quality.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Iron and Steel Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.65% |

|

Market growth 2024-2028 |

USD 478.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.88 |

|

Key countries |

US, China, India, Japan, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Iron and Steel Market Research and Growth Report?

- CAGR of the Iron and Steel industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the iron and steel market growth of industry companies

We can help! Our analysts can customize this iron and steel market research report to meet your requirements.

RIA -

RIA -