Nordic Countries Information Technology (IT) Services Market Size 2026-2030

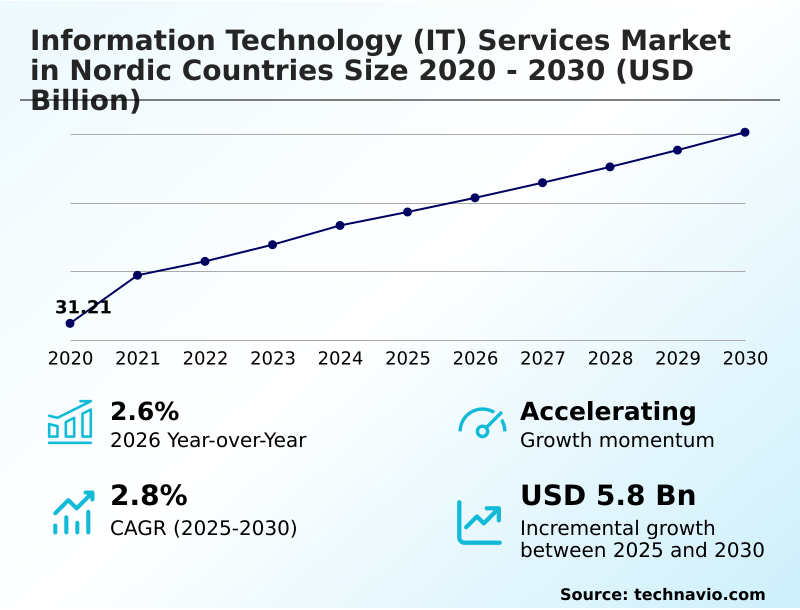

The nordic countries information technology (it) services market size is valued to increase by USD 5.80 billion, at a CAGR of 2.8% from 2025 to 2030. Standardization of National Defense Digitization and NATO infrastructure integration will drive the nordic countries information technology (it) services market.

Major Market Trends & Insights

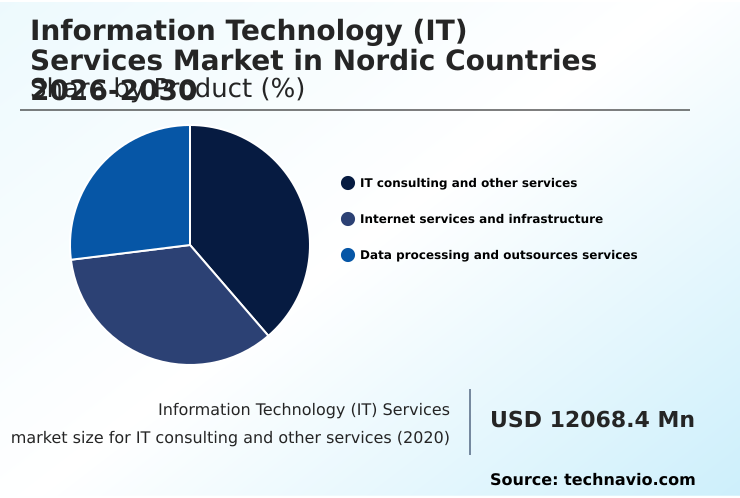

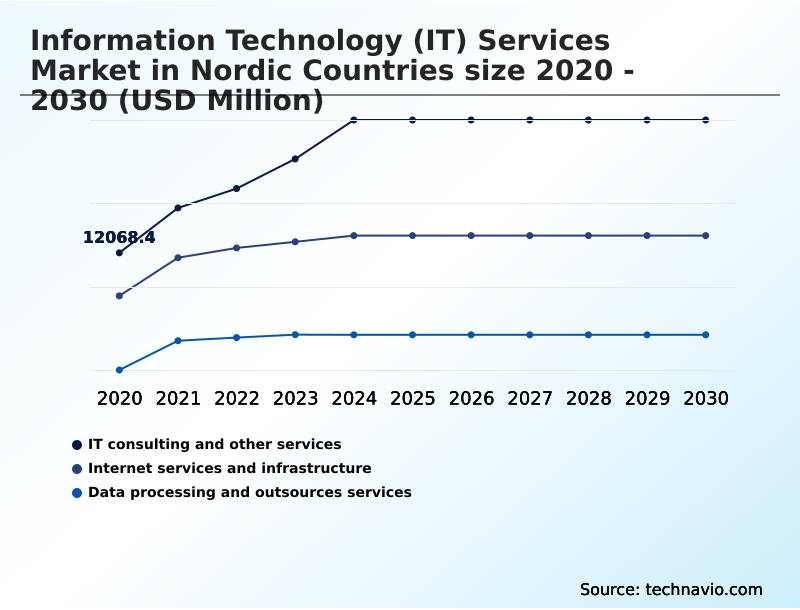

- By Product - IT consulting and other services segment was valued at USD 16.21 billion in 2024

- By Application - Technology and telecommunication segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 13.90 billion

- Market Future Opportunities: USD 5.80 billion

- CAGR from 2025 to 2030 : 2.8%

Market Summary

- The Information Technology (IT) Services Market in Nordic Countries is characterized by intensive structural modernization, with a decisive shift toward cloud-native architectures, edge computing, and the industrialization of artificial intelligence. This evolution is driven by high digital maturity and a systemic need for advanced automation to counter rising operational costs.

- Services have moved from basic infrastructure support to strategic partnerships that prioritize predictive analytics and cybersecurity within managed service frameworks. For example, a manufacturing firm can implement digital twin technologies, leveraging real-time data from industrial IoT devices to optimize production lines, predict maintenance needs, and reduce downtime.

- This data-centric approach is reinforced by stringent data sovereignty regulations, compelling the development of localized, high-security cloud solutions. However, the market's trajectory is tempered by a significant talent gap in specialized fields like data engineering and AI, creating a high-stakes environment where the ability to deliver secure, interoperable, and audit-grade services determines commercial success.

- The successful integration of human expertise with agentic AI ensures that IT services remain a cornerstone of the region's digital economy.

What will be the Size of the Nordic Countries Information Technology (IT) Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Nordic Countries Information Technology (IT) Services Market Segmented?

The nordic countries information technology (it) services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- IT consulting and other services

- Internet services and infrastructure

- Data processing and outsources services

- Application

- Technology and telecommunication

- BFSI

- Travel and hospitality

- Healthcare

- Others

- Deployment

- Cloud-based

- On-premises

- Geography

- Nordic Countries

By Product Insights

The it consulting and other services segment is estimated to witness significant growth during the forecast period.

The IT consulting and other services segment is pivotal, guiding organizations through complex digital transformation. Firms are moving beyond basic support to focus on high-value advisory for implementing cloud-native architectures and generative AI.

This involves optimizing enterprise resource planning systems and deploying business automation solutions. A key focus is on navigating digital governance and data sovereignty mandates, often requiring hybrid cloud models for compliance.

Despite high ambitions for AI integration, a skills gap persists, with fewer than 10% of knowledge workers feeling their AI literacy is sufficient.

Service providers are therefore crucial in enabling IT optimization services, automated data processing, and specialized solutions like real-time payment processing and predictive remediation to bridge this capability gap.

The IT consulting and other services segment was valued at USD 16.21 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of sovereign cloud solutions for financial services is a defining characteristic of the market, driven by intense regulatory pressure and the need for secure data environments. This has accelerated the adoption of agentic AI in IT service management, automating complex workflows and enabling proactive issue resolution.

- In parallel, edge computing for industrial automation is transforming manufacturing sectors, where real-time processing capabilities enhance efficiency and safety. The development of generative AI for linguistic models is addressing the unique language requirements of the Nordic region, creating a demand for specialized expertise.

- A key trend is the focus on sustainable data infrastructure for HPC, leveraging the region's climate and renewable energy resources. The broader push for digital transformation in public sector services is creating opportunities for providers that can navigate complex procurement and security requirements.

- Managed IT services for healthcare are evolving to support telehealth and electronic health record interoperability, while cybersecurity for critical infrastructure has become a boardroom-level priority.

- Organizations are employing a multi-cloud strategy for operational agility, supported by digital twin for manufacturing optimization and predictive analytics for supply chain improvements, which has led to inventory holding cost reductions of over 20% compared to traditional forecasting methods. This is enabled by network virtualization for 5G rollout and open banking API integration services.

- Further modernization is achieved through system integration for legacy modernization and digital engineering for software development, with cloud economics and cost optimization guiding investment in hyper-converged infrastructure on-premises and IT infrastructure consulting for SMEs.

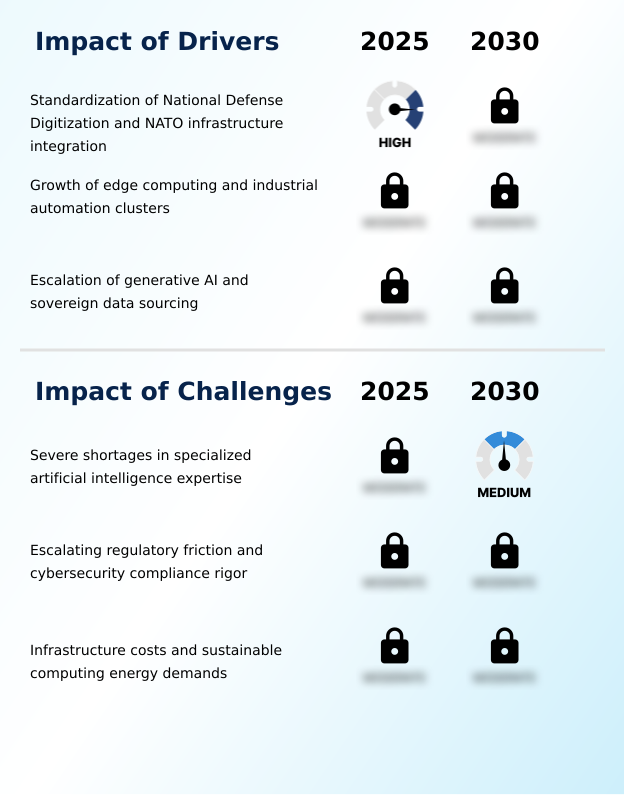

What are the key market drivers leading to the rise in the adoption of Nordic Countries Information Technology (IT) Services Industry?

- The standardization of national defense digitization and the integration of regional infrastructure into the NATO technological framework are key market drivers.

- Market growth is propelled by national defense digitization and NATO infrastructure integration, which mandates secure cross-border communication networks and boosts public sector investment in IT.

- This drive for sovereign data sourcing is paralleled by the growth of edge computing and industrial automation clusters, which improve manufacturing efficiency by up to 25%.

- IT service providers are delivering real-time analytics and advanced data engineering capabilities for high-performance computing workloads. This fuels demand for specialized application development and digital engineering services.

- System integration services are crucial for modernizing enterprise application services, ensuring interoperability and security across decentralized networks and cementing the region's leadership in high-value industrial digitalization.

What are the market trends shaping the Nordic Countries Information Technology (IT) Services Industry?

- A significant market trend is the development of sovereign cloud infrastructure, driven by the need to meet rigorous data privacy and national security requirements.

- The market is shaped by the industrialization of sovereign cloud infrastructure and the rise of agentic AI managed services. These trends enable self-healing environments, improving system uptime by over 20%. The emphasis on digital operational resilience drives adoption of Platform-as-a-Service (PaaS) and hyper-converged infrastructure to secure data within national jurisdictions.

- Simultaneously, sustainable data infrastructure and green computing are paramount, with green computing services leading to a 15% reduction in energy consumption in new data center deployments. This evolution impacts all sectors, from data processing services implementing network virtualization to healthcare integrating electronic health records and finance leveraging open banking frameworks for secure innovation.

What challenges does the Nordic Countries Information Technology (IT) Services Industry face during its growth?

- A primary challenge impacting industry growth is the severe shortage of specialized expertise, particularly in the domain of generative artificial intelligence.

- Key challenges include escalating regulatory friction and the complexities of cybersecurity compliance. Navigating disparate cybersecurity frameworks imposes significant administrative overhead on managed IT operations, with non-compliance penalties increasing operational risk by over 30%. Organizations adopting multi-cloud strategies for AI-native infrastructure face hurdles in ensuring supply chain resilience and secure workload migration.

- The rapid deployment of 5G networking and cellular IoT connectivity exposes new vulnerabilities, while local model training for Software-as-a-Service (SaaS) applications is hampered by high infrastructure costs and volatile supply chains. These issues can impede the establishment of seamless digital trade corridors, delaying technological integration as firms prioritize legal safety over innovation.

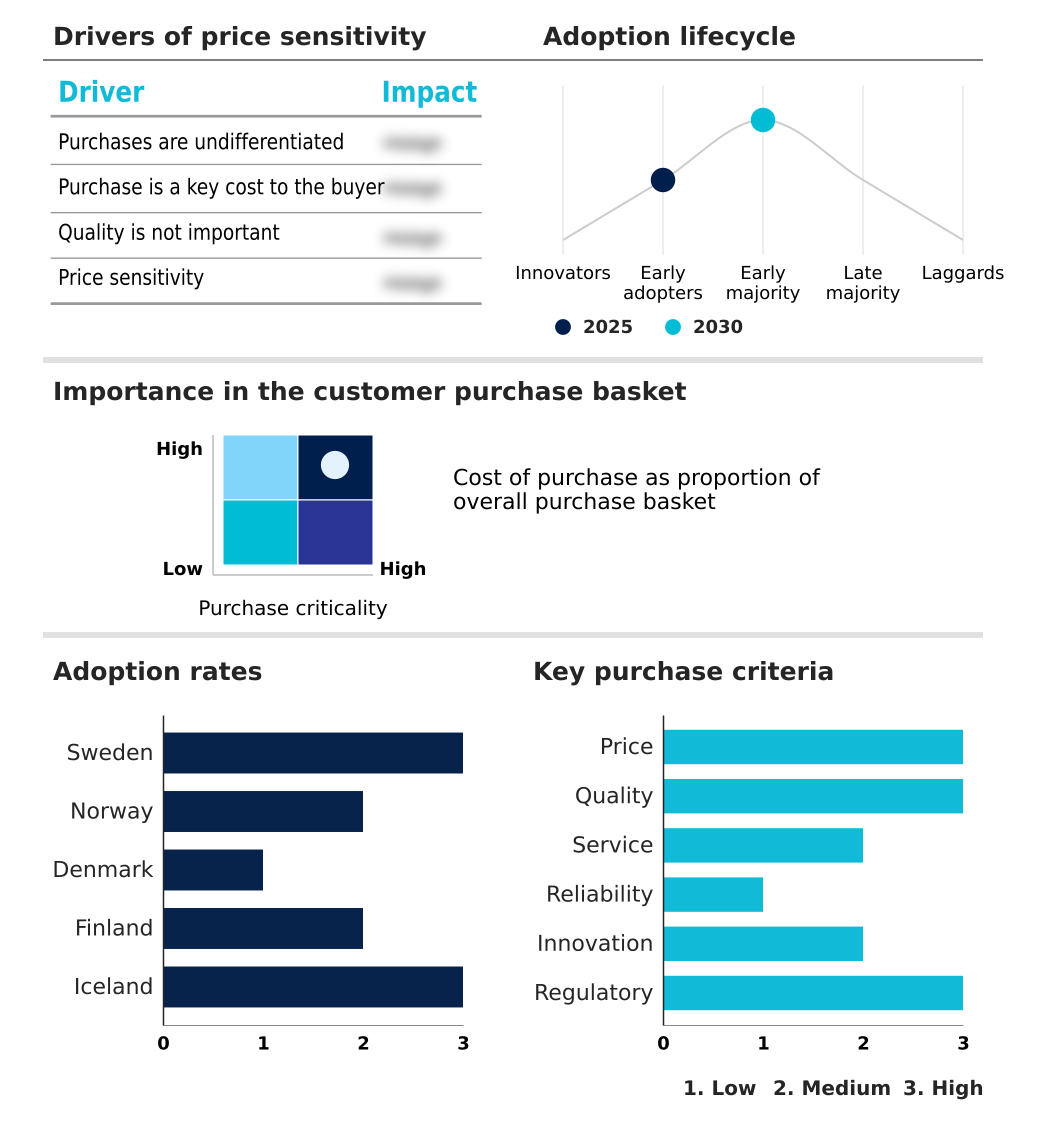

Exclusive Technavio Analysis on Customer Landscape

The nordic countries information technology (it) services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the nordic countries information technology (it) services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Nordic Countries Information Technology (IT) Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, nordic countries information technology (it) services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Offerings are centered on enabling enterprise digital transformation through integrated cloud, AI, and strategic consulting services designed to optimize business outcomes and ensure data sovereignty.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Advania Group

- Atea ASA

- Bouvet ASA

- Capgemini SE

- Crayon Group Holding ASA

- Digia Oyj

- Fujitsu Ltd.

- Hexaware Technologies Ltd.

- HiQ International AB

- IBM Corp.

- KMD

- Netcompany Group

- Nokia Corp.

- Siili Solutions Oyj

- Solita Oy

- Telefonaktiebolaget Ericsson

- Tietoevry Corp.

- Trifork

- Visma Solutions Oy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Nordic countries information technology (it) services market

- In April, 2025, CGI Inc. expanded its strategic partnership with SSAB to deliver business-critical IT services in Finland and Sweden, focusing on supply chain resilience and AI integration.

- In March, 2025, Tietoevry rebranded to Tieto Corporation, reflecting a renewed focus on specialized software and digital engineering powered by cloud and AI technologies.

- In February, 2025, Telenor Group's IoT Connect platform was highlighted for simplifying global managed connectivity for industrial sectors via a unified API and big data engine.

- In September, 2024, Tietoevry's tech services division began operating as the standalone entity Vivicta, aiming to provide more agile and tailored software solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Nordic Countries Information Technology (IT) Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 219 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.8% |

| Market growth 2026-2030 | USD 5801.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.6% |

| Key countries | Sweden, Norway, Denmark, Finland and Iceland |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a profound digital transformation, moving enterprises toward sophisticated cloud-native architectures and multi-cloud strategies. The integration of generative AI and real-time analytics is now foundational, driving demand for specialized IT infrastructure services and advanced data engineering.

- In this environment, managed IT operations are shifting to proactive models centered on cybersecurity frameworks and IT optimization services, with some firms achieving a 25% improvement in threat detection times. This evolution requires a blend of enterprise application services, system integration services, and custom application development.

- Digital engineering services are essential for building high-performance computing platforms and deploying enterprise resource planning systems that support data sovereignty. The adoption of platform-as-a-service and software-as-a-service models, governed by strict cloud economics, is accelerating. For boardroom consideration, the investment in agentic AI managed services is no longer optional but a strategic necessity for maintaining competitive agility.

- Key technologies including hyper-converged infrastructure, 5G networking, green computing, edge computing, digital twin technologies, predictive analytics, network virtualization, and open banking frameworks are all critical components. Ultimately, success hinges on effective data processing services and robust business automation solutions.

What are the Key Data Covered in this Nordic Countries Information Technology (IT) Services Market Research and Growth Report?

-

What is the expected growth of the Nordic Countries Information Technology (IT) Services Market between 2026 and 2030?

-

USD 5.80 billion, at a CAGR of 2.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (IT consulting and other services, Internet services and infrastructure, and Data processing and outsources services), Application (Technology and telecommunication, BFSI, Travel and hospitality, Healthcare, and Others), Deployment (Cloud-based, and On-premises) and Geography (Nordic Countries)

-

-

Which regions are analyzed in the report?

-

Nordic Countries

-

-

What are the key growth drivers and market challenges?

-

Standardization of National Defense Digitization and NATO infrastructure integration, Severe shortages in specialized artificial intelligence expertise

-

-

Who are the major players in the Nordic Countries Information Technology (IT) Services Market?

-

Accenture Plc, Advania Group, Atea ASA, Bouvet ASA, Capgemini SE, Crayon Group Holding ASA, Digia Oyj, Fujitsu Ltd., Hexaware Technologies Ltd., HiQ International AB, IBM Corp., KMD, Netcompany Group, Nokia Corp., Siili Solutions Oyj, Solita Oy, Telefonaktiebolaget Ericsson, Tietoevry Corp., Trifork and Visma Solutions Oy

-

Market Research Insights

- The market's dynamics are shaped by a pronounced disconnect between digital ambition and workforce readiness. While four out of five professionals expect AI to transform their work, fewer than one in ten feel equipped with the necessary skills, creating a demand for services that bridge this gap. This environment drives the need for national defense digitization and digital operational resilience.

- Enterprises are increasingly adopting self-healing environments to automate IT functions, with some achieving a 40% reduction in manual interventions. The focus on sustainable data infrastructure and green computing services aligns with regional sustainability goals.

- As organizations navigate this landscape, there is a growing reliance on external partners to manage regulatory friction, ensure cybersecurity compliance, and implement sovereign data sourcing models, solidifying the role of IT services as essential enablers of secure and efficient digital transformation.

We can help! Our analysts can customize this nordic countries information technology (it) services market research report to meet your requirements.

RIA -

RIA -