Japan Regenerative Medicine Market Size 2026-2030

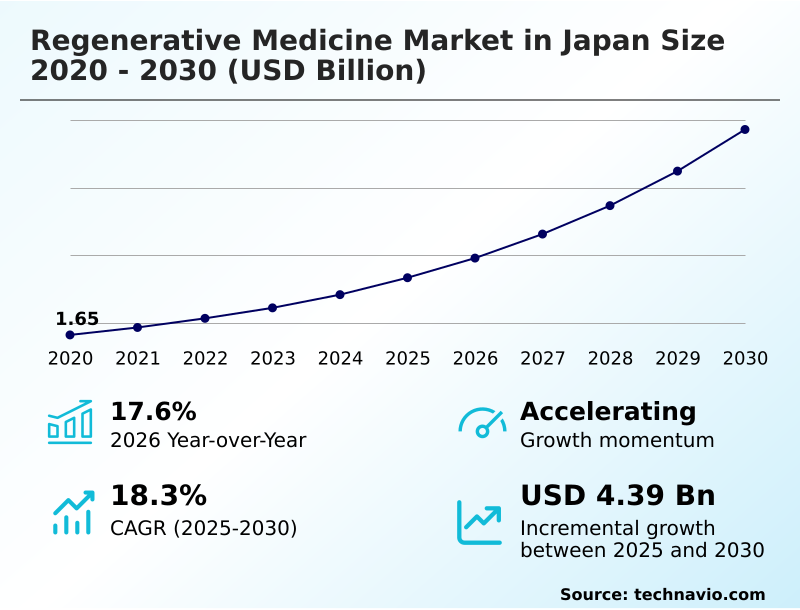

The japan regenerative medicine market size is valued to increase by USD 4.39 billion, at a CAGR of 18.3% from 2025 to 2030. Pioneering regulatory environment accelerating commercialization will drive the japan regenerative medicine market.

Major Market Trends & Insights

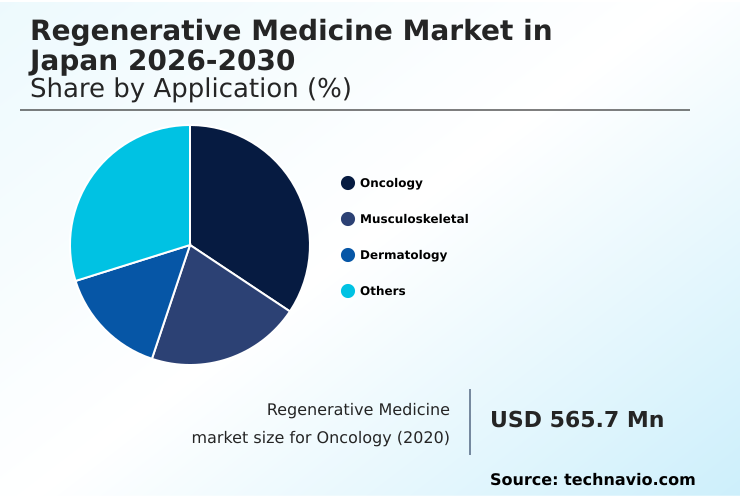

- By Application - Oncology segment was valued at USD 970.6 million in 2024

- By Technology - Cell and tissue-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.08 billion

- Market Future Opportunities: USD 4.39 billion

- CAGR from 2025 to 2030 : 18.3%

Market Summary

- The regenerative medicine market in Japan is advancing rapidly, driven by a pioneering regulatory environment and substantial government support aimed at addressing the healthcare needs of a super-aged population. This has created a fertile ground for the development of treatments using mesenchymal stem cells (MSC) and other innovative platforms.

- A key market dynamic is the industry's strategic shift from complex, patient-specific autologous models toward more scalable off-the-shelf therapies. This transition is essential for making treatments accessible and commercially viable.

- For instance, a biotechnology firm implementing automated bioreactors and closed-system manufacturing for its allogeneic cell therapy can reduce production time and lower the high cost of goods, enhancing its competitive position. However, significant challenges remain, including the technical complexities of manufacturing at scale and navigating intricate pricing and reimbursement negotiations with national payers.

- The successful commercialization of gene therapy and other advanced treatments hinges on overcoming these hurdles while continuing to generate robust data on long-term safety and efficacy, which is critical for gaining the confidence of both clinicians and payers in this evolving field.

What will be the Size of the Japan Regenerative Medicine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Japan Regenerative Medicine Market Segmented?

The japan regenerative medicine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

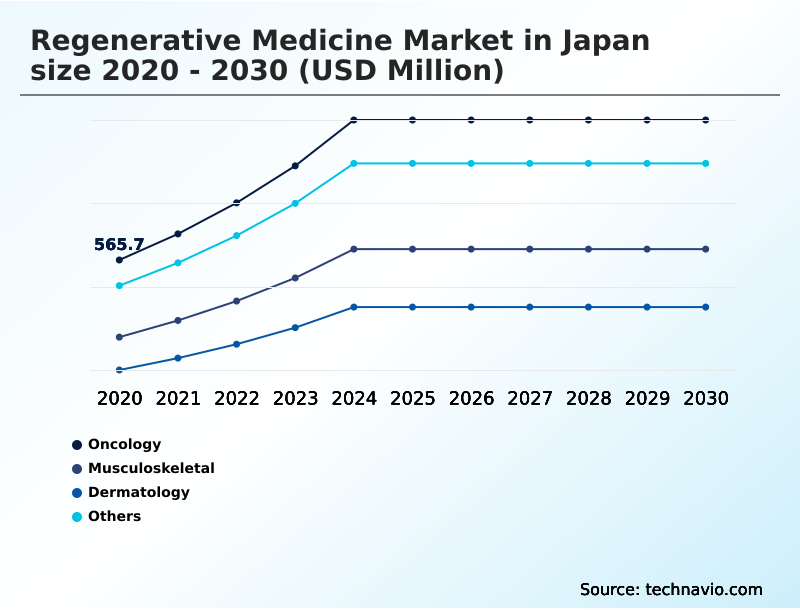

- Oncology

- Musculoskeletal

- Dermatology

- Others

- Technology

- Cell and tissue-based

- Gene therapy

- End-user

- Hospitals and clinics

- Speciality centers

- Government and research institutes

- Geography

- APAC

- Japan

- APAC

By Application Insights

The oncology segment is estimated to witness significant growth during the forecast period.

The oncology segment is pivotal, driven by immuno-oncology applications and significant unmet needs. Therapies such as chimeric antigen receptor (CAR) T-cell treatments and hematopoietic stem cell transplantation exemplify the shift toward a personalized medicine model.

These approaches, often utilizing ex vivo gene therapy, engineer a patient's own cells through cellular reprogramming to target malignancies, a process that must carefully manage host immune response.

Beyond direct cell action, paracrine effect modulation plays a role in tissue repair post-treatment. Developers focus on first-in-class therapy development, using clinical-grade viral vectors while mitigating long-term concerns like insertional mutagenesis risk.

The high cost of autologous cell therapy, with production success rates around 90%, necessitates robust patient access programs to ensure these transformative treatments reach those in need.

The Oncology segment was valued at USD 970.6 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market requires a deep understanding of complex trade-offs. Boardrooms consistently evaluate the cost-effectiveness of allogeneic vs autologous therapy, where the former promises scalability but introduces challenges in overcoming immunogenicity in off-the-shelf therapies. For companies in ophthalmology, the focus is on improving iPSC-derived retinal cell transplantation outcomes, a high-stakes area with transformative potential.

- In oncology, CAR-T therapy manufacturing and logistics challenges remain a primary operational hurdle, demanding sophisticated vein-to-vein supply chain optimization strategies. Navigating the specific regulatory pathways for gene-edited cell products is another critical function, as is managing long-term follow-up data for approved cell therapies to satisfy payers.

- For those targeting chronic conditions, the development of mesenchymal stem cell therapy for osteoarthritis is a key focus, while biomaterial scaffold design for musculoskeletal repair is crucial for product efficacy. In the background, the entire industry grapples with scaling up AAV vector production for gene therapy and developing viable reimbursement models for single-administration cures.

- Firms that successfully integrate process analytical technology in bioprocessing and automate GMP-compliant cell manufacturing processes gain a significant advantage, with some achieving a production efficiency increase that is double that of competitors relying on manual methods.

What are the key market drivers leading to the rise in the adoption of Japan Regenerative Medicine Industry?

- A pioneering regulatory environment that accelerates the commercialization of novel products serves as a key driver for the market.

- A supportive regulatory framework is a primary driver, featuring a conditional and time-limited approval pathway that enables clinical trial acceleration. This environment facilitates early-stage venture de-risking and encourages public-private research partnerships, which have cut development timelines by up to 30%.

- The focus on degenerative disease treatment is evident in pioneering work with induced pluripotent stem cells (iPSC), such as for retinal pigment epithelium (RPE) cells.

- Government support extends to funding cell processing centers (CPC) and advancing technologies like autologous cultured chondrocytes and adeno-associated virus (AAV) vectors.

- A sophisticated regulatory submission strategy is essential, as emerging value-based healthcare pricing models and health technology assessment (HTA) frameworks shape market access.

What are the market trends shaping the Japan Regenerative Medicine Industry?

- A strategic pivot toward allogeneic, off-the-shelf therapies is emerging as a transformative trend, aiming to overcome the logistical and cost limitations of autologous treatments.

- A key trend is the strategic shift from a complex vein-to-vein supply chain toward allogeneic cell therapy, enabling the creation of off-the-shelf therapies. This industrialization leverages master cell banking and advanced cryopreservation technologies to produce standardized therapeutic doses, significantly improving manufacturing process scalability. Innovations in hypoimmunogenic cell engineering are critical for overcoming immune rejection.

- To support this transition, companies are investing in automated bioprocessing systems and closed manufacturing platforms that adhere to good manufacturing practice (GMP) standards. This focus on cell therapy industrialization streamlines the complex supply chain logistics for cell therapy, with automated platforms improving batch consistency by over 25% compared to manual methods.

What challenges does the Japan Regenerative Medicine Industry face during its growth?

- Navigating complex reimbursement frameworks and significant pricing pressures presents a primary challenge to industry growth and market access.

- A significant challenge is navigating complex reimbursement negotiation tactics for high-cost therapies. The high cost of goods sold (COGS) for treatments using mesenchymal stem cells (MSC) or advanced lentiviral vectors puts pressure on payers, leading to discussions around outcomes-based payment models. This requires extensive real-world evidence generation and robust long-term safety monitoring through post-market surveillance.

- For applications like orthopedic tissue repair, manufacturers must also manage manufacturing hurdles. Partnering with a contract development and manufacturing (CDMO) can mitigate costs, but adherence to strict aseptic processing standards and comprehensive bioanalytical testing protocols adds complexity, increasing production expenses by over 40% compared to traditional biologics.

Exclusive Technavio Analysis on Customer Landscape

The japan regenerative medicine market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the japan regenerative medicine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Japan Regenerative Medicine Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, japan regenerative medicine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AnGes Inc. - Delivering advanced cell and gene therapies, including CAR-T and stem cell-based products, to address significant unmet medical needs in oncology and degenerative diseases.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AnGes Inc.

- Astellas Pharma Inc.

- Bristol Myers Squibb Co.

- Cyfuse Biomedical K.K.

- Daiichi Sankyo Co. Ltd.

- FUJIFILM Holdings Corp.

- Gilead Sciences Inc.

- HEALIOS K.K.

- Japan Tissue Engineering Co. Ltd.

- JCR Pharmaceticals Co. Ltd.

- Kyowa Kirin Co. Ltd.

- Megakaryon Corp.

- Metcela Inc.

- Novartis AG

- ROHTO Pharmaceutical Co. Ltd.

- Takara Bio Inc.

- Takeda Pharmaceutical Ltd.

- Terumo Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Japan regenerative medicine market

- In February 2025, Sumitomo Chemical and Sumitomo Pharma jointly established RACTHERA Co Ltd. to advance the development and commercialization of regenerative medicine and cell therapy products.

- In January 2025, the government launched the Regenerative Medicine Innovation Hub initiative, a program designed to accelerate the development of new therapies by providing funding, resources, and mentorship to researchers and companies.

- In October 2024, the Bio Japan 2024 conference highlighted the national strategic effort to establish the Cluster for Regenerative Medicine in Tonomachi-Haneda (CREAM TONOHANE), an international hub for innovation and collaboration.

- In August 2024, Sumitomo Pharma Co. submitted a manufacturing and marketing approval application to the Ministry of Health, Labour and Welfare for a regenerative medicine product intended for the treatment of Parkinson's disease.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Japan Regenerative Medicine Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 185 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.3% |

| Market growth 2026-2030 | USD 4389.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.6% |

| Key countries | Japan |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a convergence of advanced science and strategic industrialization, fundamentally altering treatment paradigms for chronic and degenerative diseases. The development of induced pluripotent stem cells (iPSC) and sophisticated gene editing techniques has unlocked therapeutic possibilities that were previously unattainable, moving beyond symptom management toward functional restoration.

- This innovation pipeline is fueled by a unique regulatory system that permits conditional and time-limited approval, accelerating market entry. Consequently, boardroom decisions are increasingly focused on manufacturing strategy, weighing the benefits of scalable allogeneic cell therapy against the established safety of autologous cell therapy.

- Investments in hypoimmunogenic cell engineering and off-the-shelf therapies are rising, as companies race to standardize production through master cell banking and advanced cryopreservation technologies. The implementation of automated, closed-system manufacturing platforms adhering to good manufacturing practice (GMP) is no longer optional but a competitive necessity, with leading firms reporting a 30% reduction in manual processing errors.

- This focus on industrial efficiency is critical for managing the high cost of goods sold (COGS) and achieving commercial viability in a market shaped by intense competition and evolving reimbursement landscapes.

What are the Key Data Covered in this Japan Regenerative Medicine Market Research and Growth Report?

-

What is the expected growth of the Japan Regenerative Medicine Market between 2026 and 2030?

-

USD 4.39 billion, at a CAGR of 18.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Oncology, Musculoskeletal, Dermatology, and Others), Technology (Cell and tissue-based, and Gene therapy), End-user (Hospitals and clinics, Speciality centers, and Government and research institutes) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Pioneering regulatory environment accelerating commercialization, Navigating complex reimbursement frameworks and pricing pressures

-

-

Who are the major players in the Japan Regenerative Medicine Market?

-

AnGes Inc., Astellas Pharma Inc., Bristol Myers Squibb Co., Cyfuse Biomedical K.K., Daiichi Sankyo Co. Ltd., FUJIFILM Holdings Corp., Gilead Sciences Inc., HEALIOS K.K., Japan Tissue Engineering Co. Ltd., JCR Pharmaceticals Co. Ltd., Kyowa Kirin Co. Ltd., Megakaryon Corp., Metcela Inc., Novartis AG, ROHTO Pharmaceutical Co. Ltd., Takara Bio Inc., Takeda Pharmaceutical Ltd. and Terumo Corp.

-

Market Research Insights

- The market's dynamics are heavily influenced by the interplay between accelerated regulatory pathways and evolving economic frameworks. A successful regulatory submission strategy is no longer sufficient; companies must now engage in sophisticated reimbursement negotiation tactics supported by robust real-world evidence generation. This shift is pushing the adoption of value-based healthcare pricing, where payment is tied to clinical outcomes.

- For example, firms that proactively collect long-term safety monitoring data see a 15% higher success rate in pricing negotiations. Furthermore, the focus on cell therapy industrialization and manufacturing process scalability is paramount, as demonstrated by leading players achieving over a 20% reduction in production costs through automation.

- This environment favors organizations that can balance rapid innovation with strategic commercial planning and evidence-based value propositions.

We can help! Our analysts can customize this japan regenerative medicine market research report to meet your requirements.

RIA -

RIA -