K-12 Blended E-learning Market Size 2026-2030

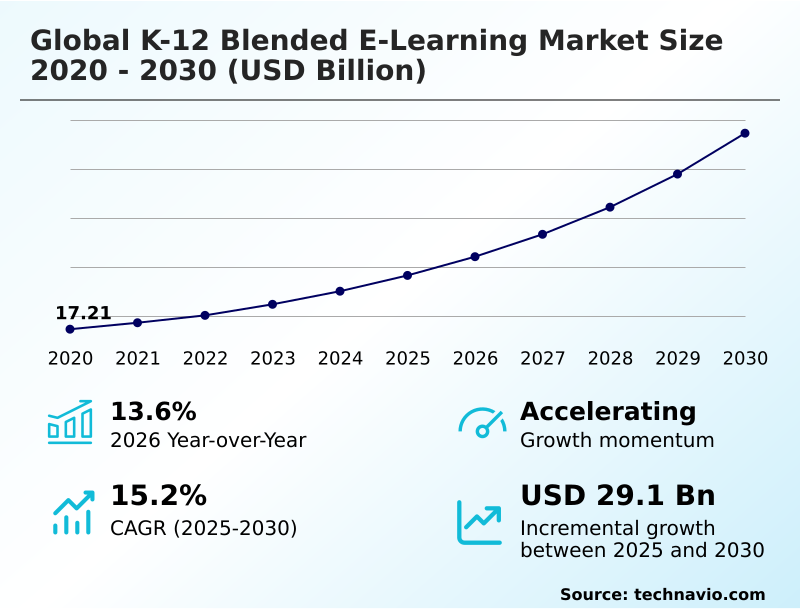

The k-12 blended e-learning market size is valued to increase by USD 29.10 billion, at a CAGR of 15.2% from 2025 to 2030. Adoption of AI for adaptive learning pathway will drive the k-12 blended e-learning market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.6% growth during the forecast period.

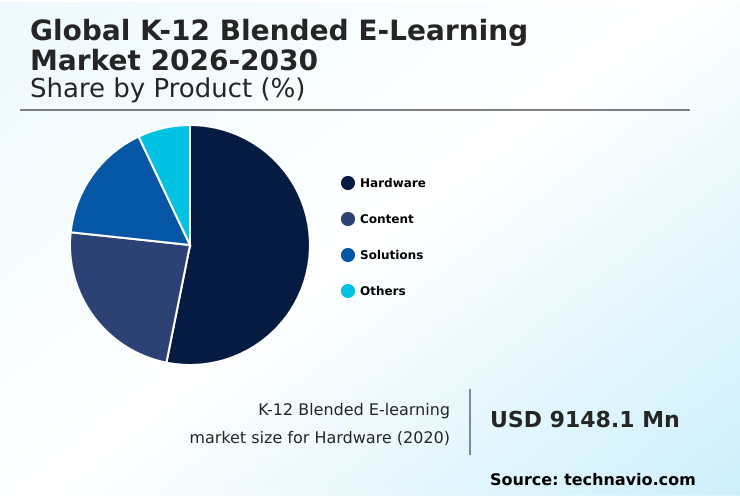

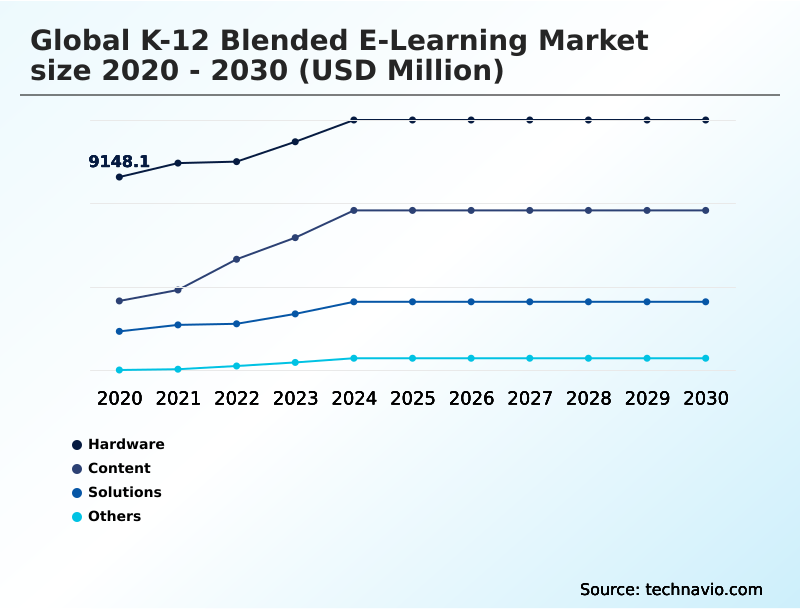

- By Product - Hardware segment was valued at USD 11.49 billion in 2024

- By Application - Pre-primary school segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 40.09 billion

- Market Future Opportunities: USD 29.10 billion

- CAGR from 2025 to 2030 : 15.2%

Market Summary

- The K-12 blended e-learning market is defined by its integration of digital platforms with traditional instruction, creating a more personalized and flexible educational environment. This evolution is driven by the need for data-driven instruction and curriculum alignment, which are facilitated by advanced machine learning algorithms.

- A key trend is the use of a mobile-first learning strategy and interactive educational tools to increase student engagement. As a result, educational institutions are shifting from static content to dynamic systems that offer a real-time feedback mechanism and support a hybrid classroom model.

- For instance, a school district can utilize a learning management system (LMS) to analyze student performance data, identify learning gaps in real-time, and reallocate tutoring resources to specific student groups. This approach improves outcomes and optimizes budgets without requiring additional staff, demonstrating the practical application of evidence-based digital pedagogy.

- However, this transition requires robust educator professional development and a focus on digital citizenship education to ensure effective and secure implementation.

What will be the Size of the K-12 Blended E-learning Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the K-12 Blended E-learning Market Segmented?

The k-12 blended e-learning industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Hardware

- Content

- Solutions

- Others

- Application

- Pre-primary school

- Primary school

- Middle school

- High school

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Product Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is foundational to the K-12 blended e-learning market, enabling the shift to digital instruction. This includes devices that support a bring-your-own-device (BYOD) framework and run sophisticated K-12 e-learning software and interactive educational tools.

The focus is on facilitating a hybrid learning model where students engage with an adaptive curriculum program through a cloud-based learning platform.

Modern devices are essential for delivering content via a personalized learning dashboard and supporting AI-powered formative assessment with a real-time feedback mechanism.

An effective educational technology platform depends on hardware that can support a mobile-first learning strategy and virtual classroom solution.

The contribution of these solutions to buyer budgets is high, influencing procurement decisions that prioritize system compatibility and functionality over premium specifications.

The Hardware segment was valued at USD 11.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

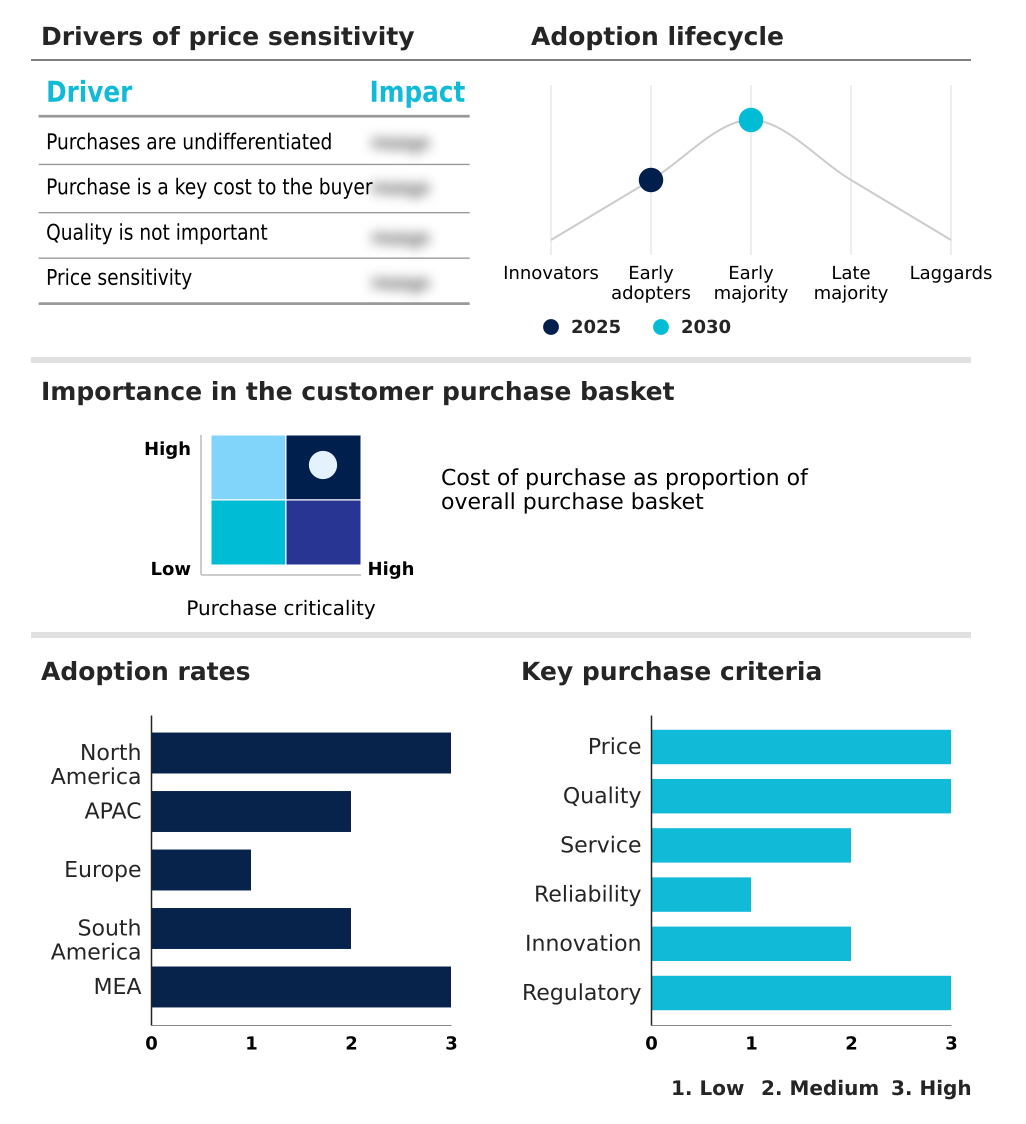

APAC is estimated to contribute 33.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How K-12 Blended E-learning Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the K-12 blended e-learning market is marked by a contrast between mature and high-growth regions. North America leads in market size, leveraging established edtech infrastructure to deploy sophisticated adaptive learning platforms and promote evidence-based digital pedagogy.

This region emphasizes curriculum alignment and the use of formative assessment tools. In contrast, APAC is the fastest-growing region, projected to contribute 33.6% of the market's incremental growth, significantly outpacing Europe's 23.77%.

This expansion is driven by government initiatives focused on digital citizenship education and the widespread adoption of gamified educational content to create an immersive learning experience.

AI in education is being used to develop personalized learning paths and digital portfolio management tools, with a strong focus on curriculum content creation that reflects regional needs.

Market Dynamics

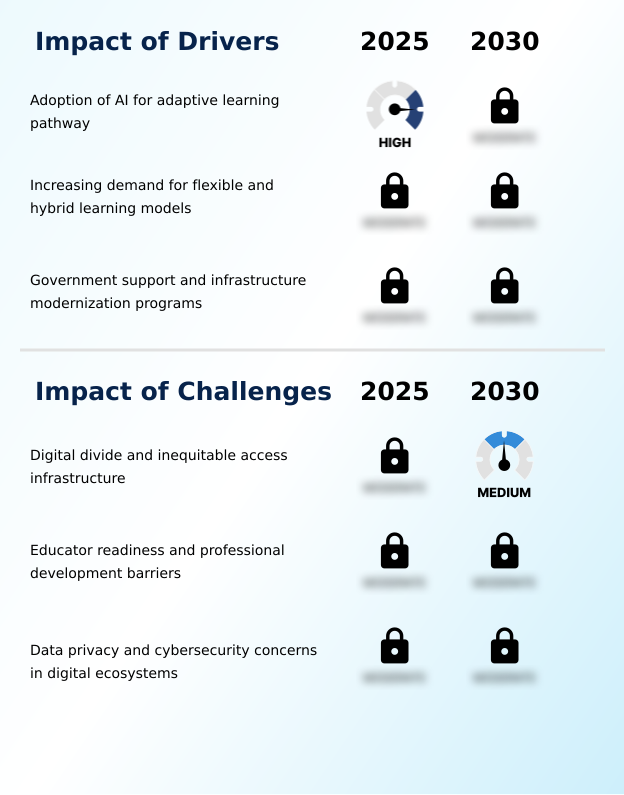

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of K-12 blended e-learning is increasingly nuanced, focusing on specific applications and outcomes. The use of AI for creating adaptive learning paths is becoming standard, personalizing instruction based on real-time student data. Simultaneously, the impact of BYOD policies on K-12 e-learning is forcing institutions to refine their security protocols for K-12 cloud platforms.

- In classrooms, educators are exploring gamification techniques for middle school math and integrating AR/VR in high school science labs to make learning more engaging. A key operational debate involves comparing cloud-based vs. on-premise LMS solutions, a decision influenced by strategies for bridging the digital divide in areas with poor connectivity.

- Deploying mobile-first learning in rural schools addresses access, while ensuring data privacy in student information systems remains a top priority. Best practices for teacher professional development are critical to address the challenges of educator readiness for edtech and to effectively use AI-powered formative assessment tools.

- The benefits of project-based digital learning are clear, but success depends on measuring student engagement in virtual classrooms and implementing a strong digital citizenship curriculum. The focus is shifting toward using AI for personalized student feedback and creating verifiable digital credentials for students to demonstrate competencies. This highlights the varying effectiveness of synchronous vs.

- asynchronous learning models, with growth in the APAC region contributing over 33% to market expansion, compared to just under 24% from Europe, indicating differing regional priorities and adoption rates.

What are the key market drivers leading to the rise in the adoption of K-12 Blended E-learning Industry?

- The adoption of artificial intelligence to enable adaptive learning pathways is a primary driver for the K-12 blended e-learning market.

- Market growth is primarily driven by the demand for flexible, technology-enabled education. The adoption of the hybrid classroom model, which blends synchronous learning with asynchronous learning, is now standard.

- This is supported by a unified cloud interface and collaborative software tools that facilitate a blended instructional approach and digital literacy development.

- Governments are accelerating this shift with investments in edtech infrastructure, with initiatives in India alone upgrading over 10,000 schools for digital readiness.

- Furthermore, with over 80% of educational organizations using AI, the demand for AI-driven tutoring systems and gamification in education is rising.

- These tools are often delivered through a mobile learning application, integrating social-emotional learning tools to enhance the student experience and provide a verifiable digital credential for skills acquired.

What are the market trends shaping the K-12 Blended E-learning Industry?

- The increasing adoption of mobile-first learning strategies and bring-your-own-device (BYOD) frameworks represents a significant trend shaping the K-12 blended e-learning landscape.

- Key market trends are redefining instructional delivery through advanced technology. The integration of a virtual reality learning environment and augmented reality education is creating a more immersive learning experience, supported by a flexible learning structure. This is coupled with the expansion of digital credentialing services, which provide verifiable digital credentials for student achievements.

- Success in this area relies on sophisticated student progress tracking and the use of a machine learning algorithm for data-driven instruction. However, these trends place greater demands on digital curriculum integration and the need for robust cybersecurity for schools to protect student data privacy.

- As a result, comprehensive teacher training programs are essential for effective implementation, as nearly half of educators report having no formal training in advanced AI tools, while institutions face a 92% rise in ransomware attacks.

What challenges does the K-12 Blended E-learning Industry face during its growth?

- The digital divide, characterized by inequitable access to infrastructure and resources, poses a significant challenge to industry growth.

- Significant challenges constrain the market's potential, primarily centered on access, readiness, and security. The digital divide prevents equitable digital content delivery, limiting the effectiveness of self-paced learning modules and interactive simulations.

- This is compounded by a lack of educator professional development, where nearly half of teachers lack formal training, hindering the use of student information system (SIS) data for blended learning analytics or to manage project-based digital learning. Consequently, institutions struggle to leverage a learning analytics dashboard for real-time student monitoring.

- Security is a major concern, with ransomware attacks on K-12 institutions increasing by 92%. This threat complicates online program management and the use of cloud-based educational services, making the protection of a secure digital portfolio a critical but difficult operational requirement.

Exclusive Technavio Analysis on Customer Landscape

The k-12 blended e-learning market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the k-12 blended e-learning market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of K-12 Blended E-learning Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, k-12 blended e-learning market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amplify Education Inc. - Analysis indicates a focus on adaptive digital curricula and integrated assessment tools that personalize learning pathways across core K-12 subjects, enhancing instructional efficacy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amplify Education Inc.

- BrainPOP

- Curriculum Associates LLC

- D2L Corp.

- DreamBox Learning Inc.

- Edmentum Inc.

- Google LLC

- Imagine Learning LLC

- Instructure Holdings Inc.

- IXL Learning Inc.

- Khan Academy Inc.

- McGraw Hill LLC

- Microsoft Corp.

- Nearpod Inc.

- Newsela

- Pearson Plc

- PowerSchool Holdings Inc.

- Renaissance Learning Inc

- Savvas Learning Co. LLC

- Stride Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in K-12 blended e-learning market

- In November, 2024, the Government of India reported that its PM SHRI program had successfully upgraded over ten thousand schools into model institutions equipped with smart infrastructure and digital classrooms to support the National Education Policy.

- In January, 2025, the State Educational Technology Directors Association released a report identifying a persistent digital use divide in the United States, highlighting that qualitative engagement with technology varies significantly by socioeconomic background even when device access is available.

- In February, 2025, the Government of Brazil reported a significant expansion of its digital education programs, which aim to provide tablets and high-speed internet to thousands of public schools, supporting blended learning models in remote areas.

- In May, 2025, the Ministry of Education in the United Arab Emirates announced a new partnership to integrate advanced artificial intelligence coaching into the national curriculum, providing students with personalized digital tutors.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled K-12 Blended E-learning Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.2% |

| Market growth 2026-2030 | USD 29095.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.6% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The K-12 blended e-learning market is evolving through the integration of sophisticated technologies aimed at personalizing education. A core component is the adaptive learning platform, which uses a machine learning algorithm for data-driven instruction and curriculum alignment. These systems, often part of a cloud-based learning platform, feature a personalized learning dashboard and a real-time feedback mechanism.

- The push toward a hybrid classroom model is supported by a bring-your-own-device (BYOD) framework and a mobile-first learning strategy, which necessitate robust digital curriculum integration. Interactive educational tools, including gamified educational content and interactive simulations, are central to this shift. The market is also seeing the rise of the virtual reality learning environment and augmented reality education.

- Key solutions include the learning management system (LMS), student information system (SIS), and collaborative software tools that support both synchronous learning and asynchronous learning. This blended instructional approach increasingly incorporates project-based digital learning and digital citizenship education.

- However, the effectiveness of these systems is constrained by workforce readiness, with nearly half of educators lacking formal training in AI-powered formative assessment tools, a critical gap for strategic planning and budgeting.

What are the Key Data Covered in this K-12 Blended E-learning Market Research and Growth Report?

-

What is the expected growth of the K-12 Blended E-learning Market between 2026 and 2030?

-

USD 29.10 billion, at a CAGR of 15.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hardware, Content, Solutions, and Others), Application (Pre-primary school, Primary school, Middle school, and High school), Deployment (Cloud-based, and On-premises) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Adoption of AI for adaptive learning pathway, Digital divide and inequitable access infrastructure

-

-

Who are the major players in the K-12 Blended E-learning Market?

-

Amplify Education Inc., BrainPOP, Curriculum Associates LLC, D2L Corp., DreamBox Learning Inc., Edmentum Inc., Google LLC, Imagine Learning LLC, Instructure Holdings Inc., IXL Learning Inc., Khan Academy Inc., McGraw Hill LLC, Microsoft Corp., Nearpod Inc., Newsela, Pearson Plc, PowerSchool Holdings Inc., Renaissance Learning Inc, Savvas Learning Co. LLC and Stride Inc.

-

Market Research Insights

- The market dynamics for K-12 blended e-learning are shaped by rapid technological adoption clashing with operational realities. While over 80% of educational organizations now use generative artificial intelligence and AI-driven tutoring systems, nearly half of all educators report receiving no formal teacher training program on these tools.

- This gap creates significant challenges in implementing a flexible learning structure and leveraging a learning analytics dashboard effectively. Furthermore, as schools adopt a hybrid learning model and increase digital content delivery, they become more vulnerable to cyber threats, with K-12 institutions seeing a 92% increase in ransomware attacks.

- This necessitates a greater focus on cybersecurity for schools and clear policies for student data privacy, complicating the rollout of any new educational technology platform or mobile learning application.

We can help! Our analysts can customize this k-12 blended e-learning market research report to meet your requirements.

RIA -

RIA -