China K-12 Online Education Market Size 2025-2029

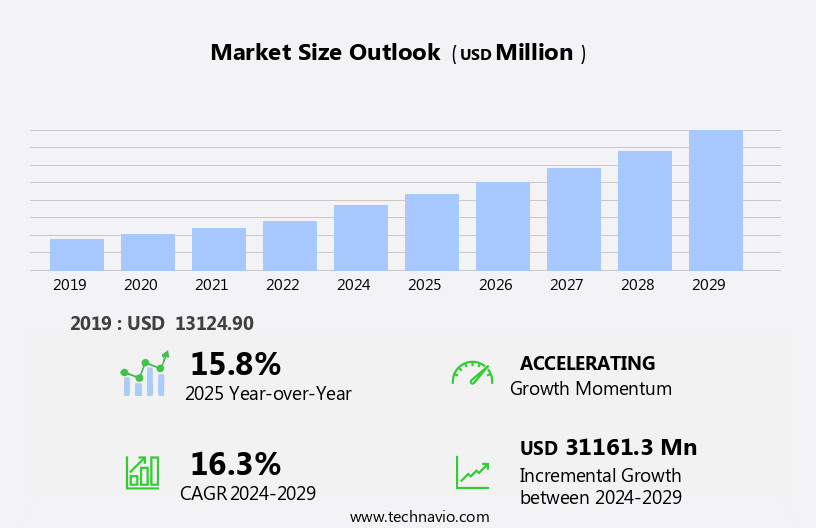

The China K-12 online education market size is forecast to increase by USD 31.16 billion, at a CAGR of 16.3% between 2024 and 2029.

- The K-12 online education market is experiencing significant growth, driven by the increasing adoption of online test preparation courses in China. This trend is a response to the country's competitive academic landscape and the convenience and accessibility that digital learning platforms offer. Additionally, the market is witnessing a growing demand for customized online education services, catering to the unique learning needs of individual students. However, this market also faces challenges, most notably the skewed interaction and socializing opportunities for students in a purely online environment.

- This lack of face-to-face interaction may hinder the development of essential social skills and limit the overall effectiveness of online education. To capitalize on the market's opportunities, companies must focus on delivering personalized, high-quality content and engaging, interactive learning experiences. Navigating the challenges will require innovative solutions to foster socialization and interaction among students, ensuring a well-rounded educational experience. The start-up ecosystem thrives, with educational content marketplaces offering a wealth of resources for teachers and students.

What will be the size of the China K-12 Online Education Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The K-12 online education market is witnessing significant advancements, driven by the integration of technology into classroom instruction and global education initiatives. Teacher collaboration platforms facilitate effective communication and coordination among educators, enhancing the quality of instruction. Learning games and personalized learning recommendations cater to individual student needs, while adaptive assessment and summative assessment tools provide valuable insights into student progress. Educational data standards ensure interoperability and data security, enabling seamless information exchange between systems. Special education technology and STEM education are gaining prominence, addressing the unique needs of diverse learners and fostering scientific literacy. Skill-based learning and interactive content delivery engage students and promote active participation.

- Formative assessment offers real-time feedback to educators, allowing for timely intervention and adjustments. Early childhood education also benefits from online platforms, providing access to high-quality instruction and resources. Personalized feedback and educational video conferencing enable effective communication between teachers and students, bridging the gap in remote learning environments. Learning outcomes alignment ensures consistency and effectiveness in instruction, while adaptive assessment and summative assessment tools provide valuable insights into student progress. The integration of these technologies and initiatives is transforming the K-12 education landscape, offering new opportunities for innovation and growth.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

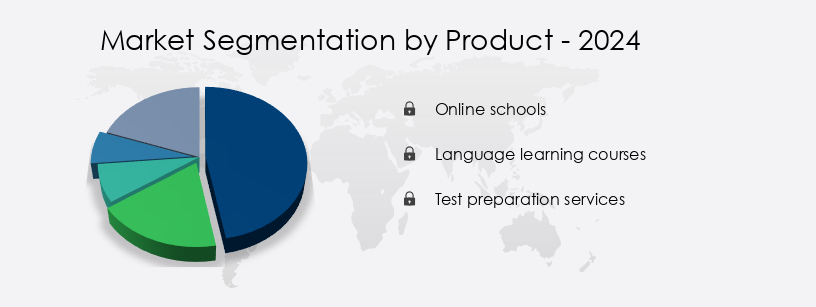

- Product

- Online schools

- Language learning courses

- Test preparation services

- End-user

- Institutional learners

- Individual learners

- Type

- Assessments

- Subjects

- Geography

- APAC

- China

- APAC

By Product Insights

The online schools segment is estimated to witness significant growth during the forecast period. The market is witnessing significant growth, with online schools holding the largest market share in 2024. This trend is driven by the flexibility and convenience offered by online schools compared to traditional institutions. The number of K-12 students opting for online education is increasing due to the personalized learning experience, innovative teaching methods, and easy access to updated course materials. Online schools also help students overcome language barriers, improve communication skills, and enhance overall personality development. Moreover, the use of collaborative learning tools, such as interactive whiteboards and virtual classroom software, facilitates effective group work and real-time feedback.

Student performance tracking and learning analytics enable teachers to monitor progress and adjust instruction accordingly. Cloud-based learning platforms provide access to educational content from anywhere, making education more accessible. Edtech investment, teacher professional development, and e-learning content development are essential components of the online K-12 education ecosystem. Personalized learning paths and distance learning programs cater to individual learning styles and schedules. Gamified learning experiences and blended learning models make education more engaging and effective. Cybersecurity in education is a critical concern, with the adoption of digital textbooks, mobile learning apps, and online tutoring services. Adaptive learning technologies and personalized learning analytics help cater to each student's unique learning needs.

Curriculum development services and online learning platforms ensure high-quality education. The edtech startup landscape is vibrant, with numerous innovations and solutions emerging to address the evolving needs of K-12 education. The market is expected to continue growing as technology integration becomes more seamless and online education becomes an integral part of the educational landscape.

Get a glance at the market share of various segments Request Free Sample

The Online schools segment was valued at USD 5101.90 million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of K-12 Online Education in China Industry?

- The significant rise in the usage of online test preparation courses in China is the primary market catalyst. The K-12 online education market has witnessed significant growth due to the increasing adoption of educational technology. Accessibility features, student performance tracking, and learning analytics are key drivers fueling this trend. Parental involvement and online community building are essential components of the K-12 online education ecosystem, contributing to equity in education and student engagement. Cybersecurity and accessibility features are critical considerations in the development and implementation of online learning platforms, ensuring a secure and inclusive environment for all students.

- Recent research indicates that educational technology adoption is expected to continue, with learning analytics and interactive tools playing a pivotal role in improving student performance. Edtech investment continues to rise, with a focus on teacher professional development to enhance the effectiveness of online learning. Edtech investment funds fuel the growth of technology integration, providing resources for cloud-based learning, live online classes, and engaging learning experiences.

What are the market trends shaping the K-12 Online Education in China Industry?

- The customization of online education services is gaining significant traction as the latest market trend. This evolution reflects the increasing demand for personalized learning experiences in the digital age. The K-12 online education market is witnessing significant growth due to the integration of technology into traditional learning environments. Companies are expanding their offerings by introducing cloud-based learning platforms, hybrid learning environments, and remote learning solutions. These technologies enhance student engagement by providing personalized learning experiences and real-time performance metrics. Digital textbook adoption is also on the rise, enabling students to access educational materials from anywhere, at any time.

- In China, some online education services offer customized learning, where teachers tailor the curriculum and learning pace to individual students' needs. Overall, the integration of technology into education is transforming the way students learn, making it more efficient, collaborative, and engaging. Learning outcomes measurement is another critical aspect of online education, ensuring that students are gaining the necessary digital literacy skills to succeed in today's world. Mobile learning apps are increasingly popular, offering flexibility and convenience for students.

What challenges does the K-12 Online Education in China Industry face during its growth?

- The unequal interaction and socializing opportunities among students represent a significant challenge impeding the growth of the industry. Online K-12 education has emerged as a viable alternative to traditional classroom learning, offering lifelong opportunities for students to access educational content and resources. This market encompasses various components, including educational software licensing, online learning platforms, e-learning content development, teacher training programs, personalized learning analytics, and adaptive learning technologies. Cybersecurity in education plays a crucial role in ensuring the safety and privacy of students' data. The shift towards online learning is driven by the flexibility and convenience it offers, allowing students to learn at their own pace and schedule. However, the lack of social interaction and face-to-face engagement with teachers and peers can be a challenge.

- This can impact the development of essential skills such as communication, collaboration, and emotional intelligence. For instance, virtual classrooms, interactive whiteboards, and real-time collaboration tools help bridge the gap between online and offline learning. Moreover, personalized learning analytics and adaptive learning technologies enable teachers to tailor instruction to individual students' needs, fostering a more effective and engaging learning experience. The K-12 online education market is a dynamic and evolving landscape, driven by the need for flexible and personalized learning opportunities. While challenges remain, ongoing research and innovation are helping to create more engaging and effective online learning experiences that support students' academic and personal growth.

Exclusive Customer Landscape

The K-12 online education market in China forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the K-12 online education market in China report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, K-12 online education market in China forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - The company specializes in delivering K-12 online education courses, including Adobe Express and Photoshop Express.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Ambow Education Holding Ltd.

- Beijing Huaxia Dadi Distance Learning

- ChinaEDU Corp.

- EIC Education

- HELLOWORLD ONLINE EDUCATION GROUP HK LTD.

- iTutorGroup Inc.

- Kaplan Inc.

- New Oriental Education and Technology Group Inc.

- Platinum Equity Advisors LLC

- Primavera Holdings Ltd.

- TAL Education Group

- TCTM Kids IT Education Inc.

- VIPKID HK Ltd.

- Xiaochuanchuhai Education Technology Beijing Co. Ltd.

- Xueda Education

- ZHAN.com

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in K-12 Online Education Market In China

- In January 2024, Microsoft Education announced the global expansion of Microsoft Education Transformation Framework, a free resource designed to help schools adapt to remote learning. The framework includes tools like Microsoft Teams for Education, OneNote, and Minecraft: Education Edition (Microsoft, 2024).

- In March 2024, Google and Apple joined forces to provide free access to their educational platforms, Google Classroom and Apple School Manager, to schools in the US and Canada during the pandemic. This collaboration aimed to support remote learning and ensure equitable access to digital tools (Apple, 2024; Google, 2024).

- In May 2025, Byju's, a leading edtech company, raised a USD200 million Series F funding round, bringing its valuation to USD16.5 billion. The investment will be used to expand its offerings in the K-12 online education market and enhance its technology platform (Byju's, 2025).

Research Analyst Overview

The K-12 online education market continues to evolve, driven by the integration of advanced technologies and shifting educational priorities. Accessibility features, student performance tracking, and learning analytics are at the forefront of this transformation. Collaborative learning tools, such as interactive whiteboards, facilitate real-time engagement and foster a more interactive learning experience. Edtech investment is on the rise, fueling the development of cloud-based learning platforms and hybrid learning environments. Student engagement metrics and remote learning solutions are essential components of these platforms, enabling personalized learning paths for students. Cybersecurity in education is a critical concern, with the increasing use of digital textbooks and online learning platforms.

Personalized learning analytics and adaptive learning technologies are revolutionizing the way students learn, allowing for customized instruction based on individual needs. Online learning platforms, teacher training programs, and e-learning content development are seamlessly integrated into this evolving landscape. Edtech startups are innovating in areas such as virtual classroom software, online tutoring services, and curriculum development services. Gamified learning experiences and blended learning models are gaining popularity, as educators seek to enhance student engagement and improve learning outcomes. The integration of educational technology is a continuous process, with new developments and applications emerging regularly.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled K-12 Online Education Market in China insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 16.3% |

|

Market growth 2025-2029 |

USD 31.16 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

15.8 |

|

Key countries |

China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks, market research and growth, market growth and forecasting, Market forecasting, market report, market forecast |

What are the Key Data Covered in this K-12 Online Education Market in China Research and Growth Report?

- CAGR of the K-12 Online Education in China industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across China

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the k-12 online education market in China growth of industry companies

We can help! Our analysts can customize this k-12 online education market in China research report to meet your requirements.

RIA -

RIA -