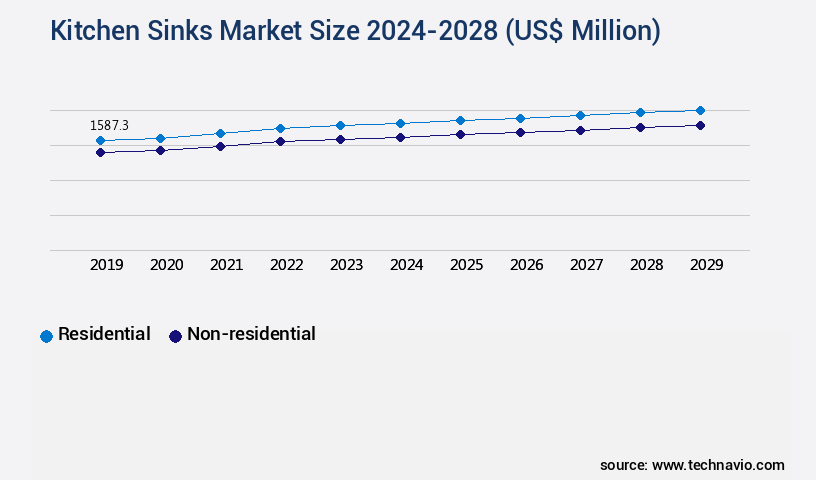

Kitchen Sinks Market Size 2024-2028

The kitchen sinks market size is valued to increase USD 950.9 million, at a CAGR of 4.93% from 2023 to 2028. Growing global residential building construction market will drive the kitchen sinks market.

Major Market Trends & Insights

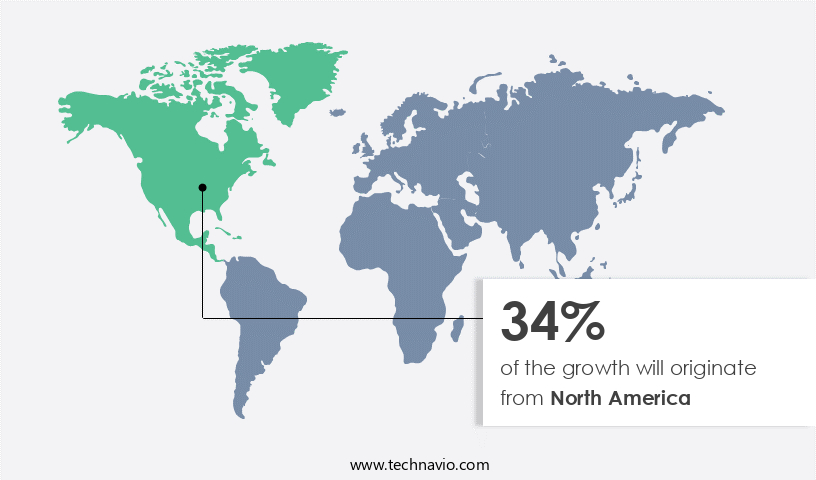

- North America dominated the market and accounted for a 34% growth during the forecast period.

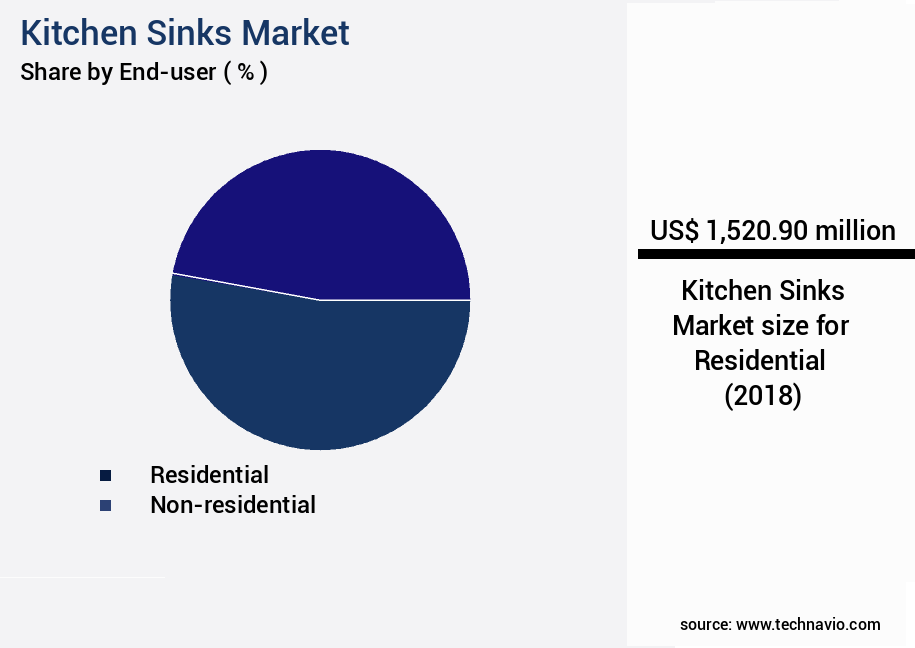

- By End-user - Residential segment was valued at USD 1520.90 million in 2022

- By Material - Metal segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 54.57 million

- Market Future Opportunities: USD 950.90 million

- CAGR : 4.93%

- North America: Largest market in 2022

Market Summary

- The market encompasses the production, distribution, and sale of various sink types used in both commercial and residential applications. This dynamic market is driven by the expanding residential building construction sector, with semi-recessed sinks experiencing significant growth. However, the market is not without challenges. Fluctuations in raw material prices, particularly for metals and plastics, pose a significant threat to profitability. Core technologies, such as stainless steel and composite materials, continue to dominate the market, while applications span from kitchens to laboratories and industrial settings.

- Regions like Asia Pacific and Europe exhibit robust demand due to increasing urbanization and infrastructure development. According to recent reports, the global kitchen sink market held a 30% share in the plumbing fixtures market in 2020. The market is an ever-evolving landscape, offering opportunities for innovation and growth in response to changing consumer preferences and market dynamics.

What will be the Size of the Kitchen Sinks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Kitchen Sinks Market Segmented and what are the key trends of market segmentation?

The kitchen sinks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Residential

- Non-residential

- Material

- Metal

- Non-metal

- Type

- Undermount

- Top-Mount

- Apron-Front

- Double Basin

- Single Basin

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Russia

- UK

- Middle East and Africa

- South Africa

- UAE

- APAC

- China

- India

- Japan

- South Korea

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant expansion, driven by the increasing demand from various end-users, including the residential and commercial sectors. The residential sector's growth, fueled by a growing population and urbanization, is anticipated to propel The market forward. The residential sector's expansion is particularly notable in regions such as APAC and North America. In the US, the housing sector is recovering from the economic downturn, while APAC hosts numerous developing economies, such as China, India, and Indonesia, which are poised for substantial growth in residential construction during the forecast period. Environmental sustainability is a crucial factor influencing market trends.

Furthermore, the market is expected to grow at a steady pace, with the residential sector's expansion contributing to approximately 30% of the total market share. Additionally, the commercial sector is expected to account for around 25% of the market share, driven by the increasing demand for commercial kitchens in the hospitality and foodservice industries. In conclusion, the market is experiencing continuous growth, fueled by the expanding residential and commercial sectors. Technological advancements and environmental sustainability are essential drivers of market trends. The market is expected to grow at a steady pace, with the residential sector accounting for the majority of the market share.

The Residential segment was valued at USD 1520.90 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Kitchen Sinks Market Demand is Rising in North America Request Free Sample

The market in North America is primarily driven by the increasing residential construction activities, leading to a rise in the demand for kitchen sinks. With the US being the major market, the growing number of residential units is anticipated to fuel the market's growth. Additionally, the expanding restaurant industry, projected to reach USD899 billion by 2022, is expected to boost the demand for various types of kitchen sinks, including dual-compartment and garbage separator models. These trends reflect the evolving dynamics of the market in North America.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a broad spectrum of products and applications, extending beyond the conventional porcelain or stainless steel sinks. This dynamic market is characterized by the integration of advanced technologies and sustainable agricultural practices to enhance crop productivity and soil health. Plant growth promoting rhizobacteria (PGPR) and microbial inoculants play a pivotal role in soil health improvement. PGPR effects on crops include nitrogen fixation, phosphorus solubilization, and disease suppression, leading to increased nutrient uptake and improved crop stress response mechanisms. Mycorrhizal fungi significantly contribute to this process by forming symbiotic relationships with plant roots, thereby facilitating nutrient absorption and improving water use efficiency in arid environments.

Humic substances are another essential component in sustainable agriculture, as they promote soil fertility and enhance nutrient use efficiency through biofertilizers. Measuring soil enzyme activity is crucial for assessing soil health, providing insights into the biological processes that drive nutrient cycling and crop growth. Biofertilizers, derived from beneficial fungi, play a significant role in nitrogen fixation in legumes, generating substantial economic impact. Precision farming techniques, such as data-driven decision-making and crop yield prediction using advanced modeling, optimize resource management and contribute to the economic and environmental benefits of sustainable agriculture. Integrated pest management strategies and organic matter amendment further bolster the market's growth.

The adoption of these sustainable intensification strategies is notable, with more than 70% of new product developments focusing on these areas. Despite the increasing trend towards sustainable agriculture, traditional fertilizer application methods continue to dominate, accounting for a significantly larger share compared to the adoption of biofertilizers. In conclusion, The market extends beyond the realm of conventional sinks, encompassing a diverse range of sustainable agricultural practices that promote soil health, nutrient use efficiency, and crop productivity. The integration of advanced technologies and precision farming techniques further enhances the market's potential, driving growth and innovation in the sector.

What are the key market drivers leading to the rise in the adoption of Kitchen Sinks Industry?

- The expanding global residential building construction market serves as the primary catalyst for market growth.

- The global residential building construction market is experiencing significant growth, driven by urbanization and increasing disposable income, particularly in the Asia Pacific region. According to the World Bank, the percentage of China's urban population grew by around 11.1% between 2011 and 2021. This demographic shift has led to a surge in residential building construction, with people investing in houses as long-term assets and potential rental properties. The market is poised to benefit from this trend, as new residential construction projects require numerous fixtures and appliances.

- The global residential building construction market is expected to reach substantial value by 2023, reflecting the ongoing demand for housing solutions.

What are the market trends shaping the Kitchen Sinks Industry?

- The trend in the market involves the emergence of semi-recessed sinks for growth. This up-and-coming design is gaining popularity.

- Semi-recessed sinks, a fusion of functionality and modern design, have emerged as a significant trend in the market. These sinks offer the benefits of undermount sinks, such as seamless counter integration, combined with the contemporary look of a kitchen sink. The increasing popularity of space-saving modular kitchens, especially in urban areas, fuels the demand for semi-recessed sinks worldwide. Semi-recessed sinks distinguish themselves by partially protruding from the surface they rest upon. This design not only adds a unique aesthetic appeal but also makes cleaning the surrounding area and the sink itself more accessible. The sink's protrusion enables easy access to the sink's edges, making it simpler to clean the countertop and the sink base.

- Additionally, the semi-recessed design saves valuable counter space, making it an attractive choice for kitchens with limited space. The advantages of semi-recessed sinks extend beyond aesthetics and space savings. Their design allows for easier installation, as they can be mounted on a template, making the process more efficient and less labor-intensive compared to undermount sinks. Furthermore, the partially exposed rim provides better support for sink accessories, such as drainboards and cutting boards, enhancing the overall functionality of the sink. In conclusion, semi-recessed sinks represent a smart and stylish solution for kitchens with space constraints and a contemporary aesthetic.

- Their unique design, ease of installation, and enhanced functionality make them an increasingly popular choice in the market.

What challenges does the Kitchen Sinks Industry face during its growth?

- The volatility in raw material prices poses a significant challenge to the industry's growth trajectory.

- The global kitchen sink market experiences ongoing fluctuations due to the volatile prices of raw materials. Ceramic, concrete, copper, glass, and steel are primary components, and their price changes significantly impact production costs. For instance, a 10% increase in material costs can lead to a corresponding rise in kitchen sink prices. This dynamic market trend is a challenge for manufacturers, as they must balance costs and consumer demand for various styles, colors, and finishes.

- The kitchen sink industry's continuous evolution reflects the need for adaptability and price competitiveness.

Exclusive Customer Landscape

The kitchen sinks market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the kitchen sinks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Kitchen Sinks Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, kitchen sinks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Azuga Inc. - The company specializes in providing a range of high-quality kitchen sinks, including the granite sink models Enigma N200 and Magic Salsa 1816. These sinks are renowned for their durability and aesthetic appeal, catering to various design preferences and functional needs. The company's commitment to innovation and customer satisfaction sets it apart in the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Azuga Inc.

- BLANCO GmbH and Co. KG

- Dornbracht AG and Co. KG

- Elkay Manufacturing Co.

- Fletcher Building Ltd.

- Fortune Brands Innovations Inc.

- FRANKE Holding AG

- Futura Kitchen sinks Ind Pvt Ltd.

- JOMOO Kitchen and Bath Co. Ltd.

- JULIEN Inc.

- Kohler Co.

- Kovinoplastika Loz d.o.o.

- Kraus USA Inc.

- Roca Sanitario SA

- Ruvati

- Schock GmbH

- TEKA INDUSTRIAL SA

- VIGO INDUSTRIES LLC

- Whitehaus Collection

- Zuhne LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Kitchen Sinks Market

- In January 2024, leading kitchen sink manufacturer, Kohler Co., introduced its new line of smart sinks, named "Sensate," at the Consumer Electronics Show (CES). These sinks feature touchless operation, voice control, and temperature-controlled water (Kohler press release, 2024).

- In March 2024, American Standard Brands, a LIXIL Group company, announced a strategic partnership with HomeAdvisor to expand its reach in the U.S. Home improvement market. This collaboration enables American Standard to offer HomeAdvisor's professional installation services to its customers (American Standard press release, 2024).

- In May 2024, Blanco, a German kitchen sink manufacturer, completed the acquisition of British sink producer, Reginox. This move strengthened Blanco's position in the European market and expanded its product offerings (Blanco press release, 2024).

- In April 2025, the U.S. Environmental Protection Agency (EPA) approved a new standard for lead content in kitchen sinks, reducing the maximum allowable limit to 0.25%. This regulation aims to improve public health and safety (EPA press release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Kitchen Sinks Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.93% |

|

Market growth 2024-2028 |

USD 950.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.61 |

|

Key countries |

Brazil, South Africa, UAE, US, Canada, Germany, UK, China, France, Italy, Japan, India, South Korea, Argentina, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of modern agriculture, the market encompasses a range of innovative practices aimed at enhancing crop productivity and promoting environmental sustainability. One such area of focus is the optimization of soil health, with an emphasis on potassium availability and nitrogen fixation processes. Growth-promoting bacteria and mycorrhizal fungi networks play a crucial role in these processes. Soil enzyme activity is a key indicator of these microbial communities' health and their ability to improve nutrient use efficiency. The application of beneficial fungi and the decomposition of organic matter contribute significantly to these improvements. Environmental sustainability metrics, such as pest resistance mechanisms and yield improvement strategies, are also essential considerations in the market.

- Water use efficiency and disease suppression methods are integral components of sustainable agriculture practices. Precision farming technologies and biofertilizer application techniques further enhance nutrient delivery and crop stress tolerance. The rhizosphere microbiome, microbial inoculants, and plant hormone modulation are essential elements of this complex ecosystem. Improved fertilizer efficiency and phosphorus solubilization are critical for optimizing nutrient cycling. Integrated pest management and humic acid fertilizers are essential for reducing fertilizer input and promoting soil health indicators. The market continues to evolve, with ongoing research and development in plant growth regulators, soil carbon sequestration, and water conservation methods. These advancements contribute to agricultural productivity gains and the adoption of sustainable agriculture practices.

- The market's microbial community structure is a dynamic and intricate web of interactions, with ongoing research revealing new insights into the intricacies of soil health and nutrient uptake enhancement.

What are the Key Data Covered in this Kitchen Sinks Market Research and Growth Report?

-

What is the expected growth of the Kitchen Sinks Market between 2024 and 2028?

-

USD 950.9 million, at a CAGR of 4.93%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Residential and Non-residential), Material (Metal and Non-metal), Geography (North America, Europe, APAC, Middle East and Africa, and South America), and Type (Undermount, Top-Mount, Apron-Front, Double Basin, and Single Basin)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing global residential building construction market, Fluctuations in raw material prices

-

-

Who are the major players in the Kitchen Sinks Market?

-

Azuga Inc., BLANCO GmbH and Co. KG, Dornbracht AG and Co. KG, Elkay Manufacturing Co., Fletcher Building Ltd., Fortune Brands Innovations Inc., FRANKE Holding AG, Futura Kitchen sinks Ind Pvt Ltd., JOMOO Kitchen and Bath Co. Ltd., JULIEN Inc., Kohler Co., Kovinoplastika Loz d.o.o., Kraus USA Inc., Roca Sanitario SA, Ruvati, Schock GmbH, TEKA INDUSTRIAL SA, VIGO INDUSTRIES LLC, Whitehaus Collection, and Zuhne LLC

-

Market Research Insights

- The market encompasses a diverse range of products designed for efficient water usage in various sectors, including agricultural and residential applications. According to industry estimates, the global demand for kitchen sinks reached approximately 25 million units in 2020, representing a steady growth of 3% year-over-year. In the agricultural sector, the integration of kitchen sinks in farming practices has led to significant improvements in nutrient cycling processes and crop growth parameters. For instance, using a kitchen sink for irrigation can reduce water usage by up to 30% compared to traditional methods, contributing to efficient resource use and output maximization. Furthermore, the implementation of sensor technology application and data-driven farming techniques in kitchen sink systems has facilitated precision agriculture, enabling farmers to optimize crop production and ensure yield stability.

- The economic viability assessment of kitchen sinks in agriculture also highlights their potential role in sustainable intensification, as they promote efficient use of nutrient management strategies and stress tolerance, while minimizing the need for pest management strategies and biocrop agents. Overall, the market continues to evolve, offering innovative solutions for optimizing agricultural productivity, resource use efficiency, and environmental stewardship.

We can help! Our analysts can customize this kitchen sinks market research report to meet your requirements.

RIA -

RIA -