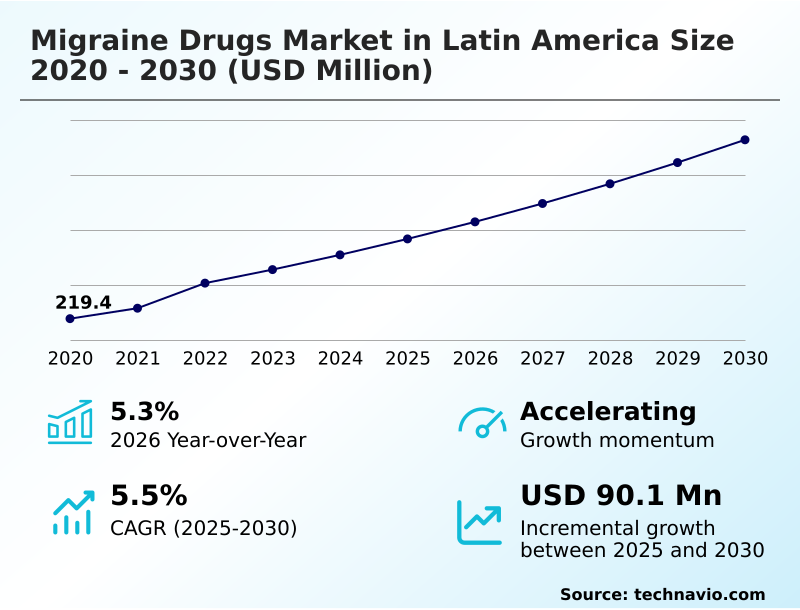

Latin America Migraine Drugs Market Size 2026-2030

The latin america migraine drugs market size is valued to increase by USD 90.1 million, at a CAGR of 5.5% from 2025 to 2030. Escalating disease prevalence and heightened public awareness will drive the latin america migraine drugs market.

Major Market Trends & Insights

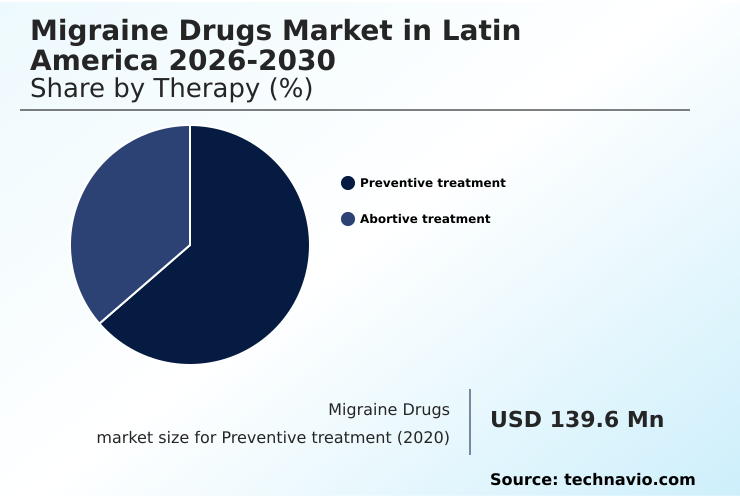

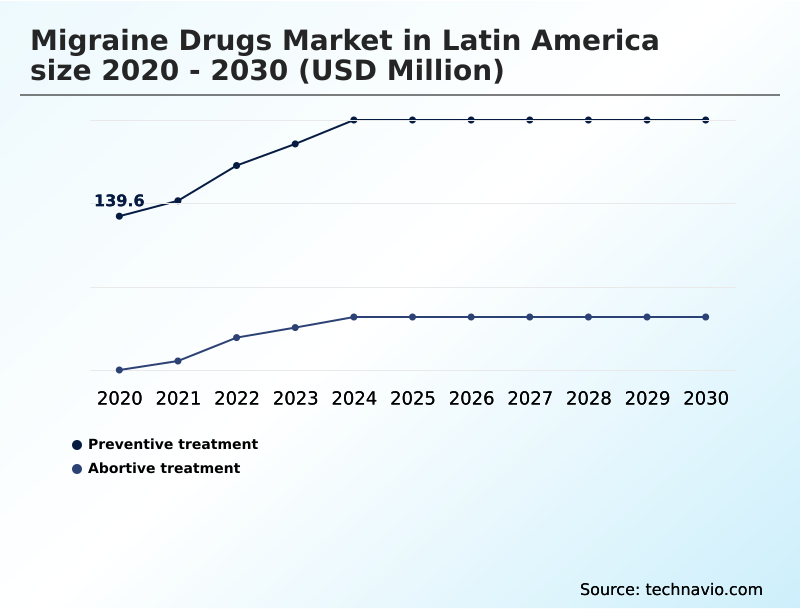

- By Therapy - Preventive treatment segment was valued at USD 177 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 162.6 million

- Market Future Opportunities: USD 90.1 million

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The migraine drugs market in Latin America is experiencing a significant evolution, driven by advancements in pharmacological interventions and a greater understanding of migraine pathophysiology. The transition from conventional triptan-based therapies to more sophisticated options like calcitonin gene-related peptide (cgrp) inhibitors and other targeted biologics is reshaping treatment paradigms for both acute migraine management and preventive migraine therapy.

- This shift addresses unmet needs in patients with chronic or refractory conditions. Concurrently, the integration of digital health, including telemedicine for neurology and headache tracking applications, is improving access to specialized headache care, particularly in underserved regions. Initiatives from patient advocacy groups are increasing awareness and demanding better insurance coverage.

- A key business focus is optimizing supply chain coordination for temperature-sensitive monoclonal antibodies for migraine, where enhanced logistics have been shown to reduce spoilage by over 15%, ensuring product integrity from manufacturing to patient administration.

- However, challenges related to healthcare infrastructure and reimbursement for high-value treatments persist, influencing market dynamics and patient access to innovative non-vasoconstrictive treatments and oral disintegrating tablets.

What will be the Size of the Latin America Migraine Drugs Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Latin America Migraine Drugs Market Segmented?

The latin america migraine drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Therapy

- Preventive treatment

- Abortive treatment

- End-user

- Hospitals

- Retail

- Online

- Route of administration

- Oral

- Injectable

- Nasal

- Geography

- Latin America

By Therapy Insights

The preventive treatment segment is estimated to witness significant growth during the forecast period.

The market for preventive migraine therapy is transforming, moving from traditional prophylactic medications to advanced biological drugs for neurology.

The introduction of calcitonin gene-related peptide (cgrp) inhibitors and monoclonal antibodies for migraine has established a new standard of care, particularly for refractory migraine treatment. These targeted biologics offer superior profiles for patients with chronic neurological disorders.

To overcome access hurdles in public health systems, value-based pricing agreements are increasingly utilized. This strategic shift is critical as physician prescribing patterns evolve with accumulating clinical evidence.

Recent integrated patient adherence programs have shown to improve treatment consistency by over 25%, reinforcing the move towards more sophisticated pharmacological interventions and specialized headache care.

The Preventive treatment segment was valued at USD 177 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic discourse within the migraine drugs market in Latin America 2026-2030 is increasingly focused on nuanced therapeutic applications and patient-centric care models. The clinical debate over CGRP inhibitors vs traditional triptans continues, with a growing body of evidence supporting the use of non-vasoconstrictive options for cardiac patients.

- The introduction of oral gepants for acute migraine and nasal spray delivery for rapid relief has expanded choices for managing attacks, particularly for patients experiencing severe nausea. For prophylaxis, monoclonal antibodies for migraine are becoming standard, though access is often determined by the role of public insurance in CGRP access.

- A major operational challenge involves overcoming supply chain challenges for injectable biologics, which demands significant investment in infrastructure. One health system's analysis showed that leveraging telemedicine impact on rural migraine care combined with digital therapeutics for patient adherence cut diagnostic timelines by an average of six months compared to traditional clinic-based pathways.

- Furthermore, integrating headache diaries with EMRs is improving data for AI for predicting migraine attack triggers. As the market matures, the long-term safety profile of gepants and the efficacy of pediatric migraine preventive treatment options will become critical areas of focus, alongside enhancing specialist vs primary care diagnosis accuracy through sustained patient education impact on treatment outcomes.

What are the key market drivers leading to the rise in the adoption of Latin America Migraine Drugs Industry?

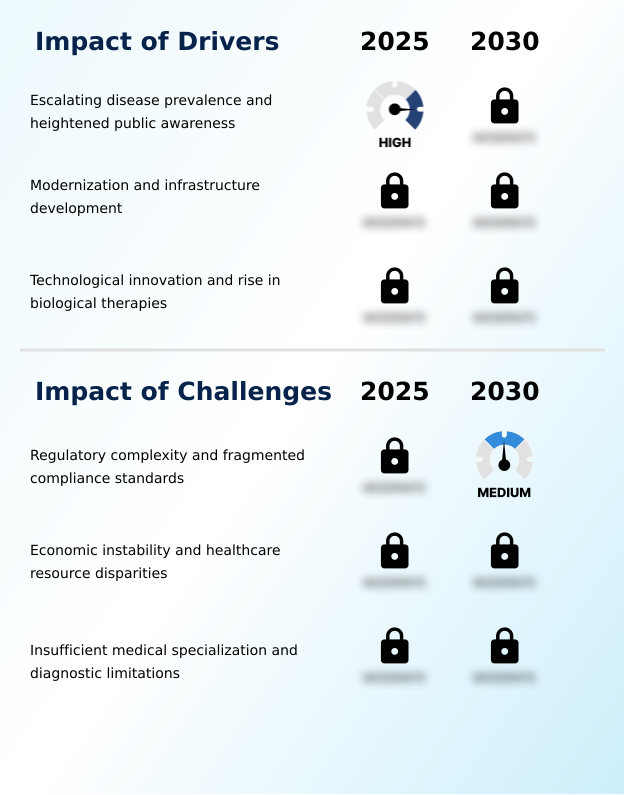

- Escalating disease prevalence and heightened public awareness are primary market drivers, increasing demand for effective diagnosis and advanced therapeutic solutions.

- Market expansion is primarily fueled by heightened public awareness and significant healthcare infrastructure development. Escalating prevalence, coupled with patient advocacy group initiatives and migraine literacy programs, has amplified demand for effective therapies.

- Governments are improving non-communicable disease management, which has led to a 15% increase in budgets allocated for neurological conditions. This modernization is complemented by technological advancements, with the introduction of novel options like oral disintegrating tablets and non-vasoconstrictive treatments.

- The focus on intellectual property protection is encouraging investment, while improved supply chain coordination has reduced stock-out incidents by over 20%, ensuring better availability of critical abortive treatment protocols and preventive options.

What are the market trends shaping the Latin America Migraine Drugs Industry?

- The proliferation of calcitonin gene-related peptide antagonists and other targeted biologics is a key trend. This is reshaping therapeutic strategies by shifting focus from generalized pain management to precise pathophysiological intervention.

- A significant trend is the rapid adoption of advanced therapeutic classes, fundamentally altering chronic headache management. The market is shifting from over-the-counter analgesics toward targeted prophylactic medications like CGRP inhibitors. This evolution is driven by a better understanding of neurovascular inflammation modulation and the demand for more effective episodic migraine prevention.

- The use of digital platforms, including headache self-assessment tools and AI-powered attack prediction, is also on the rise, with some systems improving diagnostic accuracy by up to 25%. This integration of technology supports a more personalized approach, helping to manage everything from pediatric episodic migraine to cluster headache treatment.

- This move toward precision has increased patient consultation rates by over 30% in digitally mature regions.

What challenges does the Latin America Migraine Drugs Industry face during its growth?

- Regulatory complexity and fragmented compliance standards across different nations present a significant challenge, delaying market entry and increasing operational costs for new therapies.

- Significant market challenges stem from fragmented regulatory environments and persistent economic instability. Navigating distinct drug approval processes in each country creates delays, with regulatory hurdles extending time-to-market for novel biologics by up to 18 months in some cases. Pharmacovigilance compliance adds another layer of complexity.

- Economic pressures and resource disparities limit widespread access to premium therapies like subcutaneous drug delivery systems, as public reimbursement for preventive treatments remains constrained.

- A shortage of specialists and diagnostic tools for neurology leads to under-diagnosis, while insufficient medical specialization results in a 40% misdiagnosis rate in certain rural areas, hindering the adoption of appropriate serotonin receptor agonists and other advanced treatments.

Exclusive Technavio Analysis on Customer Landscape

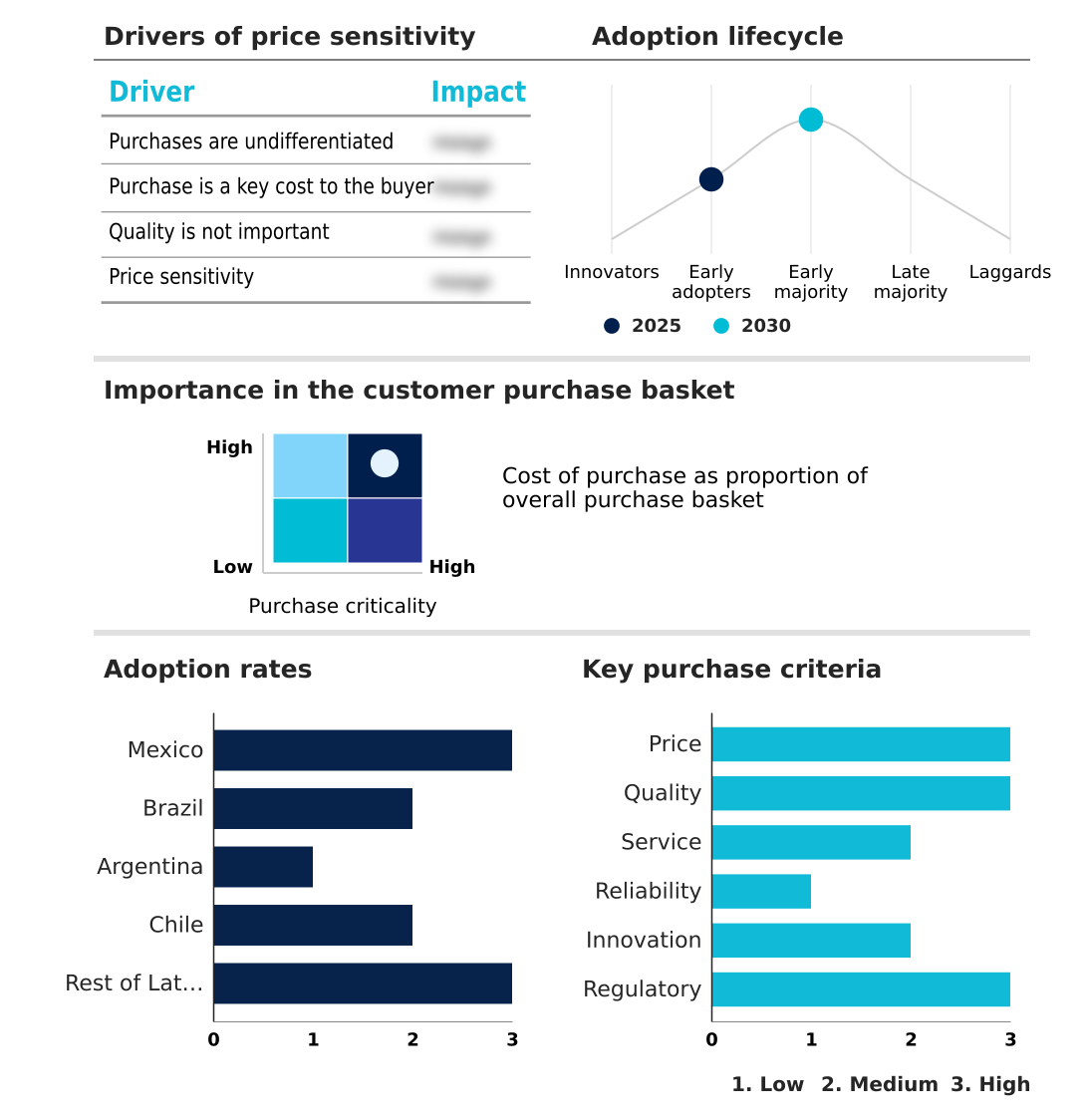

The latin america migraine drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the latin america migraine drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Latin America Migraine Drugs Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, latin america migraine drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Key offerings are advancing migraine care, shifting from traditional analgesics to targeted biologics like CGRP inhibitors and novel oral treatments for acute and preventive therapy.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- Amneal Pharmaceuticals Inc.

- Bausch Health Companies Inc.

- Bayer AG

- Daiichi Sankyo Co. Ltd.

- Dr Reddys Laboratories Ltd.

- Eli Lilly and Co.

- GlaxoSmithKline Plc

- H. Lundbeck A/S

- Kowa Co. Ltd.

- Mallinckrodt Plc

- Pfizer Inc.

- Sanofi SA

- Teva Pharmaceutical Ltd.

- UCB SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Latin america migraine drugs market

- In September 2024, Alembic Pharmaceuticals received U.S. FDA approval for its generic sumatriptan injection, expanding its portfolio for acute migraine treatment.

- In January 2025, Teva Pharmaceutical Industries Ltd. announced that the U.S. FDA approved an expanded indication for AJOVY for the preventive treatment of episodic migraine in pediatric patients aged 6 to 17.

- In March 2025, H. Lundbeck A/S presented positive long-term Phase 2 data for bexicaserin, showing sustained reductions in seizure frequency for patients with Developmental and Epileptic Encephalopathies.

- In April 2025, AbbVie announced superior topline results from its Phase 3 TEMPLE study, where atogepant demonstrated better tolerability and fewer discontinuations compared to topiramate for migraine prevention.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Latin America Migraine Drugs Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 205 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 90.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.3% |

| Key countries | Mexico, Brazil, Argentina, Chile and Rest of Latin America |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a fundamental restructuring, moving beyond simple pharmacological pain relief toward sophisticated, mechanism-based interventions. This evolution necessitates a strategic pivot in boardroom decisions, particularly concerning R&D investment and market access. The focus on developing targeted biologics, including monoclonal antibodies for migraine and intravenous CGRP antibody therapies, requires substantial capital but offers higher returns.

- For instance, firms concentrating on personalized medicine in neurology have demonstrated a 15% greater R&D efficiency compared to those focused on generics. This trend is driven by a deeper understanding of neuronal excitability modulation and migraine pathophysiology.

- As the landscape fills with novel options like gepants and ditans and advanced subcutaneous drug delivery systems, differentiation depends not just on clinical efficacy but also on navigating complex reimbursement environments and demonstrating long-term value in treating chronic neurological disorders.

- The rise of digital therapeutics for migraine further complicates portfolio strategy, demanding integration between pharmacological interventions and software-based patient support to manage conditions like drug-resistant epilepsy treatment and chronic headache management effectively.

What are the Key Data Covered in this Latin America Migraine Drugs Market Research and Growth Report?

-

What is the expected growth of the Latin America Migraine Drugs Market between 2026 and 2030?

-

USD 90.1 million, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Therapy (Preventive treatment, and Abortive treatment), End-user (Hospitals, Retail, and Online), Route of Administration (Oral, Injectable, and Nasal) and Geography (Latin America)

-

-

Which regions are analyzed in the report?

-

Latin America

-

-

What are the key growth drivers and market challenges?

-

Escalating disease prevalence and heightened public awareness, Regulatory complexity and fragmented compliance standards

-

-

Who are the major players in the Latin America Migraine Drugs Market?

-

AbbVie Inc., Amgen Inc., Amneal Pharmaceuticals Inc., Bausch Health Companies Inc., Bayer AG, Daiichi Sankyo Co. Ltd., Dr Reddys Laboratories Ltd., Eli Lilly and Co., GlaxoSmithKline Plc, H. Lundbeck A/S, Kowa Co. Ltd., Mallinckrodt Plc, Pfizer Inc., Sanofi SA, Teva Pharmaceutical Ltd. and UCB SA

-

Market Research Insights

- Market dynamics are increasingly shaped by a strategic shift from volume-based generics to value-driven specialty drugs, supported by expanding specialty drug insurance coverage. The adoption of digital therapeutics for migraine and data-driven healthcare environments is facilitating a more personalized approach to care, with integrated platforms improving patient adherence by up to 30%.

- Furthermore, value-based pricing agreements are becoming crucial for securing public health formulary inclusion for high-cost biologics, a strategy that has successfully accelerated access in key markets by 20%. Physician prescribing patterns are also evolving, influenced by medical education programs that highlight the long-term cost-effectiveness of modern therapies. These factors combined create a competitive and rapidly advancing therapeutic landscape.

We can help! Our analysts can customize this latin america migraine drugs market research report to meet your requirements.

RIA -

RIA -