LED Production Equipment Market Size 2024-2028

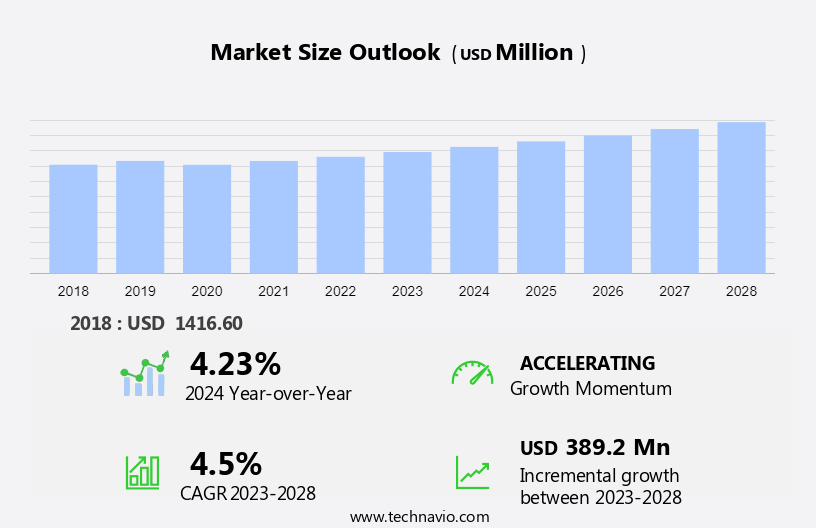

The LED production equipment market size is forecast to increase by USD 389.2 million and is estimated to grow at a CAGR of 4.5% between 2023 and 2028. The market is experiencing significant growth due to increasing government support for energy-efficient lighting solutions and advancements in LED chip production. Governments worldwide are implementing policies to promote the adoption of LED lighting, providing incentives for manufacturers and consumers. This trend is further bolstered by strategic initiatives of market players, including research and development investments, mergers and acquisitions, and partnerships. For instance, Philips Lighting, a global leader in LED lighting, has announced its commitment to exit the traditional light bulb business and focus solely on LED lighting solutions. These factors are driving the market forward, making it an attractive investment opportunity for businesses and individuals alike.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamic and Customer Landscape

The market is witnessing significant growth due to the increasing demand for energy-efficient lighting solutions and advanced display technologies. LED and OLED semiconductor devices are at the forefront of this trend, driving the need for specialized machinery and tools such as MOCVD Equipment, Lithography Equipment, Dry Etch Equipment, and PECVD Equipment for their manufacturing. The market for LED production equipment is segmented into various applications, including general lighting, automotive lighting, and displays. In the general lighting segment, LED bulbs and tubes are the most common applications. In the automotive lighting segment, LED lights are increasingly being used in headlights, taillights, and interior lighting. In the displays segment, LED backlighting is widely used in televisions, monitors, and mobile devices. The demand for LED production equipment is also driven by the growing infrastructure development in roads and highways, where LED lighting is being used extensively for street lighting. Overall, the market for LED production equipment is expected to continue its growth trajectory in the coming years, driven by the increasing adoption of LED and OLED technologies in various applications. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

Increasing government support for the production and sales of LEDs is notably driving market growth. The global market is witnessing significant growth due to the increasing demand for energy-efficient lighting solutions in various applications. Semiconductor devices, machinery and tools used in the manufacturing of LEDs, OLEDs, and other related technologies are driving the market.

Moreover, LED lighting applications, which account for over 25% of global energy consumption, are subject to stringent energy efficiency regulations. Governments worldwide are promoting the use of LEDs through incentives and subsidies, such as India's LED Street Lighting National Programme (SLNP) and Unnat Jyoti by Affordorsable LEDs for All (UJALA). Thus, such factors are driving the growth of the market during the forecast period.

Significant Market Trends

Growing investments in GaN-based technology for mini/micro-LEDs is the key trend in the market. Micro-LEDs, which are smaller than 100 micrometers in size, represent the next generation of LED technology. Unlike traditional LEDs that require backlighting, micro-LEDs are self-emissive, producing rich color and brightness with minimal power consumption. The production of LEDs primarily relies on sapphire substrates.

However, the growing demand for micro-LEDs has led manufacturers to explore alternative technologies, such as gallium nitride-on-silicon (GaN-on-Si), for their production. GaN-on-Si technology offers several advantages, including smaller size, improved efficiency, and reduced production costs. Various vendors are investing in the development of this technology to cater to the increasing market traction for micro-LEDs in various applications, including semiconductor devices, general lighting, automotive lighting, displays, backlighting, roads, bridges, buildings, public spaces, LED streetlights, architectural lighting, and public area illumination. Thus, such trends will shape the growth of the market during the forecast period.

Major Market Challenge

Challenges in manufacturing micro-LEDs is the major challenge that affects the growth of the market. Micro-LEDs, which are LEDs that generate light without external sources, have gained significant attention in the lighting and display industries due to their potential advantages over traditional LED, OLED, and LCD technologies. Micro-LED displays consist of tiny LEDs, typically smaller than 100 µm, forming individual pixel elements.

Moreover, these LEDs offer enhanced brightness, response speed, and contrast, as well as energy efficiency. However, integrating micro-LEDs into various products poses technical challenges, making LCDs, LEDs, and OLEDs more popular alternatives. Some limitations of micro-LEDs include manufacturing complexities, such as achieving uniformity, reliability, and scalability. Additionally, the semiconductor devices required for micro-LED production, including MOCVD Equipment, Lithography Equipment, Dry Etch Equipment, and PECVD Equipment, are sophisticated and costly. In the context of lighting applications, micro-LEDs have been utilized in various sectors, including general lighting, automotive lighting, displays, backlighting, roads, bridges, buildings, public spaces, LED streetlights, and architectural lighting. The DesignLights Consortium (DLC) and energy efficiency regulations have also influenced the adoption of LED technology in these sectors. Hence, the above factors will impede the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

3D Micromac AG: The company offers LED production equipment namely microCETI.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 4JET Technologies GmbH

- Accent Pro 2000 s.r.l.

- AIXTRON SE

- Apex Sound and Light Corp.

- Applied Materials Inc.

- ASM Pacific Technology Ltd.

- Canon Inc.

- Coherent Inc.

- FAROAD

- Jusung Engineering Co. Ltd.

- Manncorp Inc.

- Notion Systems GmbH

- Shanghai Micro Electronics Equipment Group Co. Ltd.

- Shenzhen ETON Automation Equipment Co. Ltd.

- Shenzhen JAGUAR Automation Equipment Co. Ltd.

- SMTnet

- Taiyo Nippon Sanso Corp.

- ULVAC Inc.

- Veeco Instruments Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

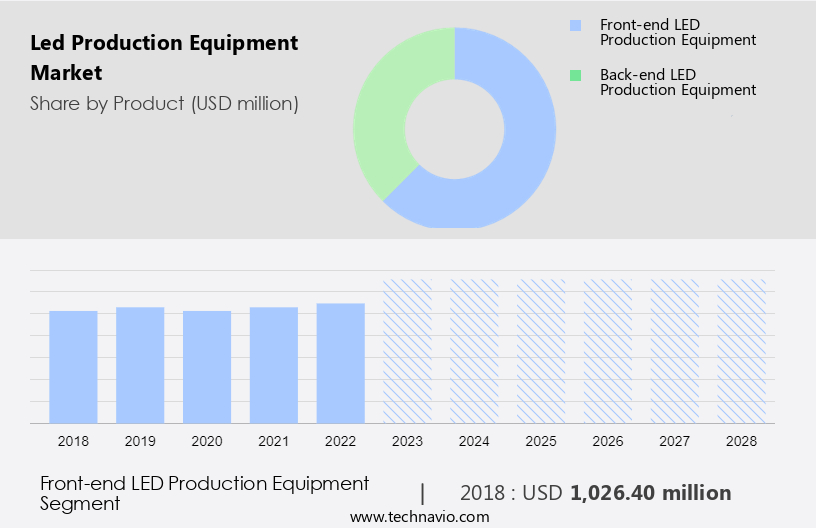

By Product

The front-end LED production equipment segment is estimated to witness significant growth during the forecast period. The market encompasses a range of machinery and tools utilized in the manufacturing process of semiconductor devices, general lighting, automotive lighting, displays, backlighting, and various types of lighting applications.

Get a glance at the market share of various regions Download the PDF Sample

The front-end LED production equipment segment was the largest segment and valued at USD 1.03 billion in 2018. Front-end LED production equipment includes essential components such as stepper systems, metal organic chemical vapor deposition (MOCVD) equipment, lithography equipment, dry etch equipment, and physical vapor deposition (PVD) equipment. In the semiconductor industry, the transition towards advanced packaging methods like flip-chip and 3D packaging is underway, driven by features such as die-stacking technology and wireless connectivity between thin dies. Hence, such factors are fuelling the growth of this segment during the forecast period.

Regional Analysis

For more insights on the market share of various regions Download PDF Sample now!

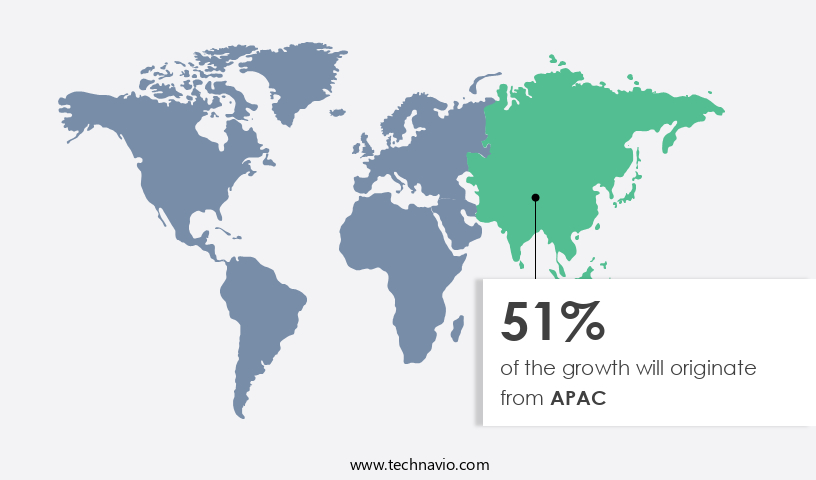

APAC is estimated to contribute 51% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. China, Japan, and South Korea are the key markets for themarket in APAC. Market growth in this region will be slower than the growth of the market in Europe. The demand for LEDs from automotive original equipment manufacturers (OEMs) has increased, which will facilitate the market growth in APAC over the forecast period. This market research report entails detaiLED information on the competitive intelligence, marketing gaps, and regional opportunities in store for vendors, which will assist in creating efficient business plans. Hence, such factors are driving the market in APAC during the forecast period.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million " for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Product Outlook

- Front-end LED production equipment

- Back-end LED production equipment

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports:

Light-Emitting Diode (LED) Market: Light-Emitting Diode (LED) Market Analysis APAC, Europe, North America, South America, Middle East and Africa - US, Taiwan, Japan, UK, Germany - Size and Forecast

LED Lighting Market: LED Lighting Market Analysis APAC, Europe, North America, Middle East and Africa, South America - US, China, Japan, Germany, UK - Size and Forecast

India LED Lighting Market: India LED Lighting Market by Product,Application and Distribution Channel - Forecast and Analysis

Market Analyst Overview

The market encompasses a range of machinery and tools used in the manufacturing of semiconductor devices, general lighting, automotive lighting, displays, backlighting, and various types of LED lighting for roads, bridges, buildings, public spaces, LED streetlights, architectural lighting, and public area illumination. The market is driven by the increasing demand for energy-efficient lighting solutions and stringent energy efficiency regulations. Semiconductor devices, such as MOCVD Equipment, Lithography Equipment, Dry Etch Equipment, and PECVD Equipment, are essential in the production of LED and OLED components. The market landscape depends on the LEDs (Light Emitting Diodes), semiconductors and mechanical parts, automated optical inspection (AOI) systems, machine learning and AI, Back-end LED Production Equipment.

Moreover, these devices enable the precise fabrication of semiconductor materials and the formation of the necessary structures for LED and OLED production. LED and OLED displays are another significant segment of the market, with the increasing demand for high-resolution, large-screen displays driving growth. Backlighting, used in LCD and OLED displays, is also a significant application for LED production equipment. LED lighting, including general lighting, automotive lighting, and architectural lighting, Global LED Production Equipment Market is a rapidly growing segment of the market. The DesignLights Consortium (DLC) and energy efficiency regulations are influential factors in the adoption of LED lighting solutions. The production of LED streetlights and public area illumination is also a significant market, with the increasing focus on energy efficiency and cost savings driving demand. The market for LED production equipment is expected to continue growing due to the increasing demand for energy-efficient lighting solutions and the ongoing development of new technologies.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 389.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 51% |

|

Key countries |

China, US, Japan, Germany, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3D Micromac AG, 4JET Technologies GmbH, Accent Pro 2000 s.r.l., AIXTRON SE, Apex Sound and Light Corp., Applied Materials Inc., ASM Pacific Technology Ltd., Canon Inc., Coherent Inc., FAROAD, Jusung Engineering Co. Ltd., Manncorp Inc., Notion Systems GmbH, Shanghai Micro Electronics Equipment Group Co. Ltd., Shenzhen ETON Automation Equipment Co. Ltd., Shenzhen JAGUAR Automation Equipment Co. Ltd., SMTnet, Taiyo Nippon Sanso Corp., ULVAC Inc., and Veeco Instruments Inc. |

|

Market dynamics |

Parent market analysis, market report, market forecast, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2023 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

RIA -

RIA -