Liquid Biopsy Market Size 2024-2028

The liquid biopsy market size is valued to increase USD 3.7 billion, at a CAGR of 25.2% from 2023 to 2028. Increasing incidence of cancer will drive the liquid biopsy market.

Major Market Trends & Insights

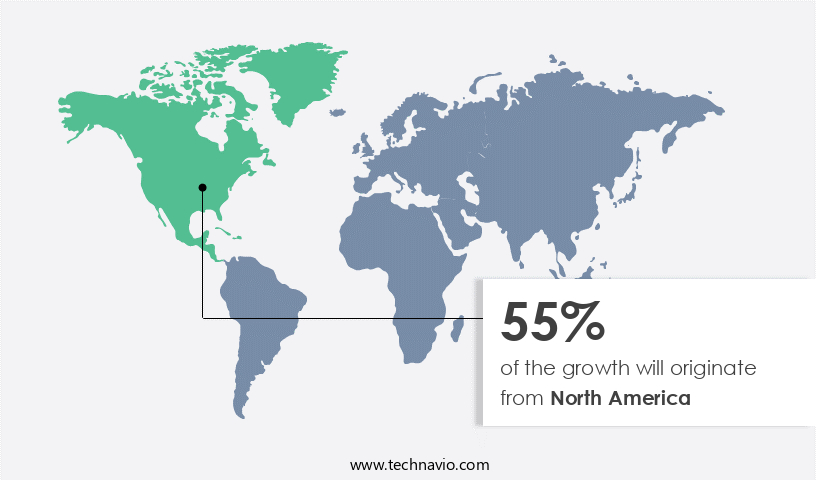

- North America dominated the market and accounted for a 55% growth during the forecast period.

- By Application - Cancer applications segment was valued at USD 812.70 billion in 2022

- By Technology - CTC and ctDNA segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 473.71 million

- Market Future Opportunities: USD 3696.40 million

- CAGR : 25.2%

- North America: Largest market in 2022

Market Summary

- The market represents a significant and rapidly expanding sector in the healthcare industry, driven by advancements in cancer diagnostics and research. This market encompasses various core technologies, including next-generation sequencing and polymerase chain reaction, and applications, such as early detection and monitoring of cancer. Service types range from testing and analysis to consulting and education. Despite the market's growth, challenges persist, including limited reimbursement and regulatory hurdles. However, increasing funding and investment in liquid biopsy technologies continue to fuel innovation and expansion.

- For instance, according to a recent report, The market is projected to reach a 30% market share in the in vitro diagnostics market by 2026. This underscores the evolving nature of the market and the opportunities it presents for stakeholders.

What will be the Size of the Liquid Biopsy Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Liquid Biopsy Market Segmented and what are the key trends of market segmentation?

The liquid biopsy industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Cancer applications

- Non-cancer applications

- Technology

- CTC and ctDNA

- Exosome and RNA

- Sample Type

- Blood

- Urine

- Cerebrospinal Fluid (CSF)

- Others

- Cancer Type

- Lung

- Breast

- Colorectal

- Prostate

- Others.

- End-User

- Hospitals & Clinics

- Diagnostic Labs

- Research Institutes

- Pharma/Biotech.

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The cancer applications segment is estimated to witness significant growth during the forecast period.

Liquid biopsy, a revolutionary approach in cancer diagnostics and monitoring, has gained significant traction in the healthcare industry. This non-invasive method allows for the detection and analysis of cancer-related biomarkers from a patient's blood or other bodily fluids. The global market for liquid biopsy is thriving, with next-generation sequencing (NGS) and multiplex assays driving its growth. Personalized medicine is a key application of liquid biopsy, as it enables the identification of circulating RNA, protein biomarkers, and ctDNA mutations. Patient stratification is another significant application, as it helps in the early detection of cancer subtypes and disease progression. NGS sequencing, RNA sequencing, and digital PCR are essential techniques used in liquid biopsy for genomic profiling and mutation burden analysis.

Sample preparation, epigenetic alterations, and tumor heterogeneity are ongoing challenges in the market. However, advancements in tumor-derived vesicles isolation, CTC enrichment, and exosomes isolation are addressing these challenges. Proteomic analysis and miRNA profiling are also gaining popularity in liquid biopsy, offering insights into drug resistance and therapeutic response. The market is expected to grow substantially, with an estimated 25% of oncology testing shifting from tissue to liquid biopsy by 2025. Furthermore, the market for non-invasive diagnostics is projected to reach a value of USD20 billion by 2027. These trends underscore the continuous evolution and unfolding of the market, offering immense opportunities for businesses and investors.

In conclusion, liquid biopsy is a game-changer in cancer diagnostics and monitoring, offering a non-invasive method for detecting and analyzing cancer-related biomarkers. The market is thriving, with significant growth expected in the coming years. Businesses and investors can capitalize on this trend by focusing on innovations in liquid biopsy techniques, sample preparation, and biomarker analysis.

The Cancer applications segment was valued at USD 812.70 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 55% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Liquid Biopsy Market Demand is Rising in North America Request Free Sample

The North American market dominates the global liquid biopsy industry, with the US and Canada contributing significantly to its share. Key players like Biocept, Guardant Health, and Myriad Genetics derive substantial revenues from this region and maintain headquarters here. The region's market growth is fueled by factors such as the rising number of cancer cases, increasing adoption of advanced biopsy tests, a growing older population, and substantial investments in cancer screening and anti-cancer drug development.

This trend is expected to continue, solidifying North America's position as a major player in the market.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to its potential in revolutionizing cancer diagnosis and treatment. This innovative approach allows for the detection of circulating tumor cells (CTCs) and cell-free DNA (cfDNA) from various body fluids, including plasma. CTDNA detection sensitivity has been a key focus, with advancements in NGS panel design for liquid biopsy enabling more accurate and comprehensive genomic profiling. Two primary techniques for CTC enrichment are exosome isolation methods comparison and circulating tumor cells enrichment techniques. Exosomes, small extracellular vesicles, carry tumor-associated RNA and proteins, making them valuable for RNA sequencing in liquid biopsy and DNA methylation analysis in cancer.

On the other hand, CTC enrichment techniques, such as size-based filtration and immunomagnetic separation, isolate intact CTCs for proteomic profiling and therapeutic response monitoring with liquid biopsy. The plasma biomarker discovery pipeline is another crucial aspect of the market. Multiplexed assays for early cancer detection, such as miRNA profiling in cancer detection, have shown promising results in identifying cancer at its earliest stages. Furthermore, liquid biopsy plays a pivotal role in minimal residual disease assessment and drug resistance prediction, enabling personalized oncology and patient stratification using liquid biopsy markers. A significant number of companies are investing in liquid biopsy technology, with a notable trend towards non-invasive prenatal testing.

The diagnostic accuracy of cell-free DNA is a critical factor in its growing adoption, particularly in cases where traditional methods are invasive or less effective. However, the market faces challenges in clinical validation of liquid biopsy assays and addressing tumor heterogeneity assessment using liquid biopsy. Despite the competition, a minority of players dominate the high-end instrument market, accounting for over 40% of the total revenue. This highlights the importance of continued innovation and clinical validation in the market.

What are the key market drivers leading to the rise in the adoption of Liquid Biopsy Industry?

- The rising prevalence of cancer significantly contributes to the growth of the market.

- Cancer is a significant health concern, characterized by the abnormal division and growth of cells, influenced by a combination of hereditary and environmental factors. Over 80 distinct types of cancer exist, significantly impacting individuals worldwide. Among these, lung, liver, colon, stomach, and breast cancers are the most prevalent. Cancer ranks as a leading cause of morbidity globally, with European Commission estimates indicating that it affects men slightly more than women, accounting for 54% of new cases and 56% of related deaths in 2020.

- This continuous health challenge underscores the importance of ongoing research and advancements in cancer diagnosis, treatment, and prevention.

What are the market trends shaping the Liquid Biopsy Industry?

- Liquid biopsy is an emerging trend in the healthcare industry, with increasing funding and investment being allocated to its development.

- Liquid biopsy, an innovative diagnostic technology, has gained significant traction in recent years due to its potential as a research tool and advanced diagnostics solution. This market expansion has attracted substantial investment for the research and development of new technologies and the commercialization of liquid biopsy products. Notable companies, such as GRAIL, Guardant Health, Exosome Diagnostics, Pathway Genomics, and Inivata, have secured funding from various investors. For instance, Dxcover raised USD14.34 million in Series A and grant financing in February 2023. This funding supports the ongoing development of Dxcover's liquid biopsy platform for the detection of early-stage cancers, including brain and colorectal cancers.

- These investments are anticipated to fuel the expansion of the market throughout the forecast period.

What challenges does the Liquid Biopsy Industry face during its growth?

- The limited reimbursement for liquid biopsy procedures poses a significant challenge to the industry's growth trajectory. This issue, which significantly affects the financial viability of implementing and expanding the use of this advanced diagnostic technology, remains a key concern for industry stakeholders.

- The market for reimbursement and treatment monitoring in liquid biopsy is currently in a state of evolution, with varying adoption rates and reimbursement policies across sectors and geographies. In developed countries, the technology is gaining traction, while in developing nations, there is a significant market potential. However, reimbursement for liquid biopsy tests is not guaranteed, even after approval, due to its novelty and unproven status. Coverage depends on factors like the type of cancer, screening procedure, and therapy. In developed countries, reimbursement levels are low, while in some developing countries, it is non-existent.

- The market is a burgeoning field, with high adoption in developed countries and substantial growth opportunities in developing regions. It is essential to navigate the complexities of this market to optimize reimbursement and treatment monitoring strategies.

Exclusive Technavio Analysis on Customer Landscape

The liquid biopsy market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the liquid biopsy market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Liquid Biopsy Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, liquid biopsy market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A. Menarini Industrie Farmaceutiche Riunite Srl - The CELLSEARCH CTC Test is a groundbreaking liquid biopsy solution that identifies and isolates circulating tumor cells from a patient's blood sample, providing valuable diagnostic and prognostic information for various types of cancer. This advanced technology enables oncologists to monitor disease progression and response to treatment more effectively.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A. Menarini Industrie Farmaceutiche Riunite Srl

- ANGLE Plc

- Bio Rad Laboratories Inc.

- Bio Techne Corp.

- Biocept Inc.

- Biodesix Inc.

- CellMax Inc.

- CIRCULOGENE

- Exact Sciences Corp.

- F. Hoffmann La Roche Ltd.

- Guardant Health Inc.

- Illumina Inc.

- Inivata Ltd.

- MDXHEALTH SA

- Mesa Laboratories Inc.

- Myriad Genetics Inc.

- Novogene Co. Ltd.

- OncoCyte Corp.

- QIAGEN NV

- SAGA Diagnostics AB

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Liquid Biopsy Market

- In January 2024, Thermo Fisher Scientific, a leading biotech company, announced the launch of its Oncomine Lung cfDNA Assay, a liquid biopsy test designed for the detection and monitoring of lung cancer through circulating tumor DNA (ctDNA) in plasma. This test is expected to enhance early detection and improve patient outcomes (Thermo Fisher Scientific Press Release).

- In March 2024, Illumina, a global leader in genomic sequencing and array-based solutions, entered into a strategic collaboration with Grail, a leading liquid biopsy company, to develop and commercialize multi-cancer early detection tests. This collaboration aims to leverage Illumina's sequencing technologies and Grail's clinical expertise to bring innovative liquid biopsy solutions to the market (Illumina Press Release).

- In May 2024, Guardant Health, a leading liquid biopsy company, raised USD300 million in a Series E funding round, bringing the total funding raised to over USD1 billion. The funds will be used to expand commercial operations, accelerate product development, and invest in research and development (Guardant Health Press Release).

- In April 2025, the US Food and Drug Administration (FDA) granted marketing authorization to Qiagen's therascreen KRAS RGQ PCR Kit, a liquid biopsy test for the detection of KRAS gene mutations in circulating tumor DNA from various solid tumors. This approval marks a significant milestone in the market, as it represents the first FDA approval for a companion diagnostic liquid biopsy test (Qiagen Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Liquid Biopsy Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.2% |

|

Market growth 2024-2028 |

USD 3696.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

19.78 |

|

Key countries |

US, Canada, Germany, UK, Japan, India, Australia, South Korea, UAE, Brazil, and Rest of World (RoW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the rapidly advancing field of healthcare diagnostics, next-generation sequencing (NGS) is revolutionizing the approach to personalized medicine. The integration of NGS technology into liquid biopsy techniques has led to significant strides in the detection and monitoring of various cancer types. Protein biomarkers and circulating RNA, including ctDNA mutation detection, have emerged as crucial components of this evolving landscape. Patient stratification, facilitated by these advanced techniques, is enabling more effective therapeutic response and improved cancer monitoring. NGS sequencing and multiplex assays have become essential tools for identifying mutation burden and epigenetic alterations, providing valuable insights into tumor heterogeneity and drug resistance.

- RNA sequencing and sample preparation methods have expanded the scope of liquid biopsy, allowing for the detection of cancer subtypes and disease progression. The application of proteomic analysis, plasma biomarkers, and microrna profiling to liquid biopsy further enhances its potential. Minimal residual disease and tumor-derived vesicles are increasingly being targeted for early cancer detection and non-invasive diagnostics. Liquid biopsy techniques have shown promise in the detection of circulating tumor cells, exosomes isolation, and digital PCR. These advancements contribute to the ongoing evolution of cancer care, offering new opportunities for early detection, personalized treatment, and improved patient outcomes. The integration of liquid biopsy into genomic profiling and targeted therapy is a significant development in the field of oncology.

- The continuous unfolding of market activities and evolving patterns in this area reflect the growing importance of these techniques in cancer care.

What are the Key Data Covered in this Liquid Biopsy Market Research and Growth Report?

-

What is the expected growth of the Liquid Biopsy Market between 2024 and 2028?

-

USD 3.7 billion, at a CAGR of 25.2%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Cancer applications and Non-cancer applications), Technology (CTC and ctDNA and Exosome and RNA), Geography (North America, Europe, Asia, and Rest of World (ROW)), Sample Type (Blood, Urine, Cerebrospinal Fluid (CSF), and Others), Cancer Type (Lung, Breast, Colorectal, Prostate, and Others.), and End-User (Hospitals & Clinics, Diagnostic Labs, Research Institutes, and Pharma/Biotech.)

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing incidence of cancer, Limited reimbursement for liquid biopsy

-

-

Who are the major players in the Liquid Biopsy Market?

-

Key Companies A. Menarini Industrie Farmaceutiche Riunite Srl, ANGLE Plc, Bio Rad Laboratories Inc., Bio Techne Corp., Biocept Inc., Biodesix Inc., CellMax Inc., CIRCULOGENE, Exact Sciences Corp., F. Hoffmann La Roche Ltd., Guardant Health Inc., Illumina Inc., Inivata Ltd., MDXHEALTH SA, Mesa Laboratories Inc., Myriad Genetics Inc., Novogene Co. Ltd., OncoCyte Corp., QIAGEN NV, and SAGA Diagnostics AB

-

Market Research Insights

- The market encompasses cancer diagnostics utilizing non-invasive blood-based testing for disease monitoring, treatment selection, and early detection. This sector continues to advance with significant strides in assay development, biomarker discovery, and data analysis. The limit of detection for these tests has decreased, enabling the identification of minimal residual disease and predictive biomarkers. Personalized oncology and precision medicine applications are gaining traction, with clinical trials underway to validate the clinical utility of these approaches. Assay performance and diagnostic accuracy are crucial factors driving market growth. For instance, molecular diagnostics based on next-generation sequencing (NGS) workflow have shown analytical validity in detecting genetic mutations associated with various cancers.

- Prognostic and diagnostic biomarkers play a pivotal role in cancer prognosis and treatment monitoring. The integration of NGS technology in liquid biopsy assays is expected to enhance assay development and regulatory approval processes. Sample processing techniques have improved, ensuring high-quality data for clinical validation. The market's potential is substantial, with an estimated 15 million liquid biopsy tests projected to be performed annually by 2025, up from 3 million in 2020. This growth signifies a promising future for this evolving and dynamic market.

We can help! Our analysts can customize this liquid biopsy market research report to meet your requirements.

RIA -

RIA -