Liver Cirrhosis Therapeutics Market Size 2024-2028

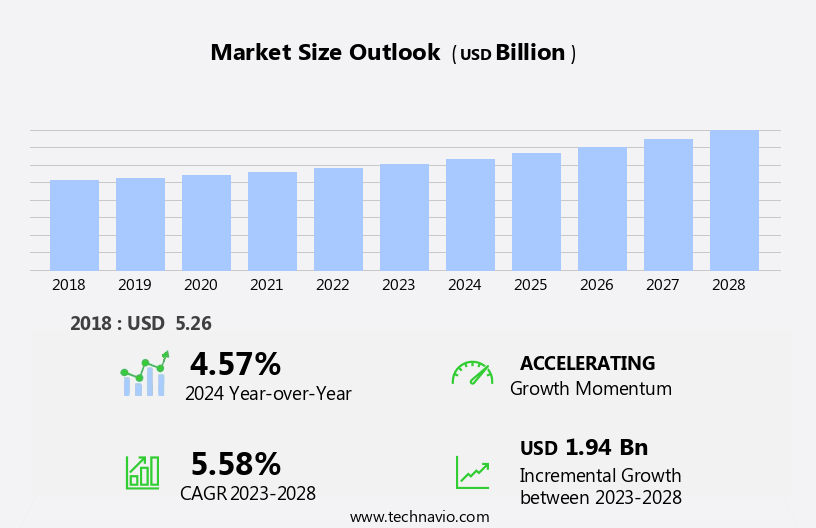

The liver cirrhosis therapeutics market size is forecast to increase by USD 1.94 billion at a CAGR of 5.58% between 2023 and 2028.

- The market is experiencing significant growth due to the rising incidence of liver cancer, which is a major cause of liver cirrhosis. According to the American Cancer Society, there will be an estimated 42,220 new cases of liver cancer in the United States alone in 2021. This trend is expected to continue, driving demand for effective therapeutic solutions. Another key trend in the market is the shift towards personalized medicine. With advances in genomic research and precision medicine, there is a growing opportunity for targeted therapies that cater to the unique needs of individual patients. However, the high cost of liver cirrhosis therapeutics remains a significant challenge.

- Many existing treatments are expensive and may not be accessible to all patients, limiting their widespread adoption. Despite these challenges, the market presents significant opportunities for companies seeking to innovate and provide cost-effective solutions. Strategic collaborations, regulatory approvals, and investments in research and development are expected to drive growth in the market. Companies that can successfully navigate these challenges and deliver effective, affordable therapeutic options will be well-positioned to capitalize on the growing demand for liver cirrhosis treatments.

What will be the Size of the Liver Cirrhosis Therapeutics Market during the forecast period?

- The market is experiencing significant activity due to the increasing prevalence of liver diseases, such as non-alcoholic fatty liver disease (NAFLD) and hepatocellular carcinoma (HCC). Novel drugs, including Vosevi and Mavyret, are gaining traction in the market as effective treatments for viral hepatitis B (HBV) and C. Research institutions, such as the American Association for the Study of Liver Diseases (AASLD), are actively engaged in exploring new treatments and therapies for liver cirrhosis, alcoholic liver disease, and chronic hepatitis. Anti-viral drugs are a key focus area in the market, as they offer effective solutions for treating hepatitis B and C.

- The liver failure market, including cirrhosis, is witnessing a rise in research activities due to the high incidence of systemic inflammation and the need for advanced treatments. Molecular hepatology and frontiers in medicine are also contributing to the development of new therapeutics for liver diseases. Lifestyle factors, such as alcohol consumption, are major contributors to liver cirrhosis. The market for liver cirrhosis therapeutics is expected to grow as the demand for effective treatments for liver diseases continues to increase. The International Liver Transplant Society (ILTS) and other organizations are working to improve access to liver transplants and other advanced treatments for patients with liver cirrhosis.

- The market for liver cirrhosis therapeutics is dynamic, with ongoing research and development in areas such as molecular hepatology and systemic inflammation. The use of advanced technologies and innovative approaches is driving the market forward, offering new opportunities for companies and investors. Key entities in the market include BMC Infectious Diseases, Cystic Fibrosis, Ildlt, and Veridos, among others. These organizations are contributing to the development of new treatments and therapies for liver diseases, including liver cirrhosis. The market for liver cirrhosis therapeutics is expected to continue growing as the demand for effective treatments increases and new technologies and approaches are developed.

How is this Liver Cirrhosis Therapeutics Industry segmented?

The liver cirrhosis therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Oral

- Injection

- End-user

- Hospitals

- Clinics

- Research and academic institutes

- Geography

- North America

- US

- Europe

- Germany

- UK

- Middle East and Africa

- APAC

- China

- Japan

- South America

- Rest of World (ROW)

- North America

By Type Insights

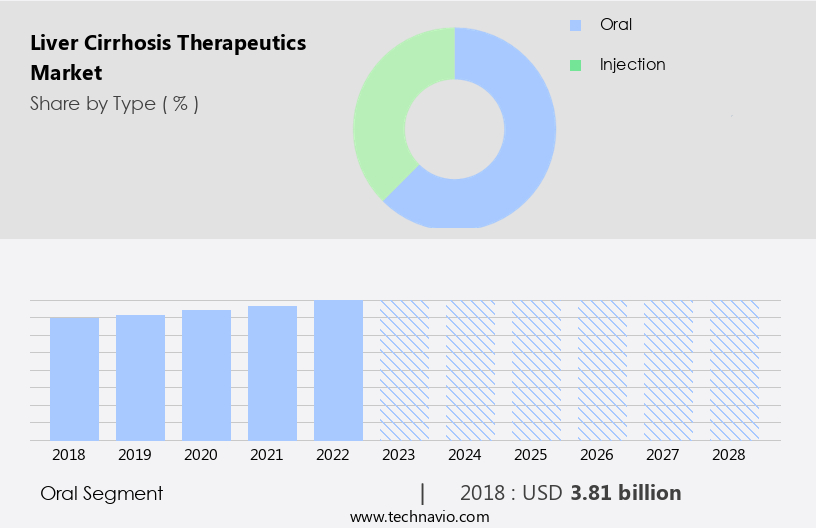

The oral segment is estimated to witness significant growth during the forecast period.

The liver cirrhosis treatment market is witnessing a significant shift towards oral medications, with obeticholic acid being a notable innovation. This trend is driven by the geriatric population's increasing preference for patient-friendly treatments and the convenience of oral administration. The demand for oral therapies, including those for non-alcoholic fatty liver disease (NAFLD) and antifibrotic medications, is on the rise. This development is influenced by the healthcare industry's focus on improving treatment adherence and the convenience that oral medications offer. The emergence of novel oral formulations targeting specific pathways in liver cirrhosis highlights the potential of this therapeutic approach.

The hepatology community is actively researching new treatments for various liver diseases, such as hepatocellular carcinoma, chronic hepatitis, and cirrhosis. Academic institutes, hospitals, and clinics are investing in awareness programs and research activities to address the challenges posed by systemic inflammation, infections, and liver failure. Hepatitis B and C continue to be major health concerns, with the development of anti-viral drugs like Zepatier, Mavyret, and Vosevi offering promising solutions. The side-effects of medications and immunosuppressants used in liver transplants are significant market restraints. However, the potential for better treatment methods and the development of novel drugs, such as Alpha-1 antitrypsin and iLDLT, provide opportunities for growth.

The role of hepatology journals, including the Hepatology journal, Frontiers in Medicine, and Molecular Hepatology, in disseminating research findings and advancing the field is invaluable. The market is also impacted by lifestyle factors, such as alcohol consumption and alcohol abuse, which contribute to liver cirrhosis and other liver diseases. The need for effective treatments for these conditions is pressing, and ongoing research into novel therapies and preventive measures is essential. The liver cirrhosis treatment market is a dynamic and evolving landscape, with a focus on improving patient outcomes and addressing the complex challenges posed by liver diseases.

Get a glance at the market report of share of various segments Request Free Sample

The Oral segment was valued at USD 3.81 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

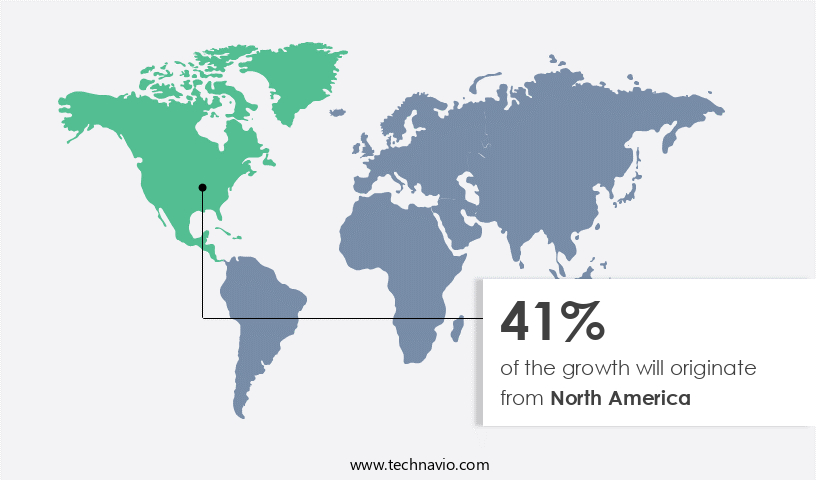

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in the US is experiencing significant growth due to several factors. The elderly population, living with conditions such as hepatocellular carcinoma, chronic hepatitis, and cirrhosis, is expanding. This demographic shift increases the demand for effective liver cirrhosis treatments. Furthermore, the rapidly changing lifestyle, with its associated health risks like alcohol consumption and syphilis infections, contributes to the market's expansion. Pharmaceutical companies are investing heavily in research activities to develop novel drugs and improve treatment methods. For instance, FDA-approved Obeticholic acid is gaining popularity for its ability to treat liver fibrosis caused by non-alcoholic steatohepatitis (NASH). Other notable treatments include Mavyret for hepatitis C, Vosevi for hepatitis B, and immunosuppressants for liver transplants.

Despite these advancements, market restraints persist. Side-effects of medications and the high cost of treatment remain significant challenges. However, awareness programs and academic institutes are working to address these issues. For example, the American Association for the Study of Liver Diseases (AASLD) and the International Liver Transplantation Society (ILTS) are actively promoting research and education in hepatology. Moreover, the healthcare infrastructure, including hospitals and clinics, is evolving to accommodate the increasing demand for liver cirrhosis treatment. Home care services and antibiotics for liver infections are also becoming more accessible. In summary, the market in the US is expanding due to the growing elderly population, increasing awareness, and advanced healthcare infrastructure.

Despite challenges like side-effects and high costs, pharmaceutical companies and academic institutions are working to develop better treatment methods and make them more accessible.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Liver Cirrhosis Therapeutics Industry?

- Increasing incidence of liver cancer is the key driver of the market.

- The market is experiencing significant growth due to the escalating prevalence of liver diseases, such as hepatitis and non-alcoholic fatty liver disease (NAFLD). According to the World Health Organization (WHO), approximately 325 million individuals worldwide are affected by viral hepatitis, increasing the risk of liver cirrhosis. Furthermore, the rising incidence of metabolic syndrome and obesity-related disorders, including NAFLD, is fueling the demand for effective treatments.

- NAFLD currently impacts around 25% of the global population, emphasizing the importance of advanced and accessible therapies. The increasing risk of cirrhosis associated with specific liver diseases is projected to propel the expansion of the market during the forecast period.

What are the market trends shaping the Liver Cirrhosis Therapeutics Industry?

- Trend towards personalized medicine is the upcoming market trend.

- The market is witnessing a shift towards personalized medicine, which involves customizing treatment plans based on unique patient characteristics. This approach considers genetic composition, liver function, and medication response to maximize therapeutic results, minimize side effects, and enhance overall patient quality of life. For instance, genetic profiling can identify specific biomarkers influencing drug metabolism, enabling the prescription of optimal medications for individual patients.

- This trend signifies a departure from the traditional one-size-fits-all strategy and a move towards improved patient outcomes and increased therapeutic efficacy in The market. The progression of precision medicine is leading this paradigm change.

What challenges does the Liver Cirrhosis Therapeutics Industry face during its growth?

- High cost of liver cirrhosis therapeutics is a key challenge affecting the industry growth.

- The market faces a significant challenge due to the high cost of treatments, which limits access for certain patient populations. Immunosuppressants and antiviral medications for hepatitis require extended courses, leading to increased healthcare expenses. Advanced therapies like liver transplantation, which can cure end-stage cirrhosis, come with substantial costs related to the surgery, post-procedure recovery, and lifelong immunosuppressive drugs. Individuals in regions with limited healthcare resources or inadequate coverage are disproportionately affected by this financial burden.

- The high cost of liver cirrhosis treatments poses a significant barrier to effective care and underscores the need for affordable solutions and increased healthcare coverage.

Exclusive Customer Landscape

The liver cirrhosis therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the liver cirrhosis therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, liver cirrhosis therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in liver cirrhosis treatment through innovative siRNA-based targeted therapies, aimed at restoring functional liver cells for patients with advanced liver diseases. This approach focuses on inhibiting specific genes responsible for disease progression, offering a potential solution for those with end-stage liver conditions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Alnylam Pharmaceuticals Inc.

- Astellas Pharma Inc.

- AstraZeneca Plc

- CSL Ltd.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Gilead Sciences Inc.

- GlaxoSmithKline Plc

- Gwo Xi Stem Cell Applied Technology

- Johnson and Johnson

- Kezar Life Sciences Inc.

- Merck KGaA

- Novartis AG

- Novo Nordisk AS

- Pfizer Inc.

- Protagonist Therapeutics Inc.

- Tessera Therapeutics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Liver cirrhosis, a chronic and progressive condition characterized by the replacement of healthy liver tissue with scar tissue, is a significant public health concern worldwide. The disease is often associated with various risk factors, including an elderly population, chronic hepatitis infections, alcohol consumption, and systemic inflammation. The market is experiencing robust growth due to the increasing burden of the disease and the need for better treatment methods. The elderly population is a major demographic affected by liver cirrhosis, as age is a well-established risk factor for the disease. With an aging population, the number of individuals diagnosed with liver cirrhosis is expected to rise, leading to a surge in demand for effective therapeutics.

Chronic hepatitis infections, such as HBV and HCV, are another significant driver of the market. These infections can lead to cirrhosis if left untreated, making the development of effective antiviral drugs a priority. The rapidly changing lifestyle and increasing prevalence of alcohol abuse are also contributing to the growing burden of liver cirrhosis. Alcoholic liver disease is a leading cause of cirrhosis, and the market for therapeutics to treat this condition is expected to grow significantly. Syphilis, a sexually transmitted infection, can also lead to liver cirrhosis if left untreated, highlighting the importance of awareness programs and investment in research activities.

Despite the progress made in the development of new drugs, such as Zepatier and Mavyret, market restraints remain. Side-effects of medications and the high cost of treatment are major challenges that need to be addressed. The liver diseases market is highly competitive, with several players vying for market share. Academic institutes and research organizations are also actively contributing to the development of novel drugs and treatment methods for liver cirrhosis. The liver cirrhosis treatment market is witnessing significant activity, with several new drugs and treatment methods under development. For instance, IL-1 receptor antagonist (IL-1Ra) and Alpha-1 antitrypsin have shown promise in treating cirrhosis.

The use of home care and hospitals and clinics for the treatment of liver cirrhosis is also gaining popularity, as it offers several advantages, including improved patient outcomes and reduced healthcare costs. The market for liver cirrhosis therapeutics is expected to face several challenges in the coming years. The high cost of treatment and the side-effects of medications are major concerns, and addressing these challenges will require significant investment and research. The development of better treatment methods and the use of immunosuppressants and antibiotics to prevent infections in liver transplant patients are expected to offer significant opportunities for market growth.

The liver diseases market is a complex and dynamic field, with several entities contributing to its evolution. The market is influenced by various factors, including demographic trends, lifestyle factors, research activities, and market dynamics. Understanding these factors and their impact on the market is crucial for stakeholders looking to invest in or enter the market. In conclusion, the market is experiencing robust growth due to the increasing burden of the disease and the need for better treatment methods. The market is influenced by several factors, including an aging population, chronic hepatitis infections, alcohol consumption, and research activities. Addressing the challenges of high cost and side-effects of medications will be crucial for market growth.

The development of novel drugs and treatment methods, such as IL-1Ra and Alpha-1 antitrypsin, offers significant opportunities for market expansion. The liver diseases market is a complex and dynamic field, and understanding its evolution is crucial for stakeholders looking to invest or enter the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.58% |

|

Market growth 2024-2028 |

USD 1.94 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.57 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Liver Cirrhosis Therapeutics Market Research and Growth Report?

- CAGR of the Liver Cirrhosis Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the liver cirrhosis therapeutics market growth of industry companies

We can help! Our analysts can customize this liver cirrhosis therapeutics market research report to meet your requirements.

RIA -

RIA -