Manometry System Market Size 2024-2028

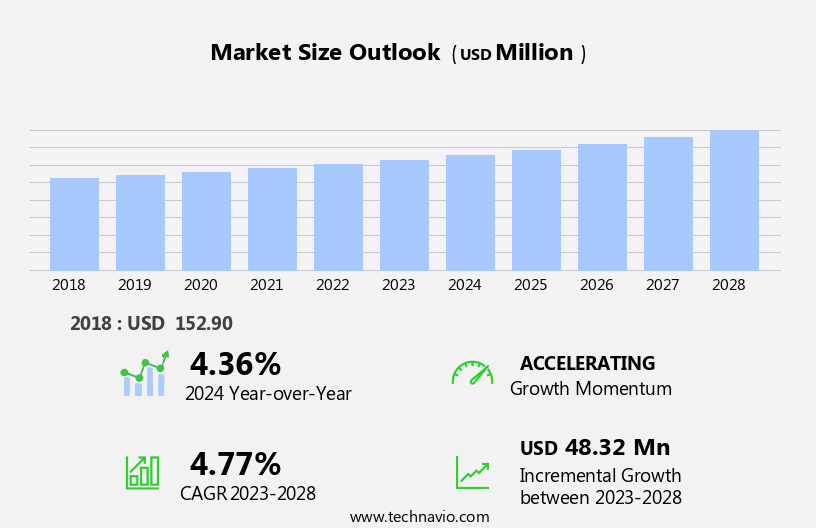

The manometry system market size is forecast to increase by USD 48.32 million, at a CAGR of 4.77% between 2023 and 2028.

- The market is witnessing significant growth, driven by the increasing incidence of gastrointestinal diseases. The diagnostic and therapeutic importance of manometry systems in assessing gastrointestinal motility disorders has led to a rising demand for these systems. Additionally, the focus on high-resolution manometry systems is gaining momentum due to their ability to provide more accurate diagnoses and improved patient outcomes. However, the market faces challenges, including frequent manometry system recalls, which can impact market confidence and hinder market growth. Manufacturers must address these challenges by ensuring product quality and reliability, while also investing in research and development to innovate and differentiate their offerings.

- Companies seeking to capitalize on market opportunities should also consider expanding their product portfolios to cater to the diverse needs of healthcare providers and patients. Overall, the market presents a promising landscape for growth, with opportunities for companies to address unmet needs and improve patient care.

What will be the Size of the Manometry System Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market encompasses a range of technologies and applications, with ongoing advancements shaping its dynamic landscape. These systems are integral to assessing various gastrointestinal functions, including esophageal pressure studies, perfusion tests, antral pressure measurements, and high-resolution manometry. Esophageal manometry, employing manometric catheters, plays a crucial role in diagnosing motor disorders. Perfusion studies, utilizing water perfusion, provide valuable insights into mucosal wave propagation and mucosal relaxation. Antral pressure assessment aids in identifying gastroparesis and other motility disorders. High-resolution manometry, featuring pressure waveforms and small bowel motility analysis, offers enhanced diagnostic accuracy. Clinical applications span from diagnosing swallowing disorders to monitoring patient response to therapy.

Innovations continue to unfold, with data analysis software, calibration procedures, and multichannel recording systems streamlining data acquisition and interpretation. Solid bolus transit, gastric emptying, and pyloric function studies further expand the scope of manometry systems. Solid-state sensors, electrical impedance, and wireless manometry are among the emerging technologies, offering improved patient comfort and ease of use. Pressure mapping and pressure topography provide detailed insights into intraluminal pressure distributions, enhancing diagnostic precision. Manometry systems continue to evolve, with continuous advancements in technology and clinical applications, ensuring their indispensable role in gastrointestinal diagnosis and patient monitoring.

How is this Manometry System Industry segmented?

The manometry system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Diagnostic centers

- Specialty clinics

- Academic research institutes

- Product

- Manometry system

- Manometry software

- Manometry system sheath and catheters

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

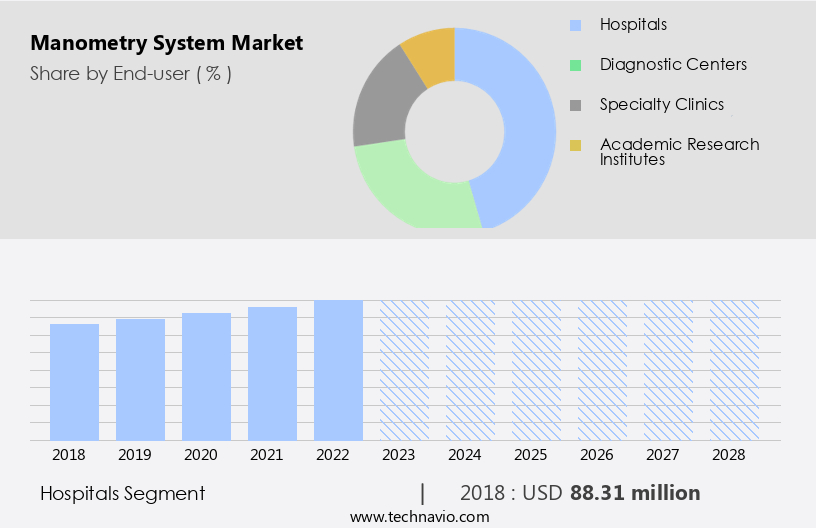

The hospitals segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant advancements, particularly in hospitals, due to the availability of specialized equipment and favorable reimbursement policies. Hospitals, both public and private, with over 500 beds are major contributors to the market's growth. These institutions have state-of-the-art infrastructure to diagnose and monitor chronic conditions, such as gastrointestinal diseases. Manometric catheters and data analysis software are integral components of manometry systems used in hospitals for the assessment of various gastrointestinal functions, including colonic motility, solid bolus transit, gastric emptying, pyloric function, and impedance planimetry. High-resolution manometry, with its pressure waveforms and multichannel recording capabilities, plays a crucial role in diagnosing esophageal peristalsis and swallowing disorders.

Pressure mapping and calibration procedures ensure diagnostic accuracy. Hospitals also employ wireless manometry and intraluminal pressure sensors for patient monitoring. Perfusion studies using water perfusion and antral pressure measurement are other clinical applications of manometry systems. Small bowel motility assessment is another emerging application, which will further boost the market's growth.

The Hospitals segment was valued at USD 88.31 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

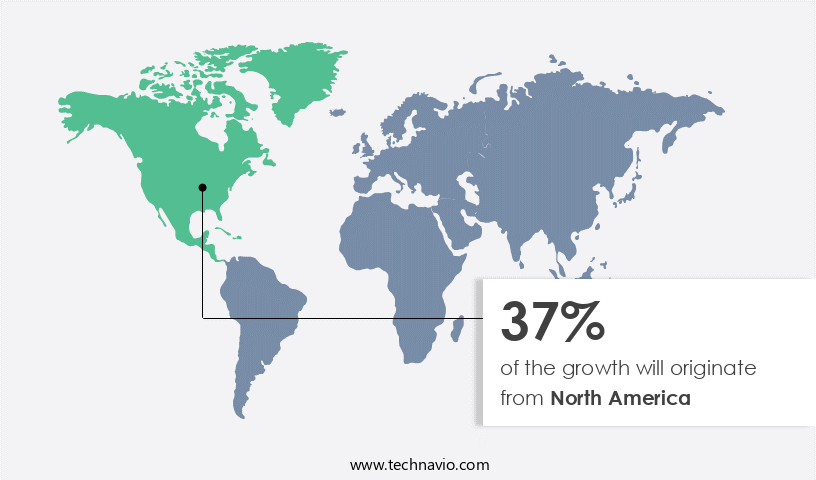

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to the increasing incidence and prevalence of chronic gastrointestinal diseases and rising healthcare expenditure. Advanced data analysis software and manometric catheters are essential tools in diagnosing and monitoring various gastrointestinal disorders, including colonic motility, gastric emptying, pyloric function, and swallowing disorders. Impedance planimetry and high-resolution impedance technologies are increasingly being used for gastric motility studies, providing valuable insights into antral pressure and bolus transit. Pharmaceutical and biotechnology companies are investing heavily in research and development to create sophisticated healthcare equipment, such as high-resolution manometry systems. These systems offer pressure waveforms, small bowel motility assessments, and pressure mapping, enabling accurate diagnosis and effective treatment of gastrointestinal disorders.

Clinical applications of manometry systems extend to diagnostic accuracy, patient monitoring, and catheter placement. The demand for wireless manometry systems and multichannel recording devices is increasing due to their ease of use and improved patient comfort. Esophageal peristalsis assessment and lower esophageal sphincter function studies are crucial in diagnosing conditions like gastroesophageal reflux disease. Perfusion studies using water perfusion and pressure sensors help evaluate the function of the pylorus and antrum. Swallowing disorders, such as achalasia and dysphagia, are common gastrointestinal conditions that require manometry testing. Calibration procedures ensure accurate measurement of intraluminal pressure, while solid-state sensors and electrical impedance technologies offer improved sensitivity and reliability.

In summary, the market in North America is driven by the increasing demand for advanced diagnostic tools and the growing prevalence of chronic gastrointestinal diseases.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Manometry System Industry?

- The rising prevalence of gastrointestinal diseases serves as the primary catalyst for market growth in this sector.

- The gastrointestinal disease landscape is witnessing a notable increase due to factors such as improper diet, inactive lifestyle, stress, food sensitivity, and bacterial or viral infections. Chronic conditions like ulcerative colitis, hemorrhoids, Inflammatory Bowel Disease (IBD), and GERD have become prevalent, leading to various medical complications and disabilities if left untreated. GERD, a chronic condition affecting individuals of all age groups, is associated with complications such as erosive esophagitis, esophageal stricture, Barrett esophagus, dental diseases, and asthma. To diagnose and assess GERD, medical professionals employ manometry tests, specifically esophageal manometry. Manometry systems utilize manometric catheters to measure the contractions and relaxations of the muscles in the gastrointestinal tract.

- Data analysis software plays a crucial role in interpreting the data collected from these tests, allowing for a more accurate diagnosis and treatment plan. Technologies like impedance planimetry and high-resolution impedance are employed in manometry systems to evaluate gastric motility, gastric emptying, and pyloric function. These advanced techniques offer improved diagnostic accuracy and enable better understanding of gastrointestinal conditions. In conclusion, the growing prevalence of gastrointestinal diseases necessitates the use of advanced diagnostic tools, such as manometry systems, to ensure timely and accurate diagnoses. The integration of data analysis software and advanced technologies like impedance planimetry and high-resolution impedance further enhances the diagnostic capabilities of these systems.

What are the market trends shaping the Manometry System Industry?

- High-resolution manometry systems are gaining significant attention in the medical industry due to their increasing use in diagnosing gastrointestinal motility disorders. The market trend is shifting towards these advanced systems as they offer higher accuracy and improved diagnostic capabilities compared to traditional manometry methods.

- High-resolution manometry (HRM) has revolutionized the clinical assessment of esophageal motility disorders by providing more detailed and accurate information than traditional manometry. HRM uses a manometry catheter with up to 36 pressure sensors, allowing for intraluminal esophageal pressure signals to be transmitted and analyzed in greater detail. This advanced technology enables the evaluation of esophageal motility patterns, including pressure waveforms in the lower esophageal sphincter and antral pressure, which are crucial in diagnosing conditions such as gastroesophageal reflux disease and achalasia. HRM also plays a significant role in the diagnostic process of small bowel motility disorders, as it provides valuable data on perfusion studies using water perfusion techniques.

- The clinical applications of HRM extend beyond the diagnosis of motility disorders, as it can also be used to assess the effectiveness of various treatments and therapies. Overall, HRM's diagnostic accuracy and ability to provide comprehensive information on esophageal motility make it an essential tool in gastrointestinal clinical practice.

What challenges does the Manometry System Industry face during its growth?

- The recurring recalls of manometry systems pose a significant challenge to the industry's growth trajectory. Manometry systems, essential for diagnosing gastrointestinal disorders, face frequent recalls due to various reasons, including technical glitches and regulatory compliance issues. This persistent challenge hampers industry progress and increases operational costs for healthcare providers.

- Manometry systems are essential diagnostic tools used in the healthcare industry to measure intraluminal pressure in various parts of the gastrointestinal tract, such as the esophagus. These systems consist of a pressure mapping system and a data acquisition system. The pressure mapping system includes solid-state sensors that measure electrical impedance to detect bolus transit and intraluminal pressure. The data acquisition system records and analyzes the data obtained from the manometry sensors. Calibration procedures are crucial in manometry systems to ensure accurate pressure readings. Manufacturers follow stringent calibration processes to maintain the system's accuracy and reliability. Wireless manometry systems offer enhanced flexibility and mobility, making them increasingly popular in clinical settings.

- Despite the benefits, manometry systems are subject to recalls due to safety or functionality issues. Product recalls can result from various reasons, including design errors, software glitches, or other technical problems. Manufacturers prioritize patient safety and issue recalls to address these issues and ensure the safe and effective use of their manometry systems. Manometry system manufacturers face the challenge of maintaining the highest standards of safety and accuracy while continuously innovating to improve the functionality and usability of their products. Regular calibration procedures and rigorous quality control measures help mitigate the risk of product recalls and ensure the delivery of reliable and effective manometry systems to healthcare providers and patients.

Exclusive Customer Landscape

The manometry system market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the manometry system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, manometry system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alacer Biomedica - The company specializes in advanced manometry systems, including high resolution esophageal manometry (MULTIPLEX) and high resolution anorectal manometry, providing valuable diagnostic insights for gastrointestinal and anorectal disorders.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alacer Biomedica

- Creo Medical Ltd.

- Daffodil Health Technology Service Co.

- Diversatek Inc.

- Innologic

- LABORIE MEDICAL TECHNOLOGIES CORP.

- Medica S.p.A.

- Medspira LLC

- Medtronic Plc

- Mui Scientific

- Standard Instruments GmbH

- TECHNOMED SYSTEMS

- THD S.p.A

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Manometry System Market

- In January 2024, Medtronic plc, a leading medical technology, services, and solutions company, announced the launch of its new Esophageal Manometry System, the MMS-7000 Series, designed to improve the diagnosis and treatment of gastrointestinal motility disorders (Medtronic Press Release, 2024).

- In March 2024, Philips Healthcare, a global leader in health technology, entered into a strategic partnership with the University of California, San Francisco (UCSF) to develop advanced manometry technologies for the diagnosis and treatment of gastrointestinal disorders (Philips Healthcare Press Release, 2024).

- In May 2024, Boston Scientific Corporation, a medical device manufacturer, completed the acquisition of EndoChoice, Inc., a leading provider of diagnostic and therapeutic solutions for gastrointestinal diseases, significantly expanding its presence in the manometry systems market (Boston Scientific Press Release, 2024).

- In February 2025, the US Food and Drug Administration (FDA) granted clearance for Olympus Corporation's new manometry system, the Endo-MRI Manometry System, which combines manometry and magnetic resonance imaging (MRI) for more accurate diagnosis of gastrointestinal disorders (Olympus Press Release, 2025).

Research Analyst Overview

- The esophageal manometry market encompasses innovative systems designed for diagnosing and monitoring various motility disorders, including esophageal spasms and deglutition disorders. System calibration plays a crucial role in ensuring accurate procedural techniques and clinical trials. Gastric emptying rate and bolus transport are essential diagnostic criteria for functional dyspepsia and gastroesophageal reflux. Signal processing and pressure waveform analysis are integral to interpreting manometry data, while clinical outcome measures and imaging integration provide valuable insights. Impedance manometry and high-resolution manometry offer enhanced diagnostic capabilities for motility disorders. Sensor placement, such as antral manometry, and wireless capsule endoscopy contribute to improved patient selection and diagnostic accuracy.

- Colonic manometry and colonic transit time are essential for diagnosing colonic motility disorders. Pressure sensor technology and data visualization tools facilitate efficient device validation and enable better understanding of complex manometry data. Gastric manometry remains a critical diagnostic tool for various gastrointestinal conditions. Motility disorders, like esophageal spasms and gastroesophageal reflux, require precise diagnostic criteria and effective treatment strategies. Proper patient selection and sensor placement are essential for accurate diagnosis and clinical outcome measures. Advancements in manometry technology, including signal processing, imaging integration, and high-resolution manometry, offer significant improvements in diagnostic accuracy and patient care.

- Continued research and development in this field will undoubtedly contribute to better understanding and management of various gastrointestinal disorders.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Manometry System Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.77% |

|

Market growth 2024-2028 |

USD 48.32 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

4.36 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Manometry System Market Research and Growth Report?

- CAGR of the Manometry System industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the manometry system market growth of industry companies

We can help! Our analysts can customize this manometry system market research report to meet your requirements.

RIA -

RIA -