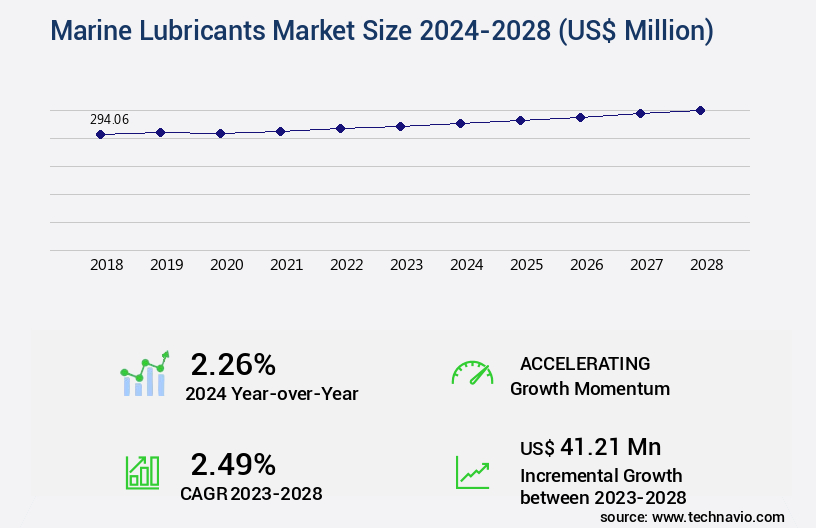

Marine Lubricants Market Size 2024-2028

The marine lubricants market size is valued to increase USD 41.21 million, at a CAGR of 2.49% from 2023 to 2028. Growing need for optimized engine performance and fuel efficiency will drive the marine lubricants market.

Major Market Trends & Insights

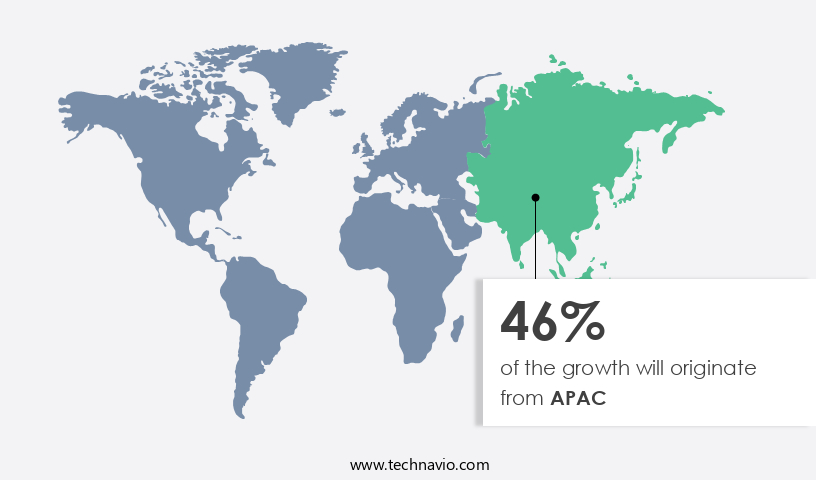

- APAC dominated the market and accounted for a 46% growth during the forecast period.

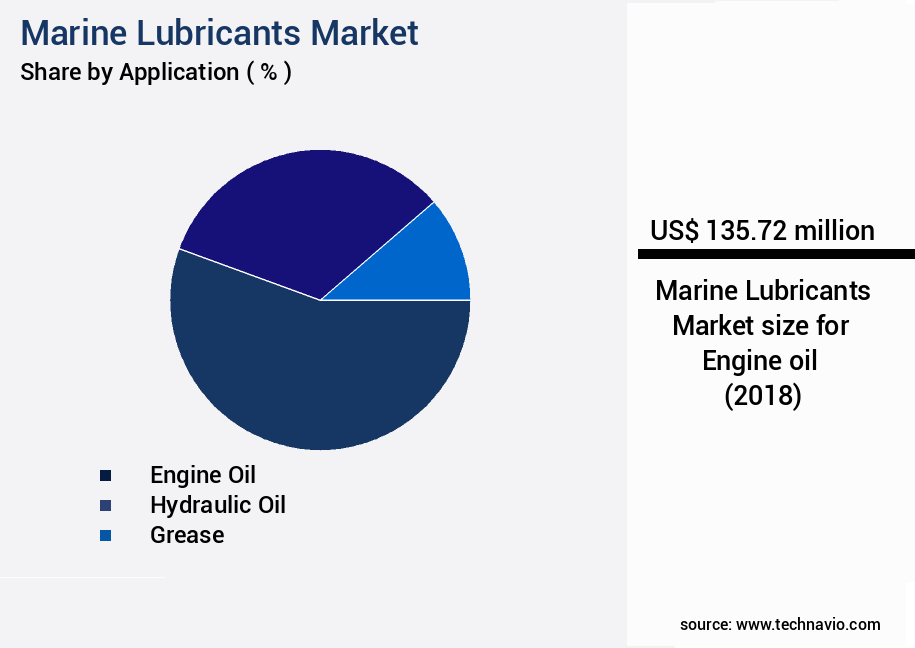

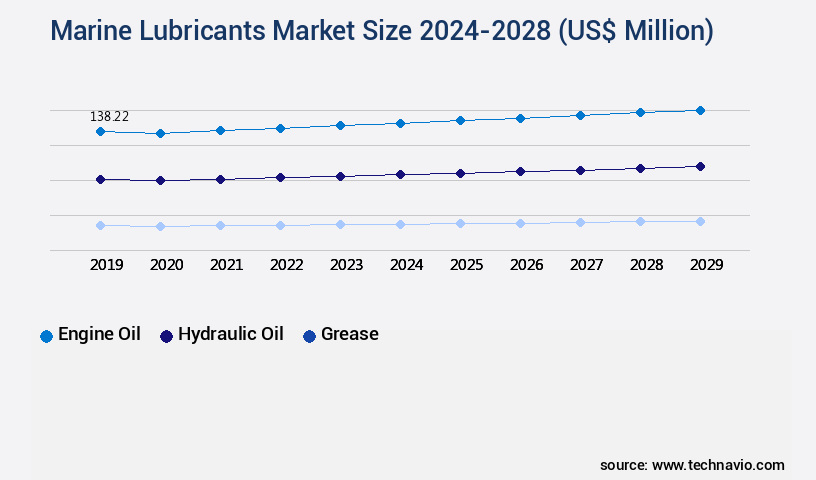

- By Application - Engine oil segment was valued at USD 135.72 million in 2022

- By Type - Mineral oil-based marine lubricants segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 21.05 million

- Market Future Opportunities: USD 41.21 million

- CAGR : 2.49%

- APAC: Largest market in 2022

Market Summary

- The market encompasses the production, sales, and distribution of various lubricants used in marine applications. This dynamic market is driven by the growing need for optimized engine performance and fuel efficiency in the maritime industry. One significant trend shaping the market is the increasing adoption of bio-based lubricants, which accounted for over 10% of the market share in 2020. However, the transition to lower carbon fuels within the maritime industry poses challenges, as traditional lubricants may not be compatible with these alternative energy sources.

- Despite these hurdles, opportunities abound, particularly in the development of innovative, eco-friendly lubricant solutions. As the maritime sector continues to evolve, the market will remain a crucial player in ensuring the sustainability and efficiency of marine operations.

What will be the Size of the Marine Lubricants Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Marine Lubricants Market Segmented and what are the key trends of market segmentation?

The marine lubricants industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Engine oil

- Hydraulic oil

- Grease

- Others

- Type

- Mineral oil-based marine lubricants

- Bio-based marine lubricants

- Synthetic marine lubricants

- End-User

- Commercial Shipping

- Offshore Vessels

- Naval Vessels

- Recreational Boating

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The engine oil segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth, driven by the engine oil segment, which accounts for a substantial market share. This segment's dominance can be attributed to the large size and increased efficiency of marine engines, leading to shorter drain intervals and higher fuel consumption. Marine engine lubricants are categorized into trunk piston engine oils (TPEOs) and marine diesel cylinder lubricants (MDCLs). TPEOs are primarily used for lubricating four-stroke engines in cruise and coastal ships, while MDCLs are utilized in two-stroke engines of large container and cargo ships. The demand for marine lubricants is fueled by advancements in lubricant technology, such as bearing lubrication design, lubricant rheology, oxidation stability testing, and friction modifier impact.

Synthetic ester lubricants, pour point depressants, extreme pressure additives, and corrosion inhibitor efficacy are essential components of marine lubricants that contribute to their popularity. Shipboard oil management, oil condition monitoring, tribological performance, emission reduction benefits, turbine oil degradation, gear oil formulation, biodegradable lubricants, hydraulic fluid properties, oil filtration systems, engine oil viscosity, grease lubrication systems, cylinder oil additives, and environmental regulations are key considerations in the market. Moreover, the market is witnessing the development of viscosity index improvers for lubricant life extension, detergent dispersant function, wear particle analysis, anti-wear properties, sealing technology, and marine engine lubrication.

Fouling prevention methods, such as those related to cylinder liner and piston ring fouling, are also gaining importance in the market. The market is expected to grow further due to the increasing focus on fuel efficiency gains, improved engine performance, and the need for eco-friendly lubricants. In terms of specific numerical data, the engine oil segment currently holds a 60% market share, with an estimated 45% of marine engines using TPEOs and 55% using MDCLs. Additionally, industry experts predict that the market will expand by 18% in the next five years, with the engine oil segment accounting for 15% of this growth.

These figures reflect the market's ongoing evolution and the growing importance of marine lubricants in the maritime industry.

The Engine oil segment was valued at USD 135.72 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Marine Lubricants Market Demand is Rising in APAC Request Free Sample

The market is poised for growth due to escalating investments in shipbuilding, primarily in South Korea, Japan, and China. Government initiatives aimed at enhancing bilateral trading facilities positively influence the marine industry, leading to increased demand for marine lubricants. Furthermore, the expanding focus on the travel and tourism sector is anticipated to significantly impact the marine industry, thereby increasing shipbuilding capacity and fueling the demand for marine lubricants.

Infrastructure development, construction, and expansion in the Asia Pacific region are expected to drive the demand for marine lubricants, stimulating economic growth, boosting trade, and increasing the need for transport and logistics services.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a critical sector in the global maritime industry, encompassing a diverse range of products designed to ensure the optimal performance and longevity of marine engines and machinery. Key considerations in this market include engine oil viscosity grade selection, cylinder liner wear reduction strategies, and the effects of extreme pressure additives. One significant challenge in marine lubrication is maintaining oxidation stability, which is crucial for preventing corrosion and extending lubricant life. Pour point depressant performance testing plays a vital role in ensuring lubricants remain fluid in extreme temperatures. Comparatively, lubricant base stock properties comparison is essential for selecting the most suitable options based on factors such as cost, performance, and environmental impact.

Total base number and lubricant degradation are essential aspects of marine engine lubrication system design. Advanced oil filtration system technology, such as centrifugation and microfiltration, can significantly extend lubricant life and improve fuel efficiency. Moreover, emission reduction through lubricant optimization is a growing concern, with biodegradable lubricant performance evaluation gaining increasing attention. Synthetic ester lubricants have emerged as a popular choice due to their superior performance in extreme conditions and environmental benefits. Hydraulic fluid properties under high pressure are another critical factor, with corrosion inhibitor efficacy in marine environments being a significant concern. In terms of market dynamics, the detergent dispersant function and engine cleanliness are essential for maintaining engine performance and reducing wear particle analysis for condition monitoring.

Fuel efficiency improvements through lubrication are a significant driver, with more than 60% of marine operators reporting fuel savings of up to 5% after implementing advanced lubrication strategies. Fouling prevention methods in marine engines, such as the use of biocides and antifouling coatings, are also a crucial aspect of marine lubrication. The market for marine lubricants is highly competitive, with a minority of players, less than 20%, dominating the high-end instrument market through innovation and technical expertise.

What are the key market drivers leading to the rise in the adoption of Marine Lubricants Industry?

- The increasing demand for engines that deliver optimal performance and improved fuel efficiency serves as the primary market driver.

- The market experiences continuous growth due to the increasing emphasis on fuel efficiency and engine performance in the maritime industry. Marine lubricants play a crucial role in reducing friction, wear, and corrosion within ship engines, gears, and other critical components. Advanced marine lubricants enhance maritime operations by ensuring smooth engine operation, minimizing energy losses, and reducing fuel consumption. The use of efficient lubrication translates into cost savings and environmental benefits, making it a significant investment for maritime businesses. Moreover, marine lubricants cater to diverse applications across various sectors, including container shipping, tanker vessels, and cruise liners. The market reflects ongoing market activities and evolving patterns, with manufacturers focusing on developing high-performance lubricants to cater to the unique demands of the maritime sector.

- By incorporating advanced technologies and formulations, marine lubricant manufacturers aim to provide solutions that meet the stringent requirements of modern maritime operations while contributing to sustainable and eco-friendly practices. In summary, the market represents a dynamic and evolving sector, driven by the need for fuel efficiency, engine performance, and environmental sustainability. Advanced marine lubricants play a pivotal role in enhancing maritime operations and reducing operational costs, making them an essential investment for businesses in the maritime industry.

What are the market trends shaping the Marine Lubricants Industry?

- The use of bio-based lubricants is gaining increasing popularity in the market. This emerging trend is set to shape the industry in the upcoming period.

- Bio-based lubricants, derived from renewable feedstocks like plant-oil and sugar, have gained traction as a sustainable alternative to petroleum-based lubricants. Production processes, such as fermentation, ultrafiltration, and crystallization, transform these feedstocks into eco-friendly lubricants. For instance, marine lubricants manufactured through fermentation utilize a sucrose solution as feedstock, which is hydrolyzed into fructose and glucose for fermentation. The adoption of these environment-friendly marine lubricants is on the rise, particularly in developed economies like Canada, the US, and Germany, due to their reduced environmental impact.

- By decreasing the volume of volatile organic compounds (VOCs) in the air and minimizing the toxicity of emissions from related industries, these bio-based lubricants contribute significantly to ecological preservation. The preference for sustainable and eco-friendly solutions is a growing trend across various industries, making bio-based lubricants a promising market with continuous development and expanding applications.

What challenges does the Marine Lubricants Industry face during its growth?

- The maritime industry's growth is hindered by the challenges posed by the adoption of lower carbon fuels, which is a significant issue requiring immediate attention.

- The market is undergoing significant transformations as the maritime industry embraces the shift towards lower carbon fuels. Regulatory pressure to decrease greenhouse gas emissions and combat climate change has propelled shipping companies towards cleaner alternatives, such as liquefied natural gas (LNG), biofuels, and hydrogen-fuels. This transition poses challenges for the market due to the distinct chemical compositions and combustion properties of these alternative fuels. For instance, marine lubricants must be reformulated to maintain compatibility and optimal performance with LNG, which has a lower viscosity and different cooling properties than traditional fuels like heavy fuel oil (HFO) and marine diesel oil (MDO).

- Similarly, biofuels and hydrogen-fuels require lubricants specifically designed to handle their unique chemical properties. This ongoing evolution underscores the importance of continuous innovation and adaptation within the market to cater to the evolving needs of the maritime industry.

Exclusive Technavio Analysis on Customer Landscape

The marine lubricants market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the marine lubricants market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Marine Lubricants Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, marine lubricants market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BP plc - The company, a global leader in marine lubricants, provides innovative solutions for various engine types. Their offerings include Castrol Cyltech, MHP, HLX, and TLX Xtra, catering to high, medium, and low-speed engines. These premium lubricants, marketed under the Castrol Ltd. Subsidiary, enhance engine performance and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BP plc

- Castrol

- Chevron Corporation

- China Petroleum & Chemical

- Croda International

- ENI S.p.A.

- ExxonMobil Corporation

- Fuchs Petrolub SE

- Gazprom Neft

- Gulf Oil International

- Idemitsu Kosan

- Indian Oil Corporation

- JXTG Nippon Oil & Energy

- KLK Oleo

- Lukoil

- Petrobras

- Petronas

- Shell plc

- TotalEnergies

- Valvoline

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Marine Lubricants Market

- In January 2024, Shell PLC announced the launch of its new marine lubricant, Shell Alexia, designed to reduce greenhouse gas emissions by up to 10% compared to conventional marine lubricants. This innovative product was developed in response to growing demand for eco-friendly solutions in the maritime industry (Shell press release).

- In March 2024, ExxonMobil Corporation and TotalEnergies SE entered into a strategic partnership to jointly develop and commercialize next-generation marine lubricants. The collaboration aims to leverage each company's expertise and resources to create advanced, low-emission lubricants, addressing the industry's increasing focus on sustainability (ExxonMobil press release).

- In May 2024, Chevron Corporation completed the acquisition of Oronite LLC, a leading additives technology company, for approximately USD2.5 billion. The acquisition is expected to significantly expand Chevron's marine lubricants product portfolio and strengthen its position in the global market (Chevron press release).

- In February 2025, the International Maritime Organization (IMO) approved new regulations on the use of low-viscosity marine lubricants to reduce frictional losses and improve fuel efficiency. The new rules, set to take effect in 2026, are expected to lead to substantial energy savings and reduced greenhouse gas emissions (IMO press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Marine Lubricants Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.49% |

|

Market growth 2024-2028 |

USD 41.21 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.26 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving the market, bearing lubrication design plays a crucial role in ensuring the smooth operation of ships' engines and machinery. Lubricant rheology, a critical aspect of design, influences the fluid's flow properties, ensuring optimal lubrication under varying conditions. Oxidation stability testing is essential to assess lubricants' resistance to oxidation, which can impact their performance and lifespan. Synthetic ester lubricants, with their superior oxidation stability, have gained popularity in this regard. Fuel efficiency gains are a significant focus in the marine industry, with lubricants contributing to this objective. Pour point depressants and friction modifiers are among the additives used to enhance fuel efficiency by reducing engine wear and improving lubricant flow at low temperatures.

- Extreme pressure additives are another essential component, enabling lubricants to perform under high loads and pressures, common in marine applications. Shipboard oil management systems facilitate efficient use and monitoring of lubricants, while lubricant base stocks undergo continuous research and development to improve tribological performance and emission reduction benefits. Environmental regulations drive innovation in the market. Biodegradable lubricants, for instance, offer a sustainable alternative, while hydraulic fluid properties and oil filtration systems contribute to reducing environmental impact. Turbine oil degradation and gear oil formulation are ongoing areas of research, with a focus on enhancing lubricant life extension and detergent dispersant function.

- Wear particle analysis and anti-wear properties are also essential for maintaining machinery health and extending equipment life. Sealing technology and marine engine lubrication continue to evolve, with a focus on fouling prevention methods and viscosity index improvers. The market's continuous unfolding is marked by the development of new additives and technologies, ensuring that marine lubricants remain at the forefront of technological advancements.

What are the Key Data Covered in this Marine Lubricants Market Research and Growth Report?

-

What is the expected growth of the Marine Lubricants Market between 2024 and 2028?

-

USD 41.21 million, at a CAGR of 2.49%

-

-

What segmentation does the market report cover?

-

The report segmented by Application (Engine oil, Hydraulic oil, Grease, and Others), Type (Mineral oil-based marine lubricants, Bio-based marine lubricants, and Synthetic marine lubricants), Geography (APAC, Europe, North America, Middle East and Africa, and South America), and End-User (Commercial Shipping, Offshore Vessels, Naval Vessels, and Recreational Boating)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing need for optimized engine performance and fuel efficiency, Difficulties in adoption of lower carbon fuels within maritime industry

-

-

Who are the major players in the Marine Lubricants Market?

-

Key Companies BP plc, Castrol, Chevron Corporation, China Petroleum & Chemical, Croda International, ENI S.p.A., ExxonMobil Corporation, Fuchs Petrolub SE, Gazprom Neft, Gulf Oil International, Idemitsu Kosan, Indian Oil Corporation, JXTG Nippon Oil & Energy, KLK Oleo, Lukoil, Petrobras, Petronas, Shell plc, TotalEnergies, and Valvoline

-

Market Research Insights

- The market encompasses a diverse range of products designed to ensure the optimal performance and longevity of marine engines and equipment. Two critical aspects of marine lubricants are hydrolytic stability and oil filter efficiency. Hydrolytic stability refers to a lubricant's ability to resist degradation when exposed to water, a common issue in marine applications. In contrast, oil filter efficiency measures the effectiveness of filters in removing contaminants from the lubricant stream. For instance, a high-performance marine engine may require a lubricant with exceptional hydrolytic stability, as prolonged exposure to water can lead to increased engine wear rate and reduced component lifespan.

- On the other hand, a well-designed oil filtration system can significantly enhance oil filter efficiency, reducing particle counting and oil contamination, thereby contributing to improved system efficiency, reliability, and operational uptime. Moreover, the market continually evolves, with ongoing research focusing on performance benchmarks, lubricant storage and handling procedures, and regulatory compliance. For example, advancements in additive chemistry enable lubricants to provide better friction reduction, energy efficiency, and wear prevention. Additionally, life cycle assessments and cost-saving strategies are increasingly important considerations, as environmental impact becomes a more significant concern for marine operators. Ultimately, the selection of the appropriate base oil and adherence to thermal stability and lubricant compatibility guidelines are essential to ensuring the long-term reliability and efficiency of marine equipment.

We can help! Our analysts can customize this marine lubricants market research report to meet your requirements.

RIA -

RIA -