Medical Devices Market Size 2026-2030

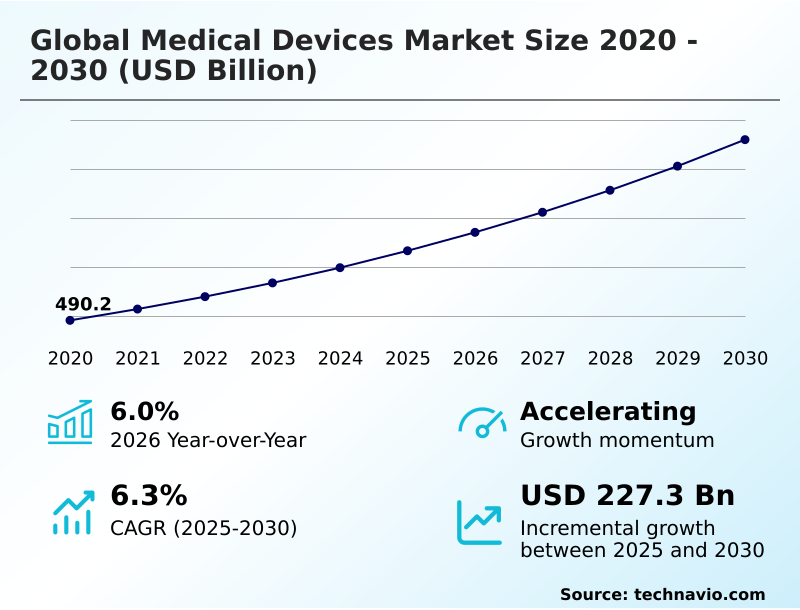

The medical devices market size is valued to increase by USD 227.3 billion, at a CAGR of 6.3% from 2025 to 2030. Technological advancements and digital transformation in medical infrastructure will drive the medical devices market.

Major Market Trends & Insights

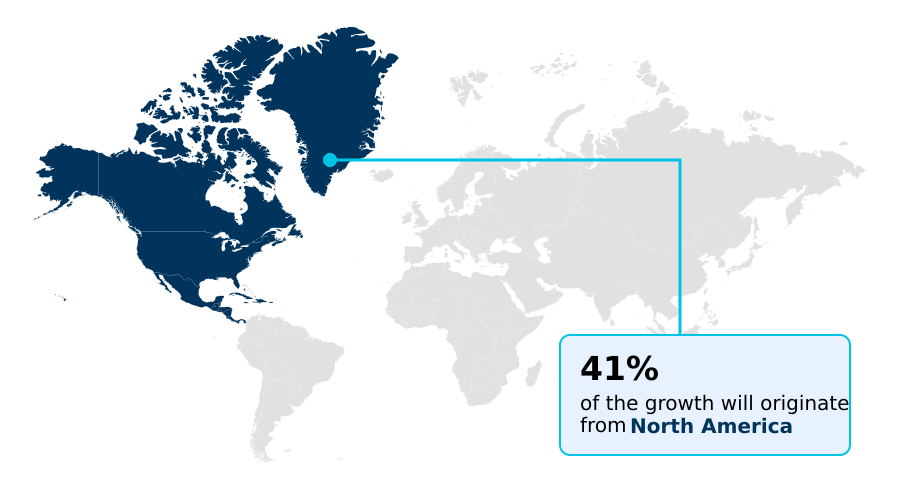

- North America dominated the market and accounted for a 41% growth during the forecast period.

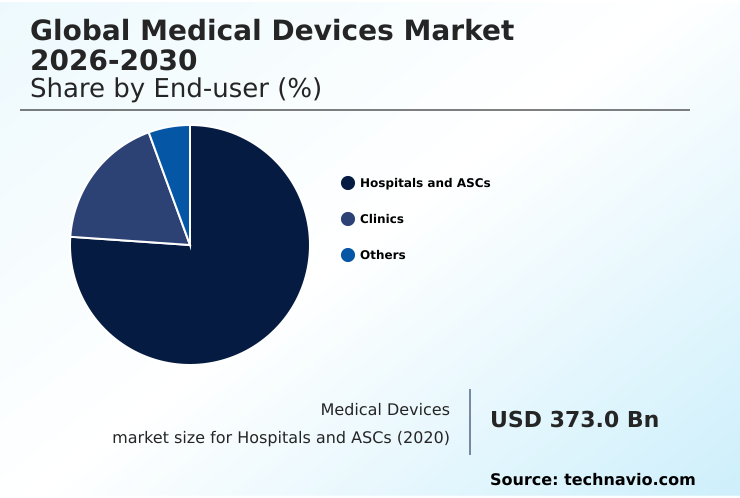

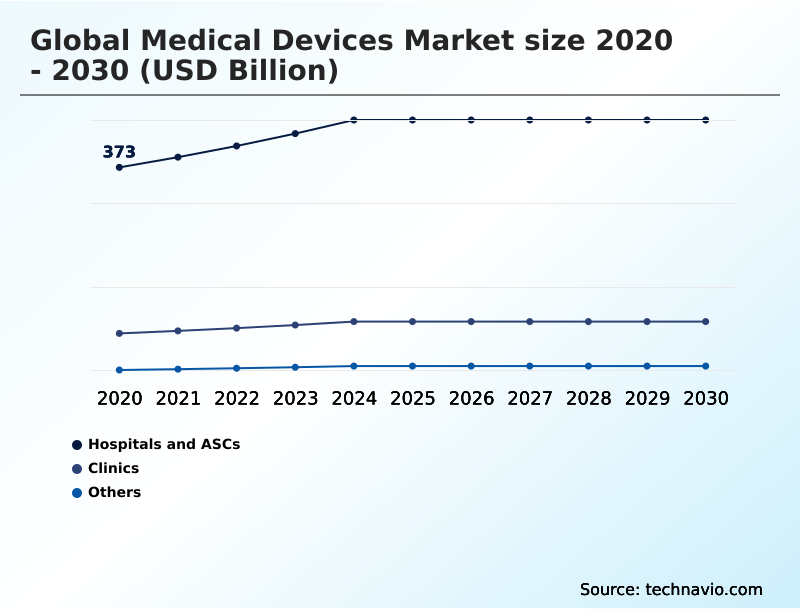

- By End-user - Hospitals and ASCs segment was valued at USD 453.8 billion in 2024

- By Product - Diagnostic devices segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 369.6 billion

- Market Future Opportunities: USD 227.3 billion

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The medical devices market is navigating a period of significant transformation, driven by the convergence of digital health technologies and an increasing focus on patient-centric care. The proliferation of the internet of medical things and the integration of AI-integrated medical devices are enhancing diagnostic accuracy and enabling predictive, rather than reactive, treatment models.

- A key trend involves the development of medical-grade wearables and remote patient monitoring tools that provide continuous, real-time data, allowing for better management of chronic diseases outside traditional hospital settings. For instance, a healthcare system can leverage this data to optimize resource allocation, anticipating patient needs and reducing readmissions by ensuring timely intervention.

- However, this increased connectivity introduces substantial challenges, particularly concerning cybersecurity threats and the need for robust data security protocols to protect sensitive patient information. Navigating complex and fragmented regulatory frameworks, such as requirements for software as a medical device, also adds significant cost and time to the product development lifecycle, shaping the competitive landscape for all participants.

What will be the Size of the Medical Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Medical Devices Market Segmented?

The medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals and ASCs

- Clinics

- Others

- Product

- Diagnostic devices

- Therapeutic devices

- Monitoring devices

- Assistive and rehabilitation devices

- Others

- Application

- Cardiovascular

- Orthopedic

- Diagnostic imaging

- Dental

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals and ascs segment is estimated to witness significant growth during the forecast period.

The hospitals and ASCs segment is shaped by investments in technologies that improve clinical workflows and patient outcomes. Facilities are adopting solutions like transcatheter aortic valve replacement systems and smart implants to meet the demands of value-based care.

The integration of augmented reality guidance in surgical settings is becoming a key differentiator, enabling higher precision.

This shift is driven by the need to manage complex procedures efficiently, with advanced robotic-assisted surgical platforms proven to reduce post-operative complications by over 30%.

As surgical procedures migrate to outpatient settings, the demand for compact, high-performance monitoring devices and innovative point-of-care use technologies, such as force-sensing scalpels, is escalating, reinforcing the segment's critical role in the healthcare ecosystem.

The Hospitals and ASCs segment was valued at USD 453.8 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Devices Market Demand is Rising in North America Get Free Sample

The geographic landscape of the medical devices market is characterized by varied regional dynamics and growth trajectories.

North America remains the largest contributor, accounting for 41% of the market's incremental growth, driven by high R&D spending and the rapid adoption of advanced technologies like AI-powered prosthetic limbs.

The region's sophisticated healthcare infrastructure supports high-end innovations, with the US market valued at more than 17 times that of Canada.

Europe follows, contributing 30.93% to the growth, with a strong focus on regulatory modernization and the integration of systems like the european database on medical devices.

Meanwhile, Asia is the fastest-growing region, fueled by expanding healthcare access and government initiatives, such as production-linked incentive schemes, to boost domestic manufacturing of technologies including high-purity specialized polymers and diagnostic hardware.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global medical devices market 2026-2030 is increasingly defined by the application of sophisticated technologies to solve complex clinical challenges. Key advancements include AI applications in oncology and cardiology, which leverage advanced algorithms for predictive diagnostics.

- The regulatory environment is evolving to manage these innovations, with a strong focus on software as a medical device regulations and post-market surveillance for software as a medical device. In surgical applications, robotic-assisted neurological and orthopedic surgery is becoming more common, enhanced by technologies like augmented reality in minimally invasive surgery.

- This integration of hardware and software necessitates robust cybersecurity for internet of medical things, with specific cybersecurity protocols for connected medical devices becoming mandatory. The push for personalized medicine is evident in the development of 3D printing for patient-specific orthopedic implants and wearable biosensors for personalized treatment plans.

- The growth of remote patient monitoring for chronic diseases is supported by implantable sensors for cardiovascular monitoring and tele-rehabilitation using virtual reality platforms. To ensure product quality and availability, the industry is addressing supply chain resilience for medical components, while innovations in point-of-care molecular diagnostic testing are decentralizing diagnostics.

- For instance, facilities using physics-based digital twins for surgical validation have reported a 15% reduction in procedural planning time compared to traditional methods. The integration of AI with diagnostic hardware, combined with new biocompatible materials for dental and orthopedic implants and real-time data analytics in clinical workflows, is setting new standards for patient care.

What are the key market drivers leading to the rise in the adoption of Medical Devices Industry?

- Ongoing technological advancements and the digital transformation of medical infrastructure are key drivers of market growth.

- Market growth is fundamentally propelled by technological innovation within clinical workflows and the rising global burden of chronic diseases. The development of decision-support systems and the application of real-world data are enhancing diagnostic accuracy, with AI-integrated medical devices becoming standard.

- The world's aging demographic, with the number of individuals over 65 projected to reach 1.6 billion by 2050, creates a sustained demand for assistive and therapeutic devices like joint replacements and bone-graft handling systems.

- Cardiovascular diseases now affect over half a billion people globally, driving the need for cardiac monitors and implantable sensors. This demographic shift necessitates a transition to continuous management models supported by wearable defibrillators and advanced drug delivery systems.

What are the market trends shaping the Medical Devices Industry?

- The integration of artificial intelligence and machine learning technologies is an emerging trend, profoundly transforming diagnostic modalities across the healthcare industry.

- The market is being reshaped by the fusion of intelligent software and advanced hardware. The proliferation of medical-grade monitoring is enabling continuous data collection for chronic disease management, a trend underscored by a 40% improvement in signal-to-noise ratios in the latest wearable ECGs.

- In parallel, advancements in robotic-assisted surgical platforms, particularly the development of a miniaturized robotic arm and haptic feedback sensors, are making minimally invasive procedures more precise and accessible. Innovations like smart surgical tools and regenerative orthobiologics are improving surgical outcomes.

- Furthermore, the use of AI-enhanced endoscopes in ambulatory surgical centers has significantly increased the detection rate of early-stage gastrointestinal lesions, showcasing the tangible benefits of integrating AI with diagnostic hardware and machine learning components.

What challenges does the Medical Devices Industry face during its growth?

- Stringent regulatory compliance requirements and evolving certification mandates present a significant challenge to industry growth.

- The primary challenges facing the market revolve around navigating stringent regulatory landscapes and mitigating growing digital risks. The complexity of compliance, including mandates for the european database on medical devices and new electronic submission template requirements, creates significant hurdles.

- Simultaneously, the rise of the internet of medical things has led to escalating cybersecurity threats, with cyber incidents in healthcare surging by 55%. Ransomware attacks targeting legacy vulnerabilities in connected infrastructure are a critical concern, and the average cost of a data breach has risen to $0.5 million.

- These digital risks, combined with ongoing supply chain volatility and issues like buffer stock management, place considerable pressure on manufacturers, impacting both cost and time-to-market for new innovations.

Exclusive Technavio Analysis on Customer Landscape

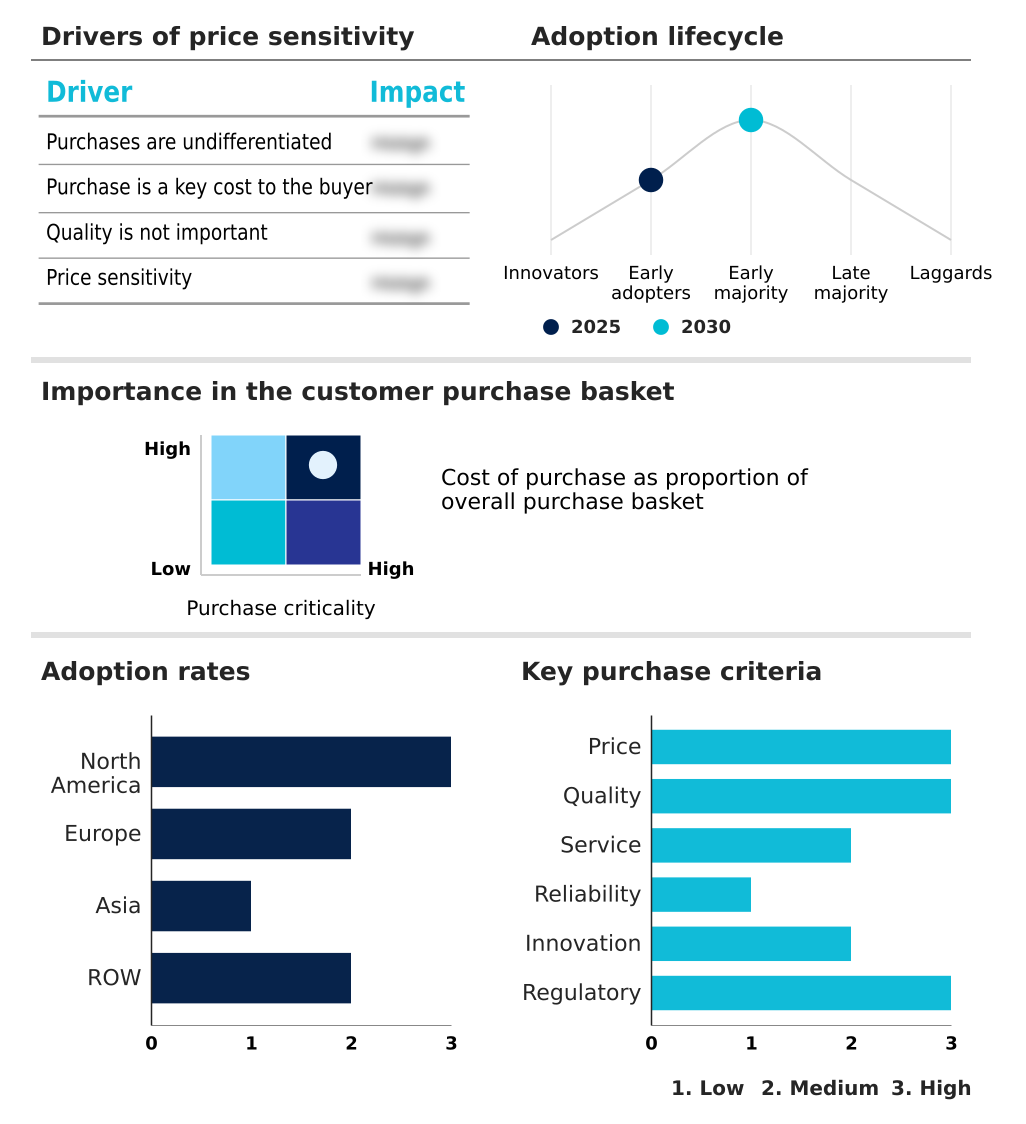

The medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Provides critical medical devices for cardiovascular and neuromodulation therapies, alongside a range of advanced, rapid diagnostic products for diverse clinical settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Alcon Inc.

- Baxter International Inc.

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Cardinal Health Inc.

- Danaher Corp.

- Dragerwerk AG and Co. KGaA

- Edwards Lifesciences Corp.

- FUJIFILM Holdings Corp.

- GE HealthCare Technologies

- Hologic Inc.

- Johnson and Johnson Services

- Koninklijke Philips NV

- Medtronic Plc

- Olympus Corp.

- Siemens Healthineers AG

- Smith and Nephew plc

- Stryker Corp.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical devices market

- In May, 2025, Nipro Europe Group announced a major expansion of its manufacturing facility in India to produce glass cartridges for dental and pen applications, aiming to meet rising local demand.

- In April, 2025, Smith and Nephew plc announced its acquisition of Integrity Orthopaedics to enhance its portfolio of niche orthopedic innovations and strengthen its market position.

- In March, 2025, Johnson and Johnson Services Inc. introduced its KINCISE 2 System, an automated surgical impactor, after receiving approval for both knee and hip revision surgeries.

- In January, 2025, GE HealthCare Technologies and Kalbe International inaugurated the first Indonesian production facility for computed tomography scanners to localize high-tech manufacturing and reduce import reliance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 320 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 227.3 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.0% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Saudi Arabia, UAE, Turkey, South Africa, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The medical devices market is undergoing a significant transformation, driven by technological convergence. The adoption of software as a medical device and AI-integrated medical devices is redefining clinical practice, with physics-based digital twins enabling virtual validation of robotic imaging. Key innovations include automated blood cell separators, cardiac monitors, and implantable sensors.

- The demand for joint replacements, wearable defibrillators, and advanced drug delivery systems is rising, alongside companion diagnostics and remote patient monitoring tools. The sector is advancing with new diagnostic hardware, medical-grade monitoring solutions, and robotic-assisted surgical platforms featuring haptic feedback sensors and force-sensing scalpels.

- Augmented reality guidance and virtual reality surgery are enhancing precision, while the development of a miniaturized robotic arm promises new possibilities in microsurgery. However, navigating the electronic submission template for the european database on medical devices poses a challenge.

- Cybersecurity for the internet of medical things is a major concern due to ransomware attacks and legacy vulnerabilities, which have seen a 55% surge in the healthcare sector. Production-linked incentive schemes and the use of high-purity specialized polymers are addressing just-in-time manufacturing risks.

- Technologies like transcatheter aortic valve replacement, photon counting computed tomography, capacitive micromachined technology, 3d printed titanium scaffolds, bioresorbable scaffolds, smart implants, and regenerative orthobiologics are pushing the boundaries of what is possible.

What are the Key Data Covered in this Medical Devices Market Research and Growth Report?

-

What is the expected growth of the Medical Devices Market between 2026 and 2030?

-

USD 227.3 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and ASCs, Clinics, Others), Product (Diagnostic devices, Therapeutic devices, Monitoring devices, Assistive and rehabilitation devices, and Others), Application (Cardiovascular, Orthopedic, Diagnostic imaging, Dental, Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Technological advancements and digital transformation in medical infrastructure, Stringent regulatory compliance and evolving certification mandates

-

-

Who are the major players in the Medical Devices Market?

-

Abbott Laboratories, Alcon Inc., Baxter International Inc., Becton Dickinson and Co., Boston Scientific Corp., Cardinal Health Inc., Danaher Corp., Dragerwerk AG and Co. KGaA, Edwards Lifesciences Corp., FUJIFILM Holdings Corp., GE HealthCare Technologies, Hologic Inc., Johnson and Johnson Services, Koninklijke Philips NV, Medtronic Plc, Olympus Corp., Siemens Healthineers AG, Smith and Nephew plc, Stryker Corp. and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market is advancing through the strategic adoption of digital health technologies that redefine clinical workflows and decision-support systems. The focus has shifted to predictive diagnostics, enabled by real-world data and machine learning components that improve diagnostic accuracy.

- Innovations in smart surgical tools and minimally invasive procedures are enhancing patient outcomes, supported by regulatory sandboxes that accelerate the approval of breakthrough devices. Telehealth platforms and medical-grade wearables are proliferating, driven by the need for remote patient monitoring tools. This evolution creates challenges around cybersecurity threats and data security protocols.

- As the industry grapples with supply chain volatility, strategies like nearshoring and reshoring are being implemented to manage inventory obsolescence and reduce reliance on a single source for critical components like diagnostic catheters.

- Implementation of voice-activated AI scribes has allowed physicians to dedicate 30% more time to direct patient interaction, while portable digital tools for home monitoring have cut hospital readmission rates by 25%.

We can help! Our analysts can customize this medical devices market research report to meet your requirements.

RIA -

RIA -