Medical Suction Devices Market Size 2024-2028

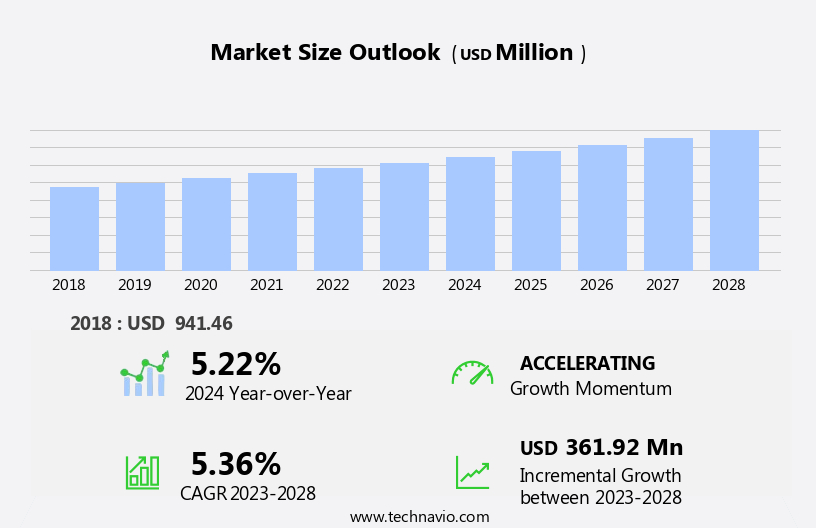

The medical suction devices market size is forecast to increase by USD 361.92 million, at a CAGR of 5.36% between 2023 and 2028.

- The market is driven by the increasing prevalence of chronic respiratory disorders, fueling the demand for effective and efficient suction devices. The market is also witnessing a surging trend towards portable and compact medical suction devices, catering to the needs of healthcare professionals for mobility and ease of use. However, challenges persist in the form of limited awareness and access to medical suction devices in underdeveloped countries, hindering market growth.

- Companies seeking to capitalize on market opportunities should focus on expanding their reach in emerging markets and investing in research and development to innovate portable and cost-effective solutions. Navigating these challenges requires strategic planning and a deep understanding of the evolving market landscape.

What will be the Size of the Medical Suction Devices Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in technology and increasing demand for effective and safe patient care solutions. Negative pressure therapy, a crucial application of medical suction devices, is used extensively in various sectors, including emergency response systems and surgical procedures. Pressure monitoring sensors, suction unit filtration, fluid level indicators, and suction regulator settings are essential components of these devices, ensuring optimal performance and patient safety. Suction canister capacity and vacuum regulation systems enable continuous suction, while suction power output varies depending on the specific application. Intermittent suction systems and emergency suction units are integral parts of trauma response and critical care settings.

Infection control protocols and noise reduction technology are crucial considerations in the design of medical suction devices. Anatomical suctioning and aspiration system design cater to the unique needs of different patient populations. Disposable suction tips and sterile suction containers facilitate efficient and hygienic use. Suction tubing materials and airflow control mechanisms contribute to the overall functionality and durability of the devices. Medical waste disposal and patient safety features are essential aspects of the design and maintenance of medical suction devices. Portable suction devices offer increased mobility and convenience, while battery-powered suction ensures uninterrupted use in remote settings. The market dynamics of medical suction devices are continuously unfolding, with ongoing developments in low-vacuum suction pumps, surgical suction tubing, and high-vacuum suction pumps.

The integration of advanced technologies, such as suction line clogging prevention and anatomical suctioning, further enhances the capabilities of these devices.

How is this Medical Suction Devices Industry segmented?

The medical suction devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Non-portable

- Portable

- Application

- Respiratory

- Gastric

- Others

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

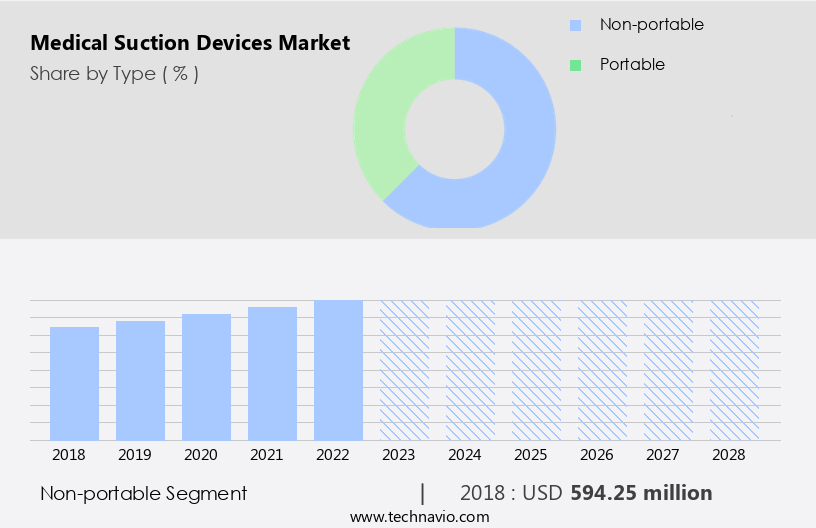

The non-portable segment is estimated to witness significant growth during the forecast period.

In the market, non-portable suction equipment is commonly used in stationary settings such as hospitals, clinics, and assisted living facilities. These devices, which are often connected to wall-mounted units or central vacuum systems, offer powerful suction capabilities. Their size and design make them less portable than handheld or portable devices. However, their strength is essential for various medical procedures, including wound care, respiratory therapy, endoscopy, and surgery. Non-portable suction devices come with additional features to ensure optimal performance and patient safety. Infection control protocols are crucial, and these devices often incorporate advanced filtration systems and sterile suction containers.

Patient interface design is another essential aspect, with ergonomic features and disposable tips to minimize cross-contamination. Suction equipment maintenance is vital to maintain performance and prevent issues like suction line clogging. Noise reduction technology is also incorporated to minimize disturbances for patients and staff. Emergency response systems are integrated into some devices to provide immediate suction in critical situations. The design of aspiration systems includes considerations for anatomical suctioning and pressure monitoring sensors to ensure accurate suction levels. Vacuum regulation systems and continuous suction systems help maintain consistent suction power output. Suction canister capacity is another essential factor, with larger canisters providing extended operation times.

Battery-powered portable suction devices offer more mobility but may not match the suction power of non-portable devices. Low-vacuum suction pumps are an alternative for situations where less suction power is required. Suction tubing materials and fluid collection systems are designed to minimize airflow control issues and medical waste disposal concerns. In conclusion, non-portable medical suction devices play a significant role in various medical procedures due to their powerful suction capabilities and additional features designed for infection control, patient safety, and ease of maintenance.

The Non-portable segment was valued at USD 594.25 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

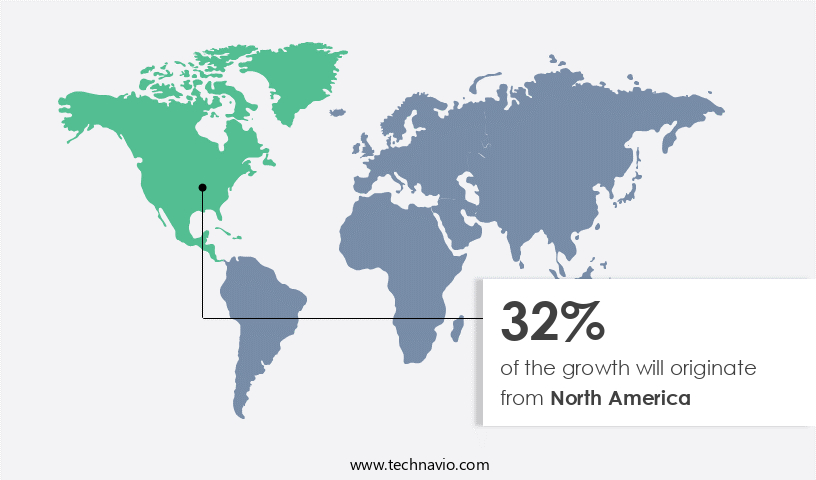

North America is estimated to contribute 32% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing growth due to increasing healthcare costs and the demand for advanced medical equipment. Technology advancements and the rise in surgical procedures are significant contributing factors. In the global market for medical suction devices, North America holds a notable share. Both portable and non-portable suction devices are essential tools in various medical applications, such as respiratory therapy, airway clearance, and surgery. They aid in eliminating secretions, fluids, and foreign objects from the body, ensuring open airways and preventing infections. Patient interface design, noise reduction technology, and infection control protocols are crucial aspects of modern medical suction devices.

Intermittent suction systems and suction equipment maintenance are essential for optimal performance and patient safety. Low-vacuum suction pumps and various suction tubing materials cater to diverse medical needs. Anatomical suctioning and aspiration system design enhance the efficiency and precision of these devices. Disposable suction tips, pressure monitoring sensors, suction unit filtration, fluid level indicators, and suction regulator settings are integral components of medical suction devices. Suction canister capacity, vacuum regulation systems, and continuous suction systems cater to various clinical requirements. Trauma suction devices, high-vacuum suction pumps, surgical suction tubing, and portable suction devices are essential for diverse medical applications.

Medical waste disposal, airflow control mechanisms, sterile suction containers, and suction catheter designs further expand the market's scope. Battery-powered suction devices offer mobility and convenience. Negative pressure therapy and emergency response systems are vital applications for medical suction devices, ensuring patient safety and improving overall healthcare outcomes. Suction line clogging and emergency suction units are essential considerations in the design and functionality of these devices. Infection control protocols and patient safety features are paramount in the development of advanced medical suction devices.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Medical Suction Devices Industry?

- The prevalence of chronic respiratory disorders has significantly driven market growth due to the increasing global incidence and prevalence of conditions such as asthma, chronic obstructive pulmonary disease (COPD), and pulmonary fibrosis.

- The market is experiencing significant growth due to the increasing prevalence of chronic respiratory illnesses worldwide. Chronic conditions such as bronchitis, asthma, and COPD are on the rise, driven by factors like smoking, air pollution, and aging populations. Medical suction devices play a crucial role in managing these illnesses by clearing the respiratory tract's secretions and opening airways through the application of negative pressure. These devices are indispensable tools for controlling the symptoms and complications of long-term respiratory diseases. Moreover, the market is also driven by advancements in patient interface design, intermittent suction systems, and noise reduction technology.

- Emergency response systems and emergency suction units are also gaining popularity due to their ability to provide immediate relief during respiratory emergencies. Suction equipment maintenance is another critical factor influencing market growth, as proper maintenance ensures the devices function optimally and effectively. However, suction line clogging remains a challenge, necessitating ongoing research and development efforts to address this issue. Overall, the market is expected to continue its growth trajectory, driven by the increasing burden of respiratory diseases and advancements in technology.

What are the market trends shaping the Medical Suction Devices Industry?

- The trend in the medical device market is shifting towards portable and compact medical suction devices due to increasing demand. These devices offer convenience and mobility, making them a popular choice among healthcare professionals and patients alike.

- The market is experiencing significant growth due to the increasing demand for portable and compact equipment. Technological advancements have enabled the development of lightweight, easily maneuverable devices, making them ideal for various clinical settings such as emergency rooms, ambulances, and home healthcare. The emphasis on infection control and patient safety is a major driving factor behind this trend. Low-vacuum suction pumps and disposable suction tips are becoming increasingly popular due to their ability to minimize the risk of cross-contamination. Suction tubing materials are also being carefully selected to ensure they meet the highest standards of infection control. Anatomical suctioning and advanced aspiration system designs are other key areas of focus in the market.

- These features enhance the effectiveness and safety of the devices, making them indispensable tools for healthcare professionals. Patient safety is a top priority, and medical suction devices are being designed with this in mind. Features such as automatic shut-off mechanisms and pressure regulators help to prevent complications and ensure a safe and comfortable experience for patients. The fluid collection system is another critical aspect of medical suction devices, and manufacturers are investing in innovative solutions to improve efficiency and reduce the risk of spills and leaks. Overall, the market is poised for continued growth as healthcare providers seek out advanced, portable, and safe equipment to meet the evolving needs of their patients.

What challenges does the Medical Suction Devices Industry face during its growth?

- In underdeveloped countries, the lack of sufficient awareness and limited accessibility to advanced medical suction devices poses a significant challenge to the growth of the healthcare industry.

- The market faces significant challenges in underdeveloped countries due to limited awareness and inadequate healthcare facilities. Many patients and medical professionals in nations such as Myanmar, Ethiopia, and Cambodia may be uninformed about the benefits and importance of medical suction equipment, leading to misuse or underutilization. Inadequate healthcare facilities in these countries often result in a scarcity of essential resources, including clean water and electricity, which can hinder the effective use of medical suction devices. Pressure monitoring sensors, suction unit filtration, fluid level indicators, suction regulator settings, suction canister capacity, vacuum regulation systems, and continuous suction systems are essential features of medical suction devices.

- These features contribute to the efficient and effective use of medical suction devices, ensuring optimal patient care. However, in underdeveloped countries, the lack of access to these advanced technologies can hinder the provision of adequate medical care. Moreover, the absence of proper maintenance and calibration of medical suction devices in these countries can further compromise patient safety and outcomes. It is crucial to address these challenges by increasing awareness, improving access to medical resources, and promoting the proper use and maintenance of medical suction devices to ensure the best possible patient care. Suction power output is a critical factor in determining the effectiveness of medical suction devices.

- The vacuum regulation system ensures consistent suction power output, which is essential for efficient and effective suction. Continuous suction systems offer uninterrupted suction, making them ideal for prolonged procedures or emergencies. These features contribute to the overall performance and reliability of medical suction devices.

Exclusive Customer Landscape

The medical suction devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical suction devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, medical suction devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The JETi hydrodynamic thrombectomy system from this company is a notable medical device, featuring a dual-action design that enhances clot removal efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Canon Inc.

- Cordis Corp.

- F. Hoffmann La Roche Ltd.

- Fresenius SE and Co. KGaA

- General Electric Co.

- Johnson and Johnson

- Koninklijke Philips N.V.

- Medtronic Plc

- Nihon Kohden Corp.

- Olympus Corp.

- OMRON Corp.

- Siemens AG

- Smith and Nephew plc

- Stryker Corp.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical Suction Devices Market

- In January 2024, Medtronic plc, a global healthcare solutions company, announced the launch of its new cordless suction device, the Respiratory System Harmony ENVSUCTION. This innovative device offers cordless mobility and improved battery life, enhancing the user experience and efficiency in clinical settings (Medtronic Press Release, 2024).

- In March 2024, Smiths Medical, a leading global medical device manufacturer, entered into a strategic partnership with Philips to integrate Philips' Lumify Point-of-Care Ultrasound solution with Smiths Medical's AirLife Vacuum Mattress System. This collaboration aims to improve patient care by enabling real-time ultrasound imaging during patient positioning procedures (Smiths Medical Press Release, 2024).

- In May 2024, Merit Medical Systems, Inc., a leading manufacturer and marketer of medical devices, completed the acquisition of certain assets of Sapphire Medical, a privately held medical device company specializing in suction technology. This acquisition expanded Merit Medical's product portfolio and strengthened its presence in the market (Merit Medical Press Release, 2024).

- In April 2025, the US Food and Drug Administration (FDA) granted 510(k) clearance to Teleflex Incorporated for its new disposable, battery-operated suction regulator, the Vacu-Aid Elite. This approval marked a significant technological advancement in the market, providing healthcare professionals with a more portable, efficient, and user-friendly alternative to traditional suction devices (Teleflex Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of equipment essential for effective surgical procedures. Surgical suction techniques rely on suction devices with varying materials, power sources, and ergonomics. Pneumatic and electric suction pumps, each with unique advantages, dominate the market. Suction device reliability, noise levels, and calibration are critical factors influencing market trends. Training for proper operation and certification ensures safety and efficiency. Sterilization and certification are paramount for maintaining hygiene and regulatory compliance. Suction pump portability, weight, and size impact ease of use and mobility.

- Suction system integration and performance are key considerations for healthcare facilities. Suction equipment lifespan, cleaning, and cost are essential factors in purchasing decisions. Closed suction systems and durable suction tubing further enhance system functionality. Suction device efficiency and suction system performance are continuously evolving, driving innovation and market growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Suction Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.36% |

|

Market growth 2024-2028 |

USD 361.92 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.22 |

|

Key countries |

US, Germany, France, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Medical Suction Devices Market Research and Growth Report?

- CAGR of the Medical Suction Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the medical suction devices market growth of industry companies

We can help! Our analysts can customize this medical suction devices market research report to meet your requirements.

RIA -

RIA -