Mercury Market Size 2024-2028

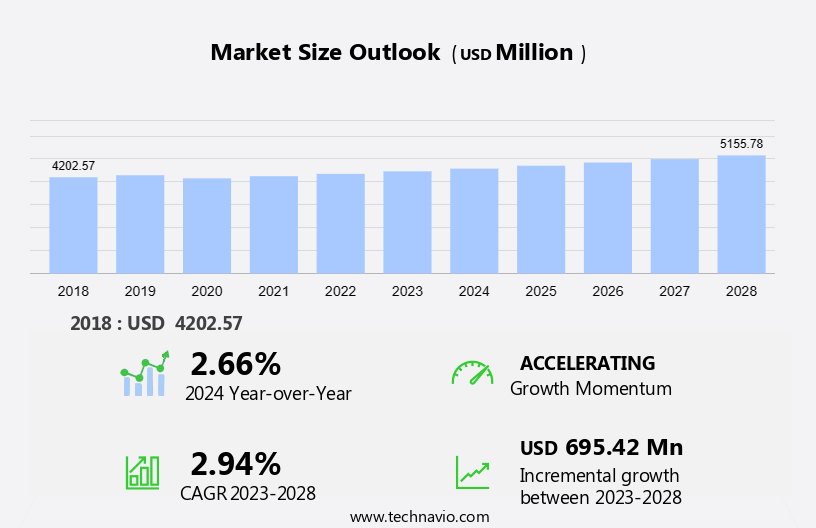

The mercury market size is forecast to increase by USD 695.42 million at a CAGR of 2.94% between 2023 and 2028. The market is witnessing significant growth due to the increasing adoption of mercury in electronics, particularly in button cell batteries. Mercury's unique properties, such as its high electrical conductivity and stability, make it an ideal choice for powering small electronic devices, including those in the semiconductor industry. Additionally, there is a growing emphasis on mercury recycling and recovery to mitigate environmental concerns and reduce the emissions of this toxic heavy metal. Stringent regulations on mercury emission and use in various industries, including healthcare, lighting systems, and pumps, are also driving market growth. In the healthcare sector, mercury continues to be used in medical instruments, such as thermometers and dental amalgams, despite efforts to find alternatives. The recycling and recovery of mercury from waste streams offer opportunities for market expansion while addressing environmental challenges. Overall, the market for mercury is expected to grow steadily due to these factors.

Market Analysis

The market encompasses various industries, primarily focusing on electronics, healthcare, and recycling. Mercury is a precious metal with unique properties, making it indispensable in numerous applications. In electronics, mercury is used in switches, sensors, and lighting systems. In healthcare, mercury is found in medical instruments such as thermometers, dental amalgams, and sphygmomanometers for blood pressure measurement. The economic activity in the construction and chemical industries also contributes to the market. Mercury testing services are essential to ensure health and safety standards, especially in the context of mercury-containing products like batteries, medical devices, and measuring devices.

The mining sector, particularly small-scale gold mining using mercury in the Amalgamated Small-Scale Gold Mining (ASGM) process, is another significant contributor. Despite its widespread use, mercury faces regulatory challenges due to its toxicity and environmental impact. Bans on mercury-containing products and initiatives to promote mercury-free alternatives are shaping the market's future. The supply chain for mercury and mercury-based components, including metals, alloys, and compounds, plays a crucial role in its availability and pricing. Consumer electronics and automotive industries are significant end-users of mercury-based components.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Electrical and electronics

- Measuring and controlling devices

- Dental application

- Gold processing

- Product

- Metal

- Alloys

- Compounds

- Geography

- APAC

- China

- North America

- Mexico

- Europe

- Norway

- Middle East and Africa

- South America

- Peru

- APAC

By Application Insights

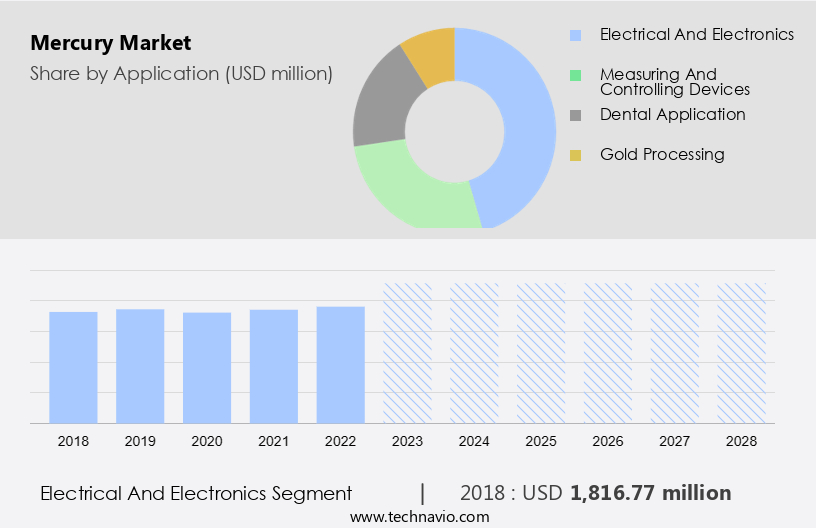

The electrical and electronics segment is estimated to witness significant growth during the forecast period. The market holds significant importance in various industries, including automotive, chemical, infrastructure, construction, agriculture, and environmental monitoring, due to mercury's unique properties. In the electrical and electronics sector, mercury's high conductivity and stable liquid state at room temperature make it an essential component in numerous devices and electronic components. For instance, mercury is used in fluorescent lamps, where it emits ultraviolet rays (253.7 nm) when an electric current passes through the lamp's electrode and collides with mercury atoms. This reaction generates light through the combination of mercury and fluorescence. For example, a 40 W linear fluorescent lamp manufactured in Japan contains approximately 5-7 mg of mercury.

Mercury's applications extend beyond lighting, as it is also used as a catalyst in various chemical processes, a component in automotive switches, and a crucial element in infrastructure projects, agriculture, and environmental monitoring and remediation.

Get a glance at the market share of various segments Request Free Sample

The electrical and electronics segment accounted for USD 1.82 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

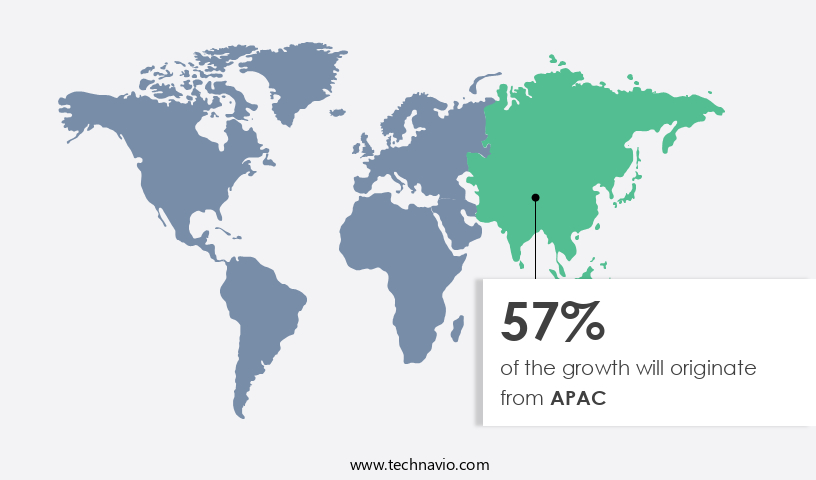

APAC is estimated to contribute 57% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The Asia-Pacific region plays a pivotal role in The market, driven by the region's industrial expansion and economic growth. Countries like China and India, in particular, are major contributors to the market's demand due to their burgeoning industries. Mercury finds extensive applications in various sectors, including electrical and electronics, chemical manufacturing, and mining, mirroring the region's industrial development. In the electronics industry, mercury's demand is on the rise due to the region's dominance in manufacturing electronic devices. Mercury is essential for producing electronic components, such as sensors, compact fluorescent lamps (CFLs), and batteries. Furthermore, mercury is used in the automotive industry for switches and in infrastructure projects, construction, agriculture, environmental monitoring, and remediation.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

An increase in adoption of mercury in button cell batteries is the key driver of the market. Mercury plays a significant role in the electronics industry, particularly in the production of batteries, specifically mercury oxide batteries. These batteries, which include button cells and certain types of alkaline batteries, utilize mercury to generate electrical energy storage due to its unique properties, such as high energy density and stable voltage output. Mercury's applications extend to medical devices and aviation equipment, where a reliable and long-lasting power source is essential. In the healthcare sector, mercury-containing button cells have been widely used in hearing aids and watches.

Moreover, mercury is employed in batteries by manufacturers worldwide to prevent internal gas accumulation that could lead to battery bulging and leaking, as stated by the US Environmental Protection Agency on February 21, 2023. Mercury's use extends beyond batteries, with applications in medical instruments, dental amalgams, and lighting systems. The recycling and recovery of mercury from waste streams is a critical aspect of minimizing its environmental impact.

Market Trends

Increasing efforts to recycle and recover emissions of mercury is the upcoming trend in the market. The market is witnessing a significant focus on recycling and recovery initiatives to minimize the environmental impact and decrease the release of mercury into the environment. As mercury is a persistent and toxic substance, there is a growing concern among stakeholders to improve recycling practices and recover mercury from end-of-life products. This includes the development of efficient mercury recycling technologies for items such as batteries, medical instruments like thermometers and dental amalgams, and lighting systems like fluorescent lamps and electronic devices. Recycling not only helps reduce the environmental footprint by preventing improper disposal but also decreases the demand for newly extracted mercury, aligning with sustainability objectives. The market growth is fueled by increasing environmental consciousness, stringent regulations, and corporate responsibility efforts.

Market Challenge

Stringent regulation on emission and use of mercury is a key challenge affecting market growth. Mercury, a significant element in electronics and various industries, including healthcare with medical instruments, thermometers, and dental amalgams, and lighting systems, is subject to increasing regulatory scrutiny due to its harmful effects on the environment and human health. The Minamata Convention, a multilateral environmental agreement signed on 10 October 2013, targets specific human activities contributing to mercury pollution. By 12 December 2023, the US Environmental Protection Agency implemented this agreement, addressing mercury emissions from industries and products. The international community acknowledges the importance of this agreement in reducing mercury pollution from major contributors over the coming decades. This collective effort will contribute significantly to the global reduction of mercury pollution, safeguarding both the environment and public health.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Aldrett Hermanos SA de CV - The company offers mercury such as Metallic Mercury, which is used in electrical switches as a liquid contact material, as a working fluid in diffusion pumps in vacuum techniques.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albemarle Corp.

- Almaden Minerals

- Avantor Inc.

- Carbanio

- China Jin Run Industrial Co. Ltd.

- Henan Tianfu Chemical Co. Ltd

- High Purity Standards

- Lab Alley

- Labogens Fine Chem Industry

- Luciteria Science

- MaTecK GmbH

- Merck KGaA

- MERU CHEM PVT. LTD.

- Nanoshel LLC

- Noah Chemicals

- NovaElements

- Spa Corp.

- Vivid India

- Wake Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Mercury, a precious metal known for its unique properties, plays a significant role in various sectors of the electronics industry and beyond. In the realm of healthcare, mercury is used in medical instruments such as thermometers and dental amalgams. The electrical and electronics sector relies on mercury for its high electrical and thermal conductivity in batteries, sensors, and lighting systems. The automotive industry incorporates mercury in automotive switches and catalysts for infrastructure projects and construction equipment. Mercury's role extends to agriculture, where it is used for environmental monitoring and remediation. In the aerospace sector, mercury-based components are essential for electronic devices and measuring devices.

The economic activity surrounding mercury is vast, with mercury testing services, bans on mercury-containing products, and the mining industry producing mercury resources. Mercury emissions stem from mine production, small-scale gold mining, coal combustion, and chemical processes. Mercury's applications span various industries, including healthcare, electronics, automotive, infrastructure, agriculture, and aerospace. Its unique properties, such as electrical and thermal conductivity, make it an indispensable component in numerous applications. However, health and safety concerns and environmental regulations necessitate careful handling and disposal of mercury-based components.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.94% |

|

Market Growth 2024-2028 |

USD 695.42 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.66 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 57% |

|

Key countries |

Mexico, China, Tajikistan, Norway, and Peru |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Aldrett Hermanos SA de CV, Albemarle Corp., Almaden Minerals, Avantor Inc., Carbanio, China Jin Run Industrial Co. Ltd., Henan Tianfu Chemical Co. Ltd, High Purity Standards, Lab Alley, Labogens Fine Chem Industry, Luciteria Science, MaTecK GmbH, Merck KGaA, MERU CHEM PVT. LTD., Nanoshel LLC, Noah Chemicals, NovaElements, Spa Corp., Vivid India, and Wake Group |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -