Metal Casting Market Size 2025-2029

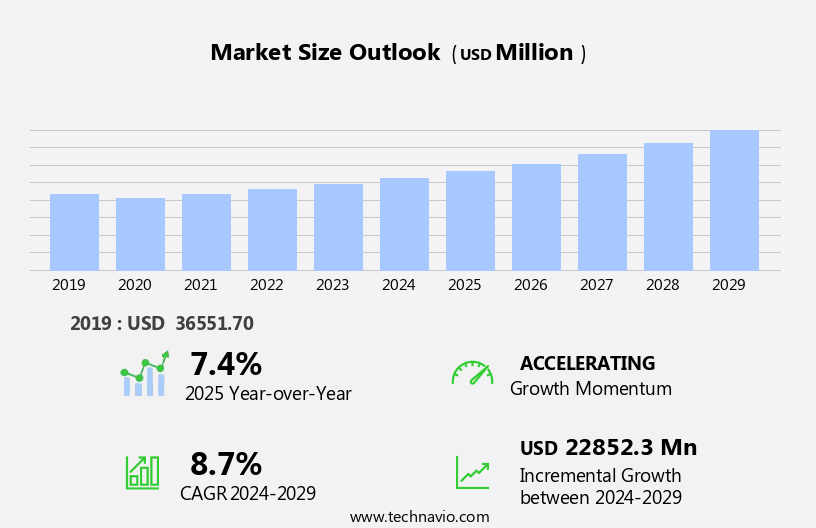

The metal casting market size is forecast to increase by USD 22.85 billion at a CAGR of 8.7% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing adoption of advanced technologies such as X-ray casting for improved defect recognition in industries like automotive engines and passenger cars. Additionally, the integration of casting process simulation technology is enhancing efficiency and reducing production costs. However, the market faces challenges from energy-consuming technologies that increase overall production costs. Key technologies shaping the market include steel casting, aluminum casting, and aluminum die casting, with applications ranging from automotive components to construction machinery and X-ray equipment. Innovations in materials like magnesium are also driving market expansion. The use of 3D printing in metal casting is a promising trend, offering customization and cost savings, but faces challenges in terms of scalability and material limitations. Overall, the market is poised for growth, driven by technological advancements and evolving industry demands.

What will be the Size of the Metal Casting Market During the Forecast Period?

- The market encompasses the production of various metal components through processes such as die casting, sand mold casting, and investment casting. This industry is characterized by its significant size and continuous growth, driven by the demand for lightweight, strong parts in diverse sectors, including automotive, construction, and industrial manufacturing. Aluminum casting, specifically grey iron metal and aluminum, holds a prominent position due to its lightweight properties and cost-effectiveness. Regulations governing waste minimization and the use of recyclable materials are influencing market trends, with an increasing focus on 3D metal shaping through technologies like cut-out molds and 3D printing. Applications span from intricate lamp poles to large structural components, with flexible designing and rapid prototyping facilitating innovation.

- Silicone molds and the integration of plastic and sand in casting processes further expand the market's scope. Overall, the metal casting industry remains a dynamic and evolving sector, driven by the demand for strong, lightweight parts and the ongoing pursuit of cost-effective, sustainable manufacturing solutions.

How is this Metal Casting Industry segmented and which is the largest segment?

The metal casting industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

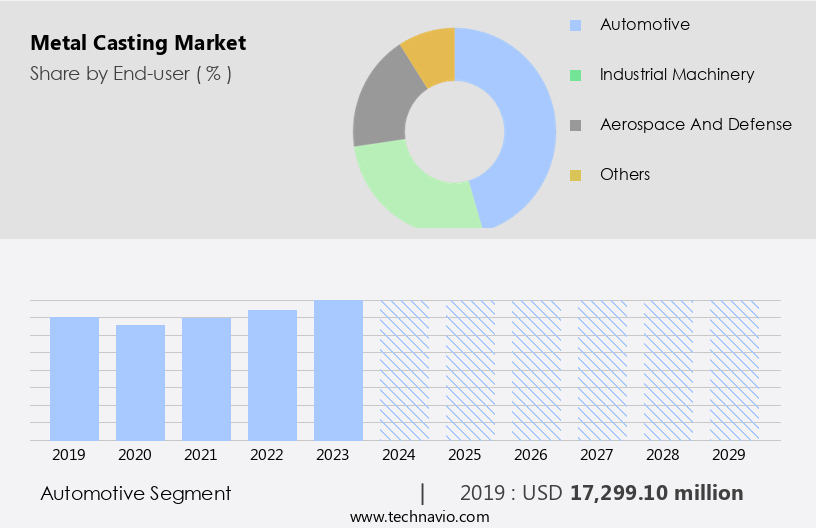

- Automotive

- Industrial machinery

- Aerospace and defense

- Others

- Material

- Aluminum

- Cast iron

- Magnesium

- Zinc

- Others

- Method

- Sand casting

- HPDC

- Gravity casting

- LPDC

- Geography

- APAC

- China

- India

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- North America

- Canada

- US

- South America

- Middle East and Africa

- APAC

By End-user Insights

- The automotive segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth, driven by the automotive industry's increasing demand for lightweight, cost-effective, and easily maneuverable components. Zinc and aluminum are the preferred metals for casting in this sector due to their properties, with ferrous and nonferrous metals and their alloys also utilized in engine and brake production. Die casting, specifically zinc and aluminum die casting, is a popular method for manufacturing automotive components. The rising number of vehicles in use, fueled by low-interest rates and affordable fuel prices, further boosts market expansion. Metal casting techniques, including sand casting, gravity casting, vacuum casting, and die casting, are employed in various industries such as oil & gas, aerospace, railroad, healthcare, mining, and manufacturing of lamp poles, bus pedals, train wheels, vehicle parts, and metal casting suppliers.

Key benefits of metal casting include the production of strong, lightweight parts, waste minimization, and cost-effectiveness. Metals used include carbon, silicon, manganese, phosphorus, and sulphur, with varying melting points and wear resistance. Machines used in metal casting include blowers, bearings, cams, engine oil pans, gears, valves, screw nuts, wire rod, and electrical sheets.

Get a glance at the market report of share of various segments Request Free Sample

The Automotive segment was valued at USD 17.3 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

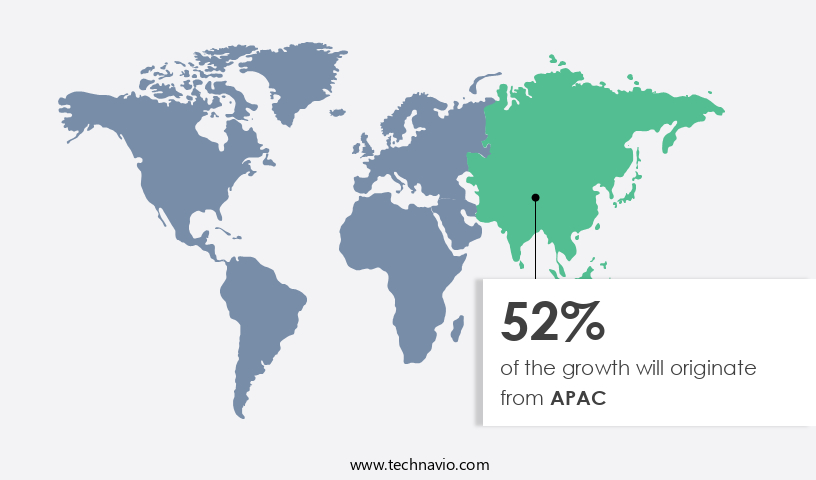

- APAC is estimated to contribute 52% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market is experiencing significant growth due to increasing demand from various sectors such as automotive, oil & gas, aerospace, railroad, healthcare, and mining. Asia Pacific is a key contributor to this market, driven by automation and clean technologies to ensure high-quality production with minimal environmental impact. The adoption of Industry 4.0 is revolutionizing the manufacturing sector, enabling digitalization of the entire value chain. Aluminum casting, using recyclable materials, is gaining popularity due to its lightweight, strong parts, and cost-effectiveness. Cast iron, grey iron, aluminum, and other metals continue to be in demand for various applications, including lamp poles, bus pedals, train wheels, vehicle parts, and metal casting suppliers.

Regulations regarding emissions and waste minimization are driving the use of technologies such as die casting, shell mold casting, gravity casting, vacuum casting, and sand casting. Key sectors like automotive, oil & gas, aerospace, railroad, healthcare, and mining are major consumers of metal casting, with applications including blowers, bearings, cams, engine oil pans, gears, valves, screw nuts, wire rod, electrical sheets, and stainless steel. The market is expected to grow due to the increasing demand for lightweight, strong parts, and cost-effectiveness, with key metals including carbon, silicon, manganese, phosphorus, and sulphur. The market is expected to remain competitive due to advancements in flexible designing, rapid prototyping, and 3D metal shaping.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Metal Casting Industry?

Growing adoption of X-ray casting increases efficiency in defect recognition is the key driver of the market.

- The markets witness an escalating demand for advanced defect recognition technologies, such as automatic or assisted defect recognition (ADR), in X-ray applications. X-ray technology's continuous evolution, with enhancements in tubes or software incorporating sophisticated algorithms, fuels this trend. Inline ADR systems are extensively utilized in production processes, making Accept or Reject decisions based on quality engineer-defined parameters. These systems ensure reliable and consistent performance, documenting results independently without human intervention. Digital radiography technology's acceptance across various end-user industries opens up avenues for software tool development. This technology's integration in metal casting processes enhances quality control, enabling the production of lightweight, strong parts with cost-effectiveness.

- Applications span industries like automotive (lightweight vehicles, vehicle parts), oil & gas, aerospace, railroad, healthcare, mining, and more. Materials like aluminum, cast iron, grey iron metal, and various alloys (carbon, silicon, manganese, phosphorus, sulphur) are commonly used in metal casting. Processes like die casting, shell mold casting, gravity casting, vacuum casting, and sand casting are employed, with machines producing components such as blowers, bearings, cams, engine oil pans, gears, valves, screw nuts, wire rod, electrical sheets, and stainless steel. Metal casting suppliers cater to diverse industries, offering solutions for various applications, including pipes, gearbox cases, cylinder heads, and more.

- Waste minimization, rapid prototyping, and flexible designing are essential aspects of metal casting, with 3D printing and silicone, metal, and plastic casting also gaining popularity.

What are the market trends shaping the Metal Casting Industry?

Incorporating casting process simulation technology is the upcoming market trend.

- Metal casting simulation technology is a valuable solution for producing precise and cost-effective components in various industries, including automotive. This method enhances casting yield, optimizes feed ability, and reduces processing time by detecting and eliminating defects. The market is witnessing an increasing trend towards simulation-based casting, particularly in the automotive sector. The demand for lightweight vehicles necessitates the production of defect-free cast parts with exact dimensions of size, weight, and shape. Simulation-based casting enables casters to meet these requirements, making it an essential tool for operators in the metal casting industry. The economic justification for casting simulation includes its ability to improve overall efficiency, minimize waste, and produce strong, lightweight parts from materials like aluminum, cast iron, grey iron metal, and others.

- The use of recyclable materials further adds to the cost-effectiveness and sustainability of the process. Simulation-based casting processes include Die Casting, Shell Mold Casting, Gravity Casting, Vacuum Casting, and Sand Casting, among others. Applications range from engine components like blowers, bearings, cams, engine oil pans, gears, valves, screw nuts, and wire rod, to industrial components like pipes, gearbox cases, cylinder heads, and various vehicle parts. Industries such as oil & gas, aerospace, railroad, healthcare, mining, and others also benefit from the use of simulation-based casting for producing high-quality, wear-resistant components with improved machinability.

What challenges does the Metal Casting Industry face during its growth?

Significant energy-consuming technology increasing overall production costs is a key challenge affecting the industry growth.

- The market is driven by the increasing demand for lightweight vehicles and components in various sectors such as oil & gas, aerospace, railroad, healthcare, mining, and automotive. Aluminum casting, utilizing recyclable materials, is a significant trend in this industry due to its lightweight and strong properties. Cast iron, including grey iron metal, remains a dominant material in metal casting, with applications in engine components, machinery parts, and infrastructure elements like lamp poles, bus pedals, and train wheels. Metal casting processes include Die Casting, Sand Casting, Shell Mold Casting, and Gravity Casting, among others. These processes require substantial energy inputs for melting metals and producing molds.

- Natural gas is commonly used for metal treatment, followed by coal coke, breeze, and electricity. The energy intensity of the metal casting process is high, particularly in developing countries like India, which is the third-largest market for metal castings. These countries often face power deficits, making energy security a critical concern for metal casters. Mold making and core making are essential processes that also require considerable energy. Waste minimization, flexible designing, rapid prototyping, and the use of alternative materials like silicone, metal, plastic, and sand, are some strategies employed to enhance cost-effectiveness and improve wear resistance. Machines, pipes, gearbox cases, cylinder heads, and various vehicle parts are some of the key applications for metal casting.

- Other materials used include carbon, silicon, manganese, phosphorus, and sulphur, with varying melting points and properties. The market is characterized by its energy-intensive nature and the need for continuous innovation to meet the demands of various sectors. The industry's growth is driven by the increasing demand for lightweight and strong parts, with aluminum casting being a significant trend. Energy security remains a critical concern, particularly in developing countries, and strategies like waste minimization, flexible designing, and the use of alternative materials are essential to ensure cost-effectiveness and improve wear resistance.

Exclusive Customer Landscape

The metal casting market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal casting market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, metal casting market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alcast Co. - The company offers metal casting services such as permanent mold aluminum foundry, semi-permanent mold aluminum foundry, and tilt pour aluminum castings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alcast Co.

- Alcoa Corp.

- Benton Foundry Inc.

- Buhler AG

- Dawang Metals Pte. Ltd.

- Decatur Foundry Inc.

- Endurance Technologies Ltd.

- Form Technologies

- Hitachi Ltd.

- Kurt Manufacturing

- Lestercast Ltd.

- OSCO Industries Inc.

- Precision Castparts Corp.

- Reliance Foundry Co. Ltd.

- Ryobi Ltd.

- Shibaura Machine Co. Ltd.

- Stahl Specialty Co.

- T.H.T. Presses Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Metal casting is a manufacturing process that involves pouring molten metal into a mold, allowing it to solidify, and then removing the solidified metal from the mold. This process is used to create a wide range of components and parts for various industries, including oil & gas, aerospace, railroad, healthcare, mining, and automotive. Die casting is a type of metal casting that uses a die to shape the molten metal under high pressure. This process is commonly used for producing complex parts with high precision and consistency. Aluminum and zinc are the most commonly used metals in die casting due to their excellent fluidity and ease of casting.

Sand mold casting is another popular metal casting process that uses sand as the mold material. This process is suitable for producing larger and more complex parts, as well as those with intricate shapes. Gray iron metal, which contains graphite flakes, is a common material used in sand casting due to its excellent machinability and wear resistance. Regulations play a significant role in the market. The use of recyclable materials, such as aluminum, is increasingly becoming a priority due to environmental concerns. The automotive industry, in particular, is focusing on producing lightweight vehicles to reduce carbon emissions and improve fuel efficiency.

Lightweight parts made from aluminum and other metals through casting processes are an effective solution for achieving this goal. The use of advanced technologies, such as 3D metal shape and 3D printing, is also gaining popularity in the market. These technologies enable flexible designing, rapid prototyping, and waste minimization, making them attractive options for manufacturers looking to reduce costs and improve production efficiency. Metal casting suppliers play a crucial role in the market by providing raw materials, equipment, and services to manufacturers. They offer a range of metals, including carbon, silicon, manganese, phosphorus, and sulphur, with varying melting points and properties to suit different applications.

The demand for metal casting is driven by various industries, including oil & gas, aerospace, railroad, healthcare, mining, and automotive. In the oil & gas industry, metal castings are used for producing pipes, machines, and other components for drilling and production equipment. In the aerospace industry, metal castings are used for producing engine parts, such as cylinder heads and gearbox cases, as well as structural components, such as wing parts and landing gear. In the railroad industry, metal castings are used for producing train wheels, axles, and other components for locomotives and rolling stock. In the healthcare industry, metal castings are used for producing medical equipment, such as surgical instruments and implants.

In the mining industry, metal castings are used for producing mining equipment, such as pumps, valves, and wear-resistant parts. The market is highly competitive, with numerous suppliers offering a range of casting processes, including die casting, shell mold casting, gravity casting, vacuum casting, and sand casting. These processes offer different advantages in terms of cost-effectiveness, production speed, and part complexity. For instance, die casting is suitable for producing complex parts in large quantities, while sand casting is suitable for producing larger and more complex parts with intricate shapes.

The use of advanced technologies, recyclable materials, and regulations are driving the growth of the market, while the demand for lightweight, strong, and cost-effective parts continues to fuel innovation and development in this field. Metal casting suppliers play a crucial role in providing raw materials, equipment, and services to manufacturers, enabling them to meet the evolving demands of their customers.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

232 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.7% |

|

Market growth 2025-2029 |

USD 22.85 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.4 |

|

Key countries |

US, China, Japan, India, UK, Canada, South Korea, Germany, France, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Metal Casting Market Research and Growth Report?

- CAGR of the Metal Casting industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the metal casting market growth of industry companies

We can help! Our analysts can customize this metal casting market research report to meet your requirements.

RIA -

RIA -