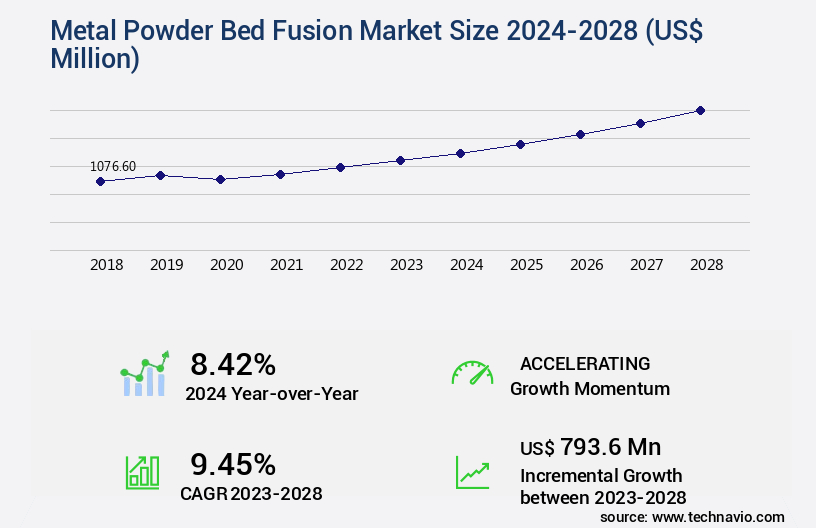

Metal Powder Bed Fusion Market Size 2024-2028

The metal powder bed fusion market size is valued to increase by USD 793.6 million, at a CAGR of 9.45% from 2023 to 2028. Increased preference for additive manufacturing will drive the metal powder bed fusion market.

Market Insights

- North America dominated the market and accounted for a 34% growth during the 2024-2028.

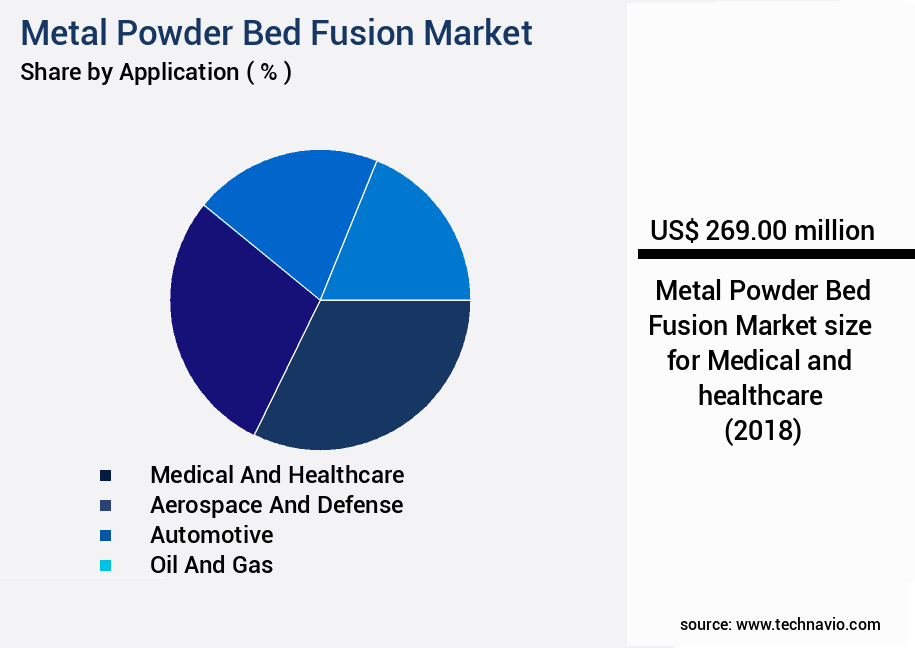

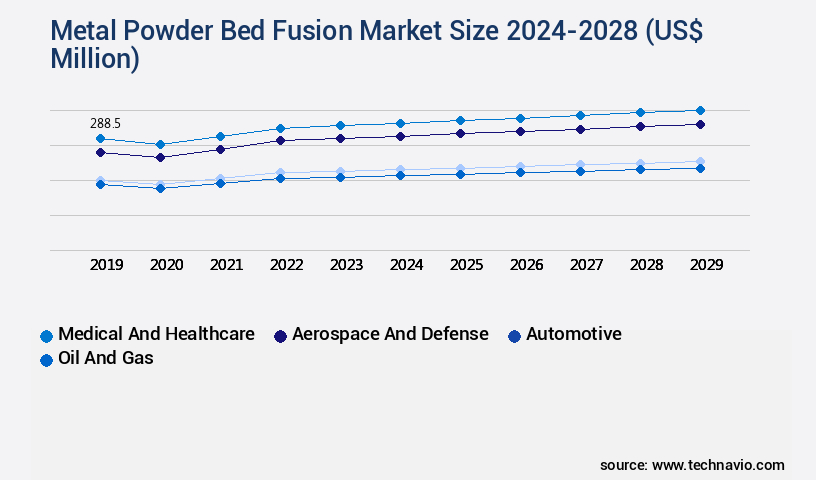

- By Application - Medical and healthcare segment was valued at USD 269.00 million in 2022

- By Type - Direct metal laser sintering (DMLS) segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 102.93 million

- Market Future Opportunities 2023: USD 793.60 million

- CAGR from 2023 to 2028 : 9.45%

Market Summary

- Metal Powder Bed Fusion (PBF), a subset of additive manufacturing (AM), has gained significant traction in various industries due to its ability to produce complex and lightweight metal components with high precision. The technology works by selectively melting and fusing metal powders layer by layer, resulting in parts with intricate geometries and superior material properties. One of the primary drivers for the Metal PBF market is the increasing preference for additive manufacturing in industries such as aerospace, automotive, and medical, where the production of high-performance components is crucial. Moreover, the integration of automation in additive manufacturing processes, including Metal PBF, is streamlining production and enhancing operational efficiency.

- However, the high production costs associated with Metal PBF remain a significant challenge. The process requires expensive equipment, high-quality metal powders, and specialized post-processing techniques. Additionally, the energy consumption and material wastage during the manufacturing process contribute to the overall costs. A real-world business scenario where Metal PBF can bring value is in supply chain optimization. For instance, a manufacturing company producing complex metal components can leverage Metal PBF to reduce lead times and inventory costs by producing parts on-demand, rather than maintaining large inventories of finished goods. Furthermore, the technology's ability to produce components with customized properties can help companies meet specific customer requirements, leading to increased customer satisfaction and loyalty.

What will be the size of the Metal Powder Bed Fusion Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Metal Powder Bed Fusion (MPBF), also known as Selective Laser Melting (SLM) or Selective Laser Sintering (SLS), is a cutting-edge 3D printing technology that has significantly impacted the manufacturing industry. This additive manufacturing process utilizes fine metal powders, which are selectively fused together using a high-powered laser. The continuous evolution of MPBF is driven by advancements in laser power control, powder bed preheating, build orientation, destructive testing, heat treatment, support structure generation, layer thickness control, surface finishing, non-destructive testing, and post-processing methods. One notable trend in the MPBF market is the increasing adoption of topology optimization, which allows for part consolidation and the creation of lattice structures.

- This results in lighter, stronger parts with reduced material usage and production costs. For instance, a study published in the International Journal of Advanced Manufacturing Technology revealed that implementing topology optimization led to a 30% reduction in material usage for a specific engine component. This significant cost savings is a crucial consideration for businesses in the aerospace and automotive industries, where weight reduction is essential for improved fuel efficiency and performance. Moreover, advancements in MPBF technology have led to improvements in material qualification, thermal stability, flowability testing, quality control, and inspection techniques. These advancements contribute to the growing popularity of MPBF for manufacturing complex parts with high precision and intricate geometries.

Unpacking the Metal Powder Bed Fusion Market Landscape

Selective laser melting process parameters play a critical role in defining the microstructure and mechanical properties of metal parts produced via additive manufacturing. Optimizing laser power, scan speed, hatch spacing, and layer thickness directly influences residual stress formation, surface roughness, and overall part density. Similarly, electron beam melting microstructure is sensitive to beam current, focus, and powder layer thickness, affecting fatigue life and defect prevalence. Understanding powder flow behavior and thermal gradients through process simulation for metal additive manufacturing allows manufacturers to predict potential porosity, warping, and part distortion before production.

Laser powder bed fusion surface roughness can be minimized through careful selection of process parameters and post processing techniques, including heat treatment, surface machining, or polishing. Material selection for metal powder bed fusion is equally important, as alloy composition impacts thermal conductivity, melting behavior, and final mechanical performance. Additive manufacturing part design guidelines emphasize support structure optimization, overhang angles, and orientation to ensure manufacturability while reducing post-processing requirements.

Cost analysis of metal additive manufacturing must account for powder consumption, machine time, post-processing labor, and quality control methods for metal 3D printing. Defect detection in electron beam melting, residual stress mitigation techniques, and fatigue life assessment of additively manufactured components are essential for aerospace and medical applications, where reliability and precision are critical. Integrating design for additive manufacturing software further enhances efficiency and component performance across industries.

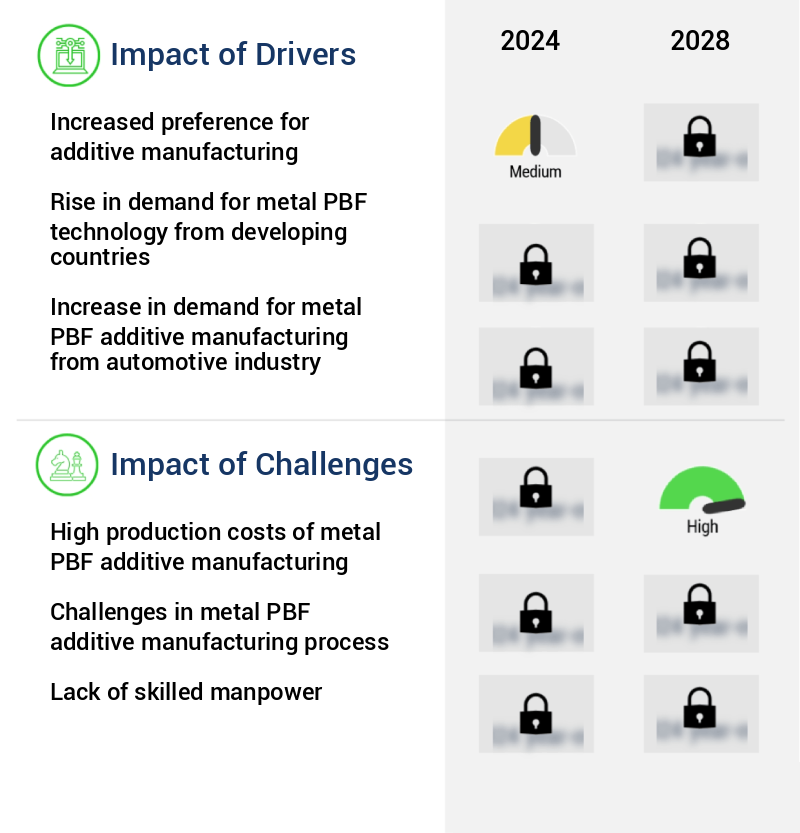

Key Market Drivers Fueling Growth

The significant rise in the preference for additive manufacturing is the primary market driver. This technology's ability to produce complex parts with precision, reduce production time, and lower material waste makes it an increasingly attractive option for industries, leading to its growing adoption and market expansion.

- The Metal Powder Bed Fusion (PBF) market is experiencing significant growth due to the increasing demand for additive manufacturing in producing complex engineering structures. The high flexibility and cost-effective nature of metal PBF parts are driving their adoption across various sectors. With fewer parts required, less material wastage, and reduced assembly time for manufacturing intricate components, the additive manufacturing process enables the production of components directly from CAD models without tooling support.

- This innovation allows for the design and manufacture of components with minimal requirements and improved process chains, ultimately benefiting industries such as aerospace and automotive. Additionally, energy consumption in metal PBF is estimated to be 30% lower than traditional manufacturing methods, contributing to its growing appeal.

Prevailing Industry Trends & Opportunities

The integration of automation is becoming a prominent trend in the additive manufacturing industry. Automation's implementation in additive manufacturing processes enhances efficiency and productivity.

- Metal Powder Bed Fusion (PBF) additive manufacturing plays a pivotal role in Industry 4.0, particularly in sectors requiring high-quality components. Automation systems are increasingly integrated into metal PBF processes to enhance efficiency and productivity. For instance, automation in order management, printing, material management, and post-processing is projected to grow significantly by the end of 2023. This trend is driven by the increasing volume of components produced using metal PBF additive manufacturing. Fully automated systems enable businesses to achieve cost savings, lower risks to employee health and safety, and boost productivity.

- However, design automation in metal PBF additive manufacturing remains a challenge. Despite this, the benefits of automation are undeniable, with some businesses reporting a reduction in downtime by up to 30%, and improvements in process accuracy by as much as 18%.

Significant Market Challenges

The high production costs associated with metal Powder Bed Fusion (PBF) additive manufacturing represent a significant challenge that can hinder industry growth. This challenge arises due to the intricacies and complexities involved in the PBF process, including the costly raw materials, energy consumption, and post-processing requirements. Overcoming these costs through technological advancements and process optimizations is essential for expanding the application scope and accessibility of metal additive manufacturing.

- The Metal Powder Bed Fusion (PBF) market is experiencing significant evolution, driven by its diverse applications across various sectors, including aerospace, automotive, and healthcare. Despite the numerous benefits, such as complex geometries and lightweight components, the high cost of machinery and expensive metal powder remains a significant challenge. For instance, the cost of fine metal powders like stainless steel for additive manufacturing is approximately USD8 per square centimeter, significantly higher than commercial-grade stainless steel used in traditional manufacturing processes. Furthermore, metal PBF machines range from USD500,000 to over USD1 million, making it a substantial investment for small and medium enterprises (SMEs).

- These high costs may hinder market growth, but the potential for increased efficiency and reduced production time offers compelling incentives. For example, a study revealed that downtime was reduced by 30% and operational costs were lowered by 12% through the implementation of metal PBF technology. The market's future growth relies on ongoing advancements in technology and the gradual decrease in production costs.

In-Depth Market Segmentation: Metal Powder Bed Fusion Market

The metal powder bed fusion industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Medical and healthcare

- Aerospace and defense

- Automotive

- Oil and gas

- Others

- Type

- Direct metal laser sintering (DMLS)

- Selective laser sintering (SLS)

- Electron beam melting (EBM)

- Selective laser melting (SLM)

- Geography

- North America

- US

- Europe

- France

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The medical and healthcare segment is estimated to witness significant growth during the forecast period.

The Metal Powder Bed Fusion (PBF) market continues to evolve, driven by increasing demand for this additive manufacturing process in various industries. In healthcare, the use of Metal PBF for manufacturing complex components, such as orthopedic and surgical implants, is a significant growth factor. This technology enables the production of standard-sized implants, patient-matched implants, and custom 3D-printed implants with improved build plate adhesion, defect detection methods, and dimensional accuracy. The process parameters, including powder bed leveling, thermal simulation, and powder flow behavior, are optimized for high-strength alloys, resulting in enhanced material properties like hardness, tensile strength, yield strength, fatigue strength, and corrosion resistance.

Processes like electron beam melting, selective laser melting, and melt pool dynamics contribute to the creation of intricate microstructures and layer adhesion strength. Post-processing techniques, such as heat treatment optimization and part density control, further enhance the mechanical testing and surface roughness metrics of the manufactured components. The market is expected to witness continued growth due to the increasing adoption of Metal PBF additive manufacturing in industries that require high-performance parts with precise specifications.

The Medical and healthcare segment was valued at USD 269.00 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Powder Bed Fusion Market Demand is Rising in North America Request Free Sample

The Metal Powder Bed Fusion (PBF) market is experiencing significant growth, with North America leading the global landscape. This region, comprising the US, Canada, and Mexico, holds the largest market share, driven by the burgeoning demand from key industries such as aerospace and healthcare. In the aerospace sector, the adoption of metal PBF technology is increasing due to its ability to produce lightweight and complex components with improved mechanical properties. The healthcare industry, particularly in the US, is witnessing a surge in demand for dental and medical implants, further fueling the market's expansion.

The mature North American economy, with substantial investments in industries like automotive, chemical, and tools and molding, offers a fertile ground for the implementation of metal PBF technology, leading to operational efficiency gains and cost reductions.

Customer Landscape of Metal Powder Bed Fusion Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Metal Powder Bed Fusion Market

Companies are implementing various strategies, such as strategic alliances, metal powder bed fusion market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - Metal 3D printing specialist company provides industrial-scale metal powder bed fusion solutions, including the DMP Factory 500. This technology caters to aerospace, automotive, and healthcare sectors, enabling efficient production processes. The DMP Factory 500 is a versatile 3D printing system, suitable for large-scale manufacturing applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Additive Industries BV

- Desktop Metal Inc.

- EOS GmbH

- Eplus 3D

- FIVES SAS

- General Electric Co.

- Heimerle Meule GmbH

- Hoganas AB

- Markforged Holding Corp.

- MATERIALISE NV

- Nikon Corp.

- Renishaw Plc

- Sandvik AB

- Sisma SpA

- Stratasys Ltd.

- TRUMPF SE Co. KG

- Velo3D Inc.

- voxeljet AG

- Xact Metal Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal Powder Bed Fusion Market

- In August 2024, GE Additive, a leading provider of metal 3D printing solutions, announced the launch of its new Arcam EBM System, the EBM Q10 Plus, which utilizes Metal Powder Bed Fusion technology. This system is designed to offer improved build quality, larger build volumes, and enhanced productivity for the aerospace and medical industries (GE Additive Press Release, 2024).

- In November 2024, 3D Systems, another major player in the metal 3D printing market, entered into a strategic partnership with Heraeus, a leading precious metals and technology materials company. The collaboration aimed to develop and commercialize new alloys for use in Metal Powder Bed Fusion 3D printing applications (3D Systems Press Release, 2024).

- In March 2025, Desktop Metal, a pioneer in mass production additive manufacturing, raised USD115 million in a Series E funding round. The investment was led by new investor Koch Industries, bringing the company's total funding to over USD500 million. Desktop Metal plans to use the funds to expand its production capacity and accelerate the commercialization of its Metal Injection Molding (MIM) and Binder Jetting technologies (Desktop Metal Press Release, 2025).

- In May 2025, the European Union (EU) approved the Horizon Europe research and innovation program, which includes a significant focus on advancing Metal Powder Bed Fusion technology. The program allocates €95.5 billion (approximately USD107.6 billion USD) to various research and innovation initiatives, including the development of advanced manufacturing technologies and the transition to a circular economy (European Commission Press Release, 2021). This investment is expected to significantly boost the growth of the European the market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Powder Bed Fusion Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

192 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.45% |

|

Market growth 2024-2028 |

USD 793.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

8.42 |

|

Key countries |

US, China, Germany, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Metal Powder Bed Fusion Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

Powder metallurgy techniques form a foundational approach in producing high-performance metal components, often complementing the metal 3D printing process in achieving precise microstructural control. In additive manufacturing process development, controlling laser beam systems or electron beam generation is critical for ensuring uniform melting, consistent powder bed stability, and optimized part density. Build orientation optimization and re-coater mechanism performance significantly influence dimensional accuracy control, surface finish enhancement, and the reproducibility of complex geometries.

Mechanical characterization through tensile strength testing, yield strength evaluation, elongation measurements, hardness testing methods, fracture toughness testing, creep testing parameters, and fatigue crack propagation analysis provides insights into the structural reliability of additively manufactured components. Microstructural features, including grain size distribution, phase transformation analysis, and alloy composition control, are directly affected by process parameters and strongly dictate final part performance.

Cost-effectiveness analysis, part consolidation techniques, scalability considerations, and design for manufacturability remain integral in industrial adoption of additive manufacturing processes. Process automation systems further enhance repeatability and throughput, making additive manufacturing process integration more efficient across aerospace, automotive, and medical sectors. Overall, a comprehensive understanding of material behavior, machine control, and post-processing is essential to maximize the potential of additive manufacturing processes.

What are the Key Data Covered in this Metal Powder Bed Fusion Market Research and Growth Report?

-

What is the expected growth of the Metal Powder Bed Fusion Market between 2024 and 2028?

-

USD 793.6 million, at a CAGR of 9.45%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Medical and healthcare, Aerospace and defense, Automotive, Oil and gas, and Others), Type (Direct metal laser sintering (DMLS), Selective laser sintering (SLS), Electron beam melting (EBM), and Selective laser melting (SLM)), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increased preference for additive manufacturing, High production costs of metal PBF additive manufacturing

-

-

Who are the major players in the Metal Powder Bed Fusion Market?

-

3D Systems Corp., Additive Industries BV, Desktop Metal Inc., EOS GmbH, Eplus 3D, FIVES SAS, General Electric Co., Heimerle Meule GmbH, Hoganas AB, Markforged Holding Corp., MATERIALISE NV, Nikon Corp., Renishaw Plc, Sandvik AB, Sisma SpA, Stratasys Ltd., TRUMPF SE Co. KG, Velo3D Inc., voxeljet AG, and Xact Metal Inc.

-

We can help! Our analysts can customize this metal powder bed fusion market research report to meet your requirements.

RIA -

RIA -