Neural Processor Market Size and Growth Forecast 2026-2030

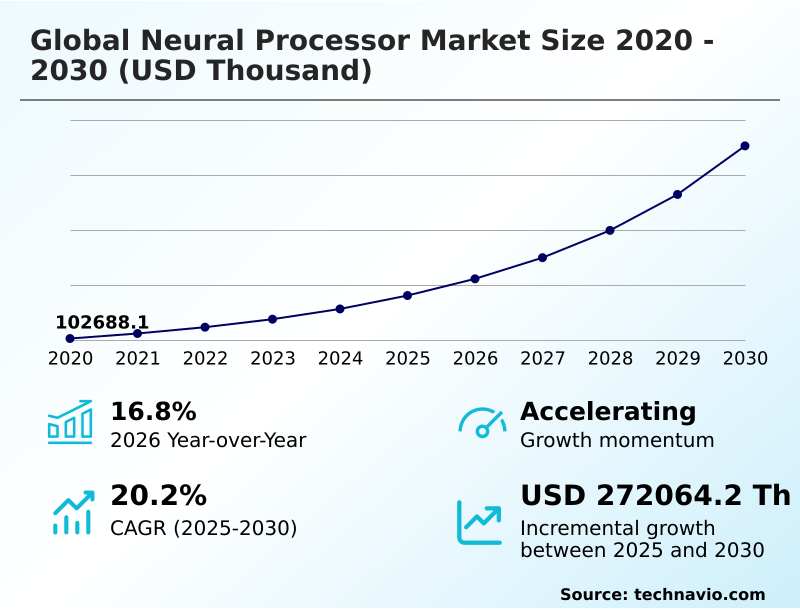

The Neural Processor Market size was valued at USD 180.87 million in 2025 growing at a CAGR of 20.2% during the forecast period 2026-2030.

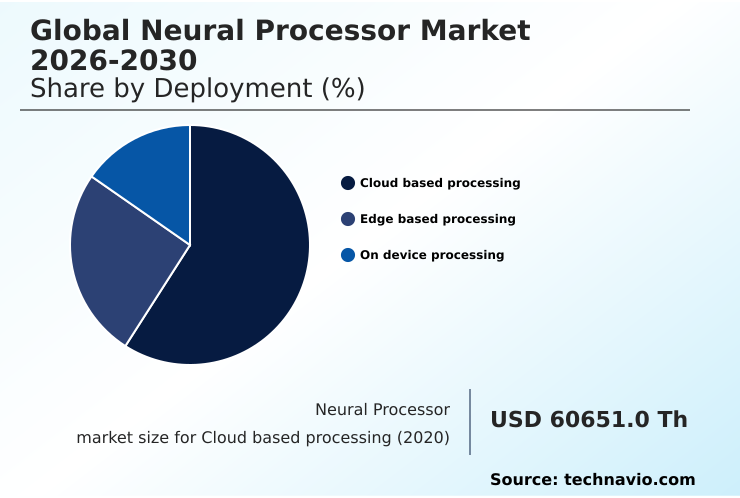

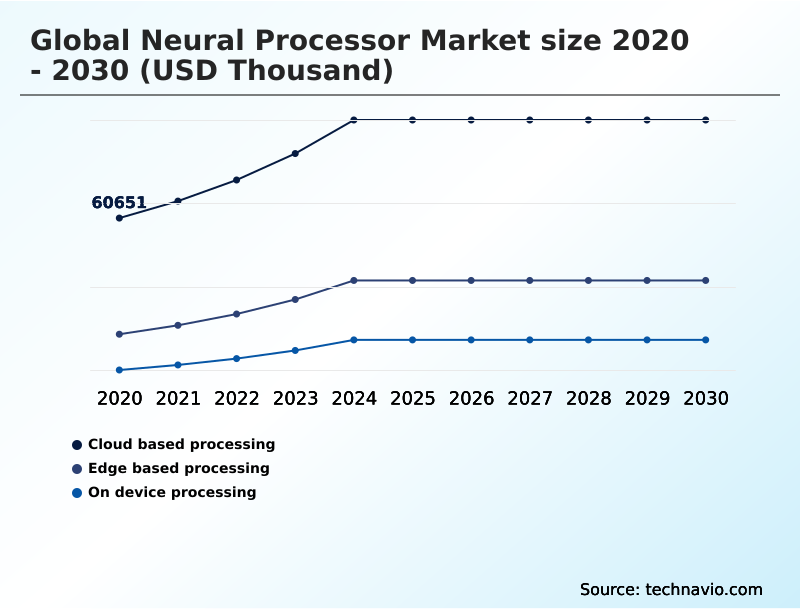

APAC accounts for 32.6% of incremental growth during the forecast period. The Cloud based processing segment by Deployment was valued at USD 89.65 million in 2024, while the Consumer electronics segment holds the largest revenue share by End-user.

The market is projected to grow by from 2020 to 2030, with USD 272.06 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Neural Processor Market Overview

The neural processor market is defined by a rapid shift toward specialized hardware acceleration, driven by the escalating complexity of AI workloads. With a year-over-year growth of 16.8%, the demand for efficient parallel computing paradigms is reshaping enterprise and consumer technology. This expansion is not uniform; North America continues to lead in deployment, but APAC is the fastest-growing region, commanding nearly 33% of the incremental growth. In a practical application, an automotive manufacturing plant deploys computer vision hardware at the end of its assembly line. This system, powered by dedicated neural network processors, performs real-time data interpretation to inspect for microscopic paint defects, reducing the manual inspection error rate and scrap costs. This level of on-device AI processing relies on sophisticated system on chip design to function without cloud latency, showcasing the market's move toward intelligent, decentralized data processing. This trend is further supported by innovations in low-latency processing and edge AI hardware, which are critical for mission-critical industrial automation.

Drivers, Trends, and Challenges in the Neural Processor Market

Strategic decisions regarding the adoption of neural processors hinge on a complex analysis that balances performance against total cost of ownership. The high cost of custom AI chip design is a significant barrier for many organizations, prompting a closer evaluation of off-the-shelf application specific integrated circuits versus developing proprietary hardware.

For instance, in a large hospital deploying an AI-powered diagnostics platform, the choice of neural processor architecture for LLMs used to analyze clinical notes is critical. The platform must adhere to strict HIPAA regulations, pushing processing to the edge. The low latency in edge computing devices is non-negotiable for real-time analysis of medical imagery.

Simultaneously, the facility must manage the energy consumption of AI hardware to comply with its ISO 50001 certification, a challenge when deploying powerful systems. This same trade-off analysis mirrors the one used for selecting a neural processor for autonomous driving, where computational power must be balanced against stringent power, thermal, and safety constraints.

The market's 20.2% growth momentum is accelerating as more industries navigate these complex hardware decisions to unlock the value of their data.

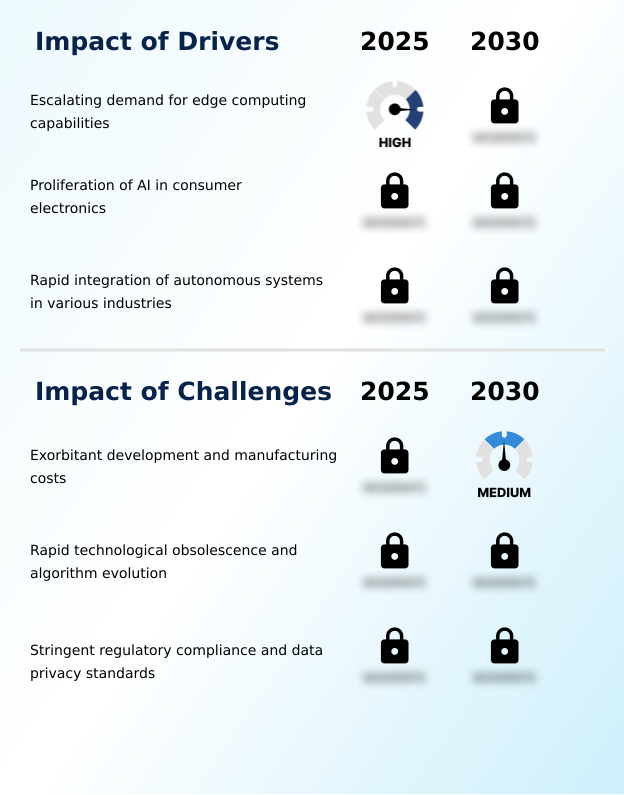

Primary Growth Driver: The escalating demand for low-latency processing in edge computing applications is a primary driver fueling market expansion.

Market growth is fundamentally driven by the proliferation of AI into latency-sensitive and power-constrained environments.

The escalating demand for edge AI hardware is a direct response to the limitations of cloud computing, enabling real-time data interpretation for industrial predictive maintenance models and smart city infrastructure.

This is amplified by the widespread integration of on-device AI processing in consumer electronics, where features like computational photography and voice recognition depend on efficient system on chip design.

Furthermore, the rapid advancement of autonomous systems navigation in the automotive sector, which contributed 32.6% to incremental growth, relies on sophisticated sensor fusion algorithms running on dedicated neural network processors.

These drivers collectively push the industry toward more powerful, efficient, and decentralized data processing capabilities.

Emerging Market Trend: A key market trend is the accelerated adoption of neuromorphic engineering and brain-inspired designs. This move toward energy-proportional architectures addresses the power and thermal limitations of conventional processors.

The market is evolving beyond raw performance, with significant trends emerging around architectural innovation and application-specific designs. An accelerated adoption of neuromorphic engineering is underway, driven by the need for more energy-efficient computing that mimics biological neural pathways, offering a solution to the thermal limitations of traditional data centers.

In parallel, the deployment of photonic neural networks is gaining momentum to address data transfer bottlenecks, using silicon photonics to enable ultra-low-latency processing for high-frequency algorithmic trading acceleration and telecommunications.

This is complemented by a surge in demand from the healthcare sector, where specialized deep learning accelerators are being integrated into medical devices for AI-powered diagnostics, fundamentally changing how clinical data is analyzed and interpreted while adhering to strict privacy mandates.

Key Industry Challenge: Exorbitant research, development, and fabrication costs for advanced process nodes represent a significant challenge to market growth and technological accessibility.

Significant challenges constrain the market's full potential, primarily stemming from economic and technological volatility. The exorbitant cost of custom silicon development and manufacturing at advanced nodes creates a high barrier to entry and inflates end-product prices.

This financial pressure is compounded by the rapid pace of algorithmic evolution; a processor optimized for today's models may be inefficient for tomorrow's generative AI workloads, leading to rapid technological obsolescence. Navigating this is further complicated by a fragmented and stringent regulatory landscape.

Companies must ensure their hardware and AI software ecosystem comply with diverse data privacy standards like GDPR in Europe and HIPAA in the US, adding significant complexity and cost to the design and validation of any hardware intended for decentralized data processing.

Explore Full Market Dynamics Analysis Request Free Sample

Neural Processor Market Segmentation

The neural processor industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Deployment Segment Analysis

The cloud based processing segment is estimated to witness significant growth during the forecast period.

Cloud-based processing remains the dominant deployment segment, accounting for over 56% of the market, driven by the intense computational demands of training large-scale AI models.

Hyperscale data centers leverage vast arrays of AI training accelerators and tensor processing units to power their cloud AI services, enabling enterprises to execute complex generative AI workloads without massive upfront capital expenditure.

This centralization facilitates data center optimization and allows for the deployment of sophisticated predictive maintenance models. However, the reliance on remote hardware introduces latency, a critical consideration for real-time applications.

The architecture of these cloud deployments is engineered for maximum throughput, utilizing high-bandwidth memory integration and advanced packaging techniques to handle petabyte-scale datasets for deep learning tasks.

The Cloud based processing segment was valued at USD 89.65 million in 2024 and showed a gradual increase during the forecast period.

Neural Processor Market by Region: APAC Leads with 32.6% Growth Share

APAC is estimated to contribute 32.6% to the growth of the global market during the forecast period.

The geographic landscape of the neural processor market is characterized by a dual-centric structure, with North America leading in design and application while APAC dominates manufacturing and shows the fastest growth, projected at a CAGR of 21.8%.

North America's market, driven by hyperscale data centers and advanced research, focuses on custom silicon development for complex AI training accelerators.

In contrast, APAC's ecosystem is the hub for high-volume production of hardware for consumer electronics and automotive-grade silicon, essential for system on chip design. This regional specialization creates a complex global supply chain.

Emerging projects in the Middle East, such as smart city infrastructure, are creating new demand hotspots for edge AI hardware and IoT device integration, diversifying the market beyond its traditional strongholds and pushing innovation in energy-efficient computing.

Customer Landscape Analysis for the Neural Processor Market

The neural processor market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the neural processor market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Neural Processor Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the neural processor market industry.

Advanced Micro Devices Inc. - Key offerings include specialized silicon such as ASICs and SoCs designed to accelerate deep learning and machine learning workloads across cloud, edge, and on-device deployments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon.com Inc.

- Apple Inc.

- Arm Ltd.

- Broadcom Inc.

- Cerebras Systems Inc.

- Google LLC

- Groq Inc.

- Hailo Technologies Ltd.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- Marvell Technology Inc.

- MediaTek Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Qualcomm Inc.

- SambaNova Systems Inc.

- Samsung Electronics Co. Ltd.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Neural Processor Market

- In January 2025, Advanced Micro Devices Inc. introduced its Ryzen AI 300 series processors, integrating the second-generation XDNA architecture to deliver over 50 TOPS of AI compute for AI-enabled laptops.

- In January 2025, at the Consumer Electronics Show, Intel Corp. introduced its Core Ultra Series 3 processors, the first commercial platform built on its 18A process node, marking a major advancement in US-based semiconductor manufacturing.

- In March 2025, Advanced Micro Devices Inc. expanded its strategic cooperation with South Korean AI lab Upstage to deploy Instinct MI355 GPUs, aiming to scale next-generation AI model training for sovereign AI initiatives.

- In April 2025, Fujitsu Ltd. announced its plan to develop a next-generation AI processor based on an advanced 1.4-nanometer fabrication process, with manufacturing to be handled domestically by Rapidus to strengthen Japan's semiconductor independence.

Research Analyst Overview: Neural Processor Market

Boardroom decisions are increasingly focused on the strategic trade-offs between leveraging third-party cloud AI services and investing in proprietary custom silicon development. This choice is complicated by the high capital expenditure and specialized expertise required for creating application specific integrated circuits, which can offer significant performance-per-watt advantages for specific generative AI workloads.

While a wafer-scale engine provides unparalleled power for training foundational models, the risk of rapid algorithmic evolution can render such specialized hardware obsolete. Therefore, many organizations are adopting a hybrid strategy, utilizing reconfigurable dataflow unit architectures and flexible AI inference chip solutions for edge AI hardware deployments.

Compliance with data regulations like GDPR further influences architecture, favoring on-device AI processing to minimize data transfer. This complex decision matrix, balancing cost, performance, and regulatory risk, is the central challenge for enterprises aiming to maintain a competitive edge through hardware acceleration and advanced packaging techniques.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Neural Processor Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.2% |

| Market growth 2026-2030 | USD 272064.2 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.8% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Israel, Saudi Arabia, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Neural Processor Market: Key Questions Answered in This Report

-

What is the expected growth of the Neural Processor Market between 2026 and 2030?

-

The Neural Processor Market is expected to grow by USD 272.06 million during 2026-2030, registering a CAGR of 20.2%. Year-over-year growth in 2026 is estimated at 16.8%%. This acceleration is shaped by escalating demand for edge computing capabilities, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based processing, Edge based processing, and On device processing), End-user (Consumer electronics, Automotive, IT and telecom, Industrial automation, and Healthcare), Application (Computer vision, Natural language processing, Autonomous systems, and Speech recognition) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Cloud based processing segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. APAC is estimated to contribute 32.6% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Israel, Saudi Arabia, South Africa, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating demand for edge computing capabilities, which is accelerating investment and industry demand. The main challenge is exorbitant development and manufacturing costs, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Neural Processor Market?

-

Key vendors include Advanced Micro Devices Inc., Amazon.com Inc., Apple Inc., Arm Ltd., Broadcom Inc., Cerebras Systems Inc., Google LLC, Groq Inc., Hailo Technologies Ltd., Huawei Technologies Co. Ltd., Intel Corp., Marvell Technology Inc., MediaTek Inc., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Qualcomm Inc., SambaNova Systems Inc., Samsung Electronics Co. Ltd. and Tenstorrent Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Neural Processor Market Research Insights

Market dynamics are increasingly shaped by the architectural trade-offs between centralized cloud deployments and decentralized edge AI hardware. While cloud-based processing constitutes the largest market segment, the imperative for real-time data interpretation in applications like industrial robotics and autonomous systems navigation is fueling growth in edge and on-device AI processing.

This shift is compounded by stringent data sovereignty and privacy regulations, such as the GDPR in Europe, which mandate that sensitive personal information be handled locally. Consequently, industries like healthcare are investing in on-premise AI-powered diagnostics that rely on localized deep learning accelerators.

This trend forces a re-evaluation of data center optimization strategies, balancing the raw power of the cloud with the security and responsiveness of localized heterogeneous computing architecture.

We can help! Our analysts can customize this neural processor market research report to meet your requirements.

RIA -

RIA -