US Nonwoven Fabrics Market Size 2024-2028

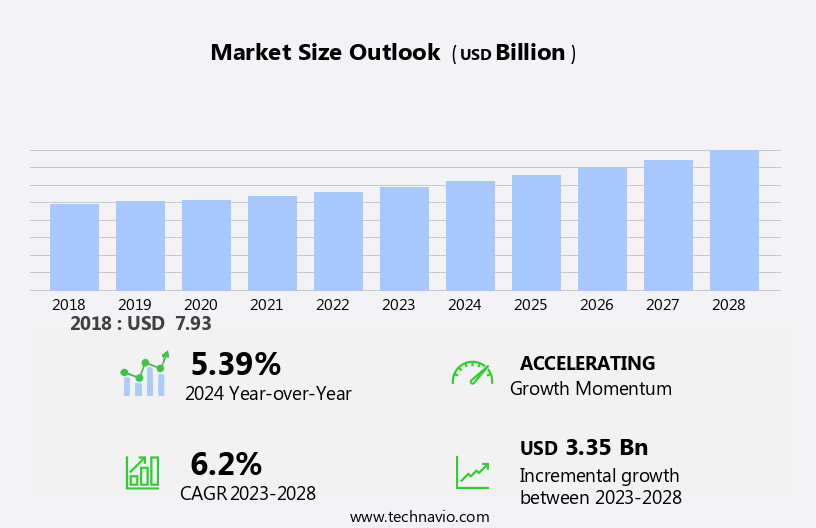

The US nonwoven fabrics market size is forecast to increase by USD 3.35 billion at a CAGR of 6.2% between 2023 and 2028.

- The market is witnessing significant growth, driven primarily by the increased consumption of hygiene products such as disposable diapers, wipes, and medical gowns. This trend is expected to continue, given the growing awareness of personal hygiene and health, particularly in the wake of the ongoing pandemic. Another key trend shaping the market is the emergence of textile recycling, which presents both opportunities and challenges. On the one hand, recycling offers a sustainable solution to the environmental concerns associated with nonwoven fabric production, particularly those made from synthetic fibers. On the other hand, the toxic nature of some synthetic fibers poses challenges in terms of safe and effective recycling processes.

- Companies seeking to capitalize on market opportunities and navigate these challenges effectively should focus on developing innovative recycling technologies and sustainable alternatives to synthetic fibers. Additionally, collaborations with industry stakeholders, including recycling companies and government agencies, can help create a circular economy for nonwoven fabrics and reduce the environmental impact of the industry.

What will be the size of the US Nonwoven Fabrics Market during the forecast period?

- The nonwoven fabrics market encompasses a diverse range of solutions, primarily utilized in various industries such as hygiene, medical, construction, and filtration. In the modern healthcare sector, nonwoven fabrics are indispensable, finding extensive applications in areas like wound management, personal protective equipment, and disposable medical devices. The global population trends, including a growing adult population and increasing birth rate, fuel the demand for nonwoven fabrics in hygiene applications, including sanitary towels, sanitary napkins, tampons, and baby diapers. Additionally, nonwoven fabrics are increasingly used in the construction industry due to their durability and strength, contributing to the growth of the market.

- Furthermore, the emergence of new applications, such as in electric vehicle, electronic components, batteries, and capacitors, presents significant opportunities for market expansion. Overall, the nonwoven fabrics market is poised for continued growth, driven by the versatility and utility of these innovative materials.

How is this market segmented?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hygiene

- Medical

- Textile

- Automotive

- Others

- Technology

- Spunbound

- Wetlaid

- Drylaid

- Type

- Disposable

- Durables

- Geography

- US

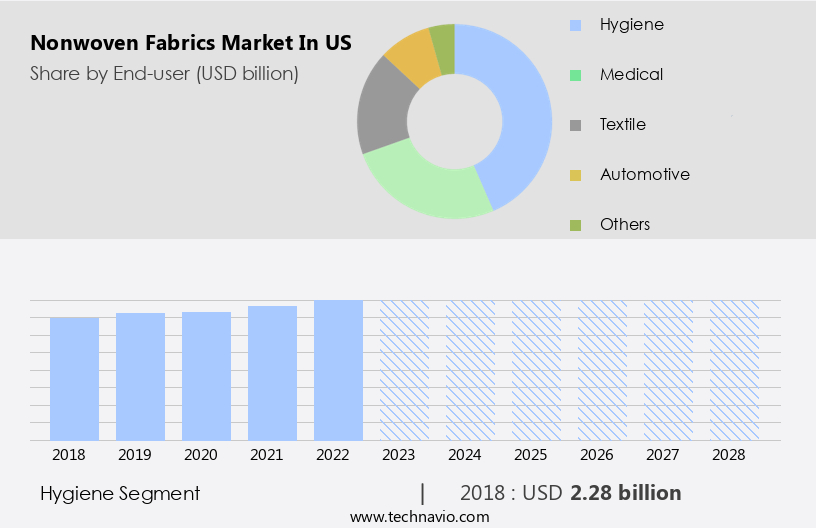

By End-user Insights

The hygiene segment is estimated to witness significant growth during the forecast period. Nonwoven fabrics have gained significant traction in the US market due to their extensive usage in various industries, particularly in hygiene and medical applications. In the hygiene sector, nonwoven fabrics are utilized in the production of disposable products such as baby diapers, sanitary napkins, and adult incontinence items. These fabrics offer advantages like lightweight, ease of use, and effective prevention of cross-infection and unpleasant odors. Hydrophobic, hydrophilic, perforated, super-soft, and elastic spun-bonded nonwoven fabrics are commonly used in this segment. In the medical sector, these fabrics are employed in the manufacturing of healthcare essentials, including disposable hospital supplies, nonwoven protection materials, and filter materials for face masks.

Furthermore, the face mask market encompasses various categories like N95 (FFP2), N99 (FFP3), civil masks, surgical masks, and respiratory masks. These fabrics contribute to the durability and strength of these masks, making them essential in medical applications. Construction activities also benefit from nonwoven fabrics, with applications including geosynthetics, sheet and web structures, fiber and filaments, and roofing components. The versatility and strength make them suitable for use in various industries, including agriculture, healthcare, and construction. These fabrics are manufactured using synthetic fibers like polyester, cotton, carbon fibers, glass fibers, high tenacity yarns, aramids, nanofibe, and polypropylene. The choice of fiber depends on the specific application requirements.

Get a glance at the market share of various segments Request Free Sample

The Hygiene segment was valued at USD 2.28 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Nonwoven Fabrics Market?

- Increased consumption of hygiene products is the key driver of the market. Nonwoven fabrics in the US market primarily cater to the hygiene end-user applications segment. This segment encompasses products for babies, adults, and feminine hygiene. The demand for these products has witnessed significant growth in recent years and is anticipated to continue expanding during the forecast period. The increasing focus on personal hygiene and product innovations, coupled with rising living standards and growing public health awareness, are key factors driving the consumption of hygiene products.

- Among various types of nonwoven fabrics, those derived from Polypropylene are extensively used in hygiene applications due to their desirable properties, such as low weight, low specific gravity, and resistance to bacteria.

What are the market trends shaping the US Nonwoven Fabrics Market?

- The emergence of textile recycling is the upcoming trend in the market. The market is witnessing a notable trend towards textile recycling. With growing environmental consciousness and the increasing demand for sustainable materials, textile recycling is becoming a popular solution to address the issue of textile waste in the country. This process involves the collection, sorting, and processing of textile waste to produce new materials, including recycled spunbond nonwoven fabrics.

- These fabrics, known for their high strength, long lifespan, and water resistance, are commonly used in single-use items and are excellent candidates for recycling. The adoption of textile recycling is expected to increase significantly during the forecast period, driving the demand for recycled nonwoven fabrics in various applications.

What challenges does the US Nonwoven Fabrics Market face during the growth?

- The toxic nature of synthetic fibers is a key challenge affecting the market growth. Nonwoven fabrics derived from various fibers, including petroleum-based synthetic fibers like polyester, have gained popularity due to their versatility and durability. However, the environmental impact of textile production, particularly from non-renewable resources, is a significant concern. Regulatory authorities have responded by imposing stricter regulations on the application and consumption of manmade fibers, such as polyester, due to health and environmental concerns. Petroleum-based nonwoven fabrics, including those made from polyester chips, PE, and PP, are non-biodegradable and contribute to the accumulation of waste in the ecosystem.

- The production of these fabrics is energy-intensive and reliant on non-renewable resources, increasing their carbon footprint. As a responsible business, it is crucial to consider the environmental implications of using these fabrics and explore sustainable alternatives.

Exclusive US Nonwoven Fabrics Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Ahlstrom Holding 3 Oy

- Berkshire Hathaway Inc.

- Berry Global Inc.

- Celanese Corp.

- DuPont de Nemours Inc.

- Exxon Mobil Corp.

- Fitesa S.A. and Affiliates

- Freudenberg and Co. KG

- Glatfelter Corp.

- Hollingsworth and Vose

- Jasztex Inc.

- Kimberly Clark Corp.

- PFNonwovens Holding s.r.o.

- Sommers Nonwoven Solutions

- Suominen Corp.

- Toray Industries Inc.

- TWE GmbH and Co. KG

- Unifrax I LLC

- VPC Group Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Nonwoven fabrics have gained significant traction in various industries due to their unique properties and versatility. These fabrics, which are manufactured without the use of traditional weaving or knitting methods, offer several advantages over their woven and knitted counterparts. These fabrics are widely used in the production of hygiene and medical solutions. Their ability to provide a high level of protection and absorbency makes them an ideal choice for healthcare essentials. Disposable hospital supplies, such as surgical gowns, drapes, gloves, and instrument wraps, are essential components of medical facilities. The increasing birth rate and geriatric population have led to a rise in demand for nonwoven materials in the production of diapers, sanitary napkins, tampons, and other hygiene products. Cost-sensitive hospitals require disposable surgical gowns, drapes, gloves, instrument wraps, and other nonwoven products for infection control.

Moreover, the construction industry is another major consumer of nonwoven fabrics. These materials offer excellent durability and strength, making them suitable for use in various applications. Geotextiles, which are used in construction activities to separate, filter, and reinforce soil, are a significant application area for nonwoven fabrics. Synthetic fibers, such as polyester, cotton, carbon fibers, glass fibers, high tenacity yarns, aramids, nanofiber, polypropylene, and others, are commonly used in the production for the construction industry. The growing demand in various industries is driven by several factors. The increasing use of nonwoven materials in the production of face masks, particularly in response to the COVID-19 pandemic, has led to a significant increase in demand.

Furthermore, these fabrics are used in the production of various types of face masks, including N95, FFP2 (N95), and FFP3 (N99), which offer different levels of protection against airborne particles. The agricultural industry is another major consumer of nonwoven fabrics. These materials are used in the production of various agricultural products, such as greenhouse shading, insulation, and modified bitumen roofing. These fabrics are also used in the production of pavement overlays, roadway reinforcements, and roofing components. The use of these fabrics in the production of electronic components, such as batteries and capacitors, is another emerging application area. These fabrics offer excellent electrical insulation properties and are used in the production of various electronic components.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.2% |

|

Market growth 2024-2028 |

USD 3.35 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.39 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -