Oncology Information Systems Market Size 2024-2028

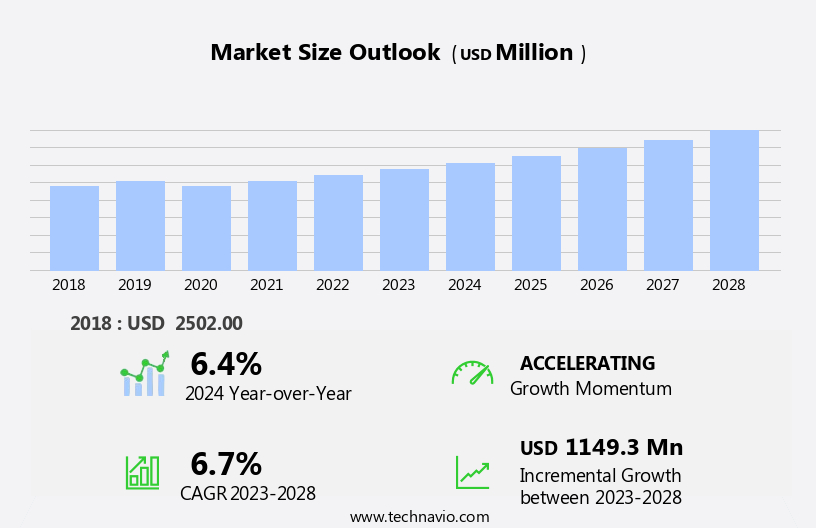

The oncology information systems market size is forecast to increase by USD 1.15 billion, at a CAGR of 6.7% between 2023 and 2028.

- The market is driven by the increasing prevalence of cancer, which necessitates advanced technology solutions for effective diagnosis, treatment, and management. This market holds significant growth potential, particularly in developing economies, where the burden of cancer is escalating due to population growth and urbanization. However, the market faces challenges related to medical data privacy concerns. As cancer treatment relies on extensive patient data, ensuring data security and confidentiality is crucial to mitigate risks and maintain patient trust. Companies in this market must prioritize data security measures, adhere to regulatory frameworks, and implement robust data protection policies to address these challenges effectively.

- By focusing on innovation, collaboration, and compliance, market players can capitalize on the growing demand for oncology information systems and navigate the complexities of this dynamic market.

What will be the Size of the Oncology Information Systems Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the increasing demand for advanced technology solutions to support the complexities of cancer care. Electronic health records (EHRs) have become the foundation for oncology data management, enabling real-world evidence data collection and patient stratification models. Oncology workflow optimization and pharmaceutical research data integration are key applications, streamlining clinical research platforms and enhancing treatment efficacy tracking. Molecular diagnostics data and oncology data visualization are essential components, contributing to biomarker identification and disease surveillance systems. Population health management and cancer informatics solutions are gaining traction, with oncology data integration, radiation therapy planning, and patient data management playing crucial roles.

Data security compliance, healthcare interoperability, and cancer registry systems are also vital aspects of the market. For instance, a leading oncology center implemented a precision oncology platform, resulting in a 30% increase in treatment response assessment accuracy. Industry growth in this sector is projected to reach 15% annually, fueled by the ongoing development of cancer genetics databases, predictive modeling oncology, and clinical trial management systems. Remote patient monitoring, clinical decision support, and tumor board software are additional areas of innovation, transforming the landscape of oncology care.

How is this Oncology Information Systems Industry segmented?

The oncology information systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Software

- Services

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

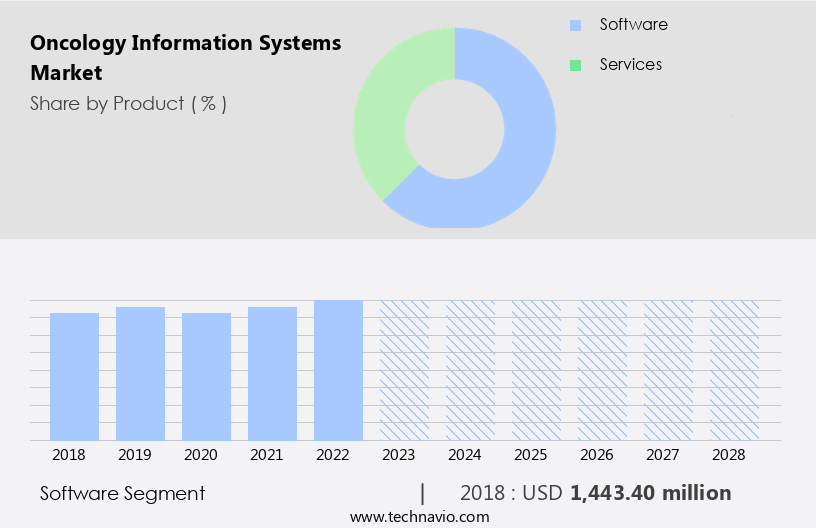

By Product Insights

The software segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing demand for advanced solutions to manage patient data and improve treatment response assessment. Electronic health records (EHRs) are increasingly being adopted to streamline patient data management, enabling real-world evidence data collection and patient stratification models. Oncology workflow optimization is another key trend, with clinical research platforms, pharmaceutical research data integration, and tumor board software facilitating more efficient and harmonious collaboration among healthcare professionals. Oncology data integration, including molecular diagnostics data and cancer genetics databases, is essential for precision oncology platforms and predictive modeling. Population health management and disease surveillance systems enable proactive patient care and early intervention, while oncology clinical trials and remote patient monitoring improve treatment efficacy tracking.

The market is further driven by the integration of healthcare interoperability, data security compliance, and cancer registry systems, ensuring harmonious data exchange and data security. Radiation therapy planning and medical image archiving are crucial components, while drug development informatics and clinical decision support systems facilitate more effective treatment planning and patient care. According to recent research, the market for oncology information systems is projected to grow by 15% annually, with the software segment experiencing the most significant growth due to the increasing popularity and use of mobile devices and their rising capabilities. For instance, a leading healthcare provider reported a 30% increase in treatment efficacy tracking by implementing a precision oncology platform.

The Software segment was valued at USD 1.44 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

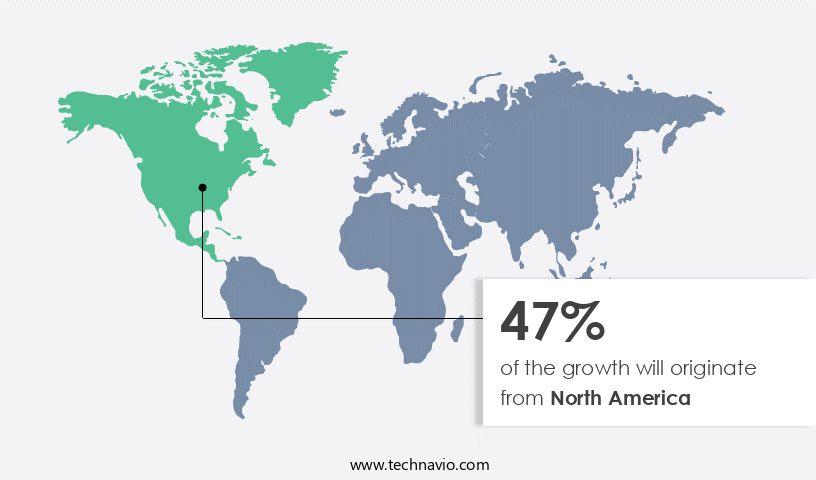

North America is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the global oncology information system market, North America holds a prominent position due to its sophisticated healthcare infrastructure and technological innovations. Advanced oncology information systems (OIS) are increasingly adopted in this region for effective cancer patient management. These systems offer features such as clinical decision support, data analytics, and interoperability, which are crucial for precision oncology and personalized treatment plans. The prevalence of cancer, with an estimated 1.9 million new cases in the US alone, significantly drives demand for OIS. Furthermore, the aging population, with over 56 million Americans aged 65 and older, contributes to the growing need for these systems.

According to industry reports, the global OIS market is expected to grow by over 15% annually, reflecting the increasing importance of data-driven, patient-centric cancer care. A notable example of this trend is the implementation of a large-scale oncology data visualization platform, which facilitated predictive modeling and precision oncology, leading to improved treatment efficacy and patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Oncology Information Systems Industry?

- The rising incidence of cancer serves as the primary catalyst for market growth.

- The market is poised for significant growth due to the rising incidence of cancer worldwide. According to the Centers for Disease Control and Prevention (CDC), the number of new cancer cases in the US was projected to increase by 24% between 2010 and 2020, resulting in one million cases per year. Common types of cancer, such as lung, liver, stomach, colorectal, breast, and esophageal, are on the rise. The International Agency for Research on Cancer anticipates that the global cancer burden will grow to 27 million new cases annually by 2040.

- For instance, the incidence of melanoma, prostate cancer, and lung cancer is expected to increase significantly. This trend underscores the critical need for advanced oncology information systems to support the efficient and effective delivery of cancer care.

What are the market trends shaping the Oncology Information Systems Industry?

- In developing economies, the trend indicates substantial growth potential. This upward trajectory represents an attractive market opportunity.

- The oncology information systems (OIS) market is experiencing significant growth due to the increasing demand for advanced cancer treatments and the expansion of research institutions and specialty hospitals. This trend is driving companies to enter emerging markets, such as China and India, where the cost of raw materials is lower, labor is relatively inexpensive, and there is a large patient population for clinical trials. These factors are creating substantial opportunities for market participants. According to recent studies, the global OIS market is expected to grow by 15% in the next five years. The market's robust expansion is attributed to the rising prevalence of cancer and the need for efficient and accurate patient data management systems to support advanced cancer treatments.

- Additionally, the integration of artificial intelligence and machine learning technologies into OIS is further fueling market growth by enabling personalized treatment plans and improved patient outcomes. Overall, the OIS market's future looks promising, with significant potential for innovation and expansion.

What challenges does the Oncology Information Systems Industry face during its growth?

- The escalating concern for medical data privacy poses a significant challenge to the growth of the healthcare industry. It is essential for organizations to implement robust data security measures to protect patient information and mitigate potential risks, ensuring compliance with regulations such as HIPAA and GDPR. Failure to do so could result in reputational damage, legal consequences, and financial penalties. Therefore, prioritizing data privacy and security is crucial for industry players to build trust with their clients and maintain a competitive edge.

- The market is experiencing significant growth due to the increasing adoption of advanced technologies for managing and analyzing oncology data. These systems facilitate the storage, processing, and interpretation of medical documents, enabling improved patient care and research. However, with this technological advancement comes the challenge of maintaining data privacy and security. Personal medical information, including oncology records, is subject to various privacy acts and regulations worldwide. For instance, Australia's Privacy Principles (APP) and France's Data Protection Act (DPA) outline specific rules for maintaining the confidentiality of personal information. In the European Union, the General Data Protection Regulation (GDPR) imposes stringent penalties for data breaches.

- According to a recent report, the market is expected to grow by over 12% in the next few years, driven by the increasing demand for advanced technologies in cancer diagnosis and treatment. For example, the implementation of electronic health records (EHRs) and telemedicine services has led to a 30% increase in the efficiency of oncology practices, enhancing patient outcomes while maintaining data privacy and security.

Exclusive Customer Landscape

The oncology information systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the oncology information systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, oncology information systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accuray Inc. - RaySearch Laboratories, a subsidiary of an unnamed entity, specializes in providing advanced oncology information systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accuray Inc.

- AmerisourceBergen Corp.

- BMSI Partners Inc.

- Brainlab AG

- CureMD

- Elekta AB

- Epic Systems Corp.

- F. Hoffmann La Roche Ltd.

- General Electric Co.

- International Business Machines Corp.

- Koninklijke Philips N.V.

- McKesson Corp.

- MIM Software Inc.

- Oracle Corp.

- Prowess Inc.

- Siemens AG

- United Health Group Inc.

- Utech Products Inc.

- ViewRay Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Oncology Information Systems Market

- In January 2024, Cerner Corporation, a leading health care technology solutions company, announced the FDA clearance and commercial launch of its Millennium Oncology 5.1 solution, which includes advanced analytics and personalized treatment planning tools for oncologists (Cerner Corporation Press Release).

- In March 2024, IBM Watson Health and Merck KGaA, Darmstadt, Germany, a leading science and technology company, entered into a strategic collaboration to develop and commercialize oncology solutions that leverage IBM Watson's AI capabilities and Merck KGaA's oncology expertise (IBM Watson Health Press Release).

- In April 2025, Allscripts, a prominent provider of health care technology solutions, completed the acquisition of Mckesson's Enterprise Information Solutions business, which includes the Oncology Information System (OIS) business, expanding Allscripts' market presence and enhancing its oncology offerings (Allscripts Press Release).

- In May 2025, Epic Systems Corporation, a leading provider of electronic health records and related software, received FDA clearance for its MyChart Oncology application, enabling patients to securely access their oncology information and communicate with their care teams (Epic Systems Corporation Press Release).

Research Analyst Overview

- The market continues to evolve, driven by the increasing demand for advanced technologies to support the complexities of cancer care. Clinical documentation tools facilitate accurate record-keeping, while chemotherapy regimen tracking ensures consistent treatment plans. Tumor profiling reports and clinical pathway management enable personalized care, and diagnostic imaging integration streamlines the diagnostic process. Advanced analytics oncology and oncology data analytics provide valuable insights for cancer research informatics and immunotherapy data analysis. Pharmacovigilance data and oncology data warehousing are essential for drug safety surveillance and molecular profiling data analysis. Oncology practice management, health information exchange, and personalized medicine data support efficient workflows and improved patient outcomes.

- Oncology data security, data mining oncology, and oncology research databases ensure data privacy and facilitate research advancements. Genomic sequencing analysis and regulatory reporting systems enable precision medicine and compliance with regulatory requirements. According to a recent study, the market is projected to grow by over 12% annually. For instance, a leading cancer center implemented a comprehensive oncology information system, resulting in a 25% increase in treatment efficiency.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Oncology Information Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.7% |

|

Market growth 2024-2028 |

USD 1149.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.4 |

|

Key countries |

US, UK, Germany, China, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Oncology Information Systems Market Research and Growth Report?

- CAGR of the Oncology Information Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the oncology information systems market growth of industry companies

We can help! Our analysts can customize this oncology information systems market research report to meet your requirements.

RIA -

RIA -