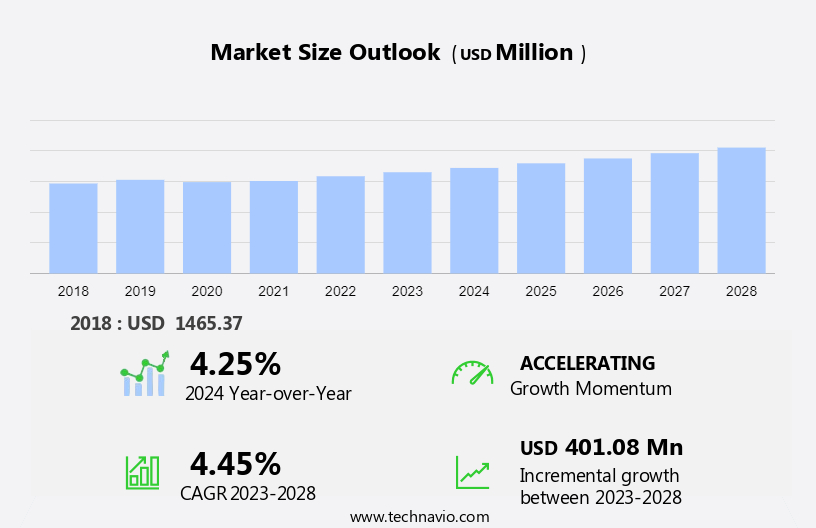

US Onshore Drilling Fluid Market Size 2024-2028

The US onshore drilling fluid market size is forecast to increase by USD 401.08 million at a CAGR of 4.45% between 2023 and 2028.

- In the US onshore drilling fluid market, the demand for sustainable drilling fluids is on the rise due to growing concerns over environmental hazards posed by single-use plastics, such as plastic bottles, in the oil and gas industry. This trend is driven by increasing awareness and regulations, including those related to BPA-free materials and recycled materials. The market is also influenced by the popularity of reusable water bottles and kitchenware, which are becoming preferred choices for picnics and other outdoor activities.

- Additionally, stringent regulatory frameworks continue to shape the market, with a focus on secure materials that minimize the risk of contamination and ensure the safety of workers and the environment. The onshore drilling fluid market in the US is expected to experience steady growth, driven by these trends and the need for sustainable and secure drilling solutions.

What will be the Size of the Market During the Forecast Period?

- The onshore drilling fluid market in the US is a critical component of the oil and gas industry, supplying fluids that enable efficient and safe drilling operations. This market is influenced by various market dynamics and trends, which are shaping its growth and development. Firstly, the market is experiencing increasing price pressure due to the volatile nature of crude oil prices and the need to reduce operational costs. Drilling fluid suppliers are responding to this trend by offering cost-effective solutions without compromising on performance. This is leading to the adoption of innovative technologies and the use of recycled fluids to minimize costs and reduce the environmental impact of drilling operations.

- Another significant trend in the onshore drilling fluid market is the growing demand for eco-friendly and sustainable solutions. The increasing environmental awareness and the push towards a circular economy are driving this trend. Suppliers are responding by offering fluids made from biodegradable materials and implementing green initiatives to minimize the environmental footprint of their operations. Moreover, the market is witnessing a shift towards tech-savvy customers who demand advanced features and customized solutions. Drilling fluid suppliers are responding to this trend by offering water-based fluids with superior drilling performance and advanced additives that enhance drilling efficiency and reduce downtime.

- Furthermore, the onshore drilling fluid market in the US is being influenced by the sustainable development goals (SDGs) and the push towards responsible consumption and climate change mitigation. Suppliers are responding by offering fluids that reduce water consumption, minimize waste, and have a lower carbon footprint. In addition, there is a growing trend towards urban greening and community gardening, which is driving the demand for sustainable agriculture practices. This trend is leading to an increased focus on the use of onshore drilling fluids that are free from harmful chemicals and do not pose a risk to groundwater resources.

- Lastly, the onshore drilling fluid market in the US is being shaped by the growing demand for renewable energy and green technology. Drilling fluid suppliers are responding to this trend by offering fluids that are compatible with renewable energy sources and have a lower environmental impact. Thus, the onshore drilling fluid market in the US is a dynamic and evolving market, influenced by various market trends and dynamics. Suppliers are responding to these trends by offering cost-effective, eco-friendly, and sustainable solutions that meet the evolving needs of their customers. The market is expected to continue growing, driven by the increasing demand for oil and gas and the push towards a more sustainable and responsible energy industry.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product Type

- Water-based

- Oil-based

- Synthetic-based

- Method

- HPHT

- Conventional

- Type

- Permian

- Eagle Ford

- Niobrara

- Others

- Geography

- US

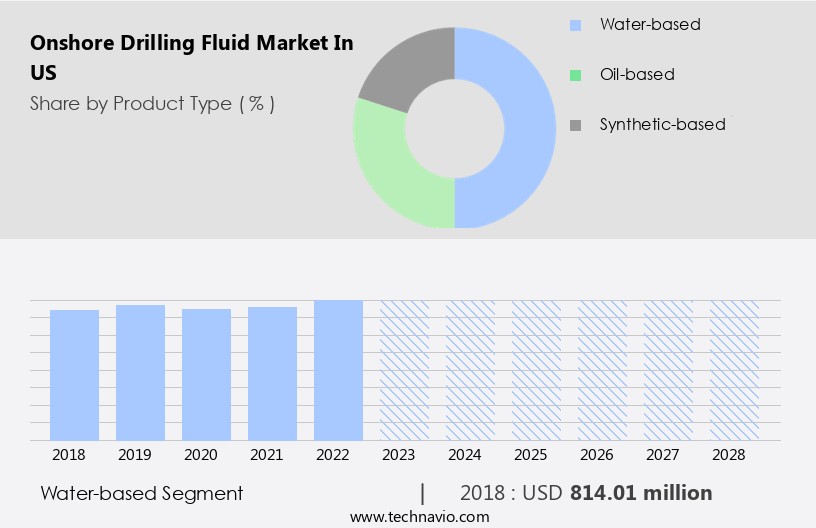

By Product Type Insights

- The water-based segment is estimated to witness significant growth during the forecast period.

In the US onshore drilling market, water-based drilling fluids have gained significant traction due to their eco-friendly properties. These fluids, primarily composed of water, offer several advantages over oil- or synthetic-based alternatives. One of the primary reasons for their popularity is their minimal carbon footprint. Unlike their oil-based counterparts, water-based drilling fluids are less toxic and simpler to dispose of, aligning with the oil and gas industry's growing commitment to sustainability. Moreover, water-based drilling fluids are compatible with sensitive formations, reducing the risk of damaging reservoir rock and enhancing overall drilling efficiency. This is crucial for preserving the environment, especially in areas with high ecological significance, such as public trails, drinking water fountains, and outdoor recreation sites.

Additionally, as the trend towards eco-friendly practices continues, single-use plastic bottles and other non-biodegradable materials are being phased out in favor of reusable drinkware made of metal, glass, and other sustainable materials. This single-use plastic ban is not only beneficial for the environment but also for the onshore drilling industry, as water-based drilling fluids contribute less to landfill waste. Thus, water-based onshore drilling fluids are a smart and sustainable choice for the US drilling market. They offer numerous benefits, including a reduced carbon footprint, compatibility with sensitive formations, and alignment with eco-friendly practices, making them a preferred option for operators seeking to minimize their environmental impact.

Get a glance at the market share of various segments Request Free Sample

The water-based segment was valued at USD 814.01 million in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Onshore Drilling Fluid Market?

Growth in demand for oil and natural gas is the key driver of the market.

- The Onshore Drilling Fluid Market in the US is experiencing significant growth due to the increasing demand for oil and gas, with the Energy Information Administration (EIA) predicting a rise in global liquid fuel consumption by 1.4 million b/d by the end of 2024 and 1.3 million b/d by 2025, primarily in non-OECD Asian countries. In response, there is a growing need to explore and develop new oil and gas reservoirs in the US. Onshore drilling fluid market participants face fierce competition, requiring high-quality, durable, and customized solutions to meet the demands of drilling operations. Technical developments, such as insulation technologies, temperature management, and pattern recognition, are essential to maintain profit margins and meet stringent regulatory frameworks.

- Similarly, raw materials, such as recycled plastic, are increasingly being used to create eco-friendly, reusable bottles, aligning with consumers' growing preference for sustainability and hygienic practices. Built-in straws, self-cleaning bottles, and bluetooth connectivity are additional features that cater to the lifestyle changes and outdoor activities of the US population. The market is also influenced by factors such as the plastic problem, single-use plastic bans, and environmental-friendly manufacturing practices. Quality standards, customization, and functionality are crucial in differentiating offerings and meeting the diverse needs of customers. Investments in shale gas and shale oil, as well as hydrogen sulfide and wellbore gasses, require specialized drilling muds and lubricant filtration systems to ensure safe and efficient drilling operations.

- Consequently, capillary pressure, pH levels, and synthetic-based fluids are critical considerations in the development of these systems. As the market evolves, it is essential to address environmental hazards, such as hydrogen sulfide and ultra-deep water drilling, while maintaining a focus on sustainability, hygienic practices, and functionality. The use of BPA-free, reusable water bottles and eco-friendly alternatives to single-use plastic is becoming increasingly important for both consumers and governments. In summary, the Onshore Drilling Fluid Market in the US is a dynamic and evolving industry, driven by the need to meet the growing demand for oil and gas while addressing environmental concerns and maintaining profitability. Participants must focus on technical developments, sustainability, and customization to remain competitive and meet the diverse needs of their customers.

What are the market trends shaping the US Onshore Drilling Fluid Market?

The rise in demand for sustainable onshore drilling fluids is the upcoming trend in the market.

- The onshore drilling fluid market in the US is experiencing a significant shift towards sustainable drilling fluid solutions. This trend is driven by a combination of factors, including stringent regulatory requirements and corporate social responsibility initiatives within the oil and gas industry. To meet these demands, market participants are developing drilling fluid formulations that minimize environmental impact. These eco-friendly alternatives address concerns related to groundwater contamination, plastic waste, and carbon footprint. Historically, drilling operations relied on oil-based fluids, which have been linked to environmental hazards such as hydrogen sulfide and wellbore gasses. However, technological advancements have led to the emergence of synthetic-based and water-based fluids.

- These new formulations offer improved lubrication, filtration, and temperature management capabilities, making them more effective and sustainable alternatives. Customization is another key trend in the onshore drilling fluid market, with customized alternatives catering to specific drilling conditions, such as pH levels, capillary pressure, and drilling mud properties. These customized solutions not only enhance functionality but also contribute to cost savings through improved efficiency and reduced waste. As consumers increasingly prioritize sustainability in their purchasing decisions, demand for reusable water bottles and other eco-friendly alternatives has grown. This trend extends to the onshore drilling fluid market, where the use of recycled materials, self-cleaning bottles, and built-in straws is becoming more common.

- Additionally, durability and hygienic practices are essential considerations for both consumers and drilling operations, ensuring the long-term viability of these solutions. Competition in the onshore drilling fluid market is fierce, with key players investing in research and development to stay ahead. Technical developments, such as bluetooth connectivity and insulation technologies, are enhancing the functionality and performance of drilling fluids. Quality standards and sustainability are essential factors in the decision-making process for both buyers and regulators, ensuring that the market remains focused on delivering eco-friendly, high-performance solutions. In summary, the onshore drilling fluid market in the US is undergoing a transformation, driven by a growing focus on sustainability, stringent regulatory requirements, and evolving consumer preferences. This shift is leading to the development of innovative, eco-friendly drilling fluid solutions that offer improved performance, cost savings, and reduced environmental impact.

What challenges does US Onshore Drilling Fluid Market face during the growth?

Stringent government regulations is a key challenge affecting the market growth.

- The Onshore Drilling Fluid Market in the US is influenced by various factors, including drilling activities, environmental regulations, and technological advancements. Drilling, well intervention, well completion, and production are integral parts of the oil and gas industry, with hydraulic fracturing and acidizing being notable completion methods. However, these processes can result in environmental concerns, such as the release of natural gases, chemicals, and groundwater contamination. To mitigate these issues, companies must adhere to stringent regulatory frameworks and invest in eco-friendly manufacturing practices. Reusable water bottles made from recycled plastic, for instance, have gained popularity due to their sustainability and hygienic benefits.

- These bottles offer customization, durability, and built-in straws, making them suitable for outdoor activities and fitness applications. Technical developments in insulation technologies, temperature management, and patterned designs have further enhanced the functionality of reusable bottles. As lifestyle changes and urbanization continue, governments and organizations are promoting the use of non-disposable, environmentally-friendly alternatives to single-use plastic bottles. This shift is expected to impact various industries, including kitchenware, household products, and outdoor recreation.

- Moreover, the transition from oil-based fluids to synthetic-based drilling chemicals and lubricant filtration systems is improving drilling operations' efficiency and reducing environmental hazards. These advancements, coupled with the increasing focus on sustainability and hygienic practices, are shaping the future of the Onshore Drilling Fluid Market in the US.

Exclusive US Onshore Drilling Fluid Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Active Minerals International LLC

- Baker Hughes Co.

- CES Energy Solutions Corp.

- Chevron Phillips Chemical Co. LLC

- Diversity Technologies Corp.

- Economy Polymers and Chemicals

- FDF Energy

- Global Drilling Fluids and Chemicals Ltd.

- Gumpro Drilling Fluids

- Halliburton Co.

- HMC Fluids and Engineering

- Imdex Ltd.

- Impact Fluid Solutions

- MATRIX Construction Products LLC

- Newpark Resources Inc.

- NOV Inc.

- Quaker Chemical Corp.

- Schlumberger Ltd.

- SUPREME DRILLING FLUID CHEMICALS

- Weatherford International Plc

- China Petroleum and Chemical Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The onshore drilling fluid market in the US has a historical footprint of providing essential fluids for drilling operations. These fluids play a crucial role in ensuring the efficiency and durability of drilling processes. The market is characterized by fierce player competitions, driven by profit margins and a sense of ownership among key players. Technical developments and sustainability are at the forefront of the industry. Customers seek reusable water bottles for outdoor activities and fitness applications, prioritizing functionality, insulation technologies, and temperature management. Customized alternatives, such as self-cleaning bottles with built-in straws, cater to personal preferences. Environmental concerns are increasingly important, with a focus on eco-friendly manufacturing, recycled plastic, and BPA-free materials.

Similarly, stringent regulatory frameworks aim to reduce the environmental impact of single-use plastic bottles and promote the use of sustainable materials. The onshore drilling fluid market adapts to these trends, offering non-disposable, environmental-friendly alternatives to oil-based fluids. These solutions contribute to reducing carbon footprint and minimizing environmental hazards, aligning with the growing demand for sustainability. Governments and local green spaces encourage the use of reusable water bottles, addressing the plastic problem and promoting lifestyle changes. The industry responds by providing a wide range of options, from metal and glass to insulated bottles, catering to various customer needs and preferences.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.45% |

|

Market growth 2024-2028 |

USD 401.08 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.25 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -