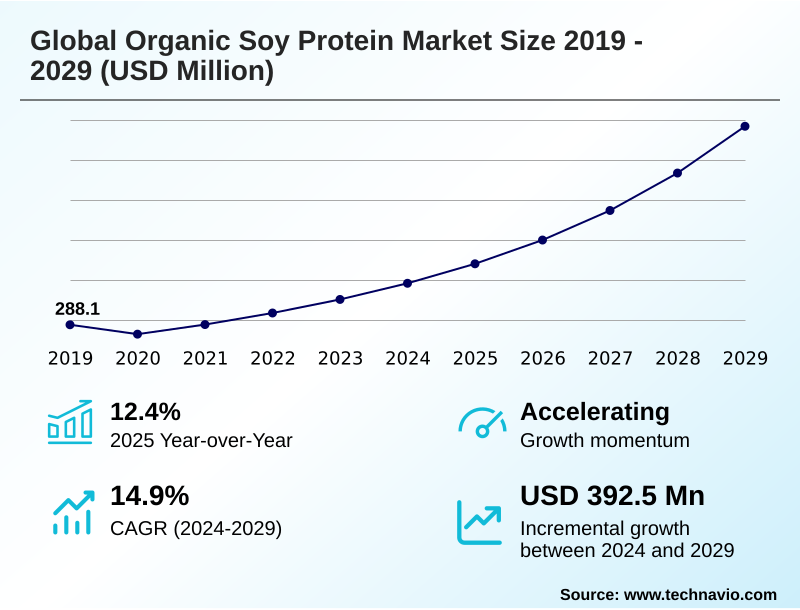

Organic Soy Protein Market Size 2025-2029

The organic soy protein market size is valued to increase by USD 392.5 million, at a CAGR of 14.9% from 2024 to 2029. Convergence of health, sustainability, and clean-label consumerism will drive the organic soy protein market.

Major Market Trends & Insights

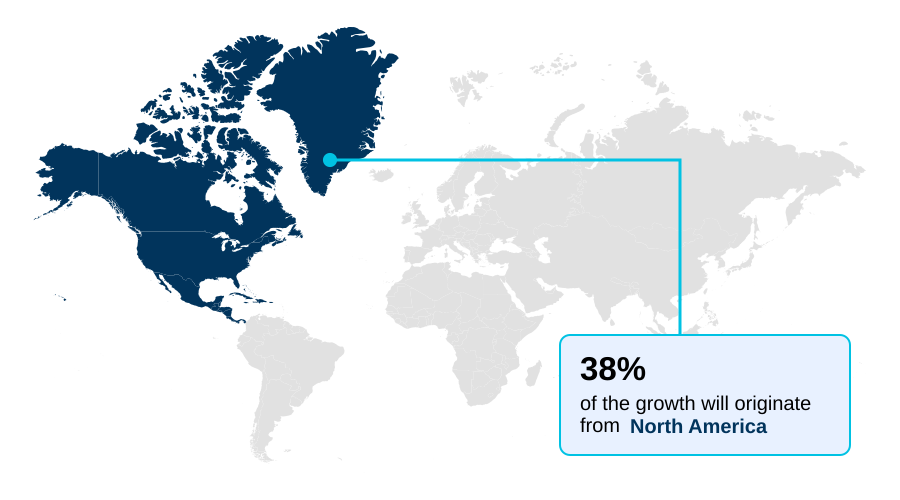

- North America dominated the market and accounted for a 37.9% growth during the forecast period.

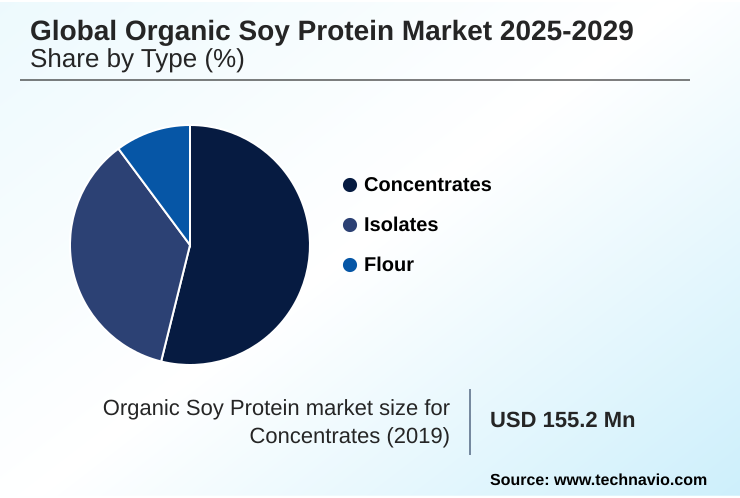

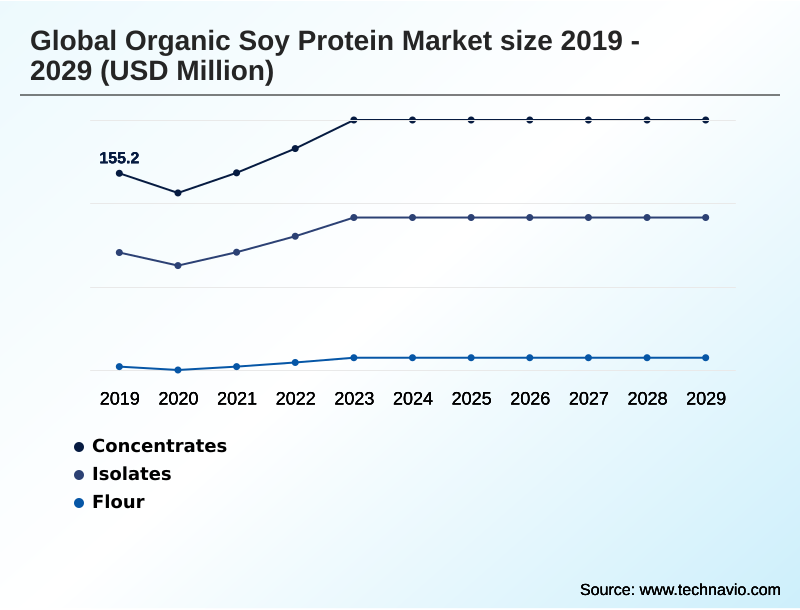

- By Type - Concentrates segment was valued at USD 189.9 million in 2023

- By Application - Functional foods segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 496.2 million

- Market Future Opportunities: USD 392.5 million

- CAGR from 2024 to 2029 : 14.9%

Market Summary

- The organic soy protein market is defined by its role as a premier plant-based protein source for health-conscious consumers. Growth is fundamentally tied to the increasing demand for clean-label soy ingredients that are non-gmo and produced via certified organic farming practices.

- This shift fuels the adoption of soy protein isolates and concentrates across diverse applications, from meat analogue ingredient formulations to bakery product fortification. A significant trend involves technological advancements in the aqueous extraction process and membrane filtration technology, aimed at improving soy protein functionality, such as water binding capacity and emulsification properties, while minimizing off-flavors.

- However, the market grapples with supply chain complexities, including maintaining identity preservation systems and ensuring sustainable soy sourcing. For instance, a food manufacturer relying on textured soy protein for a new product line must navigate potential price volatility and supply inconsistencies, making robust supplier verification and multi-sourcing strategies critical for maintaining production continuity and cost control.

- This underscores the need for advanced traceability in the soy supply chain to meet both regulatory and consumer expectations.

What will be the Size of the Organic Soy Protein Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Organic Soy Protein Market Segmented?

The organic soy protein industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Concentrates

- Isolates

- Flour

- Application

- Functional foods

- Meat alternatives

- Bakery and confectionery

- Infant formula

- Others

- Product type

- Dry

- Liquid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Type Insights

The concentrates segment is estimated to witness significant growth during the forecast period.

The market is segmented by type, including isolates, flour, and concentrates. Soy protein concentrates are a pivotal segment, produced from defatted soy flour via soy protein extraction technology like aqueous extraction.

This plant-based protein source has a protein content typically ranging from 65% to 70% and retains beneficial fiber, unlike more refined isolates.

Its favorable protein digestibility corrected amino acid score (pdcaas) and controlled soy isoflavone content meet rising food and beverage industry demand. The functional properties, including water binding capacity and emulsification, make it a key meat analogue ingredient.

While addressing anti-nutritional factors in soy remains a focus, concentrates offer a cost-effective choice for functional food formulation and bakery product fortification.

The Concentrates segment was valued at USD 189.9 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Organic Soy Protein Market Demand is Rising in North America Request Free Sample

The geographic landscape is led by North America, accounting for approximately 38% of the market opportunity, driven by demand for products highlighting soy protein fortification benefits.

Europe follows at 25%, with a mature industry focused on sustainable soy sourcing for dairy alternative protein. APAC contributes over 23%, showing rapid growth in infant formula soy protein.

Across regions, the focus is on maximizing soy protein nutritional value in functional food formulation. Processors are adopting advanced membrane filtration technology, which increases protein purity by up to 5%, to produce neutral-flavored soy protein ideal for sports nutrition.

This focus on quality and operational efficiency, including bakery product fortification, is essential for meeting diverse regional demands.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the food industry increasingly revolve around ingredient selection, with a focus on plant-based options. The application of organic soy protein in functional foods is expanding, driven by growing awareness of soy protein's role in heart health. For manufacturers, improving texture with textured soy protein is key for success in the competitive market for meat alternatives.

- Similarly, the use of organic soy flour in bakery products offers a way to enhance nutritional profiles. A critical consideration is the specific protein type; organic soy isolates for infant nutrition must meet the highest purity standards, whereas the benefits of soy protein concentrate, such as its excellent water binding capacity of concentrates, make it ideal for other applications.

- Companies are conducting detailed cost analysis of soy protein types to optimize formulations. For brands targeting consumers on high-protein diets, using non-gmo soy protein for beverages requires advanced flavor masking techniques for soy protein to ensure palatability. Supply chain management is crucial, involving clean-label organic soy protein sourcing and a commitment to the sustainable farming of organic soybeans.

- Furthermore, the debate of organic soy protein versus pea protein continues, pushing formulators to master the best practices for soy protein formulation. A key operational focus is managing allergens in soy ingredients, with stringent protocols reducing cross-contamination incidents by over 95% compared to standard procedures.

- This diligence is vital as soy protein in dairy-free products and organic soy protein for clinical nutrition become more mainstream.

What are the key market drivers leading to the rise in the adoption of Organic Soy Protein Industry?

- The primary market driver is the convergence of consumer demand for health, sustainability, and clean-label products.

- The primary driver is the growing consumer alignment with health, wellness, and sustainability, which elevates demand for sustainable plant protein ingredients.

- The market for organic soy for infant nutrition and other sensitive applications is expanding, pushing for the development of hypoallergenic soy protein.

- The complete amino acid profile of soy protein concentrates, derived from defatted soy flour, makes it a favored ingredient. Innovations in the aqueous extraction process and membrane filtration technology have improved protein yields by up to 8%, reducing waste.

- This aligns with the demand for clean-label plant protein options, particularly in applications like organic soy protein for beverages.

- The superior water binding capacity of these proteins is essential for texture in soy protein in meat alternatives, directly contributing to consumer acceptance.

What are the market trends shaping the Organic Soy Protein Industry?

- A key market trend is the focus on technological innovations designed to enhance ingredient functionality, purity, and sustainability. This creates a new generation of high-performance organic soy proteins.

- A defining market trend is the intense focus on technological innovation to enhance soy protein functionality. As the demand for organic soy protein for vegan diets grows, advancements in the soy protein manufacturing process are critical. Processors are refining methods to create superior soy protein isolates and textured soy protein from certified organic soybeans.

- This results in clean-label soy ingredients with improved emulsification properties, enabling formulators to create better plant-based products. For example, new techniques have improved protein solubility by 15%, expanding applications. The debate over organic soy protein isolates vs concentrates informs product development, as manufacturers seek the optimal balance of purity and cost.

- These innovations in the functional properties of soy protein have directly led to a 20% reduction in the use of synthetic binders in certain food systems.

What challenges does the Organic Soy Protein Industry face during its growth?

- The inherent fragility and complexity of the organic soybean supply chain presents a key challenge to market growth and stability.

- A significant market challenge is the complexity of soy protein supply chain management, particularly concerning sustainable soy sourcing. Maintaining a robust identity preservation system is paramount for ensuring traceability in the soy supply chain, a non-negotiable for organic certification. This complexity contributes to organic soy protein price trends, which can be volatile.

- For manufacturers, ensuring proper allergen labeling for soy products is a critical compliance hurdle, driving investment in producing allergen-free soy protein where feasible. On the product development side, improving soy protein taste and optimizing gelation characteristics remain key R&D goals, especially for soy protein in bakery applications.

- Advanced processes like enzymatic hydrolysis of soy can improve digestibility but add costs, with an estimated 10% increase in processing expenses for certain applications.

Exclusive Technavio Analysis on Customer Landscape

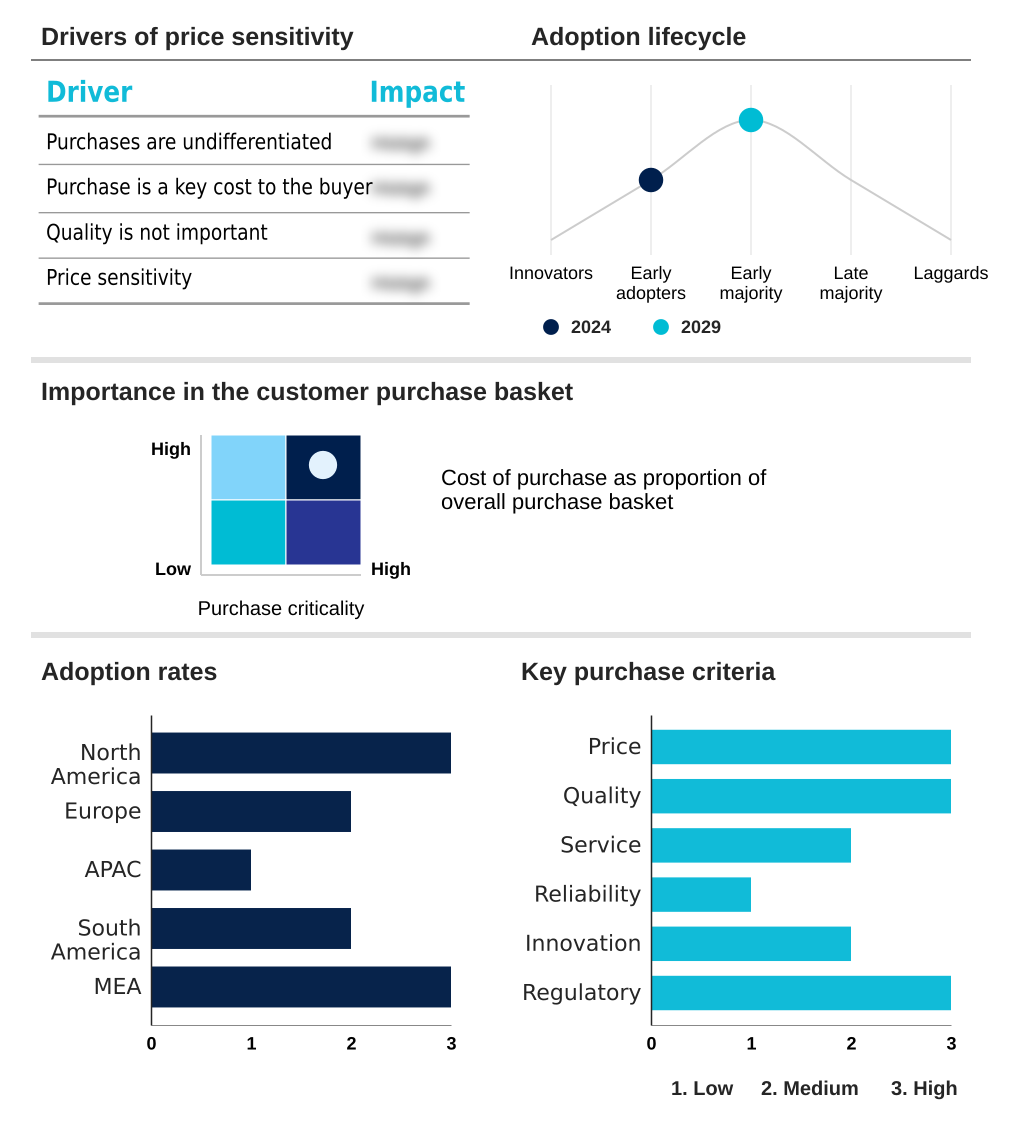

The organic soy protein market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic soy protein market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Organic Soy Protein Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, organic soy protein market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - Key offerings include organic soy protein isolates and concentrates engineered for human and animal nutrition, emphasizing functional performance and clean-label appeal in food systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Cargill Inc.

- CHS Inc.

- Eurosoy GmbH

- Farbest Brands

- Foodchem International Corp.

- Grain Millers Inc.

- Guanxian Xinrui Industrial

- Guzen Development

- Louis Dreyfus Co. BV

- Puris

- Shandong Yuxin Biotechnology

- Shiv Health Foods LLP

- Sonic Biochem Extraction

- SunOpta Inc.

- Taj Agro International

- The Scoular Co.

- Van Wankum Ingredients BV

- Wilmar International Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic soy protein market

- In September, 2024, Archer Daniels Midland Co. announced the expansion of its soy protein production facility in Decatur, Illinois, to increase its capacity for organic soy protein concentrates and isolates by 30%, citing rising demand from the meat alternatives and nutritional beverage sectors (Source: ADM Press Release).

- In November, 2024, Puris launched its new line of clean-taste organic soy protein isolates, Puris IP-90, developed using a proprietary membrane filtration technology to minimize off-flavors and improve solubility for beverage applications (Source: Puris Website News).

- In January, 2025, Cargill Inc. completed the acquisition of a European-based organic soybean processing plant to strengthen its supply chain for organic soy ingredients in the region and better serve its food manufacturing clients (Source: Bloomberg).

- In April, 2025, SunOpta Inc. entered a strategic partnership with a leading plant-based food brand to become the exclusive supplier of organic soy protein for their next generation of dairy-free yogurt and cheese products (Source: Reuters).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Soy Protein Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.9% |

| Market growth 2025-2029 | USD 392.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 12.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, South Africa, Saudi Arabia, UAE, Egypt and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is centered on enhancing soy protein functionality for a range of applications, from infant formula soy protein to bakery product fortification. Advances in the aqueous extraction process and membrane filtration technology are yielding higher purity soy protein isolates and soy protein concentrates.

- This push for technological superiority directly impacts boardroom strategy, as investment in R&D for hypoallergenic soy protein or enzymatic hydrolysis of soy becomes a key differentiator. For instance, companies that perfected soy protein texturization for meat analogue ingredient applications have seen a 20% faster adoption rate by major food brands.

- The entire value chain, from sustainable soy sourcing and organic farming practices to the final spray drying process for soy protein, is under scrutiny. Board-level decisions now hinge on managing the identity preservation system and ensuring complete traceability in the soy supply chain to validate non-gmo soy protein claims and manage soy isoflavone content.

- This focus extends to addressing anti-nutritional factors in soy and investing in soy protein flavor masking, which is critical for formulating palatable dairy alternative protein products and options for soy protein for sports nutrition.

- The ultimate goal is to deliver a clean-label soy ingredient with a complete amino acid profile and a high protein digestibility corrected amino acid score (pdcaas), balancing soy protein nutritional value with superior water binding capacity, emulsification properties, and gelation characteristics in functional food formulation.

What are the Key Data Covered in this Organic Soy Protein Market Research and Growth Report?

-

What is the expected growth of the Organic Soy Protein Market between 2025 and 2029?

-

USD 392.5 million, at a CAGR of 14.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Concentrates, Isolates, and Flour), Application (Functional foods, Meat alternatives, Bakery and confectionery, Infant formula, and Others), Product Type (Dry, and Liquid) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Convergence of health, sustainability, and clean-label consumerism, Inherent fragility and complexity of supply chain

-

-

Who are the major players in the Organic Soy Protein Market?

-

Archer Daniels Midland Co., Cargill Inc., CHS Inc., Eurosoy GmbH, Farbest Brands, Foodchem International Corp., Grain Millers Inc., Guanxian Xinrui Industrial, Guzen Development, Louis Dreyfus Co. BV, Puris, Shandong Yuxin Biotechnology, Shiv Health Foods LLP, Sonic Biochem Extraction, SunOpta Inc., Taj Agro International, The Scoular Co., Van Wankum Ingredients BV and Wilmar International Ltd.

-

Market Research Insights

- The market's dynamism is driven by evolving food and beverage industry demand for high-quality, sustainable plant protein ingredients. As consumer preferences shift, the focus on the health benefits of organic soy intensifies, particularly its role in cholesterol reduction.

- Innovations in the soy protein manufacturing process have led to significant functional improvements; for example, advancements in extraction technology have enhanced soy protein isolates' solubility by up to 25%, making them ideal for beverages. Furthermore, new flavor-masking techniques for improving soy protein taste have reduced the need for secondary additives in formulations by 15%, aligning with clean-label plant protein options.

- This progress is crucial as organic soy protein for functional foods and meat alternatives requires superior sensory profiles. Managing the soy protein supply chain remains a key operational focus, with robust protocols cutting spoilage rates by over 10% and ensuring consistent quality.

We can help! Our analysts can customize this organic soy protein market research report to meet your requirements.