Pectin Market Size 2025-2029

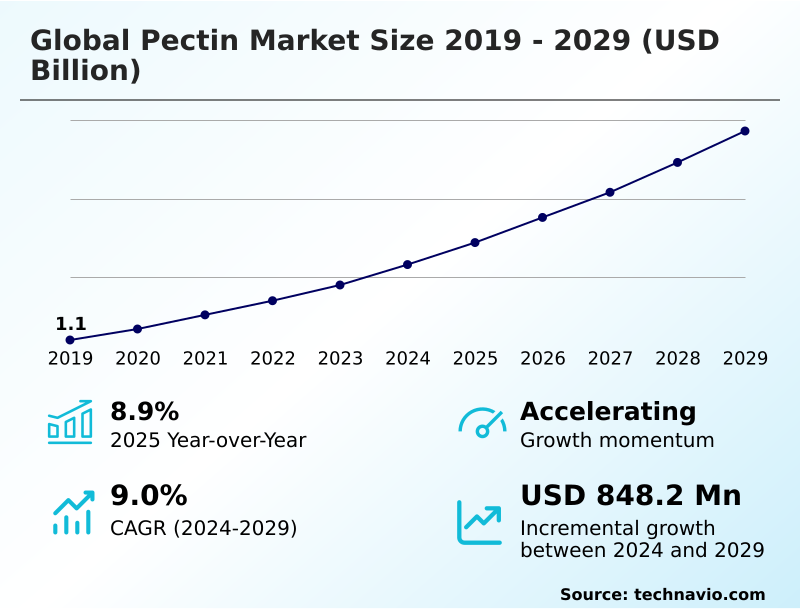

The pectin market size is valued to increase by USD 848.2 million, at a CAGR of 9% from 2024 to 2029. Increasing demand for natural and plant-based ingredients will drive the pectin market.

Major Market Trends & Insights

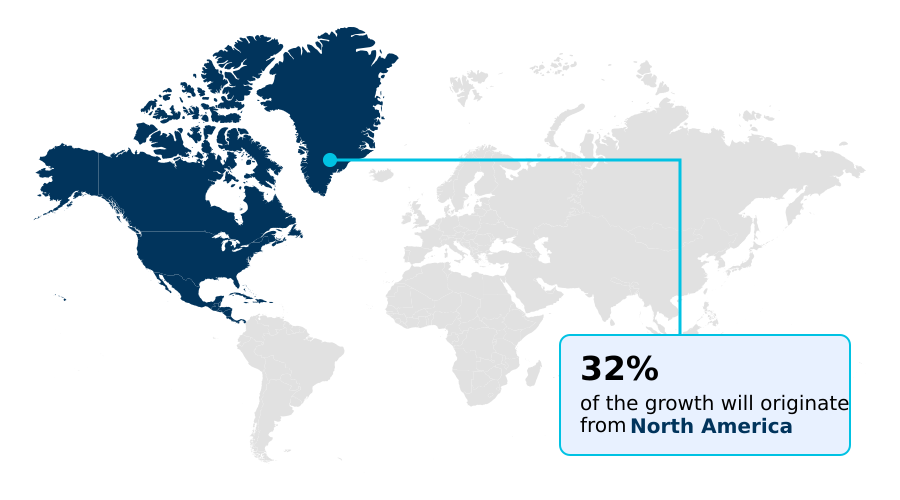

- North America dominated the market and accounted for a 32.3% growth during the forecast period.

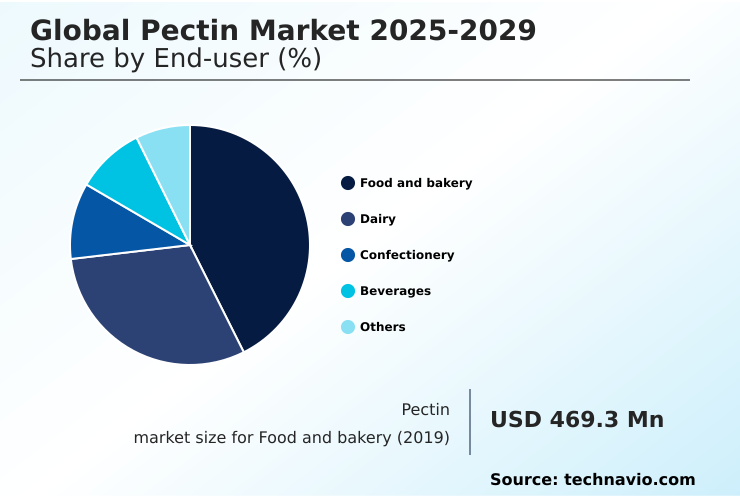

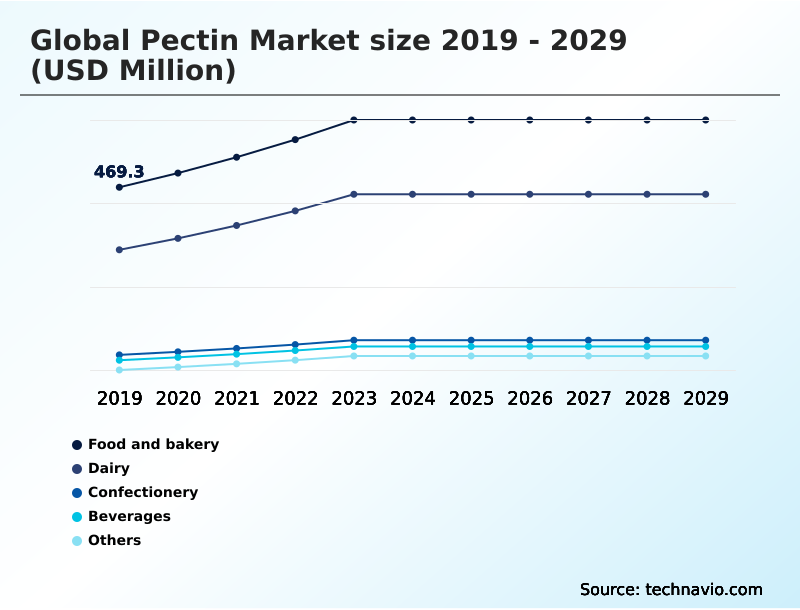

- By End-user - Food and bakery segment was valued at USD 612.2 million in 2023

- By Application - Gelling agent segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.33 billion

- Market Future Opportunities: USD 848.2 million

- CAGR from 2024 to 2029 : 9%

Market Summary

- The pectin market is defined by its integral role in the food, beverage, and pharmaceutical sectors as a functional polysaccharide. Growth is propelled by consumer demand for clean label ingredients and the expansion of plant-based and functional foods. Pectin's utility as a gelling agent, stabilizer, and thickener is indispensable.

- However, the industry grapples with challenges related to raw material price volatility and supply chain inconsistencies, which can impact production costs. For instance, a beverage manufacturer seeking to launch a new low-sugar fruit drink relies on a specific low methoxyl pectin for pulp suspension and mouthfeel.

- An unexpected shortage in apple pomace, a primary raw material, can force a costly and time-consuming reformulation with an alternative hydrocolloid, potentially delaying market entry. This scenario highlights the critical need for robust sourcing strategies and innovation in pectin extraction from diverse botanical sources to ensure market stability and support continuous product development.

- The focus remains on enhancing hydrocolloid functionality to meet evolving consumer preferences for natural and healthier products.

What will be the Size of the Pectin Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Pectin Market Segmented?

The pectin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Food and bakery

- Dairy

- Confectionery

- Beverages

- Others

- Application

- Gelling agent

- Thickener

- Stabilizer

- Fat replacer

- Others

- Source

- Citrus peel

- Apple pomace

- Others

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- Europe

By End-user Insights

The food and bakery segment is estimated to witness significant growth during the forecast period.

The food and bakery segment leverages pectin as a critical food processing aid for texture modification and stability. As a versatile natural food hydrocolloid and texturizer for baked goods, this plant-derived gelling agent is indispensable in fruit preparations.

It acts as a primary thickening agent and fat replacer in low-fat products, improving moisture retention by up to 15%. The rheological properties are fine-tuned for specific outcomes, from creating firm gels to creamy fillings.

Industry focus on citrus peel valorization supports sustainable supply. Furthermore, its use as a pharmaceutical excipient informs its high-quality standards, while hydrocolloid synergy with other ingredients is explored for advanced formulations.

It is also used as a gelling agent for yogurts.

The Food and bakery segment was valued at USD 612.2 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pectin Market Demand is Rising in North America Request Free Sample

The geographic landscape is shaped by regional consumption patterns and processing capabilities.

North America leads in innovation, especially for pectin for dairy alternatives, while APAC is the fastest-growing region, with its market expanding at a rate over 1.5% higher than Europe.

In Europe, a focus on tradition and quality drives demand for citrus pectin in classic acid sugar gel jams. Its role as a dietary fiber and functional food ingredient is gaining traction globally.

As a fruit-based stabilizer and emulsion stabilizer, it is crucial for mouthfeel enhancement and beverage pulp suspension in drinks. Advanced applications include its use in biodegradable films and as an excipient for drug delivery, forming a stable calcium pectinate gel.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic formulation in the food and beverage industry increasingly hinges on understanding the nuances of pectin. The debate over citrus pectin versus apple pectin functionality is central to product development, as each offers unique textural properties. For instance, using pectin for low sugar jam production often requires low methoxyl variants to achieve the desired gel without high solids content.

- In bakery, using pectin as a fat replacer in bakery items can improve moisture retention and shelf life. The economic impact of pectin price volatility forces manufacturers to evaluate the cost of pectin versus other hydrocolloids, making efficient raw material sourcing a priority.

- For a stabilizer for plant-based yogurt formulation, the goal is achieving creaminess and preventing whey separation, a challenge addressed by controlling syneresis with amidated pectin. In beverages, using pectin for beverage mouthfeel enhancement and for protein stabilization in drinks are key objectives. Advancements in pectin extraction technology are crucial, as are adherence to regulatory standards for food grade pectin.

- In confectionery, achieving the perfect texture in vegan gummies with pectin depends on selecting the right high methoxyl pectin for confectionery. For functional applications, the role of pectin in edible food coatings and in pharmaceutical drug delivery systems highlights its versatility, where optimizing pectin gel strength in preserves can reduce additive usage by 10% compared to standard formulations.

- The gelling properties of modified pectin continue to open new application horizons.

What are the key market drivers leading to the rise in the adoption of Pectin Industry?

- The growing demand for natural, recognizable, and plant-based ingredients is the key driver fueling expansion in the pectin market.

- Demand for natural products drives the market, with pectin’s status as a clean label ingredient and sustainable food additive being paramount. The pectin extraction process is continuously optimized to yield specific functionalities.

- Its polysaccharide structure allows for viscosity control, making it an effective thickener for sauces and a key ingredient in low-sugar jam formulation.

- As a food additive, its functionality is determined by the degree of esterification, enabling its use as a fat mimetic in foods.

- Modified pectin is developed for specialized roles, such as creating a controlled-release matrix in functional foods or providing texture in pectin for dairy alternatives, where it can reduce reliance on other stabilizers by up to 30%.

What are the market trends shaping the Pectin Industry?

- The increasing consumer shift toward plant-based food and beverage products represents a significant market trend. This movement is a primary factor driving demand for versatile, plant-derived ingredients.

- The rise of plant-based diets is a primary trend, positioning pectin as a leading plant-based texturizer and vegan gelatin alternative. Its role as a stabilizing agent is crucial for stabilizer for plant milks, where it can improve suspension and prevent separation, extending product appeal by over 25%. The specific gelling mechanism of high methoxyl pectin is leveraged in confectionery.

- Beyond food, nutraceutical applications are expanding, using pectin as a prebiotic dietary fiber. Innovations in encapsulation technology use pectin for protecting active ingredients. Advanced food texture analysis validates its performance, while its use in edible coating for produce acts as a shelf-life extension additive and supports juice clarification.

What challenges does the Pectin Industry face during its growth?

- Volatility in the availability and pricing of raw materials, such as citrus peels and apple pomace, presents a significant challenge to market growth and stability.

- Navigating raw material sourcing and price volatility remains a key challenge, making efficient apple pomace utilization crucial. The hydrocolloid functionality of apple pectin faces competition, necessitating innovation in hydrocolloid blend optimization to highlight its superior gelling properties of polysaccharides. Ensuring consistent pectin quality control is vital. In applications like dairy, syneresis control and protein stabilization are critical performance metrics.

- Formulators use low methoxyl pectin and amidated pectin to create robust gels in low-sugar environments. This is essential for the confectionery gelling system, where texture is paramount. Pectin's role also extends to hydrocolloid for cosmetics, where purity and performance must be flawless, with batch testing reducing formulation failures by 15%.

Exclusive Technavio Analysis on Customer Landscape

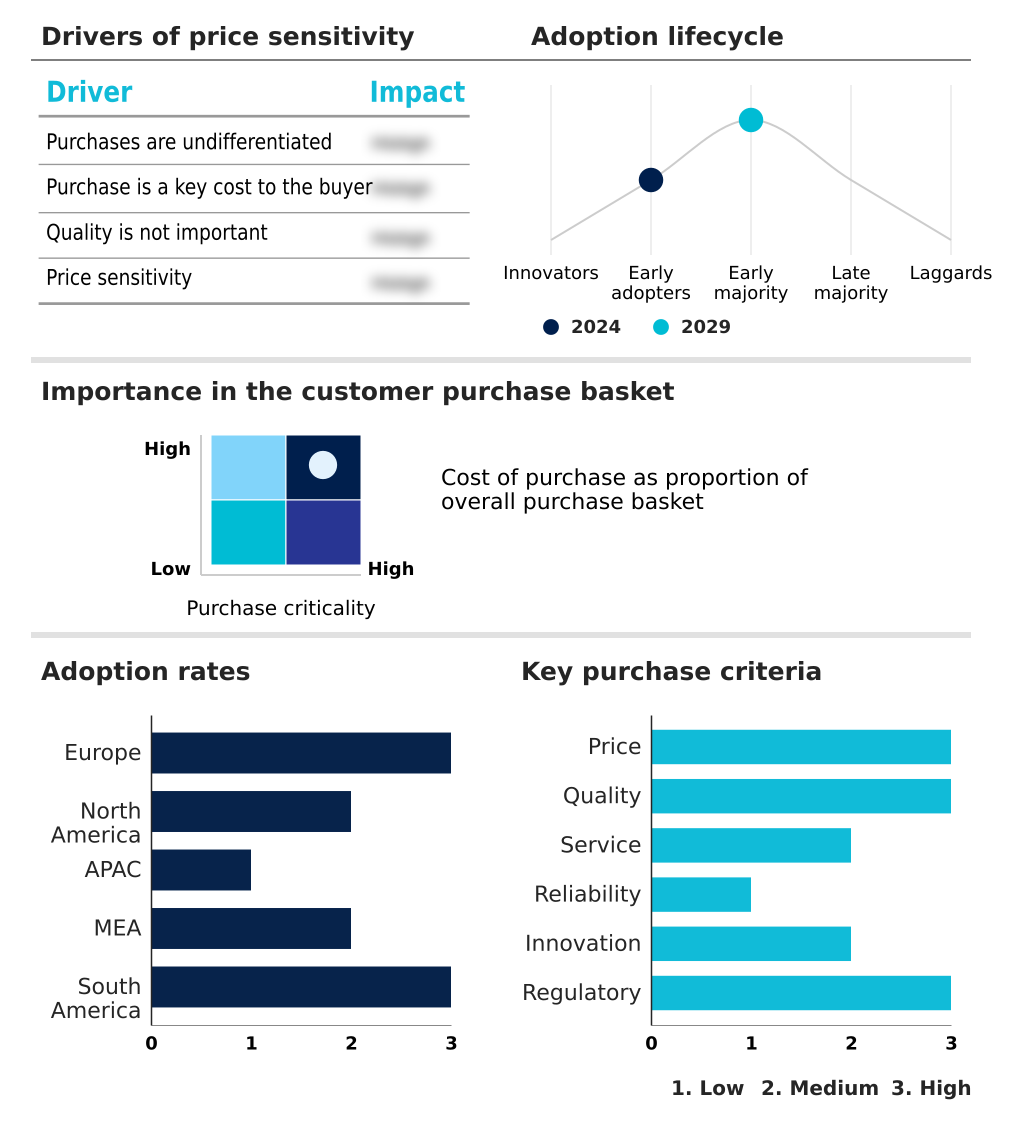

The pectin market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pectin market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pectin Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pectin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agar Corp. - Specialized citrus and apple pectins provide tailored gelling, thickening, and stabilizing solutions for diverse food, beverage, and pharmaceutical applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agar Corp.

- Al Sedanah Jordan LLC

- Cargill Inc.

- Compania Espanola S.A.

- Condio GmbH

- Devson Impex Pvt. Ltd.

- DSM Firmenich AG

- DuPont de Nemours Inc.

- Herbstreith and Fox GmbH

- Ingredion Inc.

- J. Rettenmaier and Sohne

- Jinfeng Technology Co. Ltd.

- Krishna Pectins Pvt. Ltd.

- Maspex

- Polygal Inc.

- Silvateam Spa

- Tate and Lyle PLC

- The Kraft Heinz Co

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pectin market

- In September 2024, IFF showcased its expanded portfolio of plant-based solutions, emphasizing how natural hydrocolloids like pectin are crucial for developing innovative, clean label products for the food and beverage industry.

- In November 2024, Ingredion highlighted its ingredient solutions, including pectin, tailored for the convenience food sector, demonstrating how these ingredients enable manufacturers to create stable and appealing ready-to-eat products.

- In January 2025, CP Kelco reaffirmed its commitment to process innovation and research for hydrocolloids, including pectin, to develop advanced solutions that meet the evolving demands of the food and beverage industry.

- In March 2025, Tate and Lyle PLC presented its solutions for sugar reduction and texture optimization in confectionery, which frequently involve natural hydrocolloids like pectin to meet contemporary consumer demands for healthier sweet treats.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pectin Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9% |

| Market growth 2025-2029 | USD 848.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 8.9% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, South Africa, UAE, Saudi Arabia, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pectin market's evolution is driven by its essential hydrocolloid functionality as a natural food additive. The inherent polysaccharide structure, defined by its degree of esterification, dictates its performance as a gelling agent, thickening agent, and stabilizing agent.

- Boardroom decisions are increasingly influenced by the clean label movement, pushing for reformulation with pectin as a plant-based texturizer and fat replacer, where it facilitates texture modification and mouthfeel enhancement. Companies leverage specific types like high methoxyl pectin for acid sugar gel formations and low methoxyl pectin or amidated pectin for calcium pectinate gel systems, crucial for syneresis control.

- The choice between citrus pectin and apple pectin depends on raw material sourcing and desired rheological properties. This focus has led to innovations in modified pectin for specialized nutraceutical applications, such as encapsulation technology for a controlled-release matrix, with firms reporting a 10% improvement in active ingredient stability.

- Its role extends to juice clarification, protein stabilization, and as a pharmaceutical excipient, with ongoing research into biodegradable films for sustainable packaging, all while managing viscosity control.

What are the Key Data Covered in this Pectin Market Research and Growth Report?

-

What is the expected growth of the Pectin Market between 2025 and 2029?

-

USD 848.2 million, at a CAGR of 9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Food and bakery, Dairy, Confectionery, Beverages, and Others), Application (Gelling agent, Thickener, Stabilizer, Fat replacer, and Others), Source (Citrus peel, Apple pomace, and Others) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for natural and plant-based ingredients, Raw material availability and price volatility

-

-

Who are the major players in the Pectin Market?

-

Agar Corp., Al Sedanah Jordan LLC, Cargill Inc., Compania Espanola S.A., Condio GmbH, Devson Impex Pvt. Ltd., DSM Firmenich AG, DuPont de Nemours Inc., Herbstreith and Fox GmbH, Ingredion Inc., J. Rettenmaier and Sohne, Jinfeng Technology Co. Ltd., Krishna Pectins Pvt. Ltd., Maspex, Polygal Inc., Silvateam Spa, Tate and Lyle PLC and The Kraft Heinz Co

-

Market Research Insights

- The pectin market's dynamics are heavily influenced by its role as a versatile texturizer and stabilizer. The adoption of pectin as a vegan gelatin alternative has accelerated, with product reformulations leading to a 20% increase in development cycles for some confectionery manufacturers.

- In beverages, its function in beverage pulp suspension helps maintain product homogeneity, improving consumer satisfaction scores by over 15%. The application of pectin for dairy alternatives is also expanding as formulators seek a clean label texturizer to mimic traditional mouthfeel.

- These shifts underscore the ingredient's critical role in meeting consumer demands for plant-based, natural, and functional products while providing tangible improvements in product quality and stability.

We can help! Our analysts can customize this pectin market research report to meet your requirements.