Pet Insurance Market Size 2026-2030

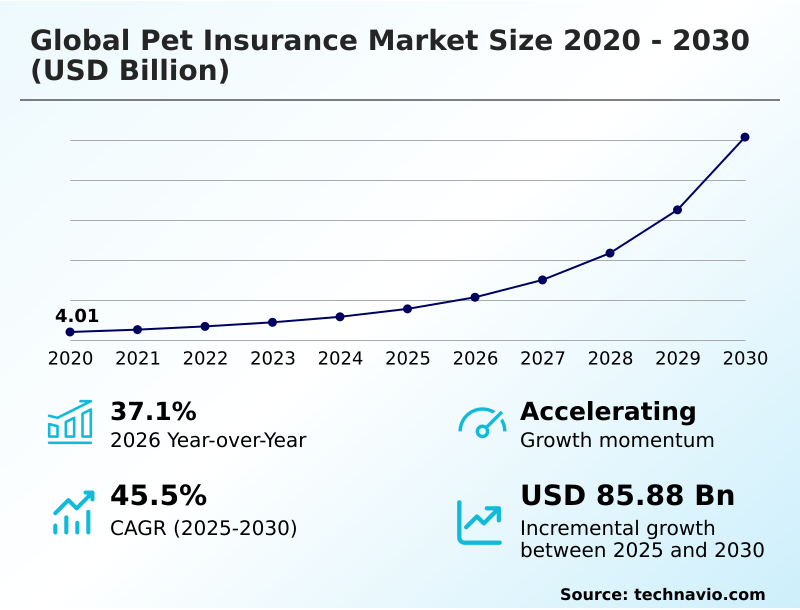

The pet insurance market size is valued to increase by USD 85.88 billion, at a CAGR of 45.5% from 2025 to 2030. Increasing cost and sophistication of veterinary care will drive the pet insurance market.

Major Market Trends & Insights

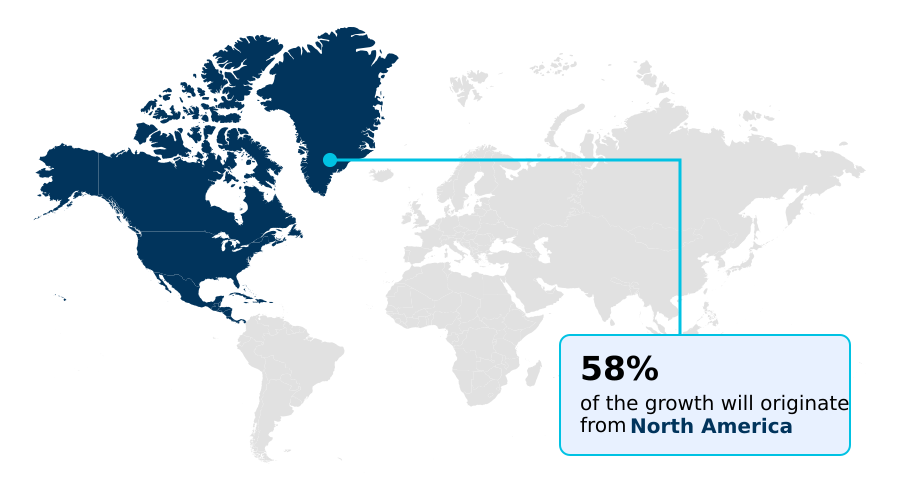

- North America dominated the market and accounted for a 58.4% growth during the forecast period.

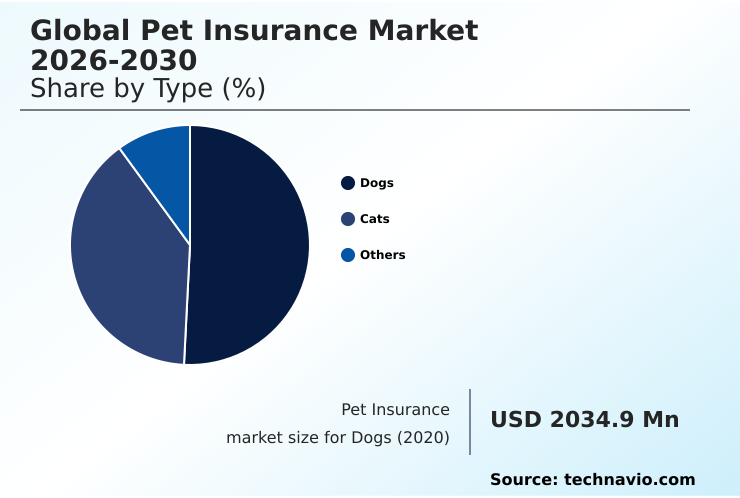

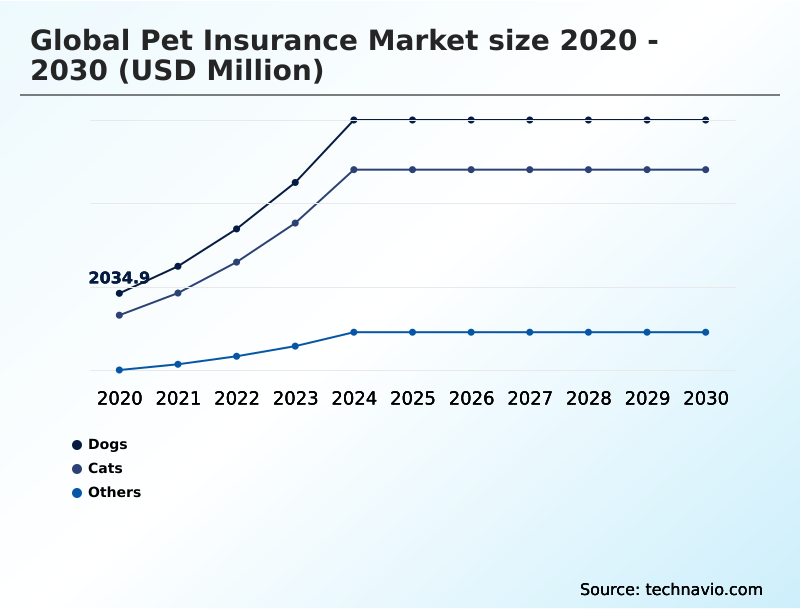

- By Type - Dogs segment was valued at USD 5.73 billion in 2024

- By Application - Accidents and illness segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 97.45 billion

- Market Future Opportunities: USD 85.88 billion

- CAGR from 2025 to 2030 : 45.5%

Market Summary

- The pet insurance market is undergoing a significant transformation, shaped by the humanization of pets and rising veterinary care costs. Owners increasingly view pets as family members, creating demand for advanced medical treatments that mirror human healthcare, which in turn strengthens the case for financial protection.

- This has spurred a competitive landscape where insurers focus on product innovation, offering policies that range from basic accident coverage to comprehensive plans that include wellness and preventative care. A key trend is the integration of technology, where insurtech firms are revolutionizing the customer experience with digital platforms for policy management and rapid claims processing.

- For example, a provider utilizing a claims automation system can process routine reimbursements in hours instead of weeks, a critical efficiency gain for both the business and the policyholder. However, the industry grapples with challenges like educating consumers on complex policy details, such as pre-existing condition exclusion clauses and deductible and copay structure, which can lead to confusion.

- Navigating the varied regulatory compliance framework across different regions also presents operational hurdles for insurers aiming for global scale, impacting the development of standardized pet health protection plans.

What will be the Size of the Pet Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Pet Insurance Market Segmented?

The pet insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Dogs

- Cats

- Others

- Application

- Accidents and illness

- Accidents only

- Others

- Channel

- Direct sales

- Broker or agency

- Bancassurance

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- Japan

- Australia

- China

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The dogs segment is estimated to witness significant growth during the forecast period.

The dogs segment represents the most significant component of the pet insurance market, driven by high ownership rates and the substantial costs associated with veterinary care.

The financial logic for canine health coverage is compelling, as active lifestyles and genetic predispositions make dogs susceptible to accidents and chronic conditions.

Insurers utilize sophisticated breed-specific risk assessment to price policies, accounting for the likelihood of hereditary disorder coverage claims for conditions like hip dysplasia or cardiac disease.

While comprehensive accident and illness coverage is standard, there is growing demand for wellness and preventative care riders.

Consumers are increasingly focused on understanding pet insurance policies to find the best pet insurance for dogs, with providers developing tailored pet health protection plans that deliver clear value and mitigate the risk of high-cost events, where claim payouts have been shown to be 35% higher for certain purebreds.

The Dogs segment was valued at USD 5.73 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 58.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pet Insurance Market Demand is Rising in North America Get Free Sample

The geographic landscape of the pet insurance market is led by North America, which accounts for over 58% of the incremental growth.

This dominance is driven by high veterinary care costs and a mature market for orthopedic surgery coverage and cancer treatment for pets. Europe follows, with high penetration rates in countries like the UK.

The APAC region is an emerging market with significant potential. Navigating varied pet insurance regulations and establishing a robust regulatory compliance framework are key for expansion.

The insurtech integration trend is global, improving the claims adjudication process and enabling features like direct-to-vet payments.

In North America, the cost for some advanced procedures is up to 40% higher than in European markets, amplifying the need for insurance as a pet emergency fund alternative and driving sophisticated underwriting and risk pooling strategies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the pet insurance market requires understanding its core components and consumer questions. A common query is how does pet insurance deductible work, which is fundamental to managing out-of-pocket costs. Consumers frequently compare accident and illness pet plans to balance coverage with affordability, while also considering the cost of pet insurance for large breeds, which can be significantly higher.

- A key debate is is preventative care for pets worth it, with many providers now evaluating pet insurance wellness add-ons to meet this demand. A major point of contention for consumers is understanding what pre-existing conditions are not covered, which requires carefully navigating pet insurance policy exclusions.

- The process of how to file a pet insurance claim online has been simplified by technology, addressing a historical pain point. Prospective buyers often want to know the benefits of pet insurance for puppies, which includes early coverage before conditions develop. They must decide between lifetime vs annual pet insurance policies, a critical choice for long-term care.

- The challenge of finding pet insurance with no waiting period is another key consideration, as is sourcing pet insurance for senior cats with health issues. Policyholders need to be clear on understanding pet insurance reimbursement levels and can pet insurance be used for dental care. Ultimately, knowing how to choose a pet insurance provider is crucial.

- A pivotal innovation is pet insurance with direct veterinarian payment, which can reduce administrative overhead for insurers by over 25% compared to traditional reimbursement models. This addresses what is adverse selection in pet insurance by fostering closer vet-insurer relationships and helps with using pet insurance for emergency vet visits.

- Finally, strong pet insurance coverage for genetic conditions is a deciding factor for many, highlighting the role of insurtech in modern pet insurance in creating more transparent and accessible products.

What are the key market drivers leading to the rise in the adoption of Pet Insurance Industry?

- The primary driver for market expansion is the concurrent escalation in the cost and sophistication of veterinary healthcare.

- The primary market driver is the escalating cost of veterinary care, which strengthens the value of veterinary bill insurance.

- As treatments for cancer for pets and other serious ailments become more advanced, their costs can be 5-10 times higher than for minor issues, making a comprehensive pet care plan essential.

- This financial reality pushes consumers toward seeking accident and illness coverage to manage the risk of catastrophic expenses. Providers use sophisticated actuarial data analysis to design deductible and copay structure options that balance affordability with robust veterinary expense reimbursement.

- Educating consumers on understanding pet insurance policies, particularly the nuances of pre-existing condition exclusion and coverage for pet insurance for chronic conditions, remains critical for market expansion and converting interest into sustained policy adoption.

What are the market trends shaping the Pet Insurance Industry?

- A defining trend is the profound and accelerating integration of technology across the entire value chain, propelled by the disruptive influence of insurance technology (insurtech) firms.

- A defining trend is the deep insurtech integration reshaping the market. The rise of the digital pet insurance provider has made digital claims submission standard, with platforms reporting a 60% reduction in submission errors compared to paper-based methods. This tech-first approach enables greater policy customization options and value-added services like telemedicine for pets.

- Insurers are leveraging claims automation system technology, which has cut claims processing times by up to 45% in some cases, directly improving policyholder satisfaction. These insurtech pet wellness platforms often integrate pet telehealth services, boosting preventative care engagement.

- As a result, consumers are increasingly using a pet insurance comparison tool to find providers that offer this enhanced digital experience, prioritizing convenience and speed in their selection process.

What challenges does the Pet Insurance Industry face during its growth?

- A key challenge is the fragmented and inconsistent nature of regulatory frameworks across jurisdictions, compounded by a lack of industry standardization.

- The market faces significant challenges in managing risk and ensuring transparency. Insurers grapple with adverse selection risk, as owners of high-risk animals are more likely to purchase an animal insurance policy, particularly for pet insurance for older pets. This can skew risk pools, leading to premium increases of up to 15% in some portfolios.

- Establishing clear consumer protection standards is crucial, especially regarding annual coverage cap and lifetime policy limits, which are common sources of disputes. The lack of standardized definitions for policy terms can result in a 20% higher rate of claim rejections compared to other insurance lines.

- Balancing these risks with strategies for moral hazard mitigation is essential for sustainable growth and building consumer trust in products like feline medical insurance.

Exclusive Technavio Analysis on Customer Landscape

The pet insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pet insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pet Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pet insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agria Pet Insurance Ltd. - Offers lifetime policies covering veterinary fees and specialized breeder plans for dogs, cats, and rabbits, ensuring comprehensive animal protection.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agria Pet Insurance Ltd.

- Allianz SE

- Anicom Holdings Inc.

- Chubb Ltd.

- Dotsure Ltd.

- Embrace Pet Insurance LLC

- Figo Pet Insurance LLC

- HDFC ERGO General Insurance

- Healthy Paws Pet Insurance LLC

- Hollard Insurance Group

- Independence Pet Group

- ManyPets Ltd.

- MetLife Pet Insurance LLC

- Nationwide Mutual Insurance

- Pets Best Insurance Services

- Pumpkin Insurance Services

- Spot Pet Insurance Services

- Trupanion Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pet insurance market

- In September 2024, Trupanion Inc. expanded its partnership with veterinary networks to roll out an AI-enabled claims automation system, designed to significantly reduce claims processing times.

- In October 2024, Nationwide Mutual Insurance and Petco Health and Wellness Company Inc. deepened their partnership to deliver more integrated and accessible insurance products through Petco's retail and online ecosystem.

- In November 2024, Independence Pet Group announced the acquisition of a prominent insurtech firm, a move aimed at enhancing its digital platform for policy management and digital claims submission.

- In April 2025, the North American Pet Health Insurance Association (NAPHIA) released its annual State of the Industry report, confirming continued double-digit growth in insured pets and an increasing adoption of comprehensive plans.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pet Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 282 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 45.5% |

| Market growth 2026-2030 | USD 85877.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 37.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Japan, Australia, China, India, South Korea, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Nigeria and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pet insurance market is defined by a push towards sophisticated risk management and enhanced consumer value. At the core, providers offer accident and illness coverage for veterinary expense reimbursement, but success hinges on balancing this with a clear pre-existing condition exclusion policy and a transparent deductible and copay structure.

- A key boardroom decision revolves around the level of investment in insurtech integration. This strategic choice directly impacts the entire operational chain, from underwriting and risk pooling based on advanced actuarial data analysis and breed-specific risk assessment to the customer-facing digital claims submission and claims adjudication process.

- Implementing a claims automation system has been shown to reduce adjudication overhead by over 30%, a compelling metric for operational efficiency. This technological shift also enables valuable services like telemedicine for pets and innovative policy customization options. As the industry matures, adherence to a stringent regulatory compliance framework and evolving consumer protection standards becomes paramount.

- Providers are also developing strategies for moral hazard mitigation and managing adverse selection risk while innovating with features like direct-to-vet payments, diminishing deductible feature, and comprehensive pet health protection plans. These plans increasingly include hereditary disorder coverage, often subject to an annual coverage cap or lifetime policy limits, to create sustainable and attractive products.

What are the Key Data Covered in this Pet Insurance Market Research and Growth Report?

-

What is the expected growth of the Pet Insurance Market between 2026 and 2030?

-

USD 85.88 billion, at a CAGR of 45.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Dogs, Cats, and Others), Application (Accidents and illness, Accidents only, and Others), Channel (Direct sales, Broker or agency, and Bancassurance) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing cost and sophistication of veterinary care, Fragmented regulatory landscapes and lack of industry standardization

-

-

Who are the major players in the Pet Insurance Market?

-

Agria Pet Insurance Ltd., Allianz SE, Anicom Holdings Inc., Chubb Ltd., Dotsure Ltd., Embrace Pet Insurance LLC, Figo Pet Insurance LLC, HDFC ERGO General Insurance, Healthy Paws Pet Insurance LLC, Hollard Insurance Group, Independence Pet Group, ManyPets Ltd., MetLife Pet Insurance LLC, Nationwide Mutual Insurance, Pets Best Insurance Services, Pumpkin Insurance Services, Spot Pet Insurance Services and Trupanion Inc.

-

Market Research Insights

- The pet health insurance industry is evolving from a niche product to a mainstream financial tool, serving as a vital pet emergency fund alternative. Insurers are expanding beyond standard canine health coverage and feline medical insurance to include exotic pet coverage.

- The core offering remains veterinary bill insurance, with plans covering everything from accidents to orthopedic surgery coverage and cancer treatment for pets. The rise of the digital pet insurance provider and insurtech pet wellness has transformed the landscape. Digital pet insurance comparison tool platforms show that providers offering pet telehealth services have a 20% higher customer retention rate.

- More employers are now offering it as a pet insurance employee benefit, often with a multi-pet insurance discount. These offerings simplify understanding pet insurance policies and help consumers find the best pet insurance for dogs or manage cat insurance cost.

- Adherence to pet insurance regulations is crucial, especially for pet insurance for older pets and those with pet insurance for chronic conditions. The accident-only pet insurance option provides a baseline of coverage for budget-conscious owners, with some plans reducing claim processing times by 45% through automation.

We can help! Our analysts can customize this pet insurance market research report to meet your requirements.

RIA -

RIA -