Pharmaceutical Packaging Market Size 2026-2030

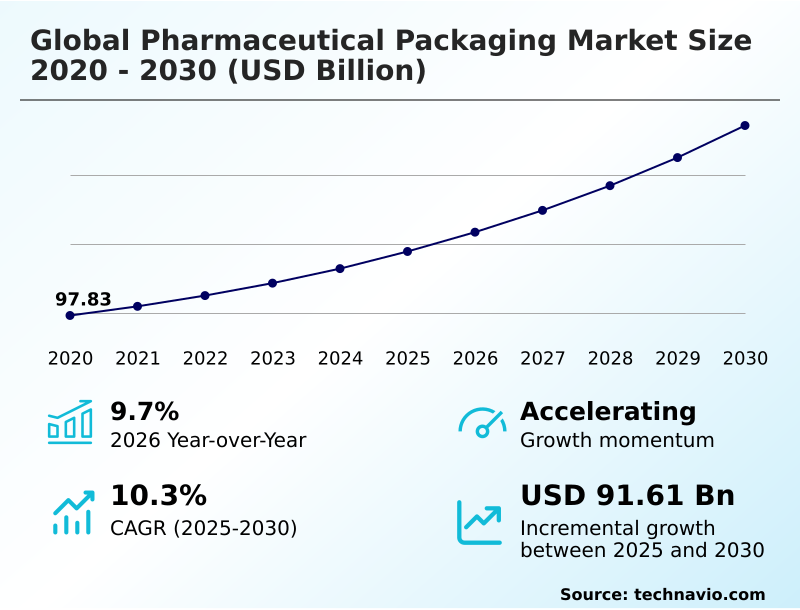

The pharmaceutical packaging market size is valued to increase by USD 91.61 billion, at a CAGR of 10.3% from 2025 to 2030. Rapid global expansion of complex biologics and injectable therapeutics will drive the pharmaceutical packaging market.

Major Market Trends & Insights

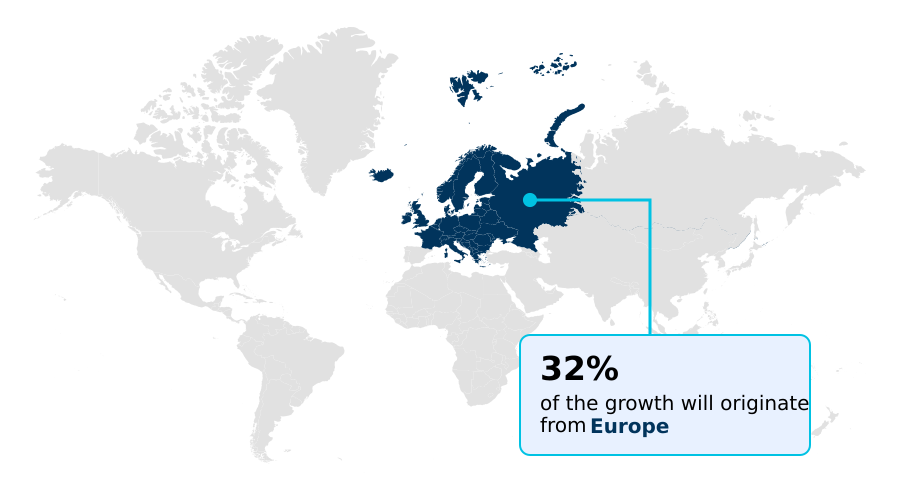

- Europe dominated the market and accounted for a 32.3% growth during the forecast period.

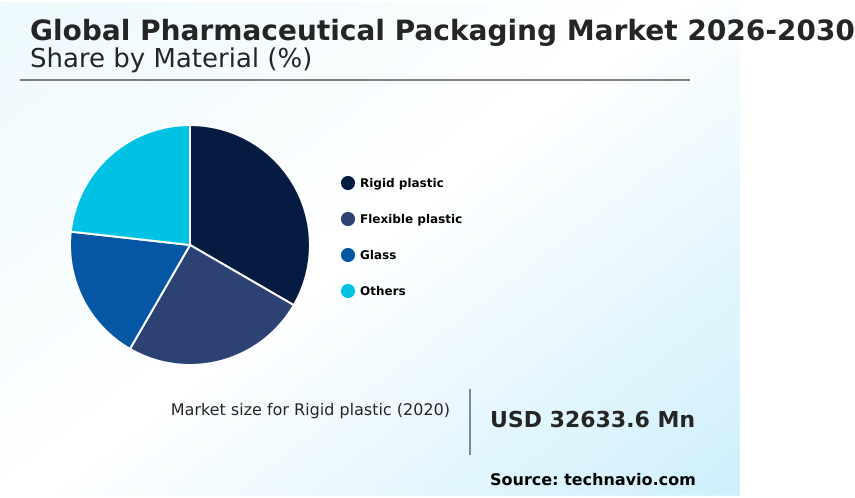

- By Material - Rigid plastic segment was valued at USD 39.66 billion in 2024

- By Product - Plastic bottles segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 138.16 billion

- Market Future Opportunities: USD 91.61 billion

- CAGR from 2025 to 2030 : 10.3%

Market Summary

- The Pharmaceutical Packaging exhibits profound structural intensification, propelled by the escalating complexity of advanced therapeutic formulations and strict regulatory compliance mandates. As modern drug development heavily prioritizes biologically sensitive large-molecule therapies, the necessity for premium parenteral containment systems has surged dramatically.

- This shift drives specialized contract manufacturing organizations to optimize supply chain resilience by integrating automated high-speed filling lines, which reduces operational processing time by 18% compared to legacy manual workflows. The expansion of complex biologics acts as a primary market driver, compelling packaging providers to engineer sophisticated prefillable delivery mechanisms that eliminate clinical reconstitution errors.

- Conversely, navigating the friction between absolute sterility requirements and zero-waste environmental objectives presents a severe operational challenge. Manufacturers face immense difficulty executing comprehensive extractables and leachables profiling when transitioning to recycled polymers, often delaying commercialization timelines. The continuous adoption of automated decentralized hospital dispensing further dictates strict adherence to standardized unit-dose formats, ensuring secure medication administration.

What will be the Size of the Pharmaceutical Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Pharmaceutical Packaging Market Segmented?

The pharmaceutical packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

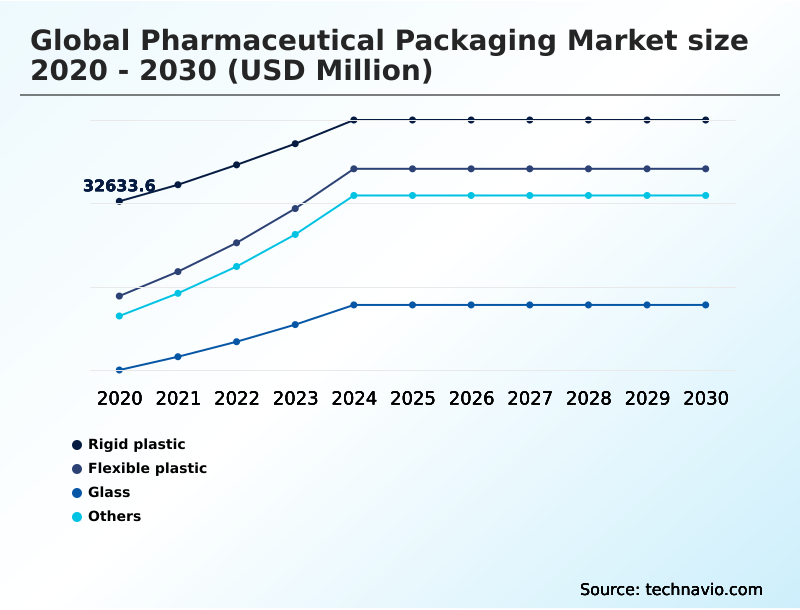

- Material

- Rigid plastic

- Flexible plastic

- Glass

- Others

- Product

- Plastic bottles

- Caps and closures

- Blister packs

- Pre-fillable syringes

- Others

- Route of administration

- Oral drugs

- Injectables

- Topical

- Nasal

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Switzerland

- APAC

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Middle East and Africa

- Saudi Arabia

- Turkey

- South Africa

- UAE

- Egypt

- South America

- Brazil

- Argentina

- Chile

- North America

By Material Insights

The rigid plastic segment is estimated to witness significant growth during the forecast period.

The rigid plastic segment within the Pharmaceutical Packaging framework serves as a foundational component for securing solid oral dosages and diagnostic materials.

Utilizing advanced cyclic olefin polymers and high-density polyethylene resins, manufacturers engineer highly durable tablet bottles and integrated device components. This structural integrity guarantees absolute primary containment protection against ambient moisture and physical impacts during transit.

As the industry transitions toward high-speed automated filling lines, rigid containers demonstrate exceptional dimensional uniformity, reducing production downtime by 15% compared to flexible alternatives.

Incorporating active oxygen scavengers directly into the plastic matrix extends shelf life and ensures biologic drug stability. Furthermore, precision-engineered child-resistant closures enhance patient safety while optimizing active pharmaceutical ingredient preservation.

This material transition allows pharmaceutical operators to achieve a 20% improvement in supply chain efficiency through reduced product loss and enhanced structural resilience.

The Rigid plastic segment was valued at USD 39.66 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pharmaceutical Packaging Market Demand is Rising in Europe Get Free Sample

Regional dynamics within the Pharmaceutical Packaging sector reveal sharp contrasts in regulatory maturity and supply chain execution between North America and APAC.

North America maintains strict serialization mandates, driving a 35% higher adoption rate of smart connected secondary cartons compared to developing Asian markets. This advanced infrastructure actively supports patient medication adherence and precise pharmaceutical compounding integration.

In contrast, APAC functions as the dominant manufacturing hub for generic oral solids, yet it is rapidly upgrading its capabilities to process advanced therapy medicinal products.

Facilities in Europe demonstrate superior operational efficiency, achieving a 20% reduction in packaging waste through early compliance with circular economy directives.

The demand for ultra-pure borosilicate glass vials and inert fluoropolymer coatings remains concentrated in Western markets, where stringent biological stability testing dictates primary container selection.

These distinct geographical priorities compel packaging manufacturers to customize localized facility investments, thereby optimizing distribution resilience and mitigating material shortage risks.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The ongoing structural transformation of the Pharmaceutical Packaging landscape heavily emphasizes absolute product integrity and operational optimization across highly regulated supply networks. As pharmaceutical laboratories shift their pipelines toward complex biologics and targeted therapies, the demand for highly specialized containment solutions has fundamentally altered procurement strategies.

- Companies are heavily investing in sterile injectable delivery systems that prevent chemical degradation and ensure safe subcutaneous administration. Simultaneously, legislative pressure to adopt sustainable practices has triggered a massive transition toward eco-friendly mono-material blister packaging, which allows manufacturers to achieve up to a 25% improvement in post-consumer recycling efficiency compared to legacy multi-layer PVC structures.

- This sustainability push is complemented by the integration of high-barrier active gas-scavenging polymers that continuously trap residual oxygen, dramatically extending the shelf life of highly sensitive therapeutic compounds. To maintain compliance with international traceability mandates, operators are deploying smart connected pharmaceutical secondary cartons equipped with digital identification markers.

- This technological upgrade secures the physical supply chain and facilitates direct communication regarding dosage instructions. Furthermore, managing the quality control of these complex formats requires flawless execution, leading facilities to implement automated machine vision inspection lines capable of detecting microscopic cosmetic anomalies at extreme line speeds.

- This comprehensive alignment of advanced materials, digital connectivity, and precision engineering guarantees that pharmaceutical packagers can securely deliver life-saving medications while adapting to evolving environmental and commercial requirements.

What are the key market drivers leading to the rise in the adoption of Pharmaceutical Packaging Industry?

- The rapid expansion of complex biologics and advanced injectable therapeutics serves as a primary driver, compelling the development of highly engineered containment systems to prevent chemical degradation.

- The unprecedented expansion of complex biologic pipelines and self-administered therapeutics functions as a formidable driver propelling Pharmaceutical Packaging innovations. This structural shift forces manufacturers to secure advanced cyclic olefin copolymers to prevent harmful chemical interactions with volatile liquid formulations.

- The immense demand for prolonged shelf-life stability accelerates the utilization of high-performance polyvinylidene chloride barrier films, optimizing the hermetic seal integrity of sensitive solid oral dosages.

- Consequently, operators upgrading to continuous automated blow-molding systems have improved overall production efficiency by 22% while simultaneously lowering energy consumption by 12%. The ongoing transition toward patient-centric unit-dose blister cards ensures exact dosage delivery and minimizes contamination risks.

- This relentless pursuit of absolute biochemical containment directly empowers healthcare providers to safely distribute highly reactive medications globally.

What are the market trends shaping the Pharmaceutical Packaging Industry?

- The accelerated deployment of intelligent connected smart packaging solutions represents a defining trend reshaping modern healthcare distribution. This technological integration transforms passive containers into active digital nodes to enhance patient engagement and supply chain security.

- The integration of digital connectivity and deep-learning visual analytics represents a transformative trend fundamentally altering Pharmaceutical Packaging architecture. As international health authorities mandate comprehensive traceability, packaging facilities are systematically embedding serialization data matrix codes and radio frequency identification tags directly into secondary cartons.

- This data-driven evolution enhances supply chain transparency, improving inventory reconciliation accuracy by 18% over traditional manual barcode scanning. Concurrently, the accelerated commercialization of advanced gene therapies necessitates the deployment of highly specialized cryogenic storage vials capable of maintaining structural integrity at extreme sub-zero temperatures.

- To support these complex biological products, manufacturers are automating sterile fill-finish operations, which has successfully reduced microscopic container defect rates by 25%. Additionally, innovations in transdermal delivery matrices are optimizing patient comfort and controlled drug release, demonstrating how targeted material engineering directly elevates therapeutic delivery and clinical adherence.

What challenges does the Pharmaceutical Packaging Industry face during its growth?

- Striking a viable balance between rigid regulatory sterility standards and increasing legislative pressure for environmental sustainability remains a formidable challenge constraining rapid material innovation.

- Balancing rigid biological sterility mandates with intensifying environmental legislation constitutes a severe operational challenge disrupting standard Pharmaceutical Packaging workflows. Transitioning away from legacy composite plastics toward highly recyclable mono-material blister configurations introduces immense technical friction, often increasing material validation times by 30% due to comprehensive regulatory stability testing requirements. Furthermore, extreme pricing volatility for specialized polymers directly compresses operational margins.

- Manufacturers face substantial difficulties integrating active oxygen scavengers into recycled resin matrices without compromising drug purity. The critical necessity to secure biopharmaceutical cold-chain shippers with precise tamper-evident tear bands and ultra-pure elastomeric vial stoppers adds significant manufacturing complexity.

- Resolving these conflicting priorities frequently elevates baseline production costs by 15%, forcing packaging converters to heavily subsidize advanced material research to prevent widespread commercialization delays.

Exclusive Technavio Analysis on Customer Landscape

The pharmaceutical packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pharmaceutical packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pharmaceutical Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pharmaceutical packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACG Group - Delivers specialized pharmaceutical packaging solutions, including high-barrier blister configurations, flexible sachets, pouches, and sterile medical containment systems designed to ensure drug stability and regulatory compliance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACG Group

- Amcor Plc

- AptarGroup Inc.

- Becton Dickinson and Co.

- Catalent Inc.

- Datwyler Holding Inc.

- Dow Chemical Co.

- Drug Plastics Group

- DS Smith Plc

- DuPont de Nemours Inc.

- Gerresheimer AG

- International Paper Co.

- Jabil Inc.

- KP Holding GmbH and Co. KG

- Perlen Packaging AG

- Smurfit Westrock plc

- Sonoco Products Co.

- Stevanato Group S.p.A

- Vitro SAB De CV

- West Pharma Services Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pharmaceutical packaging market

- In the Metal, Glass and Plastic Containers industry, the accelerated implementation of the European Packaging and Packaging Waste Regulation has mandated a strict circular economy material transition, directly impacting Pharmaceutical Packaging demand by forcing a 40% substitution of multi-layer laminates with recyclable mono-materials to ensure regulatory stability testing compliance while supporting single-use plastic reduction.

- The integration of advanced deep-learning vision systems in primary glass manufacturing has elevated zero-defect manufacturing inspection capabilities, directly impacting Pharmaceutical Packaging by reducing structural anomalies by 25% and enhancing glass delamination prevention for highly sensitive sterile barrier systems.

- The widespread adoption of blockchain-backed serialization protocols across major polymer conversion facilities has established new standards for unit-level electronic traceability, directly impacting Pharmaceutical Packaging demand by requiring the integration of anti-counterfeiting digital watermarks to maintain strict global track-and-trace compliance.

- The deployment of vacuum-insulated panel technology in container logistics has optimized the biopharmaceutical supply chain, directly impacting Pharmaceutical Packaging by improving thermal retention during temperature-controlled transit by 30% and enabling seamless continuous real-time monitoring for high-value injectable therapeutics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pharmaceutical Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.3% |

| Market growth 2026-2030 | USD 91611.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.7% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, Switzerland, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, Turkey, South Africa, UAE, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Pharmaceutical Packaging environment requires unparalleled precision, compelling corporate leadership to align containment strategies directly with stringent therapeutic risk profiles. The industry is experiencing a massive pivot toward biologic drug administration, which fundamentally reshapes procurement and product safety parameters.

- To address the acute sensitivity of large-molecule formulations, operators utilize pre-sterilized ready-to-use nested syringes, effectively streamlining aseptic fill-finish operations and minimizing cross-contamination risks. This specific architectural upgrade enables filling facilities to achieve a 30% reduction in processing time by eliminating intermediate washing and depyrogenation steps.

- Maintaining absolute hermetic seal integrity remains critical for solid oral medications, driving the rapid adoption of advanced unit-dose blister cards optimized for low moisture vapor transmission rate profiles. Packaging engineers continuously leverage multi-layer co-injection techniques to embed active moisture barriers seamlessly into primary structures. Furthermore, the strategic deployment of automated blow-molding equipment ensures high-dimensional uniformity across massive production batches.

- These operational investments secure critical biological stability while allowing pharmaceutical developers to confidently scale up their manufacturing output across highly regulated international distribution networks.

What are the Key Data Covered in this Pharmaceutical Packaging Market Research and Growth Report?

-

What is the expected growth of the Pharmaceutical Packaging Market between 2026 and 2030?

-

USD 91.61 billion, at a CAGR of 10.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Rigid plastic, Flexible plastic, Glass, and Others), Product (Plastic bottles, Caps and closures, Blister packs, Pre-fillable syringes, and Others), Route of Administration (Oral drugs, Injectables, Topical, Nasal, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rapid global expansion of complex biologics and injectable therapeutics, Striking balance between rigid regulatory sterility standards

-

-

Who are the major players in the Pharmaceutical Packaging Market?

-

ACG Group, Amcor Plc, AptarGroup Inc., Becton Dickinson and Co., Catalent Inc., Datwyler Holding Inc., Dow Chemical Co., Drug Plastics Group, DS Smith Plc, DuPont de Nemours Inc., Gerresheimer AG, International Paper Co., Jabil Inc., KP Holding GmbH and Co. KG, Perlen Packaging AG, Smurfit Westrock plc, Sonoco Products Co., Stevanato Group S.p.A, Vitro SAB De CV and West Pharma Services Inc.

-

Market Research Insights

- The Pharmaceutical Packaging framework operates as a critical defense mechanism, ensuring therapeutic efficacy and supply chain transparency. Modern facilities prioritize advanced material science to maintain track-and-trace compliance and safeguard sensitive biologics against external degradation. By optimizing thermal barriers for temperature-controlled transit, manufacturers have improved cold-chain delivery reliability by 22%, significantly reducing the spoilage of high-value vaccines.

- Furthermore, the integration of standardized unit-dose formats supports automated decentralized hospital dispensing, accelerating clinical administration speeds by 15% compared to bulk dispensing methods. Adhering to rigorous regulatory stability testing allows specialized converters to deploy robust primary containers, lowering the incidence of chemical leaching and ensuring that critical drug formulations remain entirely uncompromised throughout extended logistical lifecycles.

We can help! Our analysts can customize this pharmaceutical packaging market research report to meet your requirements.

RIA -

RIA -